AR And VR Headset Market Size, Share, Trends, Growth Report 2034

AR And VR Headset Market By Type (AR Headset, VR Headset and AR/VR Headset), By Product Type (Standalone, Tethered and Screenless Viewer), By Application (Enterprise, Consumer, Healthcare and Commercial) and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 1.3 Billion | USD 27.1 Billion | 35.5% | 2024 |

AR And VR Headset Industry Perspective:

What will be the size of the global AR And VR Headset market during the forecast period?

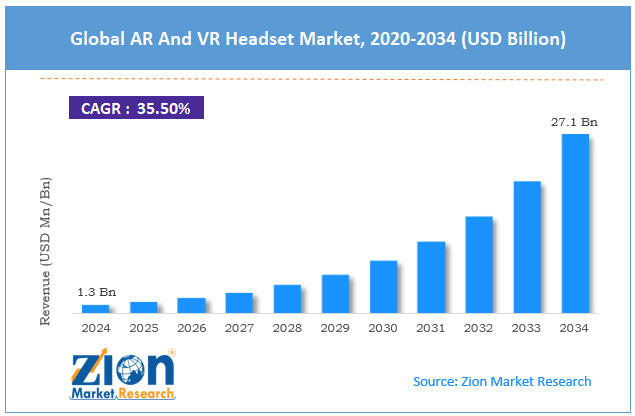

The global AR And VR Headset market size was worth around USD 1.3 billion in 2024 and is predicted to grow to around USD 27.1 billion by 2034 with a compound annual growth rate (CAGR) of roughly 35.5% between 2025 and 2034.

Request Free SampleRequest Free SampleRequest Free Sample

Request Free SampleRequest Free SampleRequest Free Sample

Key Insights

- As per the analysis shared by our research analyst, the global AR And VR Headset market is estimated to grow annually at a CAGR of around 35.5% over the forecast period (2025-2034).

- In terms of revenue, the global AR And VR Headset market size was valued at around USD 1.3 billion in 2024 and is projected to reach USD 27.1 billion by 2034.

- Increasing content ecosystem is expected to propel the AR And VR Headset market over the projected period.

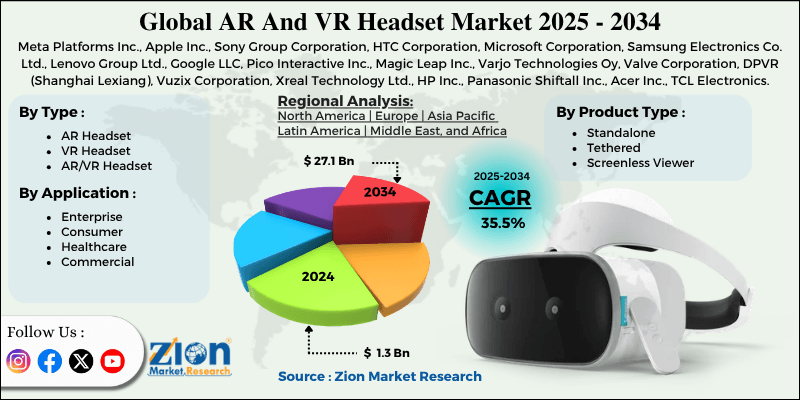

- Based on the type, the VR headset segment dominated with the largest revenue share in 2024 of over 70%.

- Based on the product type, the standalone segment captures the largest revenue share in 2024 of over 55%.

- Based on the application, the commercial segment captures the largest revenue share in 2024.

- Based on region, the Asia Pacific leads the market with 41% of revenue share in 2024.

AR And VR Headset Market: Overview

AR & VR headsets Wearable headsets that provide an immersive digital experience by overlaying or replacing a user ‘s real-world view with digital images or information. AR headsets overlaid 3D objects or information onto the real world, enabling the user to perceive it more clearly without fully shielding them from it. VR headsets completely replace the user ‘s surroundings with a fully digital environment, often using enclosed displays and head and body tracking. Newer mixed reality (MR) headsets, such as the Apple Vision Pro and Meta Quest 3, combine elements of AR & VR to allow for digital-physical interaction and manipulation in real time. These headsets are made up of components such as displays, sensors, cameras, and processors (that track head movement, gestures, and physical locations) and are used in gaming, entertainment, construction, medical/healthcare, education, and enterprise training.

Impact of the USA-Israel War on Iran on the AR And VR Headset Market

The ongoing USA-Israel vs. Iran conflict is indirectly affecting the AR & VR headset industry due to several macroeconomic, logistical, and technological reasons without directly targeting this industry. In this situation, oil prices, inflation rates, and logistical problems are rising due to conflicts, especially those related to strategic locations such as the Strait of Hormuz. Given the high dependence on semiconductor chips, sensors, and electronic devices for the operation of AR & VR headsets, this will increase production costs and delay delivery times. Another factor in the current conflict situation is the shortage of key raw materials used to manufacture electronic devices, including the rare gas Helium used in semiconductor manufacturing.

AR And VR Headset Market: Dynamics

Growth Drivers

How does the growing demand for immersive experiences drive the AR And VR Headset market?

