Can Coatings Market Size, Share, Growth, Opportunities 2034

Can Coatings Market By Type (Two-Piece Cans, Aerosol Cans, Three-Piece Cans, and Closures), By Resin Type (Polyester, Polyurethane, Epoxy, Acrylic, and Polyvinylidene chloride (PVDC)), By Application (Food Beverages, Pharmaceuticals, Household Products, Personal Care Cosmetics, and Industrial Products), and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2026 - 2034

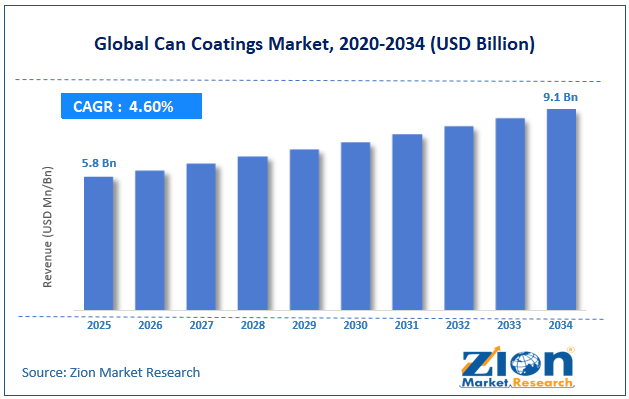

| Market Size in 2025 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 5.8 Billion | USD 9.1 Billion | 4.6% | 2025 |

Can Coatings Industry Perspective:

What will be the size of the global can coatings market during the forecast period?

The global can coatings market size was worth around USD 5.8 billion in 2025 and is predicted to grow to around USD 9.1 billion by 2034, with a compound annual growth rate (CAGR) of roughly 4.6% between 2026 and 2034.

Request Free SampleRequest Free Sample

Request Free SampleRequest Free Sample

Key Insights

- As per the analysis shared by our research analyst, the global can coatings market is estimated to grow annually at a CAGR of around 4.6% over the forecast period (2026-2034).

- In terms of revenue, the global can coatings market size was valued at around USD 5.8 billion in 2025 and is projected to reach USD 9.1 billion by 2034.

- Increasing preference for lightweight aluminum cans is expected to propel the can coatings market over the projected period.

- Based on the type, the two-piece cans are expected to capture the largest market share over the projected period.

- Based on the resin type, the acrylic segment held a prominent market share of 48% in 2025.

- Based on the application, the food & beverages segment held the largest revenue share of 68% in 2025.

- Based on region, the Asia Pacific leads the can coatings market in terms of revenue, which is around 39% of the global market.

Can Coatings Market: Overview

Can coatings are specialized protective internal and external layers applied to metal packaging, including food, beverage, and aerosol cans, to separate the metal container from its contents and the surrounding environment. Typically formulated from polymeric materials such as epoxies, polyesters, acrylics, or vinyls, these thin coatings serve two essential functions: they prevent the packaged contents—particularly acidic or otherwise corrosive products—from attacking the metal substrate, and they protect the contents from metal-induced contamination, off-flavors, discoloration, or spoilage. Applied uniformly throughout the can manufacturing process, these coatings are engineered to withstand demanding conditions, including mechanical forming, filling, sterilization, and long-term storage, thereby ensuring product safety, packaging integrity, corrosion resistance, and extended shelf life.

Impact of the USA-Israel War on Iran on the Can Coatings Market

The concerted military action taken by both the U.S. and Israel against Iran, followed by the increased conflict in the Middle East, has caused serious shock waves to ripple through global supply chains of chemicals and packaging. The coating of cans industry, which is highly dependent on specialty chemicals and other raw materials, has been particularly affected.

Can Coatings Market: Dynamics

Growth Drivers

Why does the growing demand for canned food and beverages drive the growth of the can coatings market?

