Hydrogen Combustion Engine Market Size, Share, Trends, Growth 2034

Hydrogen Combustion Engine Market By Technology (Proton Membrane Exchange, Phosphoric Acid Fuel Cell, and Others), By Application (Passenger Vehicle, Ships, Commercial Vehicle, and Others), and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 3.5 Billion | USD 46.4 Billion | 29.5% | 2024 |

Hydrogen Combustion Engine Industry Perspective:

What will be the size of the global hydrogen combustion engine market during the forecast period?

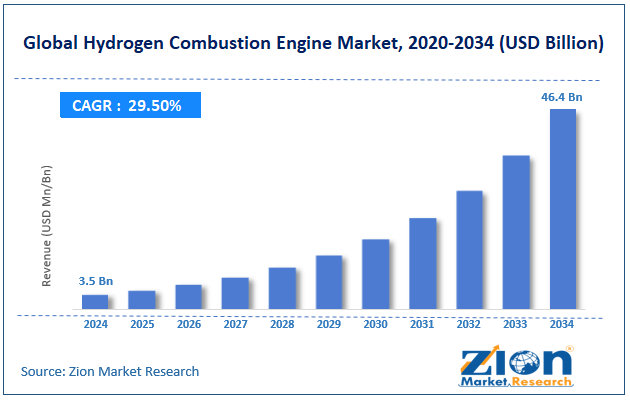

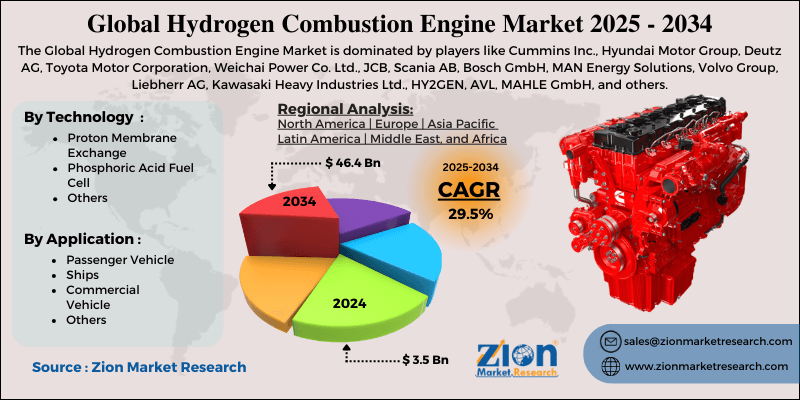

The global hydrogen combustion engine market size was worth around USD 3.5 billion in 2024 and is predicted to grow to around USD 46.4 billion by 2034, with a compound annual growth rate (CAGR) of roughly 29.5% between 2025 and 2034.

Request Free SampleRequest Free Sample

Request Free SampleRequest Free Sample

Key Insights

- As per the analysis shared by our research analyst, the global hydrogen combustion engine market is estimated to grow annually at a CAGR of around 29.5% over the forecast period (2025-2034).

- In terms of revenue, the global hydrogen combustion engine market size was valued at around USD 3.5 billion in 2024 and is projected to reach USD 46.4 billion by 2034.

- Increasing government initiatives for decarbonization are expected to drive the hydrogen combustion engine market.

- Based on the technology, the proton membrane exchange captures the largest revenue share in 2024.

- Based on the application, the commercial vehicle is expected to dominate the industry growth.

- Based on region, the North American region is expected to witness strong growth.

Hydrogen Combustion Engine Market: Overview

A hydrogen combustion engine (H2ICE) is an internal combustion engine that uses hydrogen as the source of energy, rather than more traditional fossil fuels such as gasoline or diesel. It is a mechanically similar engine to a traditional internal combustion engine, with the hydrogen combusted with air inside the cylinders to produce the drive and torque to move, with the emissions from the combustion only Carbon Dioxide (CO₂) (much less than hydrocarbon fuels) and water vapor, although NOx may form during high-temperature combustion. They can be designed as dedicated hydrogen internal combustion engines or converted from automobile gasoline or diesel engines, which makes them attractive options in situations where retaining conventional engine architecture would be advantageous, such as in heavy-duty applications, industrial machines, and marine engines.

Within the hydrogen system, this type of engine is sometimes considered part of the evolution of the hydrogen system as a whole, as a transitional or complementary technology to fuel cells and BEV systems.

Hydrogen Combustion Engine Market: Dynamics

Growth Drivers

How do the stringent emission regulations & decarbonization goals drive the hydrogen combustion engine market growth?

