Industrial Gas Turbine Market Size, Growth, Global Trends, Forecast 2034

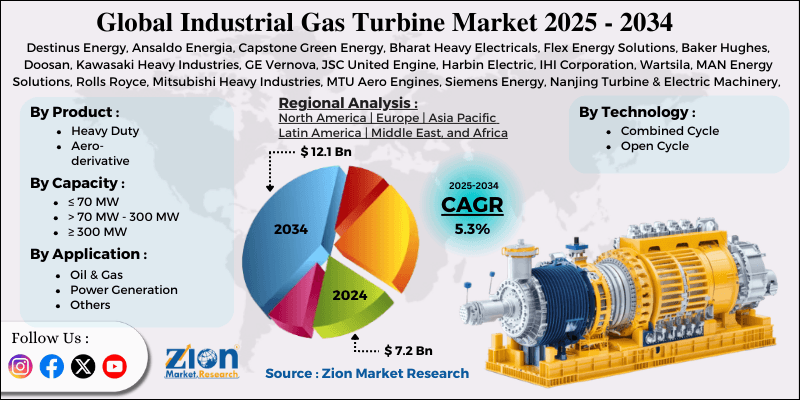

Industrial Gas Turbine Market By Capacity ( ≤ 70 MW, > 70 MW - 300 MW and ≥ 300 MW), By Product (Heavy Duty and Aero-derivative), By Technology (Combined Cycle and Open Cycle), By Application (Oil & Gas, Power Generation, and Others), and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034-

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 7.2 Billion | USD 12.1 Billion | 5.3% | 2024 |

Industrial Gas Turbine Industry Perspective:

What will be the size of the global industrial gas turbine market during the forecast period?

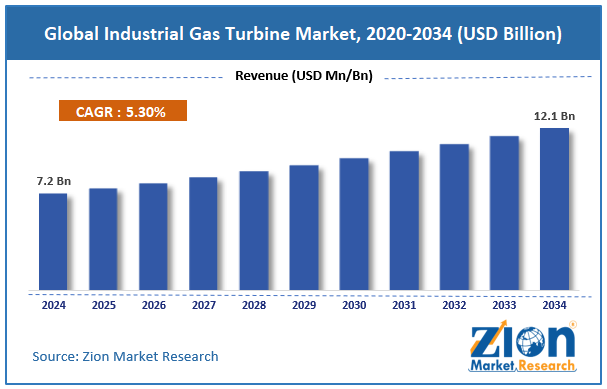

The global industrial gas turbine market size was worth around USD 7.2 billion in 2024 and is predicted to grow to around USD 12.1 billion by 2034, with a compound annual growth rate (CAGR) of roughly 5.3% between 2025 and 2034.

Key Insights

- As per the analysis shared by our research analyst, the global industrial gas turbine market is estimated to grow annually at a CAGR of around 5.3% over the forecast period (2025-2034).

- In terms of revenue, the global industrial gas turbine market size was valued at around USD 7.2 billion in 2024 and is projected to reach USD 12.1 billion by 2034.

- Growing integration with renewable energy systems is expected to dominate the industrial gas turbine market over the projected period.

- Based on the capacity, the ≤ 70 MW segment dominated the market with a 38% of market share in 2024.

- Based on the product, the aero-derivative segment is projected to grow substantially over the projected period.

- Based on the technology, the combined cycle technology accounted for the largest revenue share, over 80%, in 2024.

- Based on the application, the power generation segment is expected to dominate the market during the forecast period.

- Based on region, North America is expected to capture the largest market share over the projected period.

