Motor Starters Market Size, Share, Growth, Opportunities 2034

Motor Starters Market By Starter Type (Direct-on-Line (DOL) Starter, Slip-Ring Starter, Stator-Resistance Starter, Autotransformer Starter, Combination Starter, Star-Delta Starter and Soft Starter), By Power Rating (Up to 5 kW, 5 to 50 kW and Above 50 kW), By Voltage Class (Low Voltage (Below 1 kV), Medium Voltage (1 to 35 kV) and High Voltage (Above 35 kV)), By End-user (Manufacturing, Mining, Oil and Gas, Water and Wastewater Treatment, Automotive, Food and Beverage, Power Generation and Utilities, Building and Construction, Pulp and Paper and HVAC and Refrigeration) and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 6.2 Billion | USD 11.5 Billion | 6.4% | 2024 |

Motor Starters Industry Perspective:

What will be the size of the global motor starters market during the forecast period?

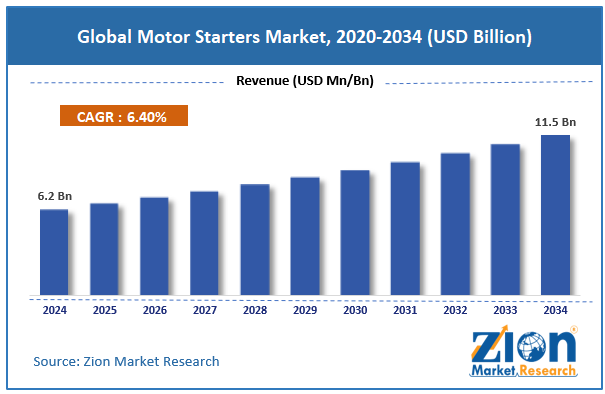

The global motor starters market size was worth around USD 6.2 billion in 2024 and is predicted to grow to around USD 11.5 billion by 2034 with a compound annual growth rate (CAGR) of roughly 6.4% between 2025 and 2034.

Key Insights

- As per the analysis shared by our research analyst, the global motor starters market is estimated to grow annually at a CAGR of around 6.4% over the forecast period (2025-2034).

- In terms of revenue, the global motor starters market size was valued at around USD 6.2 billion in 2024 and is projected to reach USD 11.5 billion by 2034.

- Rising demand for energy efficiency is expected to propel the motor starters market over the projected period.

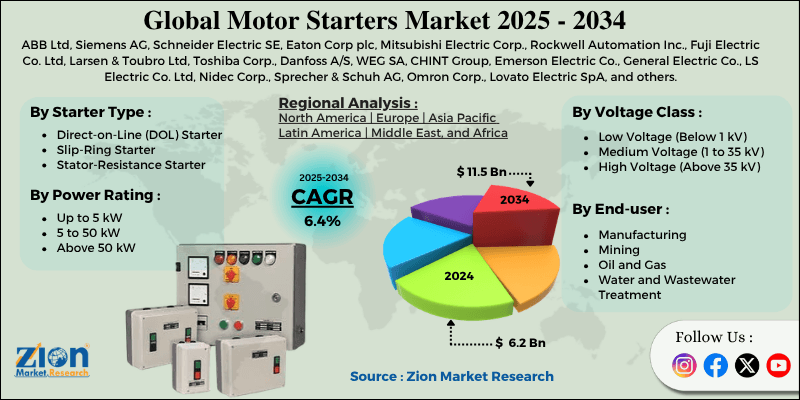

- Based on the starter type, the Direct-on-Line (DOL) Starter segment captures the largest market share in 2024 of over 33%.

- Based on the power rating, the up to 5 kW segment dominated the market with a highest revenue share in 2024 of 48%.

- Based on the voltage class, the low voltage (below 1 kV) segment dominated the market with a highest revenue share in 2024 of over 65%.

- Based on the end-user, the manufacturing segment dominated the market with a highest revenue share in 2024 of 25%.

