Engineering, Procurement and Construction (EPC) Market Size, Forecast 2034

Engineering, Procurement and Construction (EPC) Market By Project Type (Oil and Gas, Power Generation, Water and Wastewater Treatment, Chemical and Petrochemical, Infrastructure, Mining, Renewable Energy), By Contract Type (Lump Sum Turnkey, Cost Plus Fee, Unit Price), By End-User (Government and Public Sector, Private Sector, Industrial), By Service Type (Engineering Services, Procurement Services, Construction Services, Project Management Services), and By Region – Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034-

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

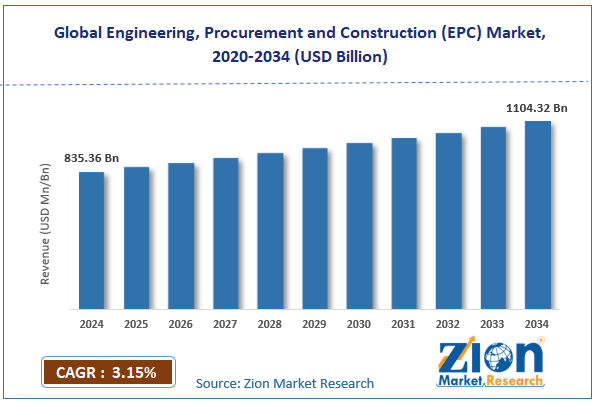

| USD 835.36 Billion | USD 1104.32 Billion | 3.15% | 2024 |

Industry Perspective:

What will be the size of the Engineering, Procurement, and Construction market during the forecast period?

The global Engineering, Procurement, and Construction market size was worth approximately USD 835.36 billion in 2024 and is projected to grow to around USD 1104.32 billion by 2034, with a compound annual growth rate (CAGR) of roughly 3.15% between 2025 and 2034.

Key Insights

- As per the analysis shared by our research analyst, the global Engineering, Procurement, and Construction market is estimated to grow annually at a CAGR of around 3.15% over the forecast period (2025-2034).

- In terms of revenue, the global Engineering, Procurement, and Construction market size was valued at approximately USD 835.36 billion in 2024 and is projected to reach USD 1104.32 billion by 2034.

- The Engineering, Procurement, and Construction market is projected to grow significantly due to expanding global energy infrastructure investment, industrial capacity growth in emerging economies, rising government spending on public infrastructure, accelerating renewable energy project development, and increasing adoption of modular and prefabricated construction approaches.

- Based on project type, the oil and gas segment is expected to lead the Engineering, Procurement, and Construction market, while the renewable energy segment is anticipated to grow significantly.

- Based on contract type, the lump sum turnkey segment is expected to lead the Engineering, Procurement, and Construction market, while the cost plus fee segment is anticipated to grow rapidly.

- Based on end-user, the industrial segment is the dominating segment, while the government and public sector segment is projected to witness sizeable revenue over the forecast period.

- Based on service type, the construction services segment is expected to lead the Engineering, Procurement, and Construction market, while the engineering services segment is expected to grow significantly.

- Based on region, Asia Pacific is projected to dominate the global Engineering, Procurement, and Construction market during the estimated period, followed by the Middle East and Africa.

Engineering, Procurement and Construction (EPC) Market: Overview

Engineering, Procurement, and Construction (EPC) is a project delivery method in which a single company manages the entire process of design, material procurement, and construction. In this model, a single contractor takes responsibility for planning the facility, purchasing equipment and materials, and completing all construction work within a fixed schedule and budget. This approach allows the project owner to work with a single main contractor rather than managing multiple separate companies for engineering, Procurement, and construction tasks. EPC contracts are commonly used for large, complex projects where careful coordination among design, supply, and construction is essential to success. Typical examples include power plants, oil refineries, chemical factories, water treatment plants, and large infrastructure projects such as bridges or industrial facilities. EPC contractors manage engineers, equipment suppliers, construction teams, and subcontractors throughout the project lifecycle.