The immersive experience is regarded as one of the key factors driving the rise of the AR/VR headset market, as there is an increased need for specialized devices that deliver high-quality immersive experiences. It means people are no longer eager to watch regular videos. Instead, they prefer to be completely immersed in the digital reality through games, music concerts, social media, movies, and so on. This means that more individuals will be looking for headsets that support spatial computing, deliver 3D images, and create immersive experiences, such as Meta Quest 3 and Apple Vision Pro. Immersive experiences are also beneficial from a business and professional perspective, as they enable professionals to train, conduct product testing, and collaborate online, among other things.

In other words, individuals can learn how to do something in a secure setting, while consumers can visualize products using 3D images before purchasing them. Therefore, it can be concluded that AR/VR technology is useful not only for entertainment but also for boosting productivity across various human activities.

Restraints

High device cost & total ownership expense hindering the AR And VR Headset industry growth

The high prices of AR & VR devices and their high total cost of ownership are seen as key factors restraining market growth. AR and VR devices feature advanced hardware, including high-quality displays, sensors, computing chips, and trackers, which makes their production cost rather high. This is one of the reasons some devices cost between $400 and more than $1,200, making them prohibitively expensive for a significant share of the target audience. It is reported that around 33–35% of companies cite high hardware prices as a main obstacle, while almost 44% of small firms consider any VR device costing more than $400 to be too expensive. The total cost of ownership (TCO) for hardware is another reason preventing wider use of VR and AR devices, including the costs of additional equipment, installation, training, and licensing.

Moreover, an enterprise-grade AR system may cost more than $900 per unit, and implementing it in corporate infrastructure requires additional effort and costs. Recent events have highlighted the problem of rising component prices for AR and VR devices: due to a global memory shortage, prices for VR devices have risen considerably, creating a hurdle to entry for new customers.

Thus, the problem of high device prices generates a cost-value paradox, which means that people and companies cannot justify paying so much money for the hardware because there are no significant benefits yet. This is why the adoption rate remains low: only early adopters, gamers, and companies with sufficient budgets use these devices. Unless the situation changes, the market for AR and VR headsets will remain constrained by high device costs.

Opportunities

Does the rising collaboration among the key market players offer a lucrative opportunity for the AR And VR Headset market?

The growing collaboration between key market players are expected to florish the market growth over the projected period. For instance, in April 2026, the company, Wearable Devices Limited, a tech development firm specializing in advanced touchless devices powered by artificial intelligence, has decided to collaborate with another tech firm, Meta-Bounds Incorporated, in the future. This collaboration aims to integrate Mudra's wristband technologies with Meta-Bounds' hardware solutions to create an amazing user experience. The companies have decided to showcase the results of their collaboration at the Augmented World Expo 2026 event to be held in Long Beach, California, USA.

Challenges

Why do the limited consumer awareness & use cases pose a significant challenge to the AR And VR Headset market?

Consumer ignorance and confusion about the application are among the biggest obstacles to the AR & VR headset market, as they negatively impact the creation of demand and the motivation to purchase. In contrast to popular devices such as smartphones or laptops, which have an evident added value for most consumers, many people simply do not realize why they should use headsets other than for games. Devices such as Meta Quest 3 or even Apple Vision Pro are not considered necessary, but something more experimental and innovative by common people. There is a lack of everyday-life application areas where AR/VR could help a lot.

However, there are some interesting and practical examples of how it can be used: conducting virtual meetings, studying educational material, training physically in sports, visualizing designs, and much more. Yet, people cannot see that they would be needed for the functions of messaging, browsing, or watching videos.

Request Free SampleRequest Free SampleRequest Free Sample

Request Free SampleRequest Free SampleRequest Free Sample

AR And VR Headset Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | AR And VR Headset Market |

| Market Size in 2024 | USD 1.3 Billion |

| Market Forecast in 2034 | USD 27.1 Billion |

| Growth Rate | CAGR of 35.5% |

| Number of Pages | 229 |

| Key Companies Covered | Meta Platforms Inc., Apple Inc., Sony Group Corporation, HTC Corporation, Microsoft Corporation, Samsung Electronics Co. Ltd., Lenovo Group Ltd., Google LLC, Pico Interactive Inc., Magic Leap Inc., Varjo Technologies Oy, Valve Corporation, DPVR (Shanghai Lexiang), Vuzix Corporation, Xreal Technology Ltd., HP Inc., Panasonic Shiftall Inc., Acer Inc., TCL Electronics, Immersed Visors Inc., and others. |

| Segments Covered | By Type, By Product Type, By Application, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

AR And VR Headset Market: Segmentation

Type Insights

Why does the VR headset dominate the AR and VR headset market?

The VR headset segment dominated with the largest revenue share in 2024 of over 70%. This is mainly due to its established presence in the gaming, entertainment, and now in the enterprise solutions space. Devices like Meta Quest 3 and PlayStation VR2 have helped increase revenues through better graphics, standalone performance, and more reasonable pricing compared to previous versions. The income generated from VR headsets primarily stems from the growing immersive gaming landscape, where consumers demand higher levels of interaction and realism, and from the expanding application of VR technology in training, simulation, and collaboration across sectors like healthcare, education, and manufacturing.

