Headlight Control Module Market Size, Growth, Global Trends, Forecast 2034

Headlight Control Module Market By Module Type (Basic Headlight Control Modules, Adaptive Headlight Control Modules), By Technology (Halogen, LED, Xenon), By Functionality (Automatic Headlight Control, Manual Headlight Control, Daytime Running Light Control, High Beam Assist, Cornering/Bending Light Control, Headlight Levelling), By Vehicle Type (Passenger Vehicles, Light Commercial Vehicles, Medium and Heavy Commercial Vehicles), By Distribution Channel (Original Equipment Manufacturer [OEM], Aftermarket), and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 1,100 Million | USD 1,590 Million | 4.75% | 2024 |

Headlight Control Module Industry Perspective:

What will be the size of the global headlight control module market during the forecast period?

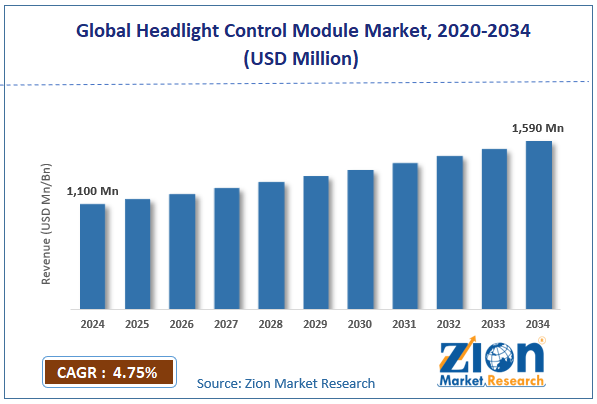

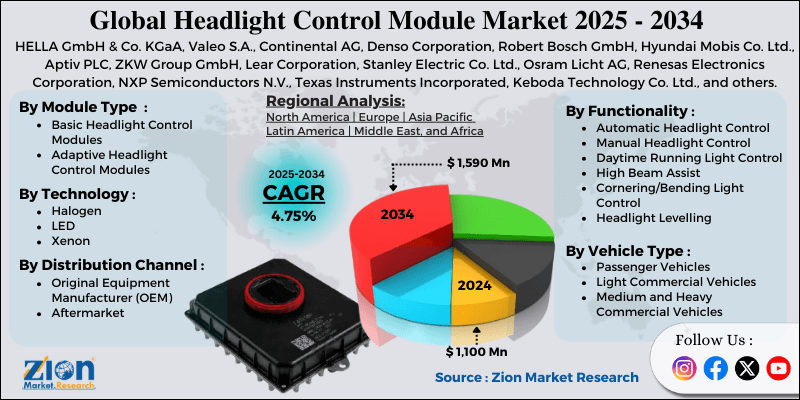

The global headlight control module market size was around USD 1,100 million in 2024 and is projected to reach USD 1,590 million by 2034, with a compound annual growth rate (CAGR) of roughly 4.75% between 2025 and 2034.

Key Insights:

- As per the analysis shared by our research analyst, the global headlight control module market is estimated to grow annually at a CAGR of around 4.75% over the forecast period (2025-2034)

- In terms of revenue, the global headlight control module market size was valued at around USD 1,100 million in 2024 and is projected to reach USD 1,590 million by 2034.

- The headlight control module market is projected to grow significantly owing to the increasing adoption of advanced lighting systems, integration of electronic control units in modern vehicles, and government regulations on automotive safety and lighting.

- Based on module type, the adaptive headlight control modules segment is expected to lead the market, while the basic headlight control modules segment is expected to grow considerably.

- Based on technology, the LED segment is the dominating segment, while the halogen segment is projected to witness sizeable revenue over the forecast period.

- Based on functionality, the high beam assist segment leads the market, while the automatic headlight control segment is anticipated to hold a remarkable share over the forecast period.

- Based on vehicle type, the passenger vehicles segment holds leadership, while the light commercial vehicles segment ranks second in the market.

- Based on distribution channel, the Original Equipment Manufacturer (OEM) segment is expected to lead the market, followed by the aftermarket segment.

