Fire Protection System Pipes Market Size, Share, Report 2034

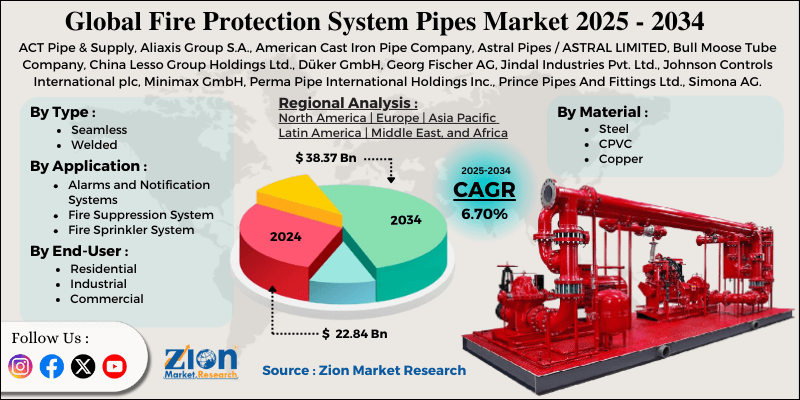

Fire Protection System Pipes Market By Type (Seamless, Welded), By Material (Steel, CPVC, Copper, and Others), By Application (Alarms and Notification Systems, Fire Suppression System, Fire Sprinkler System, and Others), By End-User (Residential, Industrial, Commercial), and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 22.84 Billion | USD 38.37 Billion | 6.70% | 2024 |

Fire Protection System Pipes Industry Perspective:

What will be the size of the global fire protection system pipes market during the forecast period?

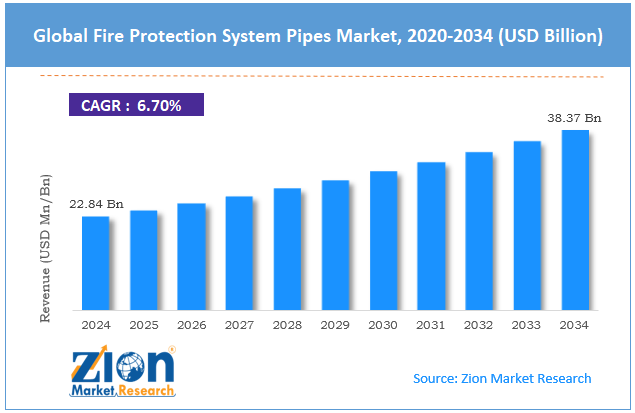

The global fire protection system pipes market size was around USD 22.84 billion in 2024 and is projected to reach USD 38.37 billion by 2034, with a compound annual growth rate (CAGR) of roughly 6.70% between 2025 and 2034. The Fire Protection System Pipes Market is driven by increasing global construction activities, rapid urbanization, and stringent enforcement of fire safety regulations across residential, commercial, and industrial sectors.

Key Insights:

- As per the analysis shared by our research analyst, the global fire protection system pipes market is estimated to grow annually at a CAGR of around 6.70% over the forecast period (2025-2034)

- In terms of revenue, the global fire protection system pipes market size was valued at around USD 22.84 billion in 2024 and is projected to reach USD 38.37 billion by 2034.

- The fire protection system pipes market is projected to grow significantly, driven by increasing construction activity globally, urbanization, rising infrastructure development, and technological advancements in fire protection materials.

- Based on type, the welded segment is expected to lead the market, while the seamless segment is expected to grow considerably.

- Based on material, the steel segment is the dominating segment, while the copper segment is projected to witness sizeable revenue over the forecast period.

- Based on the application, the fire sprinkler system segment leads, while the fire suppression system segment is expected to grow rapidly.

- Based on end-user, the commercial segment is expected to lead the market, followed by the industrial segment.

- By region, North America is projected to dominate the global market with approximately 28% share & it is dominated owing to stringent fire safety regulations, advanced infrastructure development, high retrofit activity, and strong adoption across industrial, residential, and commercial sectors.

