High-Speed Engine Market Size, Share, Trends, Growth and Forecast 2034

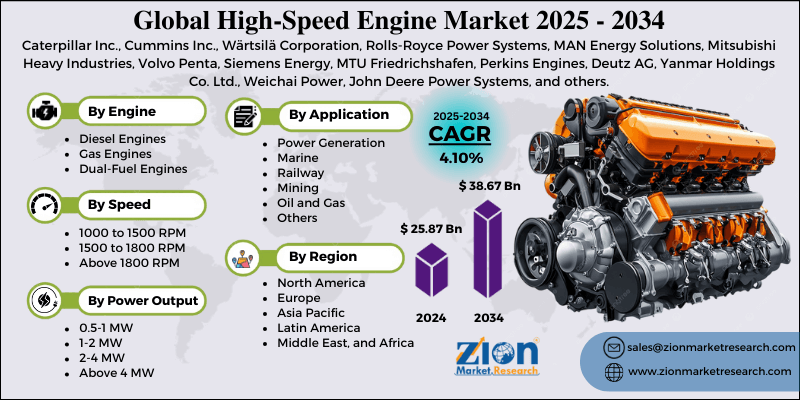

High-Speed Engine Market By Engine Type (Diesel Engines, Gas Engines, and Dual Fuel Engines), By Speed (1000 to 1500 RPM, 1500 to 1800 RPM, and Above 1800 RPM), By Power Output (0.5-1 MW, 1-2 MW, 2-4 MW, and Above 4 MW), By Application (Power Generation, Marine, Railway, Mining, Oil and Gas, and Others), By End User (Industrial, Commercial, and Residential) and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 25.87 Billion | USD 38.67 Billion | 4.10% | 2024 |

High-Speed Engine Industry Perspective:

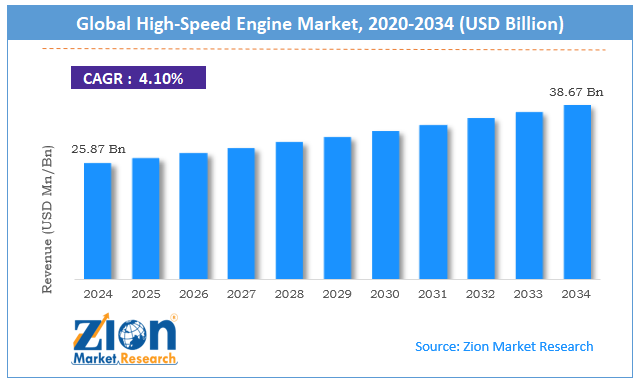

The global high-speed engine market was valued at approximately USD 25.87 billion in 2024 and is expected to reach around USD 38.67 billion by 2034, growing at a compound annual growth rate (CAGR) of roughly 4.10% between 2025 and 2034.

Request Free SampleRequest Free Sample

Request Free SampleRequest Free Sample

High-Speed Engine Market: Overview

High-speed engines are internal combustion engines operating at rotational speeds typically above 1000 RPM, offering compact size, better power-to-weight ratios, and operational flexibility across various industrial applications.

The high-speed engine market serves applications in power generation, marine propulsion, railway traction, mining, and the oil and gas industry. They provide primary power for continuous operation, backup power during outages, and power solutions for remote locations without grid access. High-speed engines range from diesel engines known for reliability and fuel efficiency to gas engines for lower emissions and dual-fuel engines for operational flexibility.

The growth of the high-speed engine industry is driven by increasing demand for distributed power generation, stringent emission regulations promoting cleaner technologies, rising need for reliable backup power systems, and ongoing infrastructure development across emerging economies.

Key Insights:

- As per the analysis shared by our research analyst, the global high-speed engine market is estimated to grow annually at a CAGR of around 4.10% over the forecast period (2025-2034)

- In terms of revenue, the global high-speed engine market size was valued at around USD 25.87 billion in 2024 and is projected to reach USD 38.67 billion by 2034.

- The high-speed engine market is projected to grow significantly due to the rising demand for high-speed engines in marine and defense applications, increasing investment in emergency power solutions for critical infrastructure, and growing use of compact engines in construction and mining equipment.

- Based on engine type, diesel engines lead the market and will continue to lead the global market.

- Based on speed, the 1500 to 1800 RPM segment is expected to lead the market.

- Based on power output, the 1-2 MW segment is expected to lead the market.

- Based on the application, power generation is anticipated to command the largest market share.

- Based on end user, industrial users are expected to lead the market during the forecast period.

- Based on region, Asia Pacific is projected to lead the global market during the forecast period.