- Based on region, the Asia Pacific captures the largest market share in 2024 of 44%.

Motor Starters Market: Overview

A motor starter is an electrical device whose purpose is to enable the safe start and shut-down of electric motors while also providing sufficient protection against damage that might result from overloads, under-voltage, phase failure, and high-current surges during motor starting. Generally, a motor starter comprises two major parts: the contactor and the overload relay. Both devices help control the flow of electrical current into the motor. Motor starters are widely used in industry and residential areas. They can be used in pumps, compressors, conveyors, HVAC equipment, fans, and other heavy-duty machines. Depending on the specific use, there are different types of motor starters.

Impact of the USA-Israel War on Iran on the Motor Starters Market

The war between the USA, Israel, and Iran has had a detrimental effect on the motor starters market, owing to several issues, including global supply chain disruptions, higher material and energy costs, and uncertainty about investments across various industries. As oil and gas prices soar due to tensions in the Strait of Hormuz, the cost of manufacturing and logistics for electrical products like contactors, relays, semiconductors, and copper used to make motor starters increases. Moreover, delays in shipping around the globe, as well as electronic component shortages, have created problems in the manufacture of automation products.

In addition, the manufacturing, oil and gas, automotive, and construction industries have delayed some capital investments due to uncertainties caused by conflicts, resulting in slower demand for motor controllers and starters. However, this conflict prompts industries to develop energy-saving, automated electrical devices.

Motor Starters Market: Dynamics

Growth Drivers

Why does the growing industrial automation drive the motor starters market?

The rising level of industrial automation is a significant trend driving the growth of the motor starters market. Industries are now incorporating more automated machines, robots, and smart manufacturing systems to increase efficiency, effectiveness, and safety in operations. As the name implies, motor starters are used to automate industrial machinery that uses electric motors, including conveyor belts, pumps, compressors, fans, and other processing equipment. Due to the growing trend towards Industry 4.0 technologies and IIoT-based solutions, there is currently a high demand for advanced, smart motor starters that can perform remote monitoring, control, and maintenance in real time.

Restraints

How do the high initial installation and upgrade costs hinder the growth of the motor starters industry?

The high initial installation and upgrade costs have become a major factor in slowing the growth of the motor starter industry. Modern types of starters, such as soft and smart starters, require a significant investment in machinery and installation. The installation cost includes wiring, installation, and protection, as well as the cost of skilled labor to install and operate the devices properly. Moreover, some industries need to install automated starter devices by renovating their existing structures, which results in high costs and wasted operational time.

Opportunities

How do the rising product launches by key market players create a lucrative opportunity for the motor starters market?

The rising product launches by key market players are expected to offer a potential opportunity to the motor starters industry expansion. For instance, in March 2025, Rockwell Automation Inc., regarded as the leading company in industrial automation and digital transformation technology worldwide, has recently announced the introduction of the M100 Electronic Motor Starter. This innovative product from Rockwell Automation will allow industries to use simpler panel wiring while simultaneously making their work easier through better functional safety solutions and improved motor-starting technology. The new M100 Electronic Motor Starter provides no derating for zero stacking up to 55 °C. The new product also allows the use of removable terminal blocks in either screw or push-in models.

Challenges

Growing adoption of Variable Frequency Drives (VFDs) poses a significant challenge to the motor starters market

The rapidly increasing use of VFDs poses a major threat to the motor starters market, as they offer superior motor control features beyond those of standard starters. While typical motor starters perform only starting, stopping, and protecting, VFDs offer additional features such as improved motor control, higher efficiency, reduced wear and tear, and process optimization. Various industries use VFDs in HVAC systems, pumping stations, conveyor systems, compressors, and other automated equipment where variable-speed performance is necessary. In addition, strict energy-efficiency regulations and ongoing efforts to minimize operating costs make it more favorable for users to adopt VFDs rather than motor starters across multiple industry verticals.