Increasing consumption of canned food products and beverages is among the most significant growth drivers for the Can Coatings Market, as each metal can needs to have coatings both inside and outside in order to safeguard the pack against corrosion, avoid any chemical reaction between the metal and the product, and retain the flavor, color, and nutrients of the contents. With the increasing consumption of canned beverages, ready-to-eat products, pet food, fruits and vegetables, fish, and soups, manufacturers are producing more and more aluminum and steel cans, which, in turn, increases the consumption of can coatings such as epoxy, polyester, acrylic, and BPA-NI coatings.

For instance, Ball Corporation, which is among the leading aluminum beverage can manufacturers in the world, decided to invest $60 million into expanding its factory in Sri City, India, after noticing the potential for rapid growth of the Indian beverage can market with the yearly growth rate of more than 10%, driven by the increasing consumption of ready-to-drink beverages and dairy beverages, and consumers' preference for sustainable packaging.

Restraints

Why do stringent regulations on BPA-based coatings hamper the growth of the can coatings industry?

Stringent regulatory requirements for BPA-based coatings are hindering the expansion of the can coatings market due to high product development costs, extended approval timelines, and increased manufacturing costs. BPA-based epoxy coatings have always been popular for food and beverage applications due to their high corrosion protection, resistance to food-metal interactions, and food protection. Nonetheless, increased concern about the negative impact of BPA migration into food has led to strict regulatory requirements on the use of BPA in food contact packaging.

Consequently, producers have to develop BPA-free and BPA non-intent (BPA-NI) products that are comparable to BPA-based products in terms of performance, but doing so requires expensive toxicological evaluations, migration testing, and customer qualification, which is a lengthy process. Moreover, alternative chemistry requires more expensive materials and sometimes necessitates manufacturing changes, thereby increasing costs for producers. Although such regulations encourage companies to produce safe, environmentally friendly packaging in the long term, in the short term, they pose financial and technological barriers to product commercialization and the growth of the overall market.

Opportunities

Why does the growing product launch offer a lucrative opportunity for the can coatings market?

Rising product launches are likely to create a lucrative opportunity for the Can Coatings Market, as they enable manufacturers to comply with evolving food safety regulations, achieve sustainability goals, and meet the growing demand for high-performance metal packaging solutions. With regulatory bans on BPA-based coatings and on beverages packaged in recyclable aluminum, coating suppliers are developing advanced, non-BPA, non-PFAS, waterborne, low-VOC coating systems that offer superior corrosion protection and food safety. Such product innovations not only differentiate the supplier’s product portfolio but also help the supplier venture into new packaging applications and replace conventional coating systems.

One such instance is PPG Industries' product launch of PPG HOBA® Pro 2848 at Paris Packaging Week in February 2025. The firm has expanded its range of non-BPA HOBA® internal coatings for aluminum bottles used to package water, wine, beer, pharmaceuticals, food, and personal care products. The PPG HOBA® Pro 2848 coating system is non-BPA, PFAS-NI, and phenolic-free. In addition, the product was honored in the 2025 ADF Innovation Awards.

Following an innovation strategy, PPG Industries further expanded its packaging coatings portfolio in July 2025 by launching three new BPA-NI beverage can end coatings, namely PPG INNOVEL® PRO 2489, PPG INNOVEL® EVO 6720, and PPG iSENSE® 5018. These coatings are suitable for aluminum beverage can ends, ensure high-speed processing, maintain beverage quality (taste and shelf life), and comply with changing food contact regulations worldwide by avoiding the use of BPA and PFAS. According to PPG Industries, the newly launched coatings increase efficiency in manufacturing processes. Moreover, PPG INNOVEL® PRO 2489 has reduced film weight, which is expected to reduce carbon emissions up to 20%.

Challenges

Increasing competition from alternative packaging materials poses a significant challenge to the can coatings market

Increasing competitive pressure from alternative packaging materials is a major obstacle to the development of the can coatings market, owing to declining demand for metal cans, a principal application segment for can coatings. Packaging materials such as flexible plastic pouches, multi-layer cartons, PET bottles, glass packaging, and paper packaging are gradually gaining popularity among food, beverage, and personal care companies on account of their lightweight features, lower shipping costs, design flexibility, and, in some cases, lower packaging costs.