They also handle technical challenges, equipment delivery schedules, and project quality standards to ensure the facility operates as required. Project owners benefit from clear timelines and fixed costs, which reduce financial risk. The EPC model also allows faster project completion because design, Procurement, and construction activities are closely coordinated. Increasing global investment in infrastructure, renewable energy projects, and industrial development continues to support strong demand for EPC services worldwide. The accelerating global need for new energy infrastructure, industrial capacity, and public works projects is expected to drive sustained growth in the Engineering, Procurement, and Construction market over the forecast period.

Engineering, Procurement and Construction (EPC) Market: Technology Roadmap 2025 to 2034

What is the projected development roadmap of the Engineering, Procurement, and Construction market over the forecast period?

The Engineering, Procurement, and Construction industry is growing rapidly due to digital transformation of project delivery, expanding global infrastructure investment, sustainability mandates, and advances in construction technology and materials science. The market is expected to grow at a CAGR of around 3.15% over the forecast period, driven by rising demand across energy, water, transportation, and industrial facility development. The following roadmap outlines key development phases expected through 2034.

2025–2027: Digital Project Delivery and Modular Construction Phase

- Building information modeling software helps engineers and construction teams collaborate using a shared 3D digital model that updates as the project progresses.

- Modular construction allows major building parts to be manufactured in factories and quickly assembled at the project site.

- Drones and satellite images are increasingly used to survey sites and monitor construction progress.

2028–2031: Automation, Artificial Intelligence, and Supply Chain Optimization Phase

- Artificial intelligence tools help project managers predict delays, track costs, and identify supply risks earlier.

- Robotic machines perform repetitive or dangerous tasks such as welding and concrete placement.

- Blockchain systems track equipment and materials from suppliers to construction sites for better transparency.

2032–2034: Sustainable Construction and Net-Zero Project Delivery Phase

- Low-carbon materials such as green steel and carbon-reduced concrete are used in new EPC projects to help reduce construction emissions and meet sustainability targets.

- Carbon-tracking systems monitor emissions from design through project completion.

- Circular design methods allow materials and components to be reused after a facility’s operational life.

Engineering, Procurement and Construction (EPC) Market: Dynamics

Growth Drivers

How is growing global investment in energy infrastructure driving the expansion of the Engineering, Procurement, and Construction market?

The Engineering, Procurement, and Construction (EPC) market is growing as countries worldwide invest heavily in building new energy infrastructure and upgrading existing power systems. Governments and private companies are developing power plants, expanding electricity transmission networks, building natural gas facilities, and constructing renewable energy projects. These large and complex projects require EPC contractors capable of managing design, equipment supply, and construction under a single contract. The global shift toward clean energy is creating strong demand for solar farms, wind power plants, hydroelectric dams, and modern energy storage systems. Many developing countries in Asia, Africa, and Latin America are building new power infrastructure to support economic growth and rising electricity demand. In developed regions, older power plants and transmission networks are being upgraded or replaced with modern systems. Energy security concerns are also encouraging countries to increase domestic energy production capacity. New energy technologies such as offshore wind projects, hydrogen production plants, and large battery storage systems are creating additional opportunities for EPC contractors during the forecast period.

Industrial expansion and investment in manufacturing capacity are boosting market demand.

The Engineering, Procurement, and Construction market is also growing as many countries build new factories and expand industrial production capacity. Manufacturing activities are returning to North America and Europe, while industrial growth continues rapidly across Asia, Southeast Asia, and parts of Africa. These developments are driving strong demand for EPC contractors capable of designing, supplying equipment, and building complex industrial facilities. Semiconductor manufacturing plants are being constructed in many countries to increase global chip production and reduce supply shortages. Chemical and petrochemical companies are expanding processing facilities to meet rising demand for plastics, fertilizers, and specialty chemicals used in many industries. Pharmaceutical companies are building new production plants to manufacture vaccines, medicines, and biotechnology products at larger scale.

Food and beverage companies are also investing in large processing and distribution facilities to serve growing populations and expanding urban markets. Electric vehicle battery manufacturing plants require advanced factory designs and specialized infrastructure, creating new opportunities for EPC contractors. Mining companies are developing new processing plants to supply minerals such as lithium, cobalt, nickel, and copper used in clean energy technologies. Growing industrial investment continues to support strong demand for EPC services worldwide.