Request Free Sample

Request Free Sample

Motor Starters Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Motor Starters Market |

| Market Size in 2024 | USD 6.2 Billion |

| Market Forecast in 2034 | USD 11.5 Billion |

| Growth Rate | CAGR of 6.4% |

| Number of Pages | 227 |

| Key Companies Covered | ABB Ltd, Siemens AG, Schneider Electric SE, Eaton Corp plc, Mitsubishi Electric Corp., Rockwell Automation Inc., Fuji Electric Co. Ltd, Larsen & Toubro Ltd, Toshiba Corp., Danfoss A/S, WEG SA, CHINT Group, Emerson Electric Co., General Electric Co., LS Electric Co. Ltd, Nidec Corp., Sprecher & Schuh AG, Omron Corp., Lovato Electric SpA, and others. |

| Segments Covered | By Starter Type, By Power Rating, By Voltage Class, By End-user, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Motor Starters Market: Segmentation

Starter Type Insights

Why does the Direct-on-Line (DOL) Starter dominate the motor starters market?

The Direct-on-Line (DOL) Starter segment captures the largest market share in 2024 of over 33%. The success has been attributed to the design’s simplicity, low-cost installation, high reliability, and applicability in small and medium motors. DOL starters have had many applications in the industry, ranging from manufacturing and waste management to agricultural operations, heating and ventilation, and air conditioning systems, as well as in commercial buildings for pumping, ventilating, compressor, and conveyor motors. This product can be used to start the motor directly under full load conditions, as it requires high starting torque, making it ideal for cases where only simple motor control is needed. In addition, the rapid industrialization in developing countries has increased demand for affordable motor controls, driving higher market profits.

Power Rating Insights

How does the up to 5 kW segment capture the largest market share in the motor starters market?

The up to 5 kW segment dominated the market with a highest revenue share in 2024 of 48%. This is mainly due to the increasing use of low-energy-consumption electric motors for residential and industrial applications. Such motors are highly applicable in machines such as water pumps, HVACs, mini compressors, fans, conveyors, and agricultural machinery, among others, thereby meeting the constant demand for small electric motor starters. Urbanization and commercialization trends, as well as automation of small-scale industrial operations, are further aiding market expansion.

Voltage Class Insights

How does the low voltage (below 1 kV) segment capture the largest market share in the motor starters market?

The low voltage (below 1 kV) segment dominated the market with a highest revenue share in 2024 of over 65%. The market growth has been driven by extensive applications across various sectors, including industry, commerce, and domestic settings, where a secure motor control solution is required. The growing popularity of low-voltage motor starters is evident in their applicability across a range of machines, including pumps, fans, compressors, air conditioners, conveyor belts, and even manufacturing equipment, as they are economical, compact, and easy to install.

End-user Insights

How does the manufacturing segment capture the largest market share in the motor starters market?

The manufacturing segment dominated the market with a highest revenue share in 2024 of 25%. The market's growth can be attributed to the rising use of automation in industry, intelligent manufacturing, and electric motors. In industry, motor starters play a vital role in controlling motors that power conveyor belts, pumps, compressors, robots, mixing machines, and machine tools. With the rising adoption of Industry 4.0 and IIoT technologies, demand for motor starters with features such as real-time monitoring and predictive maintenance is increasing.

Regional Insights

Why does the Asia Pacific lead the motor starters market?

The Asia Pacific captures the largest market share in 2024 of 44%. The growth in the region is attributed to rapid industrialization, increased manufacturing activity, investment in infrastructure, and the implementation of industrial automation solutions in countries such as China, India, Japan, and Southeast Asian nations. The governments in the region are actively promoting solutions such as smart manufacturing, renewable energy, electric vehicles, and industrial transformation, which are driving high demand for motor control and protection equipment.

