U.S. Freight Brokerage Market Size, Growth, Trends, Forecast 2034

U.S. Freight Brokerage Market By Services (Intermodal, Truckload, and Less than Truckload), By Customer Type (B2B and B2C), By Mode of Transport (Waterways, Roadways, and Others), By Industry Vertical (Retail and E-commerce, Healthcare, Automotive, Manufacturing, and Others) - Country Specific Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

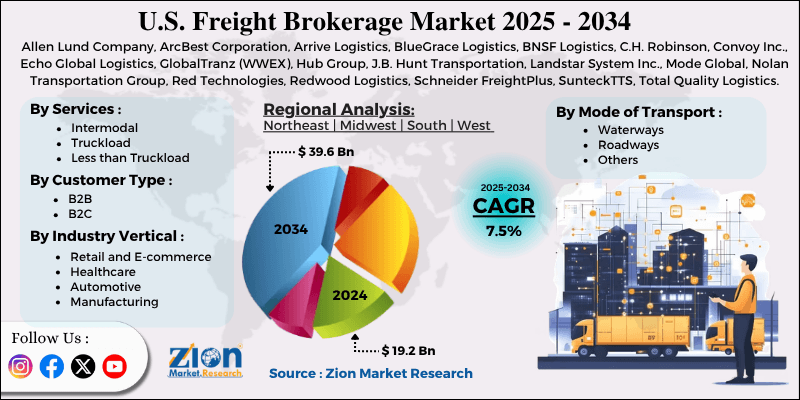

| USD 19.2 Billion | USD 39.6 Billion | 7.5% | 2024 |

U.S. Freight Brokerage Industry Perspective:

What will be the size of the U.S. freight brokerage market during the forecast period?

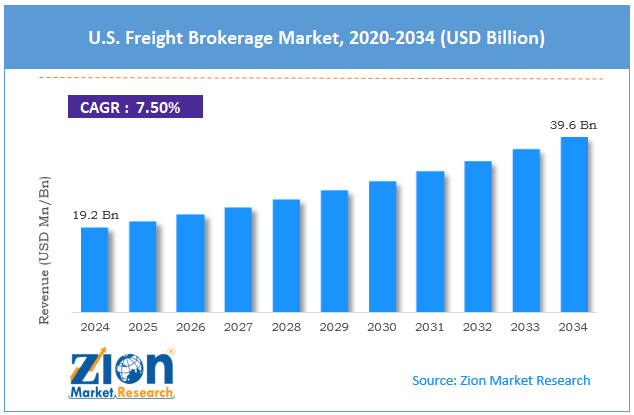

The U.S. freight brokerage market size was worth around USD 19.2 billion in 2024 and is predicted to grow to around USD 39.6 billion by 2034, with a compound annual growth rate (CAGR) of roughly 7.5% between 2025 and 2034.

Key Insights

- As per the analysis shared by our research analyst, the U.S. freight brokerage market is estimated to grow annually at a CAGR of around 7.5% over the forecast period (2025-2034).

- In terms of revenue, the U.S. freight brokerage market size was valued at around USD 19.2 billion in 2024 and is projected to reach USD 39.5 billion by 2034.

- Rapid growth in e-commerce is expected to drive the U.S. freight brokerage market over the forecast period.

- Based on the services, the intermodal segment holds the largest market share over the forecast period.

- Based on the customer type, the B2B segment held the largest revenue share of over 45% in 2024.

- Based on the mode of transport, the roadways segment dominates the market.

- Based on the industry vertical, the manufacturing segment dominates the market.

U.S. Freight Brokerage Market: Overview

Freight brokerage is a type of logistics service in which a licensed third party, called a freight broker, acts as an intermediary to match shippers who need to move freight with motor carriers capable of doing so. Freight brokers are subject to FMCSA jurisdiction and thus require operating authority as well as a BMC-84 trust fund or financial security bond or a BMC-85 trust fund (U.S. Department of Transportation, 2017). Unlike traditional asset-based carriers, freight brokers tend not to own trucks or warehousing as they embrace an asset-light approach to freight movement that encompasses load planning, rate negotiation, carrier logistics, supplier vetting, documentation management, delivery scheduling and tracking, and transport problem resolution (Fogh et al., 2013). Utilizing existing freight network relationships, market data, and trip and real-time data collection to improve their information edge over competitors, modern freight brokers then provide more balanced spanning routes, fewer empty miles, multiple route options, more reliable plan adherence, more flexible asset utilization, and increased services to shippers across FTL, LTL, terminal-to-terminal, intermodal, and specialized freight modes.

