Industrial Lighting Market Size, Trend, Growth, Industry Analysis 2034

Industrial Lighting Market By Light Source (LED, High-intensity Discharge (HID) Lighting, and Fluorescent Lighting), By Product Type (High/Low Bay Lighting and Flood/Area Lighting), By End-User (Oil and Gas, Mining, Pharmaceutical, Manufacturing, Warehouse, and Others), and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 9.5 Billion | USD 19.0 Billion | 7.20% | 2024 |

Industrial Lighting Industry Perspective:

What will be the size of the global industrial lighting market during the forecast period?

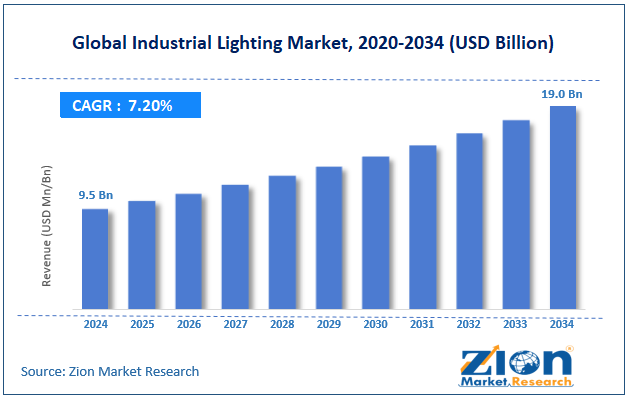

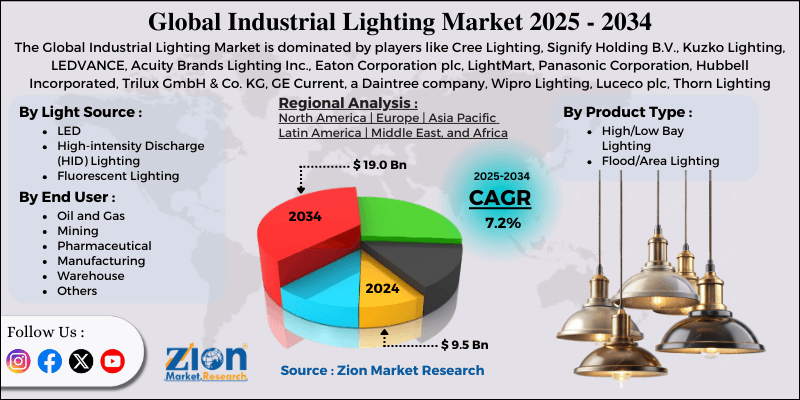

The global industrial lighting market size was worth around USD 9.5 billion in 2024 and is predicted to grow to around USD 19.0 billion by 2034, with a compound annual growth rate (CAGR) of roughly 7.2% between 2025 and 2034.

Key Insights

- As per the analysis shared by our research analyst, the global industrial lighting market is estimated to grow annually at a CAGR of around 7.2% over the forecast period (2025-2034).

- In terms of revenue, the global industrial lighting market size was valued at around USD 9.5 billion in 2024 and is projected to reach USD 19.0 billion by 2034.

- Shift to LED and smart lighting technologies is expected to drive the industrial lighting market.

- Based on the light source, the LED captures the largest revenue share in 2024 of more than 55%.

- Based on the product type, the high/low bay lighting dominates the industry growth, accounted 65% market share.

- Based on the end user, the manufacturing is expected to hold the prominent market share over the analysis period.

- Based on region, the Asia Pacific captures the largest revenue share of over 39% in 2024.

Industrial Lighting Market: Overview

The industrial lighting industry sector designs, produces, and supplies lighting products specifically for use in industrial environments such as factories, warehouses, logistics centers, power generation stations, oil & gas, metals & ores, and other heavy-duty processing areas. It specifically distinguishes itself from the general commercial lighting industry as providing high-intensity lighting capable of withstanding the extreme and often corrosive conditions present in industrial environments. It is generally used in LED high bays, LED low bays, LED floodlights, explosion-proof components, task lighting, intelligent lighting, and smart lighting, which are equipped with sensors, Internet of Things (IoT) controllers, and remote management solutions. The growth of this industry sector is driven by a growing trend towards industrialization and automation, the increasing acceptance and application of energy-efficient LED lighting technology, government regulations on workplace safety, and decreasing operational and management costs.

