Carbon Dioxide Removal CDR Market Size, Share, Trends, Growth 2034

Carbon Dioxide Removal CDR Market By Technology (DAC, Bioenergy with CCS, CCS, Soil Carbon Sequestration, and Others), By Application (Industrial, Energy Production, and Agricultural), By End-User (Corporations, Carbon Credit Markets, and Governments), By Deployment Type (Land-Based and Ocean-Based), and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

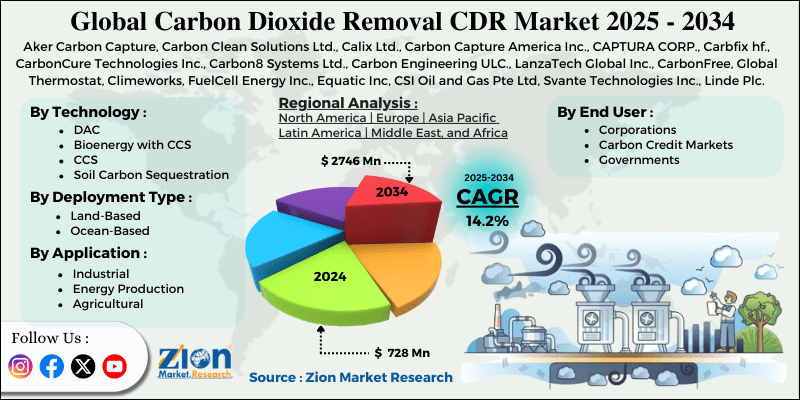

| USD 728 Million | USD 2746 Million | 14.2% | 2024 |

Carbon Dioxide Removal CDR Industry Perspective:

What will be the size of the global carbon dioxide removal market during the forecast period?

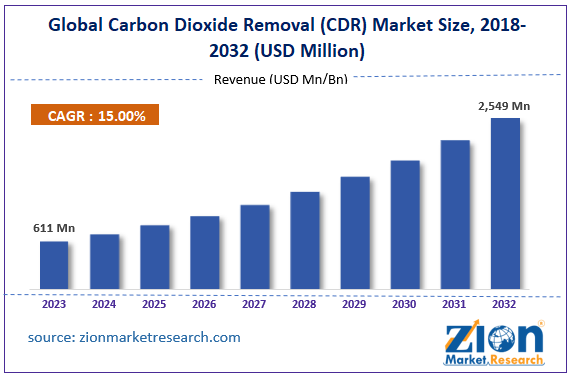

The global carbon dioxide removal CDR market size was worth around USD 728 million in 2024 and is predicted to grow to around USD 2746 million by 2034, with a compound annual growth rate (CAGR) of roughly 14.2% between 2025 and 2034.

Key Insights

- As per the analysis shared by our research analyst, the global Carbon Dioxide Removal CDR market is estimated to grow annually at a CAGR of around 14.2% over the forecast period (2025-2034).

- In terms of revenue, the global Carbon Dioxide Removal CDR market size was valued at around USD 728 million in 2024 and is projected to reach USD 2746 million by 2034.

- Rising government initiatives for net-zero carbon emissions are expected to drive the Carbon Dioxide Removal CDR market over the forecast period.

- Based on the technology, the DAC segment is expected to dominate the market over the projected period.

- Based on the application, the Industrial segment is expected to capture the largest market share over the projected period.

- Based on the end-user, the corporations segment is expected to capture the largest market share over the projected period.

- Based on the deployment type, the land-based segment is expected to capture the largest market share over the projected period.

- Based on region, North America is expected to dominate the market during the forecast period.

Carbon Dioxide Removal CDR Market: Overview

The term Carbon Dioxide Removal CDR encompasses a variety of techniques and natural methods that are intended to remove the gas carbon dioxide (CO₂) from the atmosphere and then store it for very long periods or even forever, thus lowering the total amount of greenhouse gases in the atmosphere. CDR is unlike traditional climate-mitigation approaches that focus solely on reducing emissions at the source; it also addresses residual and even historical emissions that decarbonization cannot fully eliminate. Among the various methods of CDR, some engineered solutions, such as direct air capture with geological storage and bioenergy with carbon capture and storage, are included, as are nature-based approaches like afforestation, soil carbon sequestration, biochar application, and enhanced weathering. Today, these solutions are increasingly viewed as crucial partners in emissions reduction, specifically for achieving net-zero and net-negative emissions targets, stabilizing global temperatures, and reducing the future impacts of climate change.

