Medical Packaging Market Size, Trend, Growth, Industry Analysis 2034

Medical Packaging Market By Material (Polymer, Paper and Paperboard, Nonwoven Material, Plastic, Glass, Metal, and Others), By Applications (Equipment & Tools, Pharma and Biological, Medical Devices, IVD, and Implants), By Packaging Type (Bags and Pouches, Tube, Sachet, Trays, Boxes, and Others), By Technology (Active Packaging and Smart Packaging), By Distribution Channel (Direct Supply, Distributor Network, and Online Sales), and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

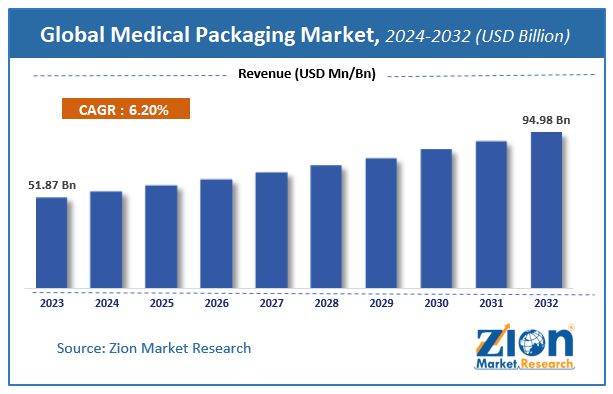

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 62.45 Billion | USD 108.34 Billion | 5.66% | 2024 |

Medical Packaging Industry Perspective:

What will be the global Medical Packaging market size during the forecast period?

The global medical packaging market size was worth around USD 62.45 billion in 2024 and is predicted to reach around USD 108.34 billion by 2034, with a compound annual growth rate (CAGR) of roughly 5.66% between 2025 and 2034. The Medical Packaging Market is driven by the escalating global volume of surgical procedures, rapid technological advancements in single-use medical devices, and strict healthcare regulations aimed at preventing cross-contamination and hospital-acquired infections.

Request Free SampleRequest Free SampleRequest Free Sample

Request Free SampleRequest Free SampleRequest Free Sample

Key Insights

- As per the analysis shared by our research analyst, the Medical Packaging market is projected to expand annually at a CAGR of around 5.66% over the forecast period (2025-2034).

- In terms of revenue, the market size was valued at nearly USD 62.45 billion in 2024 and is anticipated to reach USD 108.34 billion by 2034.

- The market is driven by strict healthcare sector mandates targeting absolute sterility alongside an escalating worldwide consumption of outpatient diagnostic monitoring kits.

- Based on the Material, the Polymer segment dominated the market with a share of over 45% because medical-grade plastics offer unmatched flexibility, superior thermoforming capabilities, and total chemical inertness when exposed to radiation or gas sterilization techniques.

- Based on the Applications, the Medical Devices segment held the largest share of approximately 38% due to the high-frequency production and packaging requirements of daily clinical disposables like syringes, catheters, and intravenous delivery kits.

- Based on the Packaging Type, the Bags and Pouches segment dominated with a share of 42% because these lightweight formats deliver cost-effective microbial isolation, flexible custom scaling, and effortless cleanroom opening mechanisms for surgical teams.

- Based on the Technology, the Active Packaging segment dominated with a share of 65% as moisture-scavenging and gas-barrier layers are structurally essential to safeguard long-term material properties during cross-border transits.

- Based on the Distribution Channel, the Direct Supply segment dominated the market with a share of 55% as large medical institutions prefer long-term procurement agreements directly with original biotechnology manufacturers to secure stable bulk pricing.

- North America dominated the global market with a share of 40% in 2024 due to highly stringent regulatory enforcement by regional health agencies, massive clinical equipment manufacturing infrastructure, and high consumer spending on advanced medical treatments.

Medical Packaging Market: Overview

The medical packaging market encompasses the specialized manufacturing, structural engineering, and commercial supply of protective containment systems designed to maintain the sterility and physical integrity of healthcare supplies from production to application. This critical industrial sector focuses on creating robust microbial barriers that safeguard diagnostic tools, surgical instruments, life-support hardware, and prosthetic implants against moisture, gaseous infiltration, and particulate entry. Utilizing clinical-grade polymers, sterilized fibrous sheets, and custom-formed structural containers, these layouts provide optimized chemical neutrality, clear structural visibility, and advanced tamper-evident features necessary to comply with modern hospital safety standards.

