Shared Urban Mobility Market Size, Share, Trends, Growth and Forecast 2034

Shared Urban Mobility Market By Service Model (Ride-Hailing, Ride Sharing, Bike Sharing, Car Sharing and Others), By Channel (Online and Offline), By Vehicle (Car, Two-wheelers and Others) and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 345 Billion | USD 1336 Billion | 14.5% | 2024 |

Shared Urban Mobility Industry Perspective:

What will be the size of the global shared urban mobility market during the forecast period?

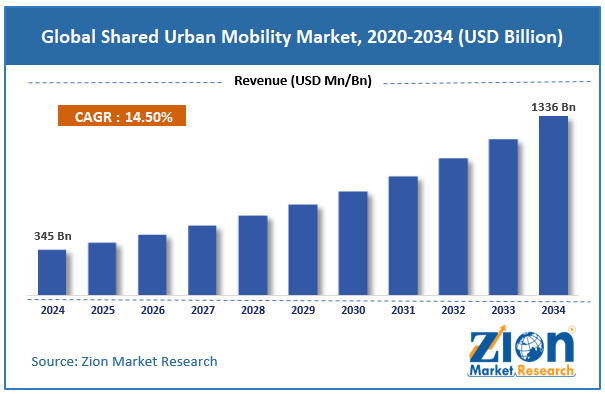

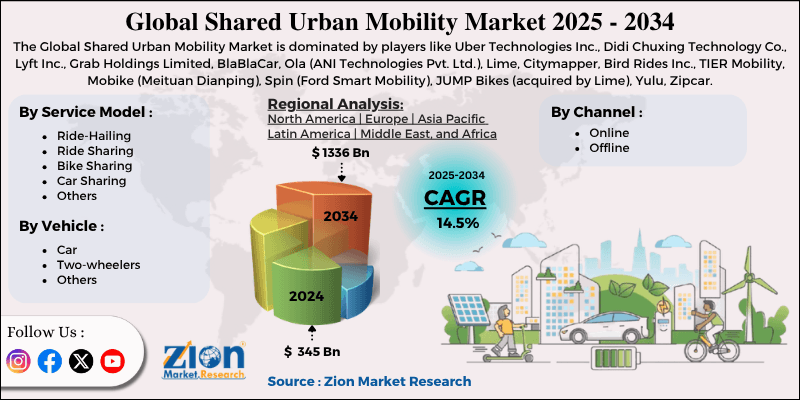

The global shared urban mobility market size was worth around USD 345 billion in 2024 and is predicted to grow to around USD 1336 billion by 2034 with a compound annual growth rate (CAGR) of roughly 14.5% between 2025 and 2034.

Key Insights

- As per the analysis shared by our research analyst, the global shared urban mobility market is estimated to grow annually at a CAGR of around 14.5% over the forecast period (2025-2034).

- In terms of revenue, the global shared urban mobility market size was valued at around USD 345 billion in 2024 and is projected to reach USD 1336 billion by 2034.

- Government support & smart city initiatives are expected to propel the shared urban mobility market over the projected period.

- Based on the service model, the ride-hailing service model segment held the largest market share of 57% in 2024.

- Based on the channel, the online segment captures the largest revenue share in 2024.

- Based on the vehicle, the car segment dominates the market in 2024 of over 80% of revenue share.

- Based on region, the Asia Pacific leads the market with 55% of revenue share in 2024.

Shared Urban Mobility Market: Overview

“Shared Urban Mobility” means the use of mobility services that require sharing vehicles or services among several people, based on demand or subscriptions, whereas conventional mobility services involve the personal ownership of vehicles by individuals. Such services include ride-hailing, carsharing, bikesharing, and micromobility, such as e-scooters. The popularity of the idea of “shared urban mobility” is attributed to companies such as Uber Technologies Inc. and Ola Cabs, which offer on-demand mobility via smartphone applications. Users can track their rides and pay for them using the mobile apps without having cash on hand.

Impact of the USA-Israel War on Iran on the Shared Urban Mobility Market

The current war going on between the USA and Israel against Iran is indirectly affecting the Shared Urban Mobility Market negatively via high fuel prices, economic uncertainty, and logistical disruptions. This war has disrupted oil production, particularly in the Strait of Hormuz, leading to spikes in oil and, by extension, fuel prices worldwide. Fuel prices directly affect the profitability and efficiency of shared urban mobility companies, leading to higher shared transportation rates for consumers. Furthermore, inflation rates, coupled with declining consumer confidence, are discouraging the use of these services.

Shared Urban Mobility Market: Dynamics

Growth Drivers

Why does the rapid urbanization & traffic congestion drive the shared urban mobility market?

Increased rates of urbanization and urban congestion are important structural factors driving the development of the Shared Urban Mobility Market, according to statistics from various governments and institutions. First, the rate of urbanization worldwide has increased dramatically since 1950, when less than 20% of the world's population lived in urban areas. Today, it ranges from 45% to 58%, with projections indicating an increase to 67% by 2050. This represents a huge burden on the transportation systems of urban environments. Second, congestion levels have risen.