U.S. Freight Brokerage Market: Dynamics

Growth Drivers

How do digital transformation and technological adoption drive the U.S. freight brokerage market growth?

Digital transformation and technology adoption are key structural growth drivers of the freight brokerage market, especially in the U.S., where shippers are demanding more technology-enabled services. To keep up with the growing complexity of supply chains and the need for speed, freight brokerages have quickly begun using digital tools like cloud-based Transportation Management Systems (TMS), online freight marketplaces, automated pricing systems, and AI tools for route optimization. These technologies help match trucks faster, provide better visibility, and increase automation.

In some cases, brokerages are using machine learning and AI techniques to power demand forecasting, dynamic pricing, capacity planning, financial fraud detection, and cost projection tools, promoting the use of fewer assets for broader service coverage. Real-time tracking and API integrations with shippers and carriers are also improving transparency and efficiency while reducing delays. Automating freight documentation, billing, and compliance processes is also supporting lower costs and easier scalability.

Digital solutions are now a baseline requirement for a successful freight brokerage—entry barriers are minimal, but returns on digital infrastructure are high, which is why higher competition is requiring more differentiation through sophisticated analytics, visibility, and managed transportation capabilities. As shippers seek improved end-to-end journey visibility, faster ship turnaround times, and operational insights, digital adoption has become less of a differentiating feature and more of a structural growth driver.

Restraints

Regulatory & financial-responsibility rules hamper the industry expansion

Regulatory and financial responsibility requirements can inhibit broker growth, especially among small- to midsize freight brokerage firms. U.S. Freight brokers are monitored by the Federal Motor Carrier Safety Administration and must obtain operating authority, secure either a $75,000 surety bond (BMC-84) or a trust fund (BMC-85), and abide by complex reporting, record-keeping, and financial demands. These financial-security standards place a substantial entry hurdle on new brokers and force existing brokerages to continuously secure liquidity.

Although a broker is not required to put up the full BMC-84 bond amount, the sensitive nature of surety premiums based on a broker’s creditworthiness has a significant impact on a broker’s operating expense. If the broker experiences even slightly diminished creditworthiness, the bonds required to be posted would increase.

Further, brokerage suspension begins upon failure to deposit a bond or upon insufficient financial responsibility. Existing regulations have been issued, and new regulations are emerging that directly impact how brokerage firms must operate in the market. These include matters such as transparency, carrier security, required documentation, and insurance verification. These ongoing regulatory questions increase fixed costs, which hinder profits—and thus the ambitions—of small- and mid-size brokerages.

Opportunities

Why does the increasing number of acquisitions present a potential opportunity for the U.S. freight brokerage industry?

The growing prevalence of deals in the freight brokerage space creates a large growth opportunity for the industry as a whole by improving scale, efficiency, and positioning across the entire space. As the industry shifts toward greater use of technology and a focus on truckloads, companies that can connect the most service providers and customers on a single digital platform are expected to be the most efficient and make the most profit, thanks to their networks and stronger negotiating power with carriers, leading to better prices for shippers.

For instance, in September 2025, Highway, the nation’s leader in Carrier Identity® and broker fraud prevention, announced today that it has acquired freight technology platform Newtrul, Inc. Neutral provides improved carrier matching algorithms along with proven TMS integration skills and will help Highway to develop the industry’s safest and most effective freight exchange.

Challenges

Do the technology investment burden & digital gap pose a significant challenge to the U.S. freight brokerage market development?

The technology investment burden and digital divide present a daunting barrier to the growth of the U.S. freight brokerage market, especially for small and mid-sized brokers. The freight brokerage industry is in the early stages of evolving into a fully digitalized, data-enabled logistics ecosystem. Monitored transportation planning, AI-driven pricing algorithms, integrated real-time tracking systems, fraud detection and prevention, automated carrier onboarding, and APIs to shippers—these are the technology features of modern freight brokerages that generate significant efficiency gains and profit uplift.

But these incredible efficiencies come at a cost: large investments for hardware, software, installation, maintenance, cybersecurity, and IT talent. Smaller brokerages on razor-thin margins cannot stomach the technology investment required to stand up their packages of automation, machine learning, and AI. The stark contrast between large, cash-rich freight brokers deploying advanced analytic and automation platforms and small, cash-conserving catering freight brokers with mid- or no automation steps is creating a digital divide in the industry.