Industrial Lighting Market: Dynamics

Growth Drivers

Does the expansion of manufacturing & industrial infrastructure drive the industrial lighting market growth?

Expansion of manufacturing and industrial infrastructure is a major factor driving the industrial lighting market growth, especially in equipment- and technology-intensive segments like industrial lighting, automation, HVAC, and power distribution. As new factories, warehouses, distribution centers, and processing plants are built, an entire set of operational systems—lights, tools, safety systems, and energy management—is required to be installed. Bolstering this trend further are the rapid rise of industrialization across developing economies, the growth of e-commerce logistics, the automotive and electronics manufacturing boom, and the increased investment needed to build smart factories. Existing facilities need to be modernized to boost efficiency and meet energy efficiency and safety standards, which stimulates further upgrades and retrofits. The expansion of industrial infrastructure encourages both new systems development and upgrades, creating a positive growth trajectory for the market.

As per the India Brand Equity Foundation, India's industrial sector is experiencing strong growth, with the Index of Industrial Production (IIP) accelerating to a 25-month high of 7.8% in December 2025, driven by manufacturing (8.1%), mining (6.8%), and electricity (6.3%).

Restraints

Why does the high initial investment cost act as a major restraint to the industrial lighting industry?

A high initial investment cost is a notable restraint, as the initial capital investment heavily influences the buying decision, and the major industries are capital-intensive, with strict cost budgets and ROI analysis. Industry sectors such as industrial lighting, automation, machinery, and smart infrastructure use advanced systems (such as LED lights with IoT controls, automation platforms, or energy-efficient equipment) that require high upfront costs for purchasing, installation, integration, or, in some cases, facility renovation.

While operating and maintenance costs are lower, a large number of companies—especially small and medium-sized enterprises (SMEs)—prefer short-term cash flow, forgo long-term savings for several months or years, and wait longer before investing in upgrades. Industries’ long asset replacement periods further disturb the costly investments, because if current systems are working well, companies prefer to wait instead of investing in new ones. Therefore, the high initial investment hampers the industrial lighting market.

Opportunities

Does growing investment by the market players in facility expansion offer a potential opportunity for the industrial lighting market growth?

Increased investment from industrial market participants in expansion activities provides further opportunities for growth in the industrial lighting sector. As manufacturers, logistics firms, energy providers, and processing plants expand or construct new sites, lighting is an essential element of infrastructure. New warehouses, cold stores, factories, and processing plants will all require comprehensive lighting systems, including high-bay, low-bay, flood, hazardous-area, and smart lighting controls. This drives up sales volumes directly and accelerates the penetration of highly profitable, energy-efficient LED and automated systems, as opposed to older technologies, in new-build sites.

For instance, in February 2025, Panasonic Life Solutions India (PEWIN) launched a new manufacturing unit in Daman, Gujarat. This new dedicated plant will strengthen PEWIN's existing manufacturing base and further grow the lighting manufacturing capacity in India. The company has committed to a Rs 15 million investment, which will enable the production of lighting fixtures in-house, as per the company's plan for continuous growth. With this strategic investment and growth plan, the company aims to lead the lighting segment by 2030. The plant's location is ideally suited to the North and West regions, which are witnessing the best growth in the lighting industry because of the ever-growing demand for lighting fixtures.

By setting up a global standard for technology and quality management systems, India could integrate the existing manufacturing knowledge of electrical materials to achieve the highest speed and quality in lighting fixture manufacturing. The facility will first make downlights, then other fixtures. Present manufacturing potential for the first year is 150,000, expanding by 115% for the full lighting industry in FY2024.

Challenges

Rapid technology obsolescence poses a significant challenge to market growth

The rapid pace of technology obsolescence represents a significant barrier to industry growth, as the short lifecycle and reliance on ever-improving technology introduce a great deal of uncertainty for potential buyers. Many industries offering technology-based products (industrial lighting, automation, smart infrastructure) face this challenge, with frequent updates to LED performance, cloud-based smart controls, integration of the Industrial Internet of Things, and energy management software issuing regular product updates, innovations, and “next best” product introductions.