Fire Protection System Pipes Market: Overview

Fire protection system pipes are an essential component of fire safety infrastructure, dedicated to distributing water and other extinguishing agents throughout a building to control or suppress fires. These pipes are usually made of steel, specialized plastics, or copper and are configured in networks such as standpipes, hydrant systems, and sprinkler systems. The global fire protection system pipes market is likely to expand rapidly, fueled by regulatory compliance and strict safety codes, construction growth and urbanization, and infrastructure modernization. Stringent building codes and fire safety norms need reliable fire protection systems. Pipes meeting these standards are crucial for compliance. This fuels consistent demand in commercial, residential, and industrial sectors.

Moreover, speedy urban development drives the construction of high-rise buildings, housing complexes, and malls. Each new structure needs fire protection piping systems. This growth ultimately increases market demand. Furthermore, older buildings and industrial facilities are being upgraded for efficiency and safety. Modern piping systems outshine outmoded networks, creating recurring industry opportunities.

Despite the growth, the global market is impeded by factors such as maintenance complexity and supply chain challenges. Fire protection pipes need regular inspections and repairs. Recurring costs and the need for skilled technicians make complexity demotivating for some building owners. Likewise, material shortages or transport delays can affect timely delivery. Proper schedules can be disturbed. Therefore, manufacturers experience operational and production barriers.

Nonetheless, the global fire protection system pipes industry stands to benefit from several key opportunities, including sustainable, green fire protection solutions and retrofitting and renovation projects. Eco-friendly pipe materials and water-efficient systems are gaining importance. Sustainability-focused projects seek such solutions. This eventually offers a growing niche industry. Additionally, aging buildings need upgraded fire safety networks. Modern pipes replace outdated infrastructure. Renovation projects augment recurring demand.

Fire Protection System Pipes Market: Dynamics

Growth Drivers

How are insurance and risk-financing pressures boosting the growth of the fire protection system pipes market?

Insurance companies primarily associate premiums and coverage with the presence of strong fire protection systems. buildings with certified fire protection piping qualify for low rates and better terms. Risk-based evaluations motivate the installation of high-class suppression systems. Financial incentives make fire protection investment more appealing for industrial and commercial properties. Owners view advanced piping as a way to reduce possible losses. Insurance considerations are hence a leading driver of the fire protection system pipes market.

How are technological improvements in pipe materials fueling growth in the fire protection system pipes market?

Advancements in materials like corrosion-resistant steel, CPVC, and composites improve installation, durability, and fire resistance. Advanced pipes smoothly integrate with smart building systems for predictive maintenance and IoT-based monitoring. These solutions lower lifecycle costs while promising reliable performance. Manufacturers are developing sustainable, hybrid materials for safety and efficiency. Improved functionality and cost-effectiveness raise adoption. Technological progress strengthens the industry demand.

Restraints

Complex installation and maintenance requirements hinder the market progress

Fire protection piping systems need skilled labor for proper installation and regular maintenance. Improper installation may compromise safety compliance and system performance. Maintenance schedules, testing, and inspections add to operational complexity—a shortage of trained personnel in developing markets limits adoption. Complexity also increases lifecycle costs for building owners. These are the key industry limitations that slow the overall market development.

Opportunities

What opportunities are available in the Fire Protection System Pipes Market?

The rising number of retrofit and renovation projects in aging buildings to meet updated fire safety codes offers substantial growth potential, especially in hotels, hospitals, and commercial complexes where modern materials and technologies can be seamlessly integrated.

Growing emphasis on sustainable and green building practices is creating demand for eco-friendly pipe materials and water-efficient systems, while expansion into emerging markets with increasing safety awareness and industrial development provides new revenue streams for innovative solutions.

Challenges

What are the major challenges in the Fire Protection System Pipes Market?

A persistent shortage of trained professionals for proper installation, maintenance, and inspection of fire protection systems poses significant risks to performance and safety, particularly in regions where training programs are limited or inaccessible.

Evolving regulatory landscapes and the need for continuous upgrades to incorporate new technologies add complexity and cost pressures, requiring manufacturers and installers to invest heavily in compliance and workforce development to sustain long-term growth.