For instance, according to INRIX 2025, congestion increased in 88% of U.S. cities, with individuals losing more than 100 hours per year in some cities such as Chicago and New York.

On a global level, the costs of congestion include billions of hours of time spent by individuals and billions of dollars in financial losses for businesses. Third, only 60% of urban residents currently have access to transport services. All these factors contribute to increased pressure on commuters who rely on shared mobility as alternatives to vehicle ownership.

Restraints

Stringent regulatory environment hindering the shared urban mobility industry growth

Regulatory uncertainty also poses a significant barrier to the development of the shared urban mobility market, as various states and countries are continually developing regulations for ride-hailing, car sharing, and micromobility. In this regard, for instance, the regulations governing ride-hailing services in cities like London and New York City include licensing requirements, congestion charges, and compliance requirements. The regulatory uncertainty affects operators such as Uber Technologies Inc.

Additionally, India presents regulatory uncertainties, with varying laws from one state to the next, including fare and license restrictions that affect operators such as Ola Cabs. Furthermore, there have been cases in Europe where certain cities ban electric scooters without prior notice. As a result, there is increased compliance cost, low profitability, and reluctance by other market participants to join the market.

Opportunities

Why does the launch of new platform by the key market players offer a lucrative opportunity for the shared urban mobility market?

The launch of new platform by the key market players are expected to offer a lucrative opportunity to the shared urban mobility market over the projected period. For instance, in September 2025, Hyundai Motor Group (the Group) has unveiled its new public-private partnership initiative, the Next Urban Mobility Alliance (NUMA), aimed at revolutionizing urban transport ecosystems through advanced mobility technologies. This initiative is set to create an ecosystem for developing solutions to societal and environmental problems by promoting mobility innovation and transforming cities into smart cities.

The event took place in the Grand Walkerhill Seoul. At this event, the next phase of Hyundai Motor Group’s initiative was formally announced, with guests including Hee-up Kang, South Korea’s Vice Minister for Transport, and Chang Song, President and Head of the Advanced Vehicle Platform (AVP) Division of Hyundai Motor Group. NUMA was unveiled earlier in March during Hyundai Motor Group's Pleos 25 event.

Challenges

How does the operational & technology challenges pose a significant challenge to the shared urban mobility market?

Operational and technological difficulties may be among the primary impediments to further development and implementation of the shared urban mobility market, as the balance among asset usage, coordination, and digitization is crucial to its successful operation. Firstly, there must always be enough drivers to match the number of vehicles and the number of customers who use such services at any particular moment. Otherwise, inaccurate predictions can delay service delivery, lead to order cancellations, and result in underutilized assets, with negative consequences for users and companies' profit margins.

In addition, in cases of shared micromobility, it is necessary to ensure that vehicle distribution is reasonable, that equipment and batteries are not vandalized, that batteries are adequately charged, and that maintaining a fleet of bikes and scooters is affordable. Secondly, shared mobility needs technological support. It requires efficient route calculation algorithms, high GPS accuracy, proper operation of the cloud computing system, flawless application performance, and appropriate payment methods. The introduction of Mobility-as-a-Service, which creates a single platform to operate various transportation modes, requires additional resources to develop data integration.

Finally, privacy and cybersecurity have become an increasingly important issue within the industry. As platforms grow, more personal information becomes available, and the investment in building robust infrastructure will have to continue. The requirement for new technologies, such as artificial intelligence, electric vehicles, and forecasting tools, increases operating costs.

Shared Urban Mobility Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Shared Urban Mobility Market |

| Market Size in 2024 | USD 345 Billion |

| Market Forecast in 2034 | USD 1336 Billion |

| Growth Rate | CAGR of 14.5% |

| Number of Pages | 227 |

| Key Companies Covered | Uber Technologies Inc., Didi Chuxing Technology Co., Lyft Inc., Grab Holdings Limited, BlaBlaCar, Ola (ANI Technologies Pvt. Ltd.), Lime, Citymapper, Bird Rides Inc., TIER Mobility, Mobike (Meituan Dianping), Spin (Ford Smart Mobility), JUMP Bikes (acquired by Lime), Yulu, Zipcar (acquired by Avis Budget Group), and others. |

| Segments Covered | By Service Model, By Channel, By Vehicle, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Shared Urban Mobility Market: Segmentation

Service Model Insights

Why does the ride-hailing service model dominate the shared urban mobility market?

The ride-hailing service model segment held the largest market share of 57% in 2024. This kind of model links drivers with clients via mobile application platforms. It has become much easier for people to access transportation via the Internet. There are many reasons for the phenomenon's popularity, including the growing number of smartphone owners, the development of sharing economies, and the need for cheap, flexible transport solutions. The convenience of services provided by ride-hailing applications and the ease of price comparison are the main reasons customers love using them.