For products like juice, dairy drinks, sauces, snacks, and household goods, these alternatives offer greater convenience and cost-effectiveness than metal cans. As brand owners adopt different packaging forms to meet ever-changing consumer requirements and sustainability factors, the number of steel and aluminum cans required for certain product types will decrease, directly affecting demand for internal and external can coatings. In addition, innovations in recyclable plastics, fiber-based packaging materials, and aseptic cartons intensify competition, forcing can coatings producers to develop new coating technologies to compete successfully.

Can Coatings Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Can Coatings Market |

| Market Size in 2025 | USD 5.8 Billion |

| Market Forecast in 2034 | USD 9.1 Billion |

| Growth Rate | CAGR of 4.6% |

| Number of Pages | 225 |

| Key Companies Covered | Akzo Nobel N.V., Eastman Chemical Company, IPC GmbH & Co. KG, Axalta Coating Systems, National Paints Factories Co. Ltd., Kupsa Coatings, RPM International Inc., VPL Coatings GmbH & Co KG, Kansai Paint Co. Ltd, TIGER Coatings GmbH & Co. KG, PPG Industries Inc., TOYOCHEM CO. LTD., The Sherwin-Williams Company, Berger Paints India, Evonik, Elementis PLC, artience Co. Ltd., Sumitomo Bakelite Co. Ltd., Hannecard Roller Coatings Inc, ASB Industries, Covestro AG, and others. |

| Segments Covered | By Type, By Resin Type, By Application, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 to 2024 |

| Forecast Year | 2026 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Can Coatings Market: Segmentation

Type Insights

Why does the two-piece can segment dominate the can coatings market?

The two-piece cans are expected to capture the largest share of the can coatings market over the projected period. This rise is attributed to the extensive use of two-piece cans in the beverage industry and to their increased use in the packaging of food products. Two-piece cans, which consist of a body and a lid with a sealed base, need to be coated inside and out due to their sensitivity to corrosion and potential reactions between the metal and the packed products. The lightweight, low-material-use design makes two-piece cans the ideal form of packaging for carbonated soft drinks, beer, energy drinks, sparkling water, ready-to-drink coffee and tea, and an increasing number of canned foods.

Resin Type Insights

How does the acrylic segment capture the largest share in the can coatings market?

The acrylic segment held a 48% share of the can coatings industry in 2025. This can be attributed to its improved performance, which makes it the best option for many uses. The coating made with acrylics is highly resistant to corrosion, chemicals, and ultraviolet rays, offering high durability for cans used for food and drink, as well as for industrial products. The coating's clear, glossy finish makes the cans more appealing to customers.

Application Insights

Does the food & beverages segment capture the largest share of the can coatings market?

The food & beverages segment held the largest revenue share, at 68%, in the can coatings market in 2025. This trend is driven by the growing consumption of packaged foods and canned drinks worldwide. Coatings that provide good corrosion resistance and maintain the taste and nutritional value of food products packed in metal cans are required. Metal cans are needed for packaging carbonated soft drinks, beer, energy drinks, ready-to-drink coffee and tea, soups, fruits, vegetables, seafood, pet food, and baby food, among others. Urbanization and changes in lifestyle have increased the use of metal cans coated with protective layers.

Regional Insights

Why does Asia Pacific lead the global can coatings market?

The Asia Pacific leads the can coatings market in terms of revenue, which is around 39% of the global market due to factors such as rapid urbanization, increased disposable incomes, the development of food and beverage processing industries, and the growing acceptance of sustainable metal packaging in China, India, Japan, and Southeast Asia. The region has developed into a major manufacturing center for canned beverages, processed foods, and aerosols, leading to strong demand for high-end coatings on both the internal and external surfaces of cans. The government's efforts to develop the food processing, recycling, and sustainable packaging industries are helping accelerate the use of aluminum and steel cans, which require sophisticated BPA-NI and low-VOC coating technologies. With continued expansion in beverage production capacity and increasing consumer demand for convenience and shelf-stable packaged products, there will be steady demand for can coatings in the Asia Pacific region.