Industrial Gas Turbine Market: Overview

The industrial gas turbine market encompasses the global industry for manufacturing, installing, and maintaining turbines for power generation and mechanical drive applications. Industrial turbines consist of a compressor and a combustor, with a power turbine coupling that converts the energy from the combustion of natural gas, diesel, hydrogen mixtures, or other similar fuels into electric power. Due to their high operational efficiency, quick start-up, and continuous operation under demanding load conditions, most industrial turbines are used in power generation, oil and gas, petrochemicals, manufacturing, and mining applications. The industry also provides turbines of various sizes, ranging from small ones used for distributed power generation to large ones used in combined-cycle plants. The increased demand for power in developing economies, the shift toward cleaner fuels over coal, and the rise in industrialization are the major drivers of the industrial gas turbine market. The market is primarily driven by the surge in global electricity consumption, rapid industrial development, and the need for efficient, flexible power generation solutions across sectors such as oil & gas, manufacturing, petrochemicals, and utilities. Gas turbines are gaining popularity as a source of flexible, efficient power due to their high efficiency, quick start-up capability, and ability to operate in combined-cycle mode.

However, the market also faces restraints that are affecting its growth. High capital investment, installation, and operating costs are decreasing adoption among smaller power producers and industries. Growing competition from renewable energy technologies, coupled with storage systems, is also challenging gas-powered energy sources. Regulations related to GHG (greenhouse gases) emissions and the uncertain supply of long-term natural gas are adding to the market barriers.

Industrial Gas Turbine Market: Dynamics

Growth Drivers

Why does the increasing global electricity demand drive the expansion of the industrial gas turbine market?

Rising global electricity demand is fueling the expansion of the industrial gas turbine market, as energy producers and industrial customers seek a dependable, scalable, and energy-efficient solution to quickly generate additional power. Industrial gas turbines are widely used in power stations and industrial setups due to their ability to generate large volumes of electricity at higher efficiency and faster acceleration time than traditional power systems. High levels of urbanization, industrialization, and digital infrastructure (data centers, manufacturing plants, and smart cities) are constantly increasing the need for efficient, uninterrupted power supply. Gas turbines are used to meet base load and transient loads in such scenarios, preserving grid stability during periods of high load demand.

Industrial gas turbines are also installed in combined-cycle plants, where they work in series with steam turbines to dramatically increase the power system's efficiency. This additional efficiency enables utilities to generate more energy from the same amount of fuel, thus providing cost advantages of gas turbine–powered generation capacity. This operational flexibility of gas turbines also allows power systems to speed up or slow down, which helps compensate for fluctuations in grid demand or aid the integration of sustainable power sources such as solar and wind energy. This surge in worldwide electricity demand is, hence, prompting authorities, power suppliers, and operators to favor gas turbine technology, thereby propelling growth in the industrial gas turbine market.

For instance, according to the International Energy Agency, global electricity consumption is increasing rapidly, driven by AI data centers, EVs, and air conditioning, and global demand is expected to grow at a CAGR of 3.4% till 2026. India recorded 9.5% growth in power consumption in FY23, and peak power demand is projected to reach 277 GW in FY26.

Restraints

High capital and installation costs are hindering the industrial gas turbine industry

High capital and development costs pose a significant barrier to growth in the industrial gas turbine industry, as developing and installing a gas turbine system requires substantial upfront capital investment. Industrial gas turbines include expensive components such as high-temperature turbine blades, advanced combustion systems, cooling and control systems, and compressors, all manufactured with high-quality materials and sophisticated engineering. In addition, the project requires supporting infrastructure, such as fuel delivery, cooling, emission-control systems, grid connection capabilities, and installation, which further increases capital expenditures for utility and industrial owners. The time-consuming process and extensive engineering required for installing an industrial gas turbine system ultimately increase capital expenditure.

For small and medium-sized power producers or industrial end users, these high up-front costs may price gas turbine projects out of the market relative to other potential power sources, such as renewable power or distributed energy technologies. This reduces potential market growth in the utility and industrial sectors, delaying interest in projects and, in some cost-sensitive markets, inhibiting sales of industrial gas turbines.

Opportunities

Will the growing number of agreements among key players present a lucrative opportunity for the industrial gas turbine market?