Ride-hailing services not only provide an affordable means of transportation but also help improve the environment in many cities by alleviating traffic congestion. However, the geographical expansion policies pursued by global ride-hailing companies will create further opportunities for the segment’s growth.

Channel Insights

Why does the online channel capture the largest market share in the shared urban mobility market?

The online segment captures the largest revenue share in 2024. Two key drivers of market growth are the digitization of transport services and the growing use of smartphones worldwide. Apps such as Uber Technologies Inc., Ola Cabs, and Lyft Inc. have transformed the transportation industry by providing easy booking, GPS-based tracking, mobile payments, and personalized services tailored to passenger needs.

Moreover, the benefits of flexible pricing structures, subscription services, and the incorporation of digital wallets would boost consumer adoption. Additionally, advancements in Mobility-as-a-Service and increased connectivity levels in emerging economies would fuel demand for online booking services.

Vehicle Insights

Does car segment dominates the shared urban mobility market?

The car segment dominates the market in 2024 of over 80% of revenue share. Growth in the car segment will be spurred by increasing demand for easy, cost-effective modes of travel, as people seek ways to move away from owning automobiles.

Additionally, the gig economy is growing, making it necessary for people to move around for work. The growing number of electric and hybrid vehicles will support this segment's growth. Several providers in the industry are shifting to electric and hybrid vehicles for their environmental benefits and the potential long-term cost savings from lower maintenance and fuel costs.

Regional Insights

Why does the Asia Pacific lead the shared urban mobility market?

The Asia Pacific leads the market with 55% of revenue share in 2024. The area is home to some of the largest and most rapidly growing cities, and hence, there is an increased need for transportation that is easily accessible and environmentally friendly. The rapid expansion of ride-hailing services in the region, driven by firms like Uber and Grab, has been quite successful, as they provide a more convenient and economical means of transport than conventional taxis. Besides, many firms have diversified their businesses by offering other modes of transport, such as bicycles and car-sharing.

Shared Urban Mobility Market: Competitive Analysis

The global shared urban mobility market is dominated by players like:

- Uber Technologies Inc.

- Didi Chuxing Technology Co.

- Lyft Inc.

- Grab Holdings Limited

- BlaBlaCar

- Ola (ANI Technologies Pvt. Ltd.)

- Lime

- Citymapper

- Bird Rides Inc.

- TIER Mobility

- Mobike (Meituan Dianping)

- Spin (Ford Smart Mobility)

- JUMP Bikes (acquired by Lime)

- Yulu

- Zipcar (acquired by Avis Budget Group)

The global shared urban mobility market is segmented as follows:

By Service Model

- Ride-Hailing

- Ride Sharing

- Bike Sharing

- Car Sharing

- Others

By Channel

- Online

- Offline

By Vehicle

- Car

- Two-wheelers

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table Of Content

Methodology

FrequentlyAsked Questions

“Shared Urban Mobility” means the use of mobility services that require sharing vehicles or services among several people, based on demand or subscriptions, whereas conventional mobility services involve the personal ownership of vehicles by individuals.

Key growth drivers of the Shared Urban Mobility Market include rapid urbanization, rising traffic congestion, increasing smartphone adoption, and the expansion of app-based platforms such as Uber Technologies Inc. and Ola Cabs.

Major challenges restraining the Shared Urban Mobility Market include regulatory uncertainty, high operational and technology costs, infrastructure limitations, and strong competition impacting platforms like Uber Technologies Inc. and Ola Cabs.

Based on the service model, the ride-hailing segment is expected to dominate the shared urban mobility market growth during the projected period.

Emerging trends and innovations in the shared urban mobility market include the rapid adoption of electric and autonomous vehicles, expansion of Mobility-as-a-Service (MaaS) platforms, AI-driven fleet optimization, and the growth of micro-mobility solutions, all aimed at enhancing efficiency, sustainability, and seamless multimodal transportation.

According to the report, the global shared urban mobility market size was worth around USD 345 billion in 2024 and is predicted to grow to around USD 1336 billion by 2034.

The global shared urban mobility market is expected to grow at a CAGR of 14.5% during the forecast period.

The global shared urban mobility industry growth is expected to be led by the Asia Pacific over the forecast period.

The global shared urban mobility market is dominated by players like Uber Technologies Inc., Didi Chuxing Technology Co., Lyft Inc., Grab Holdings Limited, BlaBlaCar, Ola (ANI Technologies Pvt. Ltd.), Lime, Citymapper, Bird Rides, Inc., TIER Mobility, Mobike (Meituan Dianping), Spin (Ford Smart Mobility), JUMP Bikes (acquired by Lime), Yulu and Zipcar (acquired by Avis Budget Group) among others.

The market report covers the geographical market along with a comprehensive competitive landscape analysis. It also includes cash flow analysis, profit ratio analysis, market basket analysis, market attractiveness analysis, sentiment analysis, PESTLE analysis, trend analysis, SWOT analysis, trade area analysis, demand & supply analysis, Porter’s five forces analysis, and value chain analysis.

HappyClients