Rigid emission regulations and universally agreed-upon decarbonization targets by the global community are key drivers of the hydrogen combustion engine market, as they pressure both regulators and companies to develop economically viable, environmentally sustainable methods to minimize CO and other pollutant emissions from the transportation and industrial sectors. For instance, the European Green Deal, India's Bharat Stage VI standards, and vehicle fuel-efficiency standards (aligned with the Paris agreement) demand a system that can achieve a drastic reduction in CO emissions while simultaneously meeting other legislated emission standards. This presents a strong motivator for OEMs and fleet operators to concurrently shift from diesel and petrol engines to cleaner options, such as hydrogen combustion engines. A hydrogen combustion engine uses the same basic internal combustion engine design as traditional vehicles while emitting almost zero tailpipe emissions of CO, thus more easily satisfying regulatory obligations without transitioning to battery-electric technology.

Moreover, carbon taxes, emissions trading systems, and government support for hydrogen development make H₂ engines more financially attractive, leading to further proliferation. As the world moves increasingly closer to establishing decarbonization targets, regulatory bodies are further implementing tighter restrictions, encouraging investment into hydrogen infrastructure and the subsequent commercialization of hydrogen engines.

Restraints

Underdeveloped infrastructure for hydrogen is hampering the market expansion

Limited hydrogen infrastructure is a key factor holding back the growth of the hydrogen combustion engine market, as it prevents the general scale-up of adoption of hydrogen-powered products. Unlike fossil fuels such as gasoline and diesel, which are available globally, hydrogen must be produced in industrial settings, stored at high pressure, transported, and used at specialized refueling stations. The number of hydrogen refueling stations is limited in areas where they currently exist, both in absolute numbers and in the context of the population density, and thus it is practically incompatible with the demands of fleet-scale use, whether in terms of driving distance, cargo volume, or duration. Build-out of distributed generation equipment, such as compressors, liquefiers, pipelines, tanks, and dispensing stations, requires significant initial investment, delaying deployment in developing economies. Logistical complications involved in transporting hydrogen as either gaseous compression or cold gas further increase the cost. As existing fueling infrastructure is inadequate, manufacturers and fleet services providers are reluctant to make large investments in fuel cell technology or hydrogen combustion engines. This debate creates what is referred to as a “chicken-and-egg” problem, and it is a factor in the relatively slow growth of the hydrogen combustion engine market.

Opportunities

Does growing investment by the market players in facility expansion offer a potential opportunity for the hydrogen combustion engine market growth?

Market players’ increasing allocation of resources toward facility expansion presents one of the most significant opportunities for the growth of the hydrogen combustion engine market. Building more production facilities, research and development centers, hydrogen fuel system plants, and parts manufacturing units increases the overall ability to supply hydrogen combustion engines and helps bring the technology to market. Setting up more facilities across the PSE map reduces the manufacturing cost of each hydrogen combustion engine through economies of scale, thereby making the technology more price-competitive with diesel engines and ICEs.

For instance, in December 2025, Johnson Matthey (JM) officially opened its first hydrogen internal combustion engine (HICE) facility to evaluate innovative emissions control systems. As a global leader in sustainable technologies, JM has established this new center of excellence to further enhance its world-leading heavy-duty vehicle testing capability. Using zero-carbon hydrogen fuel in well-established engine technology, HICE offers a commercially attractive approach to clear medium- and heavy-duty vehicles, such as trucks and buses, of carbon emissions. The investment increases additional HICE testing capability for JM, the first time that most components can be tested in a full engine. This reinforces their commitment to supporting the dynamic evolution of both the market and regulatory framework in response to this demand in the transport sector.

Challenges

Does the competition from electrification and fuel cells pose a challenge to the hydrogen combustion engine industry's expansion?

The competition from electrification and fuel cell technology remains a key restraining factor on the growth of the hydrogen combustion engine industry. Electric vehicles—namely battery electric vehicles (BEVs) and hydrogen fuel cell electric vehicles (FCEVs)—are often the focus of government policy, funding programs, and infrastructure implementation plans. For instance, Tesla, Inc., quickly moved toward mass commercialization of batteries on a large scale, and major automakers such as Hyundai Motor Company and Toyota Motor Corporation have focused resources on commercializing fuel cell electric technology.

Industry funding and research through these companies have attracted enormous resources, policy incentives, and dedicated programs that help push BEV and FCEV adoption, while potentially leaving hydrogen combustion engine vehicles somewhat less supported. Battery electric vehicle technology has the benefit of a rapidly expanding charging network, falling battery costs, and growing consumer awareness in passenger vehicles. Hydrogen fuel cells will often be viewed as a “zero-emission” alternative to current “combustion” hydrogen engines because they generate power electrochemically, without burning, which eliminates NOx emissions, while H2ICE vehicles potentially still have emissions.