U.S. Freight Brokerage Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | U.S. Freight Brokerage Market |

| Market Size in 2024 | 19.2 Billion |

| Market Forecast in 2034 | 39.6 Billion |

| Growth Rate | CAGR of 7.5% |

| Number of Pages | 225 |

| Key Companies Covered | Allen Lund Company, ArcBest Corporation, Arrive Logistics, BlueGrace Logistics, BNSF Logistics, C.H. Robinson, Convoy Inc., Echo Global Logistics, GlobalTranz (WWEX), Hub Group, J.B. Hunt Transportation, Landstar System Inc., Mode Global, Nolan Transportation Group, Red Technologies, Redwood Logistics, Schneider FreightPlus, SunteckTTS, Total Quality Logistics (TQL), Trinity Logistics, and others. |

| Segments Covered | |

| Regions Covered in U.S. | Northeast, Midwest, South, and West |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

U.S. Freight Brokerage Market: Segmentation

By Services Insights

Why does intermodal hold the dominant position in the U.S. freight brokerage market?

The intermodal segment holds the largest market share over the forecast period. The revenue increase is a reflection of its cost savings, fuel efficiencies, and environmental benefits over long-haul trucking. There has been growing interest in the intermodal marketplace among shippers seeking lower transportation costs for shipments over 700 miles. Rail transportation—in which a train hauls a shipment that is a combination of truck and rail—has benefited from prevailing high diesel prices and trucking capacity shortages, due to its better fuel efficiency per ton-mile relative to over-the-road trucking.

By Customer Type Insights

How is the B2B segment growing significantly in the U.S. freight brokerage industry?

The B2B segment held the largest revenue share of over 45% in 2024. Flexibility in the face of the complexity and international nature of supply chains is also a factor that drives demand from business customers. The convenience of having access to a wide network of carriers who can find the fastest, most cost-effective way to get the consignment from point to point is attractive.

In addition, as global trade continues, B2B customers again turn to freight brokers to guide them through cross-border processes with regard to documentation and compliance. New products and changes in the marketplace increase demand for freight brokers within the business.

By Mode of Transport Insights

Do the roadways dominate the U.S. freight brokerage market?

The roadways segment dominates the market. The growth is driven by homogeneity, the broad presence of brokerage services, and the fact that it is suitable for expedites. The brokerage revenue in the roadway segment increases because trucking is still the prevalent mode of domestic cargo transportation for short- and medium-haul shipments. The U.S. trucking industry is intensely fragmented, comprising thousands of small carriers and independents. This creates a constant demand for brokers, enabling them to pool capacity, negotiate rates, and reliably match loads with shippers.

By Industry Vertical Insights

Does manufacturing dominate the U.S. freight brokerage market?

The manufacturing segment dominates the market. The manufacturing industry is one of the most significant markets for freight brokerage services, due to the benefits these services bring to the manufacturing supply chain. Freight brokers enable manufacturing industries to become more flexible and responsive to changes in production requirements by bridging their needs with the right carriers. It ultimately optimizes logistics solutions and transportation costs for the manufacturing industries. Also, by using information technology, freight brokerages will increase their visibility and responsiveness by tracking and analyzing the entire transportation process.

U.S. Freight Brokerage Market: Competitive Analysis

The U.S. freight brokerage market is dominated by players like:

- Allen Lund Company

- ArcBest Corporation

- Arrive Logistics

- BlueGrace Logistics

- BNSF Logistics

- C.H. Robinson

- Convoy Inc.

- Echo Global Logistics

- GlobalTranz (WWEX)

- Hub Group

- J.B. Hunt Transportation

- Landstar System Inc.

- Mode Global

- Nolan Transportation Group

- Red Technologies

- Redwood Logistics

- Schneider FreightPlus

- SunteckTTS

- Total Quality Logistics (TQL)

- Trinity Logistics

The U.S. freight brokerage market is segmented as follows:

By Services

- Intermodal

- Truckload

- Less than Truckload

By Customer Type

- B2B

- B2C

By Mode of Transport

- Waterways

- Roadways

- Others

By Industry Vertical

- Retail and E-commerce

- Healthcare

- Automotive

- Manufacturing

- Others

By Region

The U.S.

- Northeast

- Midwest

- South

- West

Table Of Content

Methodology

FrequentlyAsked Questions

HappyClients