The growing number of alliances among major players shall provide an attractive proposition for the industrial gas turbine sector, as alliances enable the fast-tracking of technology development, the introduction of new technologies into the market, the implementation of market penetration strategies, and the support of large power plant projects. Alliances among turbine manufacturers, energy companies, utilities, and engineering companies provide access to technical and financial resources and enable the sharing of widely used distribution networks, making it easier to roll out new turbine systems across regions worldwide. The formation of alliances, such as joint ventures, long-term service agreements, technology licensing, and supply partnerships, shall enable companies to develop high-efficiency turbines, develop turbines compatible with hydrogen fuels, and improve maintenance, digital control, sensing, and monitoring systems. This shall also help manufacturers of gas turbines secure large power-plant projects and long-term maintenance contracts, thereby ensuring revenue stability.

For instance, in June 2025, IHI Corporation and GE Vernova Inc. announced the successful completion of a new Large-scale Combustion Test (LCT) facility at IHI Aioi Works in Hyogo, Japan. The facility is designed to enable new capabilities for next-generation combustion technologies that use ammonia, a hydrogen derivative that contains no carbon and produces no net CO2 emissions when burned. The test facility is designed to simulate the conditions of a GE Vernova F-class operating gas turbine (pressures, temperatures, and air and fuel flows).

Challenges

Does competition from renewable energy sources challenge the expansion of the industrial gas turbine industry?

Competition from renewable energy would be another long-term constraint to the growth of the industrial gas turbine industry. The rapid development of renewable energy technologies (solar, wind, and hydropower) has led to significant changes in the global energy structure, as governments and utilities worldwide are emphasizing cleaner, more sustainable power generation methods. This trend is declining the installation costs (makes renewable power generation equipment more affordable), encouraging policies from various governments and rising investment in renewable energy projects and grid integration, and has attracted more and more power producers to put their eyes on the development of renewable power generation facilities rather than traditional conventional power generation systems based on fossil fuels.

Advances in energy storage technology (for instance, battery-based storage systems) also enable renewable energy to deliver higher-rate power generation and a more reliable power supply, making it more competitive with gas turbine–based power plants. A global commitment to reducing greenhouse gas emissions and adopting an emissions trading system would also stimulate further renewable power development. Meanwhile, gas turbines are still based on fossil fuels like natural gas, which limits their competitiveness; the penetration of renewable energy sources would negatively affect the growth of the industrial gas turbine industry.

Industrial Gas Turbine Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Industrial Gas Turbine Market |

| Market Size in 2024 | USD 7.2 Billion |

| Market Forecast in 2034 | USD 12.1 Bllion |

| Growth Rate | CAGR of 5.3% |

| Number of Pages | 222 |

| Key Companies Covered | Destinus Energy, Ansaldo Energia, Capstone Green Energy, Bharat Heavy Electricals, Flex Energy Solutions, Baker Hughes, Doosan, Kawasaki Heavy Industries, GE Vernova, JSC United Engine, Harbin Electric, IHI Corporation, Wartsila, MAN Energy Solutions, Rolls Royce, Mitsubishi Heavy Industries, MTU Aero Engines, Siemens Energy, Nanjing Turbine and Electric Machinery, Vericor, Solar Turbines, and others. |

| Segments Covered | By Capacity, By Product, By Technology, By Application, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Industrial Gas Turbine Market: Segmentation

Capacity Insights

What factor causes the ≤ 70 MW segment to hold a dominant position in the industrial gas turbine market?

The ≤ 70 MW segment dominated the market with a 38% of market share in 2024. Growth in the segment is primarily fueled by increased demand for distributed power generation, small industrial power installations, and flexible energy sources. Gas turbines in this capacity range are currently used in manufacturing, oil and gas, chemicals, and commercial/institutional installations that require dependable power from on-site sources. Their small footprint, lower capital investment than that of large turbines, and fast run-up times make them suitable for captive plants/standby applications and decentralized energy systems.

Product Insights

Why does aero-derivative grow substantially in the industrial gas turbine market?