As a result, regulators and environmental agencies may lean toward funding for fuel cells rather than combustion engines in long-term decarbonization pathways. When OEMs are required to divvy up research and development dollars between competing innovations, electric and fuel cell development tends to take priority over hydrogen engine development, and commercialization steps such as scale-up can be slower. However, the momentum behind electrification and fuel cells remains a restraint that can still slow the overall market.

Request Free SampleRequest Free Sample

Request Free SampleRequest Free Sample

Hydrogen Combustion Engine Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Hydrogen Combustion Engine Market |

| Market Size in 2024 | USD 3.5 Billion |

| Market Forecast in 2034 | USD 46.4 Bllion |

| Growth Rate | CAGR of 29.5% |

| Number of Pages | 223 |

| Key Companies Covered | Cummins Inc., Hyundai Motor Group, Deutz AG, Toyota Motor Corporation, Weichai Power Co. Ltd., JCB, Scania AB, Bosch GmbH, MAN Energy Solutions, Volvo Group, Liebherr AG, Kawasaki Heavy Industries Ltd., HY2GEN, AVL, MAHLE GmbH, and others. |

| Segments Covered | By Technology, By Application, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Hydrogen Combustion Engine Market: Segmentation

Technology Insights

Why does proton membrane exchange hold the dominant position in the hydrogen combustion engine market?

The proton membrane exchange captures the largest revenue share in 2024. Hydrogen combustion engine growth in revenue is coincident with further development of Proton Exchange Membrane (PEM) technology, but the two are different technological trajectories. Proton exchange membrane (PEM) systems—most often deployed in Proton Exchange Membrane Fuel Cell applications—have attracted significant policy and capital backing because of their zero tailpipe emissions; larger-scale proton exchange membrane development also expands the capacity and affordability of the hydrogen supply chain, which directly affects the possibility of having affordable, readily available fuel to power combustion engines.

With budgets being made available for hydrogen hubs, electrolyzer facilities, and distribution systems through government funding, corporate stakes, and industry backing, the entire hydrogen economy will become larger. Toyota Motor Corporation and other engine manufacturers are working on both fuel cells and combustion engines, with cross-technology innovation fostering complementary advances in engine and fuel technology, high-pressure systems, and injection systems.

Application Insights

Why does the commercial vehicle hold the largest share in the hydrogen combustion engine industry?

The commercial vehicle is expected to dominate the industry growth. Segment growth is mainly fueled by the necessity to decarbonize heavy-duty transport without compromising vehicle efficiency. Trucks, coaches, and long-haul freight vehicles need to offer high power, long range, and convenient refilling —hydrogen ICE combustion engines have specific technical and economic advantages over battery-electric solutions in these areas. Hydrogen ICE-powered trucks can take advantage of established engine platforms and production value chains, enabling savings for fleets shifting to these vehicles. Leading commercial vehicle manufacturers like MAN Truck & Bus, Volvo Group, and Cummins Inc. have made investments in developing hydrogen-powered engines to comply with increasingly strict emissions regulations and net-zero commitments.

Regional Insights

Why does North America hold the largest share in the hydrogen combustion engine market?

The North American market for hydrogen combustion engines is witnessing significant revenue growth driven by favorable policies, industry decarbonization, and increased spending on hydrogen infrastructure. Programs for greenhouse gas mitigation in the US and Canada—such as cash subsidies for clean hydrogen hubs and incentives for low-carbon heavy-duty transportation—are fostering the transition to hydrogen-based technologies.

In the US, the Department of Energy and the Inflation Reduction Act are endorsing a policy environment that boosts the proliferation of hydrogen generation, storage, and transmission projects, thus indirectly driving the dynamics of the hydrogen combustion engine ecosystem.

Hydrogen Combustion Engine Market: Competitive Analysis

The global hydrogen combustion engine market is dominated by players like:

- Cummins Inc.

- Hyundai Motor Group

- Deutz AG

- Toyota Motor Corporation

- Weichai Power Co. Ltd.

- JCB

- Scania AB

- Bosch GmbH

- MAN Energy Solutions

- Volvo Group

- Liebherr AG

- Kawasaki Heavy Industries Ltd.

- HY2GEN

- AVL

- MAHLE GmbH

The global hydrogen combustion engine market is segmented as follows:

By Technology

- Proton Membrane Exchange

- Phosphoric Acid Fuel Cell

- Others

By Application

- Passenger Vehicle

- Ships

- Commercial Vehicle

- Others

By Region

- North America

- The U.S.

- Canada

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Southeast Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Table Of Content

Methodology

FrequentlyAsked Questions

HappyClients