- Based on region, the Asia Pacific is projected to dominate the global market during the estimated period, followed by North America.

Headlight Control Module Market: Overview

A headlight control module is an electronic unit in new, advanced vehicles that automatically controls the headlights. It processes inputs from sensors, such as steering angle, vehicle speed, and ambient light, to control functions such as high-beam assist, on/off, and adaptive lighting. The global headlight control module market is likely to expand rapidly, driven by the growing adoption of adaptive lighting systems, the growth of hybrid and electric vehicles, and the increasing integration of automotive electronics. Adaptive lighting systems adjust headlight direction and intensity based on speed, steering, and road conditions. Headlight control modules manage these functions to enhance safety and visibility. Surging demand for advanced driver-assistance features is fueling their adoption.

Moreover, the growth of hybrid and electric vehicles is augmenting the demand for energy-efficient lighting solutions. Headlight control modules optimize power use and integrate with vehicle electronics. Growing EV adoption worldwide supports market growth. Furthermore, modern vehicles use electronic control units to manage multiple functions, comprising lighting. Headlight control modules connect vehicle networks to control performance. This rising integration of automotive electronics is escalating HCM demand.

Nevertheless, the global market faces limitations, including the high cost of advanced lighting systems and the complexity of system integration. Advanced headlight control modules use advanced electronics, software, and sensors, increasing production costs compared to traditional systems. High costs may limit adoption in the economy and budget vehicles. Likewise, incorporating a headlight control module with vehicle electronics and lighting solutions is technically complex. Compatibility issues in diverse platforms may grow, raising engineering costs and development time for producers.

Still, the global headlight control module industry benefits from several favorable factors, including the development of ADAS and autonomous vehicles and the growing aftermarket lighting upgrades. Semi-autonomous and autonomous vehicles depend on smart lighting systems and sensors for navigation and safety. Headlight control modules integrate with radar, cameras, and other ADAS components. The rise of autonomous fueling technologies is creating new market prospects. Additionally, consumers are actively upgrading vehicle lighting for enhanced aesthetics and performance. Advanced headlight control modules allow retrofitting of smart lighting features. This trend expands revenue opportunities for the aftermarket segment.

Growth Drivers

How are stricter safety and glare‑reduction regulations fueling the headlight control module market?

Governments around the world are tightening regulations on nighttime visibility, dynamic beam patterns, and glare mitigation. Compliance mandates compel automakers to adopt automated leveling, glare suppression, and adaptive beam shaping systems. As basic halogen lighting systems become non-compliant, advanced modules gain preference in mainstream automobiles. Regulatory focus on reducing road accidents strengthens investment in smart lighting controls. Hence, HCM adoption is expanding across commercial fleets and passenger cars worldwide, driving the headlight control module market.

How are technological advancements in lighting systems notably fueling growth in the headlight control module market?

Continuous improvements, such as AI-based adaptive beam algorithms, matrix LED arrays, and multi-sensor fusion, expand the capabilities of HCM. Novel modules provide real-time predictive illumination based on speed, navigation, and road curvature data. Tier-1 suppliers are heavily investing in over-the-air updates and software-defined lighting features to stay competitive. These advancements enhance aesthetic appeal and safety, offering automakers better differentiation. As technology progresses, HCMs become central to next-generation vehicle electronics architectures.

Restraints

Compatibility issues with legacy platforms adversely impact the market progress

Retrofitting modern HCMs into older vehicles is technically costly and challenging. Legacy electrical architectures usually lack communication protocols or adequate power capacity. Integration requires redesigning the wiring software and harnesses, increasing development time. OEMs may delay upgrades to avoid platform reengineering. These technical challenges reduce adoption in entry-level and older models. Compatibility barriers hamper HCM market growth.

Opportunities

How is the potential for aftermarket upgrades creating promising avenues for the growth of the headlight control module industry?