High-Speed Engine Market: Growth Drivers

Energy security concerns and distributed power generation

The high-speed engine market is growing fast as concerns about grid reliability and energy security are rising globally. Weather-related outages, aging infrastructure, and lack of grid capacity drive the demand for backup power systems. Post-pandemic industrial recovery has made operational continuity a business imperative.

The distributed generation model, where power is generated closer to the point of consumption, is gaining momentum as organizations seek to reduce their dependence on centralized grids.

High-speed engines are the perfect foundation for these systems, with rapid response, compact installation footprint, and flexible fuel options that fit the distributed generation model for urban and rural applications.

Environmental regulations and technological advancements

Global stringent emission regulations and technological evolution are reshaping the high-speed engine industry. Manufacturers are developing low-emission engines that perform while meeting the rules. Technology has improved fuel efficiency, longer maintenance intervals, and overall engine performance.

The digitalization of engine systems, including integrated monitoring, predictive maintenance, and remote diagnostics, creates premium segments with higher operational efficiency. There is growing interest in hybrid power solutions combining high-speed engines with renewable energy sources and energy storage systems for applications that need reliability and sustainability.

High-Speed Engine Market: Restraints

Alternative power technologies and fuel price volatility

Despite the growth, the high-speed engine industry faces challenges from competing power technologies and economic uncertainty. The rapid adoption of renewable energy technologies, especially solar and wind, with decreasing cost of electricity, is putting pressure on some applications.

Battery storage technology is enabling longer backup times without engine intervention. Initial capital investment for high-speed engine installations is still high compared to some alternatives and affects adoption, especially among price-sensitive customers.

Fuel price volatility creates operational cost uncertainty, especially for diesel engines, making long-term operational expenditure difficult to predict. Some regions still have infrastructure limitations regarding fuel supply logistics and technical expertise for maintenance and operation.

High-Speed Engine Market: Opportunities

Emerging markets and hybrid system integration

The high-speed engine market presents substantial opportunities with expanding geographical reach and evolving system architectures. Rapid industrialization and infrastructure development in emerging Southeast Asia, Africa, and Latin America markets create demand for new centers with huge growth potential. These regions often don’t have reliable grid infrastructure, so high-speed engines are ideal for the power supply.

Hybrid power systems combining high-speed engines with renewable energy sources optimize operational efficiency and reduce environmental impact. There is also interest in alternative fuels like biofuels, hydrogen blends, and synthetic fuels, which can expand the market and address ecological concerns. The demand for modular, containerized power solutions with rapid deployment capabilities is a big opportunity for manufacturers to develop standardized, pre-integrated systems.

High-Speed Engine Market: Challenges

Technical complexity and skills shortage concerns

The high-speed engine industry faces technical requirements and human resource constraints. Engine management systems and emissions control technology are getting more complex.

End users struggle to find technicians with the skills for modern high-speed engines. Technology is moving so fast that manufacturers and service providers struggle to keep up with updated training and technical documentation.

Long lead times and supply chain disruptions still affect product availability and project timelines. The market is fragmented with different application requirements across industries, so we need customized solutions, making standardization harder and potentially more expensive.

Request Free SampleRequest Free Sample

Request Free SampleRequest Free Sample

High-Speed Engine Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | High-Speed Engine Market |

| Market Size in 2024 | USD 25.87 Billion |

| Market Forecast in 2034 | USD 38.67 Billion |

| Growth Rate | CAGR of 4.10% |

| Number of Pages | 212 |

| Key Companies Covered | Caterpillar Inc., Cummins Inc., Wärtsilä Corporation, Rolls-Royce Power Systems, MAN Energy Solutions, Mitsubishi Heavy Industries, Volvo Penta, Siemens Energy, MTU Friedrichshafen, Perkins Engines, Deutz AG, Yanmar Holdings Co. Ltd., Weichai Power, John Deere Power Systems, and others. |

| Segments Covered | By Engine Type, By Speed, By Power Output, By Application, By End User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

High-Speed Engine Market: Segmentation

The global high-speed engine market is segmented into engine type, speed, power output, application, end user, and region.

Based on engine type, the market is segregated into diesel engines, gas engines, and dual-fuel engines. Diesel engines lead the market due to their proven reliability, fuel efficiency, wide operating range, and established service networks across global markets.

Based on speed, the high-speed engine market is categorized into 1000 to 1500 RPM, 1500 to 1800 RPM, and above 1800 RPM. The 1500 to 1800 RPM segment leads the market due to its optimal balance between operational efficiency, maintenance requirements, and power output capabilities across various applications.

Based on power output, the high-speed engine industry is classified into 0.5-1 MW, 1-2 MW, 2-4 MW, and above 4 MW. Of these, the 1-2 MW segment holds the largest market share due to its versatility across multiple applications, optimal balance of power density and fuel efficiency, and suitability for both prime power and backup applications.