Carbon Dioxide Removal CDR Market: Dynamics

Growth Drivers

Why do climate policy and regulatory pressures propel the growth of the carbon dioxide removal market?

The Carbon Dioxide Removal CDR market is largely influenced by climate policy and regulatory pressures, as governments are increasingly viewing emission reductions as only one tool to achieve climate goals. The combination of national and regional emissions-neutrality and negativity commitments, aligned with international climate goals, not only encourages policymakers to consider carbon removal as part of the long-term climate strategy but also helps them understand the role of carbon removal in the context of the international climate goals. Governments, through their policies, are creating a need for the removal of CO₂ that is proven to be long-lasting and verifiable, which is done by using regulators' means such as carbon pricing, subsidies, tax credits, and public procurement programs, which in turn are driving investment in both artificial and natural CDR technologies.

Besides, the new regulations on corporate climate emissions reporting and the quality of carbon offsets are tilting the scales toward high-integrity traditional carbon removal credits, thereby expediting market adoption. With the development of regulatory frameworks and their integration of CDR into the compliance and voluntary carbon markets, policy pressure remains the main driver of scaling up deployment and shaping the global Carbon Dioxide Removal CDR market's growth path. For instance, India has set a target to reduce its carbon emissions by 50% by 2030 and achieve net neutrality in the economy by 2070.

Restraints

Does the high cost of technology impede the carbon dioxide removal industry’s growth?

One big reason for the industry's slow growth is the high cost of technology, especially in an innovative, costly sector like the Carbon Dioxide Removal (CDR) market. The main reasons are that such advanced technologies (Direct Air Capture and carbon storage infrastructure) are not commercially feasible at a large scale due to very high initial investments, expensive materials, labor-intensive processes, and ongoing maintenance costs. These costs keep on the minds of buyers who are conscious of prices, and thus they not only slow down project deployment but also increase the financial risks that investors and developers have to bear.

Consequently, market growth often depends on government subsidies, tax incentives, carbon pricing mechanisms, or long-term power purchase agreements just to survive. It will take more time before technological breakthroughs, higher production volumes, and supply-chain improvements reduce costs to the extent that high technological costs are no longer the sole barrier to widespread industry development, and that the initial phases of market development are not the hardest hit.

Opportunities

Will the rising collaboration offer a potential opportunity for the carbon dioxide removal market?

The increasing collaboration is expected to offer a potential opportunity to the Carbon Dioxide Removal CDR market over the projected period. For instance, in April 2024, the launch of the Asia Centre of Carbon Excellence (ACCE) by South Pole and GenZero is a major step toward bringing together international experts who will primarily focus on developing carbon projects, policymaking, and training. The ASEAN nations, with the EDB as a partner, will have access to the latest technical know-how in carbon financing, which will be necessary to challenge existing barriers and unlock new possibilities for climate action across Asia. The ACCE team will pursue carbon project development by collaborating with regional companies and governments, thereby also securing the realization of that market within value chains, not only in Asia but also worldwide. The ACCE team is focused on helping the public and private sectors meet their global net-zero strategies and goals in the most cost-effective manner, thereby speeding up the path towards a green, sustainable future.

Challenges

Policy, regulatory, and standards gaps pose a major challenge to market expansion

The gaps in policy, regulation, and standards have been a significant hurdle to market development, especially in new areas like the Carbon Dioxide Removal (CDR) market, which is now seen as the largest emerging sector. The lack of clear, consistent, and globally harmonized regulations creates uncertainty not only for investors but also for project developers and buyers. It is a case in which market players are under pressure due to higher risks associated with compliance, credibility, and long-term returns, as they are not provided with well-defined policies for deliverable measurements, verifications, credits, and inclusions to national or corporate climate targets.