Restraints

How are project cost overruns and schedule delays limiting the growth of the Engineering, Procurement, and Construction market?

The Engineering, Procurement, and Construction (EPC) industry faces challenges, as many large projects still experience delays and cost overruns despite EPC contracts promising clear budgets and schedules. Some projects begin with inaccurate cost estimates during the bidding stage, which makes it difficult for contractors to complete the work within the original budget. Unexpected problems such as difficult ground conditions, environmental issues, or new regulations can also require design changes and additional construction work. Supply chain disruptions may delay the delivery of critical equipment, slowing the entire project timeline. Managing many subcontractors and workers across large construction sites can also lead to coordination and quality issues. Due to past project failures, many clients place stricter contract conditions on EPC contractors and transfer more financial risk to them. This makes contractors more cautious when selecting projects to bid on. As a result, fewer contractors compete for some projects, which can increase overall project costs in the market.

Opportunities

How is renewable energy and green infrastructure development driving growth in the Engineering, Procurement, and Construction market?

The Engineering, Procurement, and Construction (EPC) market is growing rapidly as the global shift toward clean energy drives a surge in infrastructure projects. Countries are investing in solar power plants, wind farms, hydro storage facilities, and hydrogen production systems. These projects are large and technically complex, making EPC contractors important, as they manage design, equipment supply, and construction. Many governments have set ambitious renewable energy targets that require the construction of thousands of new projects over the coming years. This creates a steady pipeline of work for EPC companies with experience in clean energy development. Offshore wind projects are especially important because they require specialized engineering, marine construction vessels, underwater cables, and complex installation processes. EPC contractors with strong technical skills in offshore wind are expected to gain major competitive advantages as this sector expands globally. Electricity grid modernization is also creating significant EPC opportunities, as renewable energy sources require stronger transmission networks. Projects such as battery storage systems, high-voltage power transmission lines, and smart grid technologies need advanced engineering and construction expertise. Governments and development banks are also providing funding support to accelerate green infrastructure projects worldwide.

Challenges

How are skilled labor shortages and workforce development gaps creating challenges for the Engineering, Procurement, and Construction industry?

The Engineering, Procurement, and Construction (EPC) market is facing a growing shortage of skilled workers needed to complete large infrastructure and industrial projects. Engineers with experience in civil, mechanical, electrical, and process design are in high demand yet remain in short supply in many countries. Skilled workers such as welders, electricians, pipefitters, and technicians are also difficult to find, especially in regions where infrastructure and energy investments are increasing quickly. The situation is made more difficult by the fact that many experienced workers are approaching retirement, while fewer young professionals are entering construction and engineering careers. Many younger workers prefer jobs in technology, finance, or other industries that offer office environments and long-term career stability. Construction work is often physically demanding and may require working at remote project sites for long periods. EPC companies are trying to solve this problem by investing in training programs, hiring workers from international labor markets, and improving employee benefits and career opportunities. Some companies are also adopting automation and digital construction technologies to reduce dependence on manual labor. However, the shortage of skilled workers remains a major challenge for the EPC industry's growth.

Engineering, Procurement and Construction (EPC) Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Engineering, Procurement and Construction (EPC) Market |

| Market Size in 2024 | USD 835.36 Billion |

| Market Forecast in 2034 | USD 1104.32 Billion |

| Growth Rate | CAGR of 3.15 |

| Number of Pages | 226 |

| Key Companies Covered | Bechtel Corporation, Fluor Corporation, McDermott International, Saipem, Technip Energies, Wood Group, Worley, Samsung Engineering, Hyundai Engineering and Construction, Petrofac, and others. |

| Segments Covered | By Project Type, By Contract Type, By End-User, By Service Type, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, the Middle East and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 - 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Engineering, Procurement and Construction (EPC) Market: Segmentation

The global Engineering, Procurement, and Construction market is segmented based on project type, contract type, end-user, and region.

Why is the oil and gas segment expected to lead the Engineering, Procurement, and Construction market?