Millions of vehicles on the road lack HCMs, creating a large market for retrofits. Aftermarket modules enhance the driver experience and safety without requiring a full vehicle replacement. Service centers and distributors can target suburban and urban consumers seeking advanced features. Kits tailored to be compatible with existing headlights increase adoption. Continuous upgrades extend the module lifecycle. The aftermarket segment offers a major revenue stream, ultimately creating opportunities for the growth of the headlight control module industry.

Challenges

Skilled workforce and knowledge gaps limit the market growth

Designing HCMs need proficiency in embedded systems, software development, and automotive standards. Skilled engineers are scarce, which increases training and recruitment costs. Smaller suppliers struggle to maintain the right talent for research and development and manufacturing, and knowledge gaps may slow product deployment and innovation. Retaining skilled personnel is vital for competitive benefit. Workforce limitations challenge the industry’s technological growth.

Headlight Control Module Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Headlight Control Module Market |

| Market Size in 2024 | USD 1,100 Million |

| Market Forecast in 2034 | USD 1,590 Mllion |

| Growth Rate | CAGR of 4.75% |

| Number of Pages | 221 |

| Key Companies Covered | HELLA GmbH & Co. KGaA, Valeo S.A., Continental AG, Denso Corporation, Robert Bosch GmbH, Hyundai Mobis Co. Ltd., Aptiv PLC, ZKW Group GmbH, Lear Corporation, Stanley Electric Co. Ltd., Osram Licht AG, Renesas Electronics Corporation, NXP Semiconductors N.V., Texas Instruments Incorporated, Keboda Technology Co. Ltd., and others. |

| Segments Covered | By Module Type, By Technology, By Functionality, By Vehicle Type, By Distribution Channel, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 - 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Headlight Control Module Market: Segmentation

The global headlight control module market is segmented based on module type, technology, functionality, vehicle type, distribution channel, and region.

Why is the Adaptive Headlight Control Modules segment projected to dominate the headlight control module market?

Based on module type, the global headlight control module industry is divided into basic headlight control modules and adaptive headlight control modules. The adaptive headlight control modules segment accounts for 58% of the total market share, as they automatically adjust direction and beam intensity based on driving conditions. Their adoption is growing because of integration with ADAS systems and strict safety standards.

On the other hand, the basic headlight control modules segment holds the second-largest market share at 47%. They are widely used in entry-level and cost-sensitive vehicles due to their simplicity and affordability.

What factors are driving the LED segment to lead the headlight control module market?

Based on technology, the global market is segmented into halogen, LED, and xenon. The LED segment dominates the market with a 55% share, driven by its long lifespan, durability, and flexible design. They are broadly used in electric, passenger, and commercial vehicles, signaling strong OEM adoption.

Conversely, the halogen segment ranks second with 35% market share. They are largely used in entry-level and cost-sensitive vehicles. Though less used due to the adoption of LEDs, they remain common for their simplicity and affordability.

What are the reasons for the growth of the High Beam Assist segment in the headlight control module market?

Based on functionality, the global headlight control module market is segmented into automatic headlight control, manual headlight control, daytime running light control, high beam assist, cornering/bending light control, and headlight levelling. The high beam assist segment holds a dominant 29% market share, thanks to its automatic beam switching for improved night-time visibility. It is largely adopted in modern vehicles for safety and convenience.

Nevertheless, the automatic headlight control segment holds a second position with 28% market share. It uses sensors to turn lights off and on based on ambient conditions. Its adoption of stronger, premium, and mid-range vehicles supports driver safety.

Why does the Passenger Vehicles segment hold leadership in the headlight control module market?

Based on vehicle type, the global market is segmented into passenger vehicles, light commercial vehicles, and medium and heavy commercial vehicles. The passenger vehicles segment leads the market with 63% of total market share, driven by high worldwide production and the growing adoption of advanced lighting features.

However, the commercial vehicles segment registers for nearly 24% of the total market, backed by fleet modernization and safety regulations. Demand from the transportation and logistics sectors fuels the segment's dominance.

Which major reasons dominate the Original Equipment Manufacturer (OEM) segment in the headlight control module market?

Based on the distribution channel, the global market is segmented into Original Equipment Manufacturer (OEM) and aftermarket. The OEM segment holds a dominant 91% of the market, as most headlight control modules are factory-installed in new vehicles. They integrate advanced features like adaptive lighting and high-beam assist.