The market dynamics are heavily accelerated by expanding institutional investments in physical clinical networks across emerging economies and private surgical facilities globally. Long-term volume consumption is primarily driven by rising public health spending, expanding elderly populations requiring prolonged clinical care, and a massive shift towards convenient pre-sterilized disposables inside emergency departments. However, unpredictable pricing cycles in raw medical polymers and mounting environmental regulations regarding the disposal of hazardous, single-use clinical materials act as significant structural restraints on profit margins. High-value expansion opportunities are heavily concentrated in the commercialization of bio-based smart packaging systems, while maintaining absolute microbial seal security under extreme transit variations remains a persistent technical challenge for global market participants.

Medical Packaging Market: Dynamics

Growth Drivers

How is the global rise in surgical volume and infection control initiatives driving market growth?

The continuous expansion of public surgical centers, specialized outpatient treatment clinics, and emergency healthcare facilities functions as a primary driver for the global medical packaging sector. As global populations age and suffer from rising rates of chronic conditions such as cardiovascular issues, cancer, and orthopedic damage, the demand for operations increases. To manage high patient footfall safely and lower hospital-acquired infections (HAIs), clinical networks depend on pre-sterilized, single-use medical tool kits. This strict focus on maintaining immediate tool sterility drives consistent high-volume purchase orders for medical-grade packaging materials.

Additionally, standard guidelines implemented by health organizations to enforce clean handling procedures inside medical centers create a reliable secondary growth stream. Governments across developing countries are introducing helpful medical financing plans and updating local healthcare infrastructures to match modern international safety rules. This regulatory update encourages local clinical tool manufacturers to transition away from traditional open-bin tool management to custom primary packaging pouches, boosting retail sales for specialized material formulators globally.

Restraints

What challenges do raw polymer price volatility and environmental plastic disposal regulations pose to the industry?

Unpredictable pricing loops in essential industrial polymer feedstocks, such as polypropylene, high-density polyethylene, and specialized polyester films, present a persistent challenge to steady market expansion. Medical packaging assembly requires specialized, ultra-pure resins to ensure no chemical leaching occurs during high-temperature gas or radiation sterilization steps. Because these high-purity materials are directly derived from crude oil processing, geopolitical conflicts, trade tariffs, and maritime shipping delays can cause sudden spikes in manufacturing expenses. These unpredictable cost increases squeeze structural margins for small-scale suppliers who cannot easily pass the added expense onto large hospital procurement networks.

At the same time, rigid state environmental laws and municipal waste reduction targets place heavy pressure on the use of single-use clinical materials. Because medical packaging frequently comes into contact with human bodily fluids or biological tissue samples, it is classified as bio-hazardous waste after opening, requiring energy-heavy sterilization or secure incineration. Growing public demand for green corporate operations forces medical tool developers to reconsider their bulk plastic consumption, creating a long-term challenge for traditional high-volume packaging suppliers who rely on standard single-use plastics.

Opportunities

Can the engineering of sustainable bio-derived sterile materials unlock new revenue avenues?

Continuous investments in research and development focused on creating high-barrier, bio-sourced polymers and fully recyclable fibrous composites present an exceptional avenue for long-term market value expansion. Advanced material brands are designing innovative packaging sheets from sustainable plant sugars that behave identically to traditional plastics, allowing safe cleanroom sterilization without structural degradation. Successful commercial rollout of these certified green medical coatings enables providers to capture interest from climate-conscious hospital groups, command healthy premium prices, and build an eco-friendly corporate image.

Moreover, the fast rollout of personalized home monitoring kits and customized implant procedures offers excellent potential for structural product expansion. Modern patients are increasingly utilizing advanced in-vitro diagnostic (IVD) setups and self-testing panels at home to check chronic health markers independently, bypassing central labs. Developing custom, user-friendly blister trays and impact-resistant container boxes specifically tailored for direct-to-home clinic shipping lines creates highly profitable niche streams for innovative engineering corporations.

Challenges

How do strict validation protocols and intense competition from cheap regional substitutes challenge operators?

Navigating the exhaustively detailed compliance frameworks and validation protocols enforced by international medical safety board’s remains a severe challenge for chemical converters. Every new medical packaging layout must undergo continuous laboratory shelf-life tests, transport vibration models, and chemical compatibility reviews to verify the microbial seal remains intact over years. These drawn-out verification cycles require substantial capital investments, prolong initial product development timelines, and delay the global market launch of updated packaging formats.

Furthermore, the rapid market expansion of uncertified, lower-tier regional packaging alternatives creates a tough price environment in cost-sensitive developing territories. Local suppliers frequently utilize basic plastic extrusion tools to manufacture low-cost non-sterile bags and standard secondary box containers, selling them at deep discounts to budget-restricted community clinics. To safeguard their corporate positioning, premium global corporations must continuously highlight their certified cleanroom manufacturing setups, superior burst-strength ratings, and traceable quality verification files.