While these innovations boost performance, they can cause product obsolescence and force buyers to be cautious of jumping straight into what could be a short-lived purchase. The result is longer purchasing cycles as many companies wait for the “next best” product to come along. For manufacturers, these developments can escalate R&D costs, and shorter product life cycles lead to increased inventory risk. One further complication is the integration of widely varying system components, which also can hinder upper-end adoption levels.

Industrial Lighting Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Industrial Lighting Market |

| Market Size in 2024 | USD 9.5 Billion |

| Market Forecast in 2034 | USD 19.0 Bllion |

| Growth Rate | CAGR of 7.2% |

| Number of Pages | 224 |

| Key Companies Covered | Cree Lighting, Signify Holding B.V., Kuzko Lighting, LEDVANCE, Acuity Brands Lighting Inc., Eaton Corporation plc, LightMart, Panasonic Corporation, Hubbell Incorporated, Trilux GmbH & Co. KG, GE Current, a Daintree company, Wipro Lighting, Luceco plc, Thorn Lighting, and others. |

| Segments Covered | By Light Source, By Product Type, By End User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Industrial Lighting Market: Segmentation

Light Source Insights

Why does LED hold the dominant position in the industrial lighting market?

The LED captures the largest revenue share in 2024 of more than 55%. The market is being fueled by demand from industrial end users for cost-effective and energy-efficient LED lighting solutions. Commercial LED lighting solutions are used by industrial end users, as LED lighting is more energy-efficient and has a longer lifespan than traditional lighting equipment; LED is the preferred option for smart lighting in a home. Tax incentive programs by the government and energy-saving service programs also boost the market penetration of LEDs in industrial facilities to upgrade infrastructure.

Product Type Insights

Why does high/low bay lighting hold the largest share in the industrial lighting industry?

The high/low bay lighting dominates the industry growth, accounted 65% market share. The lighting fixtures are used for their large number of light outputs, high efficiency, and their ability to be used effectively in high-ceiling applications. Its predominant use in warehouses, factories, and industrial settings is due to its low power consumption and ease of maintenance.

End-User Insights

Does manufacturing hold a prominent share in the industrial lighting market?

The manufacturing is expected to hold the prominent market share over the analysis period. This growth is driven by the continued growth of the industry and the continued increase in the number of production plants, as well as the widespread adoption of energy-saving lighting systems. Production facilities such as assembly lines, warehouses, and quality checking stations have to be lit by robust lighting systems to ensure the safety of operating personnel, accurate production, and maximum productivity. LED high-bay and intelligent lighting, and other LED systems replacing traditional lighting (HID, fluorescent lamps, and others) account for a substantial revenue increase.

Regional Insights

Why does the Asia Pacific hold the largest share in the industrial lighting market?

The Asia Pacific captures the largest revenue share of over 39% in 2024. The market is booming owing to the fast pace of industrialization, urbanization, and mass manufacturing and capital development projects across the 5 major economies (China, India, Japan, South Korea, and Southeast Asia). The growing investment in the automotive, electronics, logistics, and pharmaceutical industries is leading to the need to build new factories, warehouses, industrial zones, and ports, which invariably require hi-tech, energy-saving, and eco-friendly lighting systems.

At the same time, governments across the region are imposing energy-efficiency norms and sustainability schemes that are forcing the replacement of conventional lighting systems with highly efficient LED and smart lighting arrangements. GST (shopfloor automation), Industry 4.0 trends, and automation across industries are also increasing the demand for integrated lighting controls, IoT-enabled lighting, and advanced lighting control systems.

Industrial Lighting Market: Competitive Analysis

The global industrial lighting market is dominated by players like:

- Cree Lighting

- Signify Holding B.V.

- Kuzko Lighting

- LEDVANCE

- Acuity Brands Lighting Inc.

- Eaton Corporation plc

- LightMart

- Panasonic Corporation

- Hubbell Incorporated

- Trilux GmbH & Co. KG

- GE Current

- a Daintree company

- Wipro Lighting

- Luceco plc

- Thorn Lighting

The global industrial lighting market is segmented as follows:

By Light Source

- LED

- High-intensity Discharge (HID) Lighting

- Fluorescent Lighting

By Product Type

- High/Low Bay Lighting

- Flood/Area Lighting

By End User

- Oil and Gas

- Mining

- Pharmaceutical

- Manufacturing

- Warehouse

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table Of Content

Methodology

FrequentlyAsked Questions

HappyClients