For instance, the Indian government’s “Make in India” program, Production Linked Incentives (PLIs), Smart City projects, and Industrial Corridor development projects are fostering growth in the number of factories and machines, leading to increased demand for low-voltage and intelligent motor starters.

Motor Starters Market: Competitive Analysis

The global motor starters market is dominated by players like:

- ABB Ltd

- Siemens AG

- Schneider Electric SE

- Eaton Corp plc

- Mitsubishi Electric Corp.

- Rockwell Automation Inc.

- Fuji Electric Co. Ltd

- Larsen & Toubro Ltd

- Toshiba Corp.

- Danfoss A/S

- WEG SA

- CHINT Group

- Emerson Electric Co.

- General Electric Co.

- LS Electric Co. Ltd

- Nidec Corp.

- Sprecher & Schuh AG

- Omron Corp.

- Lovato Electric SpA

The global motor starters market is segmented as follows:

By Starter Type

- Direct-on-Line (DOL) Starter

- Slip-Ring Starter

- Stator-Resistance Starter

- Autotransformer Starter

- Combination Starter

- Star-Delta Starter

- Soft Starter

By Power Rating

- Up to 5 kW

- 5 to 50 kW

- Above 50 kW

By Voltage Class

- Low Voltage (Below 1 kV)

- Medium Voltage (1 to 35 kV)

- High Voltage (Above 35 kV)

By End-user

- Manufacturing

- Mining

- Oil and Gas

- Water and Wastewater Treatment

- Automotive

- Food and Beverage

- Power Generation and Utilities

- Building and Construction

- Pulp and Paper

- HVAC and Refrigeration

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table Of Content

Methodology

FrequentlyAsked Questions

A motor starter is an electrical device whose purpose is to enable the safe start and shut-down of electric motors while also providing sufficient protection against damage that might result from overloads, under-voltage, phase failure, and high-current surges during motor starting.

Key growth drivers for the motor starters market include rising industrial automation, increasing demand for energy-efficient motor control systems, rapid infrastructure and manufacturing expansion, growing adoption of smart factories and Industry 4.0 technologies, and increasing investments in water treatment, HVAC, and renewable energy projects.

Major challenges restraining the growth of the motor starters market include high installation and upgrade costs, increasing adoption of Variable Frequency Drives (VFDs), integration complexity with legacy systems, and maintenance requirements for advanced motor control technologies.

Based on the end-user, the manufacturing segment is expected to dominate the motor starters market growth during the projected period.

Emerging trends and innovations impacting the motor starters market include the adoption of smart and IoT-enabled motor starters, integration with Industry 4.0 and predictive maintenance systems, rising demand for energy-efficient soft starters, increasing use of AI-based motor monitoring, and the growing shift toward digital motor control solutions and VFD-integrated systems.

According to the report, the global motor starters market size was worth around USD 6.2 billion in 2024 and is predicted to grow to around USD 11.5 billion by 2034.

The global motor starters market is expected to grow at a CAGR of 6.4% during the forecast period.

The global motor starters industry growth is expected to be led by the Asia Pacific over the forecast period.

The global motor starters market is dominated by players like ABB Ltd, Siemens AG, Schneider Electric SE, Eaton Corp plc, Mitsubishi Electric Corp., Rockwell Automation Inc., Fuji Electric Co. Ltd, Larsen & Toubro Ltd, Toshiba Corp., Danfoss A/S, WEG SA, CHINT Group, Emerson Electric Co., General Electric Co., LS Electric Co. Ltd, Nidec Corp., Sprecher & Schuh AG, Omron Corp. and Lovato Electric SpA among others.

The market report covers the geographical market along with a comprehensive competitive landscape analysis. It also includes cash flow analysis, profit ratio analysis, market basket analysis, market attractiveness analysis, sentiment analysis, PESTLE analysis, trend analysis, SWOT analysis, trade area analysis, demand & supply analysis, Porter’s five forces analysis, and value chain analysis.

HappyClients