Product Type Insights

Does the standalone capture the largest market share in the AR and VR headset market?

The standalone segment captures the largest revenue share in 2024 of over 55%. A standalone headset is a VR device that works independently without being connected to anything. It is popular among players and entertainers because it is easy to use and does not require a powerful PC or game console. The combination of standalone headsets with 5G and cloud technologies has been a critical factor in improving their performance. Due to the access to 5G technology, these headsets will be able to connect to the internet and the cloud, thus creating countless opportunities for their users. It will allow them to watch high-resolution videos, receive real-time updates, and interact with others in virtual space.

Application Insights

Why the commercial capture the largest market share in the AR And VR Headset market?

The commercial segment captures the largest revenue share in 2024. The growth is driven by the increasing use of immersive technologies to improve productivity, efficiency, and training outcomes.

Regional Insights

Why does the Asia Pacific lead the AR and VR headset market?

The Asia Pacific leads the market with 41% of revenue share in 2024. With robust government backing and the introduction of technology initiatives such as smart city development and the metaverse, the adoption and implementation of AR/VR solutions are rapidly growing across multiple industries, including education, medicine, manufacturing, and retail. The already developed electronics manufacturing ecosystem in countries like China helps lower manufacturing costs while boosting innovation and the release of new products.

In addition, the expansion of 5G networks has enabled users to experience more interactive content and real-time, low-latency applications, thereby encouraging headset purchases. The emerging economies of India have also played a major role, driven by the growing popularity of VR technology in gaming centers.

AR And VR Headset Market: Competitive Analysis

The global AR And VR Headset market is dominated by players like:

- Meta Platforms Inc.

- Apple Inc.

- Sony Group Corporation

- HTC Corporation

- Microsoft Corporation

- Samsung Electronics Co. Ltd.

- Lenovo Group Ltd.

- Google LLC

- Pico Interactive Inc.

- Magic Leap Inc.

- Varjo Technologies Oy

- Valve Corporation

- DPVR (Shanghai Lexiang)

- Vuzix Corporation

- Xreal Technology Ltd.

- HP Inc.

- Panasonic Shiftall Inc.

- Acer Inc.

- TCL Electronics

- Immersed Visors Inc.

The global AR And VR Headset market is segmented as follows:

By Type

- AR Headset

- VR Headset

- AR/VR Headset

By Product Type

- Standalone

- Tethered

- Screenless Viewer

By Application

- Enterprise

- Consumer

- Healthcare

- Commercial

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table Of Content

Methodology

FrequentlyAsked Questions

AR & VR headsets Wearable headsets that provide an immersive digital experience by overlaying or replacing a user ‘s real-world view with digital images or information. AR headsets overlaid 3D objects or information onto the real world, enabling the user to perceive it more clearly without fully shielding them from it.

Key growth drivers for the AR & VR headset market include rising demand for immersive experiences, expanding enterprise adoption, continuous hardware advancements, increasing content availability, and growing integration with technologies like AI and 5G.

Major challenges restraining the AR & VR headset market include high device costs and total ownership expenses, hardware limitations (battery life, comfort, motion sickness), limited consumer awareness and compelling use cases, privacy and data security concerns, and fragmented ecosystems with lack of standardization.

Based on the product type, the standalone segment is expected to dominate the AR And VR Headset market growth during the projected period.

Emerging trends and innovations in the AR & VR headset market include the rise of spatial computing and mixed reality (XR), integration of AI for smarter immersive experiences, expansion of lightweight AR smart glasses, growth of enterprise applications, and adoption of 5G and cloud technologies enabling real-time, ultra-immersive environments.

According to the report, the global AR And VR Headset market size was worth around USD 1.3 billion in 2024 and is predicted to grow to around USD 27.1 billion by 2034.

The global AR And VR Headset market is expected to grow at a CAGR of 35.5% during the forecast period.

The global AR And VR Headset industry growth is expected to be led by the Asia Pacific over the forecast period.

The global AR And VR Headset market is dominated by players like Meta Platforms Inc., Apple Inc., Sony Group Corporation, HTC Corporation, Microsoft Corporation, Samsung Electronics Co. Ltd., Lenovo Group Ltd., Google LLC, Pico Interactive Inc., Magic Leap Inc., Varjo Technologies Oy, Valve Corporation, DPVR (Shanghai Lexiang), Vuzix Corporation, Xreal Technology Ltd., HP Inc., Panasonic Shiftall Inc., Acer Inc., TCL Electronics and Immersed Visors Inc. among others.

The market report covers the geographical market along with a comprehensive competitive landscape analysis. It also includes cash flow analysis, profit ratio analysis, market basket analysis, market attractiveness analysis, sentiment analysis, PESTLE analysis, trend analysis, SWOT analysis, trade area analysis, demand & supply analysis, Porter’s five forces analysis, and value chain analysis.

HappyClients