Medical Packaging Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Medical Packaging Market |

| Market Size in 2024 | USD 62.45 Billion |

| Market Forecast in 2034 | USD 108.34 Billion |

| Growth Rate | CAGR of 5.66% |

| Number of Pages | 229 |

| Key Companies Covered | Amcor plc, Berry Global Group Inc., Oliver Healthcare Packaging, Bemis Company, DuPont, WestRock Company, Sealed Air Corporation, Sonoco Products Company, Nelipak Healthcare Packaging, Constantia Flexibles, Technipaq Inc, and others. |

| Segments Covered | By Material, By Applications, By Packaging Type, By Technology, By Distribution Channel, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Market Segmentation

The Medical Packaging market is segmented by material, applications, packaging type, technology, distribution channel, and region.

Based on Material, the medical packaging market is divided into polymer, paper and paperboard, nonwoven material, plastic, glass, metal, and others. The Polymer segment is the most dominant material category within the global market. This leading market position is due to its exceptional clarity, high impact strength, and distinct ability to undergo clean thermoforming processes into custom-fitted protective shapes. This high flexibility allows polymers to support complex clinical instruments effortlessly, driving high volume consumption across the value chain. Pharmaceutical companies rely heavily on this material family for rigid thermoformed components. The second most dominant group is Paper and Paperboard, which remains highly valued for producing porous sterilization wraps and outer secondary shipment boxes due to its lightweight properties and structural recyclability.

Based on Applications, the medical packaging market is divided into equipment & tools, pharma and biological, medical devices, IVD, and implants. The Medical Devices segment acts as the leading application area, holding a major portion of global market revenue. The dominance of this segment is powered by heavy, recurring institutional orders for everyday high-use disposables, such as syringes, needles, catheters, and surgical tubing sets that must be discarded instantly after single patient application. The massive scale of these medical routines allows this application group to act as the primary engine for market volume growth. The second most dominant category is Equipment & Tools, driven by the continuous necessity to package heavy surgical steel sets, endoscopes, and reusable operating room hardware safely.

Based on Packaging Type, the medical packaging market is divided into bags and pouches, tube, sachet, trays, boxes, and others. The Bags and Pouches segment represents the most dominant packaging format globally. Its leading market position is due to the extensive use of lightweight film combinations that offer high cleanroom peelability, low transport weight, and total microbial seal security for surgical accessories. The second most dominant category is Trays, which are heavily utilized by device manufacturers to securely hold heavy orthopedic implants and sensitive cardiovascular tools in fixed geometries during turbulent transcontinental shipping.

Based on Technology, the medical packaging market is divided into active packaging and smart packaging. The Active Packaging segment stands out as the absolute dominant structural configuration within the marketplace. This dominance is driven by the fact that active barriers incorporate moisture absorbers and oxygen scavengers directly within the film layers, serving as an essential requirement to keep long-term clinical materials chemically stable. The second most dominant category is Smart Packaging, which integrates electronic tracking sensors or chemical indicators that alter visual tones when temperature limits are breached during transport.

Based on Distribution Channel, the medical packaging market is divided into direct supply, distributor network, and online sales. The Direct Supply segment is the most dominant distribution channel, as major healthcare systems and nationwide hospital groups enter direct long-term bulk supply agreements with manufacturers to guarantee reliable cartridge delivery schedules. The second most dominant category is Distributor Network, which is heavily relied upon to manage local distribution, inventory supply, and technical assistance across decentralized rural clinics.

Regional Analysis

Why will North America continue to dominate the global market during the projection period?

North America is projected to maintain its leading position in the global Medical Packaging market through the forecast period, supported by strict regional health mandates and an extensive medical device manufacturing cluster. The region's dominance is primarily driven by the United States, where rigid safety rules enforced by food and drug administration’s mandate clear validation records for cleanroom packaging materials, keeping premium product demand exceptionally high.

Additionally, strong investments into advanced biological implants and the quick integration of smart digital tracking labels across clinical supply channels support steady market growth. The region's healthy disposable incomes and well-established clinical insurance networks also encourage regular upgrades to high-barrier medical packaging configurations.

The Asia-Pacific region is anticipated to experience the highest growth rate during the forecast period. Countries like China and India are undergoing massive healthcare transformations, with state departments focusing heavily on expanding local public hospital networks and modernizing medical manufacturing zones. The rapid growth of regional middle-class demographics, combined with increasing public investments in bio-pharmaceutical research, drives high demand for precision sterile consumables.