Fire Protection System Pipes Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Fire Protection System Pipes Market |

| Market Size in 2024 | USD 22.84 Billion |

| Market Forecast in 2034 | USD 38.37 Billion |

| Growth Rate | CAGR of 6.70% |

| Number of Pages | 216 |

| Key Companies Covered | ACT Pipe & Supply, Aliaxis Group S.A., American Cast Iron Pipe Company, Astral Pipes / ASTRAL LIMITED, Bull Moose Tube Company, China Lesso Group Holdings Ltd., Düker GmbH, Georg Fischer AG, Jindal Industries Pvt. Ltd., Johnson Controls International plc, Minimax GmbH, Perma Pipe International Holdings Inc., Prince Pipes And Fittings Ltd., Simona AG, Victaulic Company, and others. |

| Segments Covered | By Type, By Material, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, the Middle East and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Fire Protection System Pipes Market: Segmentation

The global fire protection system pipes market is segmented based on type, material, application, end-use, and region.

Why will the welded pipes segment dominate the fire protection system pipes market?

Based on type, the global fire protection system pipes industry is divided into seamless and welded. The welded pipes segment accounts for approximately 73.6% of the total market due to their cost efficiency and widespread use in industrial projects and infrastructure. On the other hand, the seamless pipes segment progresses with 26.4% of the total market. This is primarily used in specific high-performance applications where reliability and strength are prioritized.

How much market share does the steel pipes segment hold in the fire protection system pipes market?

Based on material, the global market is segmented into steel, CPVC, copper, and others. The steel pipes segment dominates with 46% of the overall market share due to their strong preference for durability, high strength, pressure resistance, and compliance with strict fire safety standards. This makes them ideal for large-scale industrial, commercial, and high-rise applications.

Conversely, the copper pipes segment holds 25% of the market share due to their good corrosion resistance, reliable performance in fire suppression systems, and suitability for specific installations. They are prominent for their thermal and longevity properties.

Will the fire sprinkler system continue to dominate the fire protection system pipes market?

Based on application, the global fire protection system pipes market is segmented into alarms and notification systems, fire suppression systems, fire sprinkler systems, and others. The fire sprinkler system segment leads with 50% market share. This leadership signifies extensive use of sprinkler networks in industrial, commercial, and residential buildings for automatic fire suppression through water distribution pipes.

However, the fire suppression system segment ranks second with a 30% market share. Pipes in this category are used in wider suppression solutions, comprising foam, gas, water, and other agents in high-risk facilities where automatic extinguishing is crucial.

Why will the commercial segment emerge as dominant in the fire protection system pipes market?

Based on end-user, the global market is segmented into residential, industrial, and commercial. Commercial buildings, such as hospitals, hotels, retail centers, and offices, require extensive fire protection piping. High occupancy and stringent safety regulations fuel strong demand. Hence, the segment holds a leading market share.

Nonetheless, the industrial segment, including chemical complexes, oil and gas plants, and factories, requires robust piping systems for high-risk environments. Fire suppression needs make the segment second-leading.

Fire Protection System Pipes Market: Regional Analysis

Why does North America hold a dominant position in the global Fire Protection System Market?

North America is anticipated to retain its leading role with a 6.3% CAGR in the global fire protection system pipes market, driven by a strong regulatory framework, a high revenue share, developed markets, and advanced infrastructure and retrofit activity. North America dominates due to strict fire safety regulations and building codes, particularly in the US under NFPA and local mandates. These regulations promise the continuous adoption of modern piping solutions, increasing industry penetration.

Moreover, the region accounts for a substantial share of global revenue, ranging from nearly 25.4% to more than 30% of the overall market, making it the leading regional contributor. Sophisticated industries in Canada and the U.S. mean a high base of installations for industrial, residential, and commercial fire safety systems. Furthermore, North America’s broader infrastructure and current urban development drive both retrofitting and new installations of outmoded fire systems, especially in industrial facilities, logistical hubs, and high-rise buildings. Increased awareness of safety standards, along with upgrades in old buildings sustain demand for fire protection pipes.