In addition, fragmented standards for monitoring, reporting, and verification (MRV) pose significant challenges for comparing projects and ensuring their permanence and environmental integrity. This regulatory uncertainty results in longer project approval periods, reduced large-scale investment, and the non-integration of CDR into compliance and voluntary carbon markets. Consequently, the unresolved policy and standards gap continues to undermine market confidence, scalability, and sustained growth.

Carbon Dioxide Removal CDR Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Carbon Dioxide Removal CDR Market |

| Market Size in 2024 | USD 728 Million |

| Market Forecast in 2034 | USD 2746 Million |

| Growth Rate | CAGR of 14.2% |

| Number of Pages | 215 |

| Key Companies Covered | Aker Carbon Capture, Carbon Clean Solutions Ltd., Calix Ltd., Carbon Capture America Inc., CAPTURA CORP., Carbfix hf., CarbonCure Technologies Inc., Carbon8 Systems Ltd., Carbon Engineering ULC., LanzaTech Global Inc., CarbonFree, Global Thermostat, Climeworks, FuelCell Energy Inc., Equatic Inc, CSI Oil and Gas Pte Ltd, Svante Technologies Inc., Linde Plc, Saipem S.p.A., NET Power, Shell plc, and others. |

| Segments Covered | By Technology, By Application, By End User, By Deployment Type, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Carbon Dioxide Removal CDR Market: Segmentation

Technology Insights

The DAC segment is expected to dominate the market over the projected period. The expansion of this segment is largely driven by ongoing advancements in the global chemical industry. Additionally, awareness of the need to reduce CO2 emissions, coupled with advancements in electrochemical processes, is driving market growth. Furthermore, the increase in government funding for the research and development of DAC is likely intended to increase market size.

Application Insights

The industrial segment is expected to grow at a significant rate over the projected period. The main drivers of growth are the rise in industrial demand for long-lasting carbon removal solutions and the incorporation of CDR technologies into industrial processes. The chemical, steel, cement, and manufacturing industries, which are subject to stringent regulatory requirements, are increasingly turning to CDR methods to neutralize their hard-to-abate emissions and fulfill their environmental commitments. This tendency is mirrored in market forecasts that predict the overall CDR market will grow considerably, particularly in the industrial applications sector, as rising emissions drive increased demand and revenue potential.

End-User Insights

The corporation’s segment is expected to grow substantially over the forecast period because businesses are gradually incorporating CDR into their climate strategies for net-zero or carbon-neutral objectives, in response to stakeholder demands. From finance to oil and gas, the carbon neutrality commitment made by corporations is almost a rule. Most of them, however, will not be able to mitigate their emissions or even have a lot of carbon left behind difficult to remove. Thus, they will have no option but to get rid of that carbon through the purchase of long-lasting carbon removal solutions like direct air capture, biochar, etc.

In addition, they might purchase additional carbon credits. These purchase agreements, which can take various forms such as long-term offtake contracts and up-front funding commitments, will guarantee steady income for the CDR project developer/technology provider, thereby accelerating commercial deployment and investment in the sector.

Deployment Type Insights

The land-based segment is expected to grow substantially over the forecast period. Land-based CDR methods — such as afforestation/reforestation, soil carbon sequestration, biochar application, and improved land management practices — capture and store CO₂ in plants and soils, providing one of the cheapest and most scalable ways, alongside some engineered technologies. This has lured revenue from different sources: purchasers in voluntary carbon markets seeking cheap, co-benefit-rich credits; ecosystem restoration for climate resilience funded by governments and public programs; and private investors who see the connection between growing demand and sustainability goals and have thus come to recognize it as a profitable area.

Regional Insights

What factors help North America dominate the Carbon Dioxide Removal CDR market?

North America dominates the carbon dioxide removal market, accounting for more than 55% of revenue in 2024. The main factor driving this increase is the attractive government measures and the backing of regulatory systems, especially in the United States and Canada, that offer incentives, tax credits, and financial support for carbon removal projects, which in turn help to develop long-term revenue streams and thus lower the investment risk for the developers. Moreover, there is significant corporate interest in the North American market for high-quality carbon credit removal, driven by companies pursuing net-zero targets and seeking to strengthen their sustainability profiles, thereby increasing demand and market growth through higher revenue.