Moreover, rising funding aimed at tracking local infectious diseases and scaling out neighborhood diagnostic pharmacies creates immense demand for lightweight, low-cost primary pouches and diagnostic trays. The entry of major global medical packaging corporations and the rapid setup of advanced automated cleanrooms across regional chemical corridors further accelerate the regional market's expansion.

Recent Developments

- In January 2026, Amcor plc completed the strategic acquisition of a specialized medical film converter to increase its production capacity for high-barrier thermoformed trays across European clinical hubs.

- In October 2025, Berry Global Group announced a substantial investment in setting up a new advanced cleanroom facility dedicated entirely to producing sustainable, bio-based medical pouches for device manufacturers.

- In April 2026, Oliver Healthcare Packaging introduced a new line of fully eco-certified, high-porosity sterilization lids featuring advanced visual indicators that change color when optimal sterilization gas exposure is achieved.

Competitive Analysis

The global Medical Packaging market is dominated by players:

- Amcor plc

- Berry Global Group, Inc.

- Oliver Healthcare Packaging

- Bemis Company, Inc. (Amcor)

- DuPont (Tyvek)

- WestRock Company

- Sealed Air Corporation

- Sonoco Products Company

- Nelipak Healthcare Packaging

- Constantia Flexibles

- Technipaq, Inc.

What are the key trends in the Medical Packaging Market?

The Rising Proliferation of Smart Interactive Temperature-Tracking Labels

A major trend impacting the market is the integration of smart visual indicators and radio-frequency tracking sensors onto primary medical packaging. Modern manufacturers are actively applying thin digital tags that continuously check temperature variations during shipping, alerting hospital staff instantly if sensitive diagnostic chemicals or biological implants have been exposed to degrading environmental heat.

The Rapid Transition Toward Mono-Material Recyclable Formats

Modern chemical conversion plants are changing fast due to the development of high-performance mono-material medical pouches. This design trend involves creating both the flexible base tray and the top sealing film from identical polymer families, allowing hospitals to discard the waste directly into standard polymer recycling lines without manual material separation.

The global Medical Packaging market is segmented as follows:

By Material

- Polymer

- Paper and Paperboard

- Nonwoven Material

- Plastic

- Glass

- Metal

- Others

By Applications

- Equipment & Tools

- Pharma and Biological

- Medical Devices

- IVD

- Implants

By Packaging Type

- Bags and Pouches

- Tube

- Sachet

- Trays

- Boxes

- Others

By Technology

- Active Packaging

- Smart Packaging

By Distribution Channel

- Direct Supply

- Distributor Network

- Online Sales

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table Of Content

Methodology

FrequentlyAsked Questions

Medical Packaging refers to specialized containment structures manufactured from clinical-grade polymers, sterile papers, or nonwoven materials designed to preserve the absolute sterility and structural performance of healthcare equipment from factory production to surgical use.

The primary growth drivers include expanding worldwide surgical procedure volumes, strict international regulatory mandates regarding hospital infection controls, rapid technological updates in single-use device lines, and the growing public adoption of home-based diagnostic kits.

The global market size was valued at approximately USD 62.45 billion in 2024 and is projected to reach around USD 108.34 billion by the end of 2034.

The global Medical Packaging market is expected to grow at a compound annual growth rate (CAGR) of approximately 5.66% during the forecast period from 2025 to 2034.

Key challenges include unpredictable cost volatility in medical-grade plastic resins, increasing regulatory pressures regarding single-use plastic waste disposal, strict purity demands to avoid chemical leaching, and competition from low-cost generic brands.

Emerging trends highlight the application of smart temperature-tracking digital labels, the structural shift toward mono-material recyclable plastic designs, the use of bio-sourced plant resins, and custom impact trays built for direct-to-home diagnostics.

The value chain includes raw polymer and specialized paper substrate sourcing, cleanroom injection molding and film extrusion, sterile package conversion, medical device assembly and product sterilization, wholesale distribution, and final hospital utilization.

North America will continue to contribute a major share of overall market value due to its mature healthcare financing infrastructure, while the Asia-Pacific region is anticipated to achieve the fastest growth rate.

Amcor plc, Berry Global Group, Inc., Oliver Healthcare Packaging, Bemis Company, DuPont, WestRock Company, Sealed Air Corporation, Sonoco Products Company, Nelipak Healthcare Packaging, Constantia Flexibles, and Technipaq, Inc.

The report delivers comprehensive projections on revenue metrics, deep assessments of market drivers and restraints, structural segment breakdowns, regional competitive landscape maps, and clear guidance on shifting material development pathways.

HappyClients