What position will Asia Pacific hold in the fire protection system pipes industry?

Asia Pacific ranks as the second-largest region in the global fire protection system pipes industry, with a 6.4% CAGR, driven by rapid urbanization, heightened regulatory focus and safety awareness, and a large regional market. Commercial complexes, high-rise residential buildings, and industrial parks in APAC need extensive fire safety systems. The region’s construction scale outshines others, fueling substantial demand for pipe.

Moreover, governments are strengthening fire safety codes and mandating fire protection systems in existing and new buildings. Updated regulations and compliance initiatives in India, China, and neighboring nations are driving the adoption of certified pipes. Elevated corporate and public awareness of fire hazards augments industry growth. Additionally, APAC holds a leading share of the global market, making it the second-largest regional contributor. While North America remains the dominant region, APAC is the fastest-growing, narrowing the gap in revenue share as its industrial and construction sectors expand.

Europe experiences steady growth propelled by harmonized European Union directives that impose uniform fire safety requirements across member states, driving upgrades in both residential and commercial buildings amid ongoing urbanization. Countries such as Germany and the United Kingdom lead the region with their emphasis on sustainable construction and renovation of historic structures, where fire protection pipes must blend modern performance with architectural preservation. A strong focus on environmental standards pushes manufacturers toward eco-friendly materials, while robust public-private partnerships support large-scale infrastructure projects that integrate comprehensive fire suppression networks. The region's advanced research and development landscape enables quick adoption of smart piping solutions, ensuring compliance with evolving codes and enhancing overall resilience against fire incidents.

Recent Developments

- In April 2025, Ferguson Enterprises, Inc. completed the acquisitions of Independent Pipe & Supply Corp. and National Fire Equipment Ltd. to strengthen its commercial fire protection and fabrication capabilities across North America.

- In May 2025, Johnson Controls International plc expanded its fire suppression portfolio by introducing advanced smart fire detection and sprinkler systems integrated with AI-driven monitoring technologies.

- In November 2024, Victaulic Company opened an expanded manufacturing facility in Pennsylvania, United States, to boost production capacity for fire protection pipe fittings and related components.

- In December 2025, Aliaxis SA acquired Johnson Controls’ CPVC pipe fittings business to enhance its residential and light commercial sprinkler systems portfolio and expand its global fire protection presence.

Fire Protection System Pipes Market: Competitive Analysis

The leading players in the global fire protection system pipes market are:

- ACT Pipe & Supply

- Aliaxis Group S.A.

- American Cast Iron Pipe Company

- Astral Pipes / ASTRAL LIMITED

- Bull Moose Tube Company

- China Lesso Group Holdings Ltd.

- Düker GmbH

- Georg Fischer AG

- Jindal Industries Pvt. Ltd.

- Johnson Controls International plc

- Minimax GmbH

- Perma Pipe International Holdings Inc.

- Prince Pipes And Fittings Ltd.

- Simona AG

- Victaulic Company

What are the key trends in the global Fire Protection System Pipes Market?

Integration of IoT and Smart Technologies

The integration of IoT-enabled monitoring and predictive maintenance capabilities into fire protection piping systems is transforming traditional installations into intelligent networks that provide real-time alerts, automated diagnostics, and seamless connectivity with building management platforms, significantly enhancing response times and reducing downtime while appealing to modern smart-building developers.

Adoption of Advanced and Sustainable Materials

A clear shift toward lightweight, corrosion-resistant composites and eco-friendly CPVC alternatives is gaining momentum as these materials lower installation costs, minimize environmental impact, and deliver superior longevity compared to conventional options, aligning with global sustainability goals and supporting green certification requirements in construction projects.

The global fire protection system pipes market is segmented as follows:

By Type

- Seamless

- Welded

By Material

- Steel

- CPVC

- Copper

- Others

By Application

- Alarms and Notification Systems

- Fire Suppression System

- Fire Sprinkler System

- Others

By End-User

- Residential

- Industrial

- Commercial

By Region

- North America

- The U.S.

- Canada

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Southeast Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Table Of Content

Methodology

FrequentlyAsked Questions

HappyClients