North America’s advanced technology providers and startups are another contributor to the growth of the carbon dioxide removal (CDR) market, as they attract more investment and form partnerships that support the scaling up of CDR solutions. The innovation ecosystem in the region, coupled with increasing public-private co-operation, is the basis for diverse CDR methods — from direct air capture to soil and biomass sequestration — to be commercialized, thereby driving overall revenue growth in the North American CDR market.

Carbon Dioxide Removal CDR Market: Competitive Analysis

The global Carbon Dioxide Removal CDR market is dominated by players like:

- Aker Carbon Capture

- Carbon Clean Solutions Ltd.

- Calix Ltd.

- Carbon Capture America Inc.

- CAPTURA CORP.

- Carbfix hf.

- CarbonCure Technologies Inc.

- Carbon8 Systems Ltd.

- Carbon Engineering ULC.

- LanzaTech Global Inc.

- CarbonFree

- Global Thermostat

- Climeworks

- FuelCell Energy Inc.

- Equatic Inc

- CSI Oil and Gas Pte Ltd

- Svante Technologies Inc.

- Linde Plc

- Saipem S.p.A.

- NET Power

- Shell plc

The global Carbon Dioxide Removal CDR market is segmented as follows:

By Technology

- DAC

- Bioenergy with CCS

- CCS

- Soil Carbon Sequestration

- Others

By Application

- Industrial

- Energy Production

- Agricultural

By End User

- Corporations

- Carbon Credit Markets

- Governments

By Deployment Type

- Land-Based

- Ocean-Based

By Region

- North America

- The U.S.

- Canada

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Southeast Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Table Of Content

Methodology

FrequentlyAsked Questions

The term Carbon Dioxide Removal CDR encompasses a variety of techniques and natural methods that are intended to remove the gas carbon dioxide (CO₂) from the atmosphere and then store it for very long periods or even forever, thus lowering the total amount of greenhouse gases in the atmosphere.

The Carbon Dioxide Removal CDR market is driven by a combination of climate urgency, policy support, and rising corporate demand for durable carbon removal solutions. Governments worldwide are implementing stricter climate policies and net-zero commitments, recognizing that emissions reductions alone are insufficient to meet long-term climate goals, which creates direct demand for CDR technologies.

The high cost of CDR technology is hampering the industry's growth.

Based on the technology, the DAC segment is expected to dominate the Carbon Dioxide Removal CDR market growth during the projected period.

The Carbon Dioxide Removal CDR market is rapidly evolving as new technological and commercial innovations expand both the depth and breadth of carbon removal solutions. Advanced engineered methods, such as improved Direct Air Capture (DAC) systems with lower energy needs and integrated electrochemical conversion pathways (e.g., direct air electrowinning), are emerging to reduce costs and improve efficiency.

According to the report, the global Carbon Dioxide Removal CDR market size was worth around USD 728 million in 2024 and is predicted to grow to around USD 2746 million by 2034.

The global Carbon Dioxide Removal CDR market is expected to grow at a CAGR of 14.2% during the forecast period.

The global Carbon Dioxide Removal CDR industry growth is expected to be led by North America over the forecast period.

The global Carbon Dioxide Removal CDR market is dominated by players like Aker Carbon Capture, Carbon Clean Solutions Ltd., Calix Ltd., Carbon Capture America, Inc., CAPTURA CORP., Carbfix hf., CarbonCure Technologies Inc., Carbon8 Systems Ltd., Carbon Engineering ULC., LanzaTech Global Inc., CarbonFree, Global Thermostat, Climeworks, FuelCell Energy Inc., Equatic Inc., CSI Oil and Gas Pte Ltd, Svante Technologies Inc., Linde Plc, Saipem S.p.A., NET Power, and Shell plc, among others.

The carbon dioxide removal market report covers the geographical market along with a comprehensive competitive landscape analysis. It also includes cash flow analysis, profit ratio analysis, market basket analysis, market attractiveness analysis, sentiment analysis, PESTLE analysis, trend analysis, SWOT analysis, trade area analysis, demand & supply analysis, Porter’s five forces analysis, and value chain analysis.

HappyClients