Nonetheless, the aftermarket segment ranks second, offering retrofit and replacement modules for existing vehicles. Demand grows with upgrades to adaptive and LED lighting.

Headlight Control Module Market: Regional Analysis

What gives Asia Pacific a competitive edge in the global Headlight Control Module Market?

Asia Pacific is projected to maintain its dominant position in the global headlight control module market, with a 9-10% CAGR, owing to high automotive production, the growing adoption of advanced lighting technologies, and rising vehicle demand and a middle-class population. APAC leads other regions due to a strong automotive manufacturing base in economies such as India, China, Japan, and South Korea. The region produces a large share of global vehicles, creating consistent demand for headlight control modules used in new-vehicle assembly.

Moreover, automakers in the region are increasingly integrating adaptive, LED, and smart lighting systems into vehicles. These advanced technologies need specialized control modules to manage direction, brightness, and automatic lighting functions, fueling industry growth. Furthermore, rapid urbanization and rising disposable incomes in APAC have increased passenger vehicle ownership. Consumers are purchasing more vehicles equipped with comfort and advanced safety features, which supports higher demand for headlight control modules.

Why does North America rank second in the global Headlight Control Module Market?

North America maintains its position as the second-largest region, with a 7-7.5% CAGR in the global headlight control module industry, driven by strong adoption of advanced automotive technologies, presence of major automotive manufacturers and suppliers, and stringent vehicle safety regulations. North America has a high level of adoption of advanced vehicle technologies, such as automatic lighting systems, adaptive headlights, and ADAS integration. These features require advanced headlight control for proper operation. This strong focus on innovation backs steady market growth. The region is home to many major automotive electronics suppliers and automakers developing advanced lighting solutions. Close collaboration between technology providers and OEMs accelerates innovation. This strong market ecosystem drives industry demand.

Additionally, North America holds stringent vehicle safety regulations that encourage the use of ADAS and advanced lighting. These standards enhance nighttime driving visibility and safety. Hence, the demand for smart headlight control modules continues to grow.

Headlight Control Module Market: Competitive Analysis

The leading players in the global headlight control module market are:

- HELLA GmbH & Co. KGaA

- Valeo S.A.

- Continental AG

- Denso Corporation

- Robert Bosch GmbH

- Hyundai Mobis Co. Ltd.

- Aptiv PLC

- ZKW Group GmbH

- Lear Corporation

- Stanley Electric Co. Ltd.

- Osram Licht AG

- Renesas Electronics Corporation

- NXP Semiconductors N.V.

- Texas Instruments Incorporated

- Keboda Technology Co. Ltd.

What are the key trends in the global Headlight Control Module Market?

Rapid shift toward LED and Matrix LED headlights:

LED-based lighting systems are largely replacing traditional xenon and halogen headlight systems due to their durability, improved efficiency, and design flexibility. Matrix LED technology enables precise control of multiple light segments for adaptive lighting. This shift is fueling the development of more innovative headlight control modules.

Growing demand from electric and software-defined vehicles:

The growth of software-defined vehicle architectures and electric vehicles is creating fresh opportunities for smart lighting control. Modern vehicles need electronic modules capable of advanced processing, energy-efficient lighting management, and connectivity. This shift accelerates innovation in headlight control module technology.

The global headlight control module market is segmented as follows:

By Module Type

- Basic Headlight Control Modules

- Adaptive Headlight Control Modules

By Technology

- Halogen

- LED

- Xenon

By Functionality

- Automatic Headlight Control

- Manual Headlight Control

- Daytime Running Light Control

- High Beam Assist

- Cornering/Bending Light Control

- Headlight Levelling

By Vehicle Type

- Passenger Vehicles

- Light Commercial Vehicles

- Medium and Heavy Commercial Vehicles

By Distribution Channel

- Original Equipment Manufacturer (OEM)

- Aftermarket

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table Of Content

Methodology

FrequentlyAsked Questions

HappyClients