Based on project type, the global Engineering, Procurement, and Construction industry is categorized into oil and gas, power generation, water and wastewater treatment, chemical and petrochemical, infrastructure, mining, and renewable energy. The oil and gas segment accounted for approximately 31% of the global market share and is expected to remain significant during the forecast period due to continued investment in upstream exploration and production infrastructure, midstream pipeline and processing facilities, and downstream refining capacity across producing nations in the Middle East, North America, and Southeast Asia. The renewable energy segment follows as the fastest-growing category, with nearly 21% market share, driven by surging investment in solar, wind, and storage projects worldwide.

What supports the leadership of the lump sum turnkey segment in the Engineering, Procurement, and Construction market during the forecast period?

Based on contract type, the market is divided into lump-sum turnkey, cost-plus-fee, and unit-price. The lump-sum turnkey segment accounts for around 58% of the market share. It is expected to lead throughout the forecast period, as project owners across most sectors strongly prefer the cost certainty and single-point accountability this contract structure provides. The cost-plus-fee segment holds about 27% market share, supported by its use in complex projects where scope and technical requirements are not fully defined early.

Why does the industrial segment dominate the Engineering, Procurement, and Construction market?

Based on end-user, the global Engineering, Procurement, and Construction market is segregated into the government and public sector, private sector, and industrial sectors. The industrial segment accounts for nearly 49% of the overall market share. It continues to lead because large-scale factory construction, chemical plant development, and energy facility projects require exactly the kind of technically integrated, risk-managed project delivery that the EPC model is designed to provide. The government and public sector segment accounts for approximately 32% of the market, driven by public investment in water treatment infrastructure, transportation networks, public buildings, and utility facilities.

Why is the construction services segment expected to lead the Engineering, Procurement, and Construction market?

Based on service type, the global Engineering, Procurement, and Construction industry is categorized into engineering services, procurement services, construction services, and project management services. The construction services segment accounted for approximately 36% of the global market share and is expected to remain dominant during the forecast period, driven by the significant share of project costs associated with on-site construction activities, civil works, equipment installation, and infrastructure development across major industrial and energy projects worldwide. The engineering services segment is the fastest-growing, driven by rising demand for advanced project design, digital engineering tools, and complex infrastructure planning.

Engineering, Procurement and Construction (EPC) Market: Regional Analysis

What factors enable the Asia Pacific to dominate the global Engineering, Procurement, and Construction market during the forecast period?

Asia Pacific is expected to grow at a CAGR of about 7.4% during the forecast period and remain the most active region in the Engineering, Procurement, and Construction (EPC) market. The region leads because it has large-scale infrastructure projects, rapid industrial growth, rising energy demand, and a large pool of experienced EPC contractors. Countries across the Asia Pacific are building new roads, bridges, airports, railways, power plants, factories, and water systems to support economic growth and urban development. China is the largest EPC market in the region due to continuous investment in transportation networks, energy projects, and large industrial facilities under long-term national development plans. India is one of the fastest-growing EPC markets, with government programs focused on expanding power generation, highways, railways, and urban infrastructure.

Countries in Southeast Asia, such as Indonesia, Vietnam, Thailand, and Malaysia, are also investing heavily in manufacturing zones, ports, energy projects, and city infrastructure. These investments help attract foreign companies and strengthen economic development. Australia remains an important EPC market due to large-scale mining, liquefied natural gas, and renewable energy projects. Japan and South Korea have some of the world’s most advanced EPC companies that compete for major projects globally. Strong government support and development financing continue to encourage large-scale infrastructure and energy investments across the Asia Pacific region.

Why is the Middle East and Africa expected to be the second leading region in the global Engineering, Procurement, and Construction market?

The Middle East and Africa are expected to grow at a CAGR of about 6.8% over the forecast period and remain the second-largest regional contributor to the Engineering, Procurement, and Construction (EPC) market. The region is experiencing strong growth as many countries invest in large infrastructure, energy, and industrial development projects. Gulf countries such as Saudi Arabia, the United Arab Emirates, and Qatar are investing heavily in economic diversification programs to reduce their dependence on oil revenues. Saudi Arabia’s Vision 2030 plan includes many large projects in tourism, manufacturing, renewable energy, transportation, and modern city development. The United Arab Emirates is also investing in clean energy projects, advanced technology infrastructure, and modern industrial facilities to strengthen its economy. Qatar continues to expand energy production facilities and infrastructure to support both domestic development and global energy exports.