Based on application, the market is divided into power generation, marine, railway, mining, oil and gas, and others. Power generation is expected to lead the market during the forecast period due to growing electricity demand, increasing power reliability concerns, and the rising adoption of distributed generation models worldwide.

Based on end users, the market is segmented into industrial, commercial, and residential users. Industrial users lead the market share due to their continuous high power requirements, critical operations necessitating reliable backup systems, and the economic impact of power interruptions on production facilities.

High-Speed Engine Market: Regional Analysis

Asia Pacific to lead the market.

Asia Pacific leads the global high-speed engine market due to rapid industrialization, massive infrastructure development, and increasing power demand in emerging economies.

The region accounts for 42% of the global market share, with China and India being the growth engines. Many countries face power reliability challenges, so the demand for backup and prime power solutions is high.

Manufacturing sector growth and industrial development policies have increased the demand for power sources independent of the grid. Considerable investments in telecommunications, data centers, and regional healthcare facilities require power solutions with zero downtime. Mining, oil and gas, and marine sectors in Asia Pacific are expanding their operations, creating more demand channels for high-speed engines.

Europe is to maintain a significant market presence.

Europe is growing in the high-speed engine industry, characterized by stringent emission regulations, technological leadership, and a strong focus on efficiency and sustainability. Germany, the UK, and Scandinavian countries are the main markets with established industrial bases. The emphasis on environmental compliance has driven the adoption of advanced gas engines and dual-fuel technologies with lower emissions.

Europe’s strong maritime industry means consistent demand for marine propulsion and auxiliary power applications. Europe’s leadership in engine research and development continues to drive global standards.

The growing focus on grid resilience and microgrids, particularly in response to climate-related disruptions, means steady demand for distributed power solutions based on high-speed engines.

Recent Market Developments:

- In January 2025, Deere & Company introduced its advanced JD14 and JD18 marine engines, offering 298 to 599 kW power output for heavy-duty marine applications, marking a key innovation expected to drive high-speed engine market growth.

High-Speed Engine Market: Competitive Analysis

The global high-speed engine market includes diverse manufacturers ranging from large diversified industrial conglomerates to specialized engine producers. Leading players include:

- Caterpillar Inc.

- Cummins Inc.

- Wärtsilä Corporation

- Rolls-Royce Power Systems

- MAN Energy Solutions

- Mitsubishi Heavy Industries

- Volvo Penta

- Siemens Energy

- MTU Friedrichshafen

- Perkins Engines

- Deutz AG

- Yanmar Holdings Co. Ltd.

- Weichai Power

- John Deere Power Systems

The global high-speed engine market is segmented as follows:

By Engine Type

- Diesel Engines

- Gas Engines

- Dual-Fuel Engines

By Speed

- 1000 to 1500 RPM

- 1500 to 1800 RPM

- Above 1800 RPM

By Power Output

- 0.5-1 MW

- 1-2 MW

- 2-4 MW

- Above 4 MW

By Application

- Power Generation

- Marine

- Railway

- Mining

- Oil and Gas

- Others

By End User

- Industrial

- Commercial

- Residential

By Region

- North America

- The U.S.

- Canada

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Southeast Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Table Of Content

Methodology

FrequentlyAsked Questions

High-speed engines are internal combustion engines operating at rotational speeds typically above 1000 RPM, offering compact size, better power-to-weight ratios, and operational flexibility across various industrial applications.

The high-speed engine market is expected to be driven by increasing power reliability concerns, growing distributed generation adoption, stringent emission regulations promoting cleaner technologies, rapid industrialization in emerging economies, and digital integration enhancing operational efficiency.

According to our study, the global high-speed engine market was worth around USD 25.87 billion in 2024 and is predicted to grow to around USD 38.67 billion by 2034.

The CAGR value of the high-speed engine market is expected to be around 4.10% during 2025-2034.

The global high-speed engine market will register the highest growth in the Asia Pacific during the forecast period.

Key players in the high-speed engine market include Caterpillar Inc., Cummins Inc., Wärtsilä Corporation, Rolls-Royce Power Systems, MAN Energy Solutions, Mitsubishi Heavy Industries, Volvo Penta, Siemens Energy, MTU Friedrichshafen, and Deutz AG.

The report comprehensively analyzes the high-speed engine market, including an in-depth discussion of market drivers, restraints, emerging trends, regional dynamics, and future growth opportunities. It also examines competitive dynamics, technological innovations, regulatory impacts, and the evolving customer requirements shaping the industrial power generation landscape.

HappyClients