The aero-derivative segment is projected to grow substantially over the projected period. The growth of the segment is attributed to gas turbines’ high efficiency, operational flexibility, and lightweight construction, enabled by advances in aircraft engine technology. Aero-derivative gas turbines are widely used in oil & gas processing, offshore platforms, distributed generation, and emergency/peaking power plants due to their quick start-up and improved fuel efficiency compared to most heavy-duty turbines. Modular construction makes them easier to install, maintain, and transport, and therefore desirable in remote or tight-field industrial sites.

Technology Insights

Why does combined cycle technology contribute a significant share to the industrial gas turbine market?

The combined cycle technology accounted for the largest revenue share, over 80%, in 2024. The growth of this technology will be driven by how efficient and at what cost the power can be generated. The world's combined-cycle power plants operate gas turbines alongside steam turbines, capturing the waste heat from the gas turbines to generate additional power. Combined-cycle plants achieve higher efficiencies than single-cycle systems, enabling utilities and other energy-intensive operations to produce more electricity with less fuel. Rising interest in lower-emission power generation, along with the conversion of coal-fired power plants to natural gas, is a major driver of the adoption of combined-cycle technologies.

Furthermore, combined-cycle power plants provide greater operational flexibility and lower greenhouse gas emissions than traditional power plants, enabling greater penetration of peak-shaving applications, backup power for wind farms, and zero-emission power generation to meet increasingly strict environmental regulations. These factors will translate into higher deployment rates for combined-cycle gas turbine systems, driving revenue growth in this segment.

Application Insights

Does power generation holds prominent market share in the industrial gas turbine industry?

The power generation segment is expected to dominate the market during the forecast period. The launching of modular power solutions drives the segment expansion. For instance,

in February 2026, Rolls-Royce unveiled a new modular concept for gas-engine power plants to secure supply and accelerate the German Government's Power Plant Strategy. The turnkey plants, which range in power from 5 to 500 megawatts (depending on customers' needs), are H2-ready solutions that can be operated in hydrogen in the future. The energy plants, composed of preassembled, pretested modules of 10, 20, and 30 megawatts, can go online within 12 to 18 months of placing an order.

Regional Insights

Why does North America lead the industrial gas turbine market?

North America is expected to capture the largest market share over the projected period. The regional growth will be driven by increasing demand for electricity, modernization of the region's legacy power infrastructure, and the trend toward natural gas-based power generation. The United States and Canada have access to large natural gas resources, making it attractive for utilities and industrial customers to switch to gas turbine technology as a cleaner, lower-emission option.

Further, increasing investment in the area is driving market growth. For instance, in February 2026, Siemens Energy AG announced that it had completed a plan to invest $1 billion to scale-up manufacturing of gas turbines and power-grid solutions in the US. This followed GE Vernova's announcement at the end of last month to invest around US$ 600mn in the US over the next two years for similar output. The investment program involves several brownfield expansions, including increased transformer production and servicing, as well as further support for the development of large gas turbine manufacturing.

Industrial Gas Turbine Market: Competitive Analysis

The global industrial gas turbine market is dominated by players like:

- Destinus Energy

- Ansaldo Energia

- Capstone Green Energy

- Bharat Heavy Electricals

- Flex Energy Solutions

- Baker Hughes

- Doosan

- Kawasaki Heavy Industries

- GE Vernova

- JSC United Engine

- Harbin Electric

- IHI Corporation

- Wartsila

- MAN Energy Solutions

- Rolls Royce

- Mitsubishi Heavy Industries

- MTU Aero Engines

- Siemens Energy

- Nanjing Turbine and Electric Machinery

- Vericor

- Solar Turbines

The global industrial gas turbine market is segmented as follows:

By Capacity

- ≤ 70 MW

- > 70 MW - 300 MW

- ≥ 300 MW

By Product

- Heavy Duty

- Aero-derivative

By Technology

- Combined Cycle

- Open Cycle

By Application

- Oil & Gas

- Power Generation

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table Of Content

Methodology

FrequentlyAsked Questions

HappyClients