The trends are backed by government figures. According to data from the Ministry of Food Processing Industries of India, the country's alcoholic beverage industry was worth around USD 39.3 billion in 2024, and its non-alcoholic beverage market stood at around USD 30.85 billion in 2023. The growth of industries is increasing the production of aluminum and steel beverage cans, thereby increasing demand for food-contact can coatings.

Moreover, efforts in the region's circular economy have also contributed to increased demand for metal packaging. One such example is China's aluminum beverage can recycling system, which is among the most sophisticated in the world, according to the International Aluminum Institute, with an approximate 95% separation rate for aluminum beverage cans.

Can Coatings Market: Competitive Analysis

The global can coatings market is dominated by players like:

- Akzo Nobel N.V.

- Eastman Chemical Company

- IPC GmbH & Co. KG

- Axalta Coating Systems

- National Paints Factories Co. Ltd.

- Kupsa Coatings

- RPM International Inc.

- VPL Coatings GmbH & Co KG

- Kansai Paint Co. Ltd

- TIGER Coatings GmbH & Co. KG

- PPG Industries Inc.

- TOYOCHEM CO. LTD.

- The Sherwin-Williams Company

- Berger Paints India

- Evonik

- Elementis PLC

- artience Co. Ltd.

- Sumitomo Bakelite Co. Ltd.

- Hannecard Roller Coatings Inc

- ASB Industries

- Covestro AG

The global can coatings market is segmented as follows:

By Type

- Two-Piece Cans

- Aerosol Cans

- Three-Piece Cans

- Closures

By Resin Type

- Polyester

- Polyurethane

- Epoxy

- Acrylic

- Polyvinylidene chloride (PVDC)

By Application

- Food Beverages

- Pharmaceuticals

- Household Products

- Personal Care Cosmetics

- Industrial Products

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table Of Content

Methodology

FrequentlyAsked Questions

Can coatings be specialized protective internal and external layers applied to metal packaging, including food, beverage, and aerosol cans, to separate the metal container from its contents and the surrounding environment.

Increasing consumption of ready-to-eat meals, canned fruits and vegetables, soups, seafood, pet food, and beverages is driving higher production of metal cans, boosting demand for protective can coatings.

The growing adoption of flexible packaging, PET bottles, glass containers, cartons, and paper-based packaging reduces demand for metal cans in several food and beverage applications, limiting the need for can coatings.

Based on the resin type, the acrylic segment is expected to dominate the can coatings market growth during the projected period.

Manufacturers are increasingly developing BPA non-intent (BPA-NI) and BPA-free coating systems to comply with evolving food safety regulations and meet consumer demand for safer food-contact packaging.

According to the report, the global can coatings market size was worth around USD 5.8 billion in 2025 and is predicted to grow to around USD 9.1 billion by 2034.

The global can coatings market is expected to grow at a CAGR of 4.6% during the forecast period.

The global can coatings industry growth is expected to be led by the Asia Pacific over the forecast period.

The global can coatings market is dominated by players like Akzo Nobel N.V., Eastman Chemical Company, IPC GmbH & Co. KG, Axalta Coating Systems, National Paints Factories Co. Ltd., Kupsa Coatings, RPM International Inc., VPL Coatings GmbH & Co KG, Kansai Paint Co. Ltd, TIGER Coatings GmbH & Co. KG, PPG Industries Inc., TOYOCHEM CO., LTD., The Sherwin-Williams Company, Berger Paints India, Evonik, Elementis PLC, artience Co., Ltd., Sumitomo Bakelite Co., Ltd., Hannecard Roller Coatings, Inc - ASB Industries, and Covestro AG, among others.

The can coatings market report covers the geographical market along with a comprehensive competitive landscape analysis. It also includes cash flow analysis, profit ratio analysis, market basket analysis, market attractiveness analysis, sentiment analysis, PESTLE analysis, trend analysis, SWOT analysis, trade area analysis, demand & supply analysis, Porter’s five forces analysis, and value chain analysis.

HappyClients