In Africa, many countries are attracting international investment for power plants, mining projects, transportation networks, and industrial infrastructure. EPC contractors play an important role in the design and construction of these complex projects. Water infrastructure, such as desalination plants and irrigation systems, is also expanding rapidly as many countries in the region face severe water shortages and rising population demand.

Recent Developments

- In January 2026, Solarworld Energy Solutions won a 250-MW solar photovoltaic EPC contract from NTPC Renewable Energy in Rajasthan, covering design, Procurement, and construction of the grid-connected solar facility.

- In February 2026, Power Mech Projects secured EPC orders worth about ₹10 billion from subsidiaries of Adani Power for the construction and installation of turbine and generator systems at large thermal power plants.

Engineering, Procurement and Construction (EPC) Market: Competitive Analysis

The leading players in the global Engineering, Procurement, and Construction market are:

- Bechtel Corporation

- Fluor Corporation

- McDermott International

- Saipem

- Technip Energies

- Wood Group

- Worley

- Samsung Engineering

- Hyundai Engineering and Construction

- Petrofac

The global engineering, procurement, and construction (EPC) market is segmented as follows:

By Project Type

- Oil and Gas

- Power Generation

- Water and Wastewater Treatment

- Chemical and Petrochemical

- Infrastructure

- Mining

- Renewable Energy

By Contract Type

- Lump Sum Turnkey

- Cost Plus Fee

- Unit Price

By End-User

- Government and Public Sector

- Private Sector

- Industrial

By Service Type

- Engineering Services

- Procurement Services

- Construction Services

- Project Management Services

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table Of Content

Methodology

FrequentlyAsked Questions

Engineering, Procurement, and Construction is a project delivery model in which a single contractor is responsible for designing a facility, sourcing all materials and equipment, and completing all construction work under one integrated contract, giving project owners a single point of accountability.

The global Engineering, Procurement, and Construction market is projected to grow due to expanding global energy infrastructure investment, industrial capacity growth in emerging economies, rising government spending on public infrastructure, accelerating renewable energy development, and growing adoption of digital project management tools.

According to a study, the global Engineering, Procurement, and Construction market size was worth around USD 835.36 billion in 2024 and is predicted to grow to around USD 1104.32 billion by 2034.

The CAGR value of the Engineering, Procurement, and Construction market is expected to be around 3.15% during 2025-2034.

Which region will contribute notably to the Engineering, Procurement, and Construction market value?

Asia Pacific is expected to lead the global Engineering, Procurement, and Construction market during the forecast period.

The major players profiled in the global Engineering, Procurement, and Construction market include Bechtel Corporation, Fluor Corporation, McDermott International, Saipem, Technip Energies, Wood Group, Worley, Samsung Engineering, Hyundai Engineering and Construction, and Petrofac.

The report examines key aspects of the Engineering, Procurement, and Construction market, including a detailed analysis of current growth drivers and constraints, as well as future growth opportunities and challenges.

Macroeconomic factors such as government infrastructure spending, energy investment cycles, inflation in construction materials, and global interest rates will strongly influence the Engineering, Procurement, and Construction market by shaping project demand, investment flows, and overall construction activity worldwide.

In the Engineering, Procurement, and Construction market, pricing trends are influenced by rising costs of steel, cement, equipment, and skilled labor. Contractors are increasingly adopting risk-sharing contracts, flexible pricing structures, and cost-plus models to manage volatility in raw materials and supply chains across large infrastructure and energy projects.

To remain competitive in the Engineering, Procurement, and Construction market, companies should invest in digital project management tools, modular construction techniques, and supply chain optimization. Strengthening partnerships, improving workforce training, and expanding expertise in renewable energy and infrastructure projects can also help firms capture new EPC opportunities globally.

HappyClients