Direct Carrier Billing Market Size, Share, Growth, Opportunities 2034

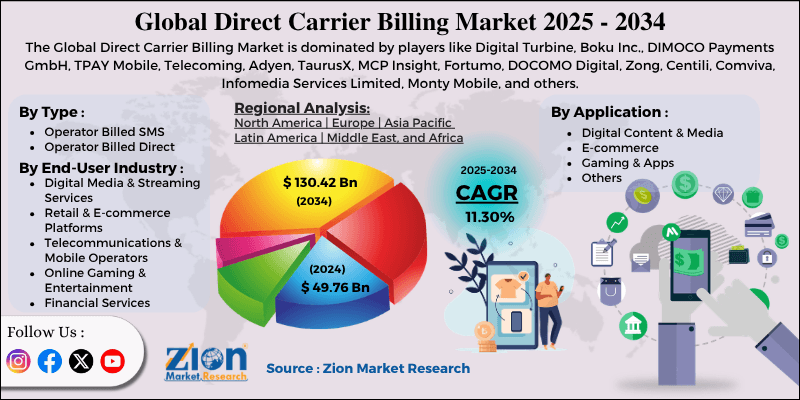

Direct Carrier Billing Market By Type (Operator Billed SMS and Operator Billed Direct), By Application (Digital Content & Media, E-commerce, Gaming & Apps, and Others), By End-User Industry (Digital Media & Streaming Services, Retail & E-commerce Platforms, Telecommunications & Mobile Operators, Online Gaming & Entertainment, and Financial Services), and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 49.76 Billion | USD 130.42 Billion | 11.30% | 2024 |

Direct Carrier Billing Industry Perspective:

What is the anticipated size of the global digital printing packaging market during the projection period?

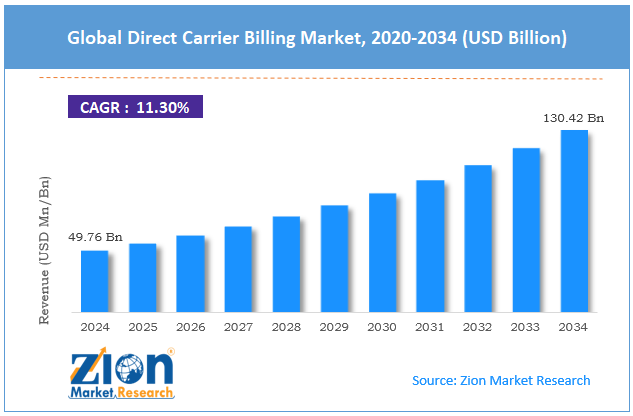

The global direct carrier billing market size was worth around USD 49.76 billion in 2024 and is predicted to grow to around USD 130.42 billion by 2034, with a compound annual growth rate (CAGR) of roughly 11.30% between 2025 and 2034.

Key Insights:

- As per the analysis shared by our research analyst, the global direct carrier billing market is estimated to grow annually at a CAGR of around 11.30% over the forecast period.

- In terms of revenue, the global direct carrier billing market size was valued at around USD 49.76 billion in 2024 and is projected to reach USD 130.42 billion by 2034.

- The digital printing packaging market is projected to grow at a significant rate due to the rising penetration of mobile commerce and subscription-based digital services worldwide.

- Based on the type, the operator-billed direct segment is growing at a high rate and will continue to dominate the global market, as per industry projections

- Based on the application, the digital content & media segment is anticipated to command the largest market share

- Based on the end-user industry, the online gaming & entertainment segment is expected to lead the market growth trends

- Based on region, the Asia Pacific is projected to dominate the global market during the forecast period.

Direct Carrier Billing Market: Overview

Direct Carrier Billing (DCB) is a telecom-based mobile payment mechanism that enables users to charge digital purchases directly to their postpaid mobile bills or deduct payments from their prepaid balances. The system eliminates dependency on credit cards, debit cards, and traditional banking infrastructure. Key components of direct carrier billing systems include telecom billing platforms, payment gateway integration layers, authentication modules, subscription management tools, fraud detection engines, and merchant onboarding interfaces. These components work collectively to ensure secure authorization, transaction processing, and recurring billing management. Initially introduced for SMS-based purchases such as ringtones and wallpapers, the technology has evolved into API-integrated billing systems embedded within OTT platforms, gaming marketplaces, and mobile app stores. Integration with subscription ecosystems has significantly strengthened its commercial relevance.

During the forecast period, demand for direct carrier billing is expected to increase due to the expansion of mobile-first commerce, rising digital subscription adoption, and collaboration between telecom and fintech. However, regulatory compliance requirements and revenue-sharing structures may impact market growth trends in the coming years.

Direct Carrier Billing Market: Dynamics

Growth Drivers

How will the expansion of mobile commerce affect the growth rate of the direct carrier billing market?

The global direct carrier billing market is expected to be driven by the rapid expansion of mobile commerce worldwide. Increasing smartphone penetration, affordable data connectivity, and rising digital consumption are accelerating in-app purchases and subscription-based transactions. Digital platforms are integrating carrier billing to simplify checkout experiences and improve transaction approval rates. The convenience of one-click payments encourages impulse purchases and recurring subscription enrolments.

Financial inclusion trends to drive demand for direct carrier billing in the coming years

The growing need for financial inclusion across emerging economies is expected to further support market expansion. Millions of consumers remain unbanked but possess mobile connectivity. Direct carrier billing enables these users to access digital content and services without requiring credit cards or banking credentials. This capability expands digital participation and supports inclusive payment ecosystems globally, allowing improved revenue in the global direct carrier billing market.

Restraints

What will be the impact of revenue-sharing models on the direct carrier billing market during the projection period?

The global direct carrier billing industry is expected to be limited due to layered revenue-sharing agreements between telecom operators, aggregators, and digital merchants. These structures may reduce net margins compared to alternative payment platforms. Additionally, compliance with billing transparency regulations, consumer consent frameworks, and anti-fraud mandates increases operational complexity, which may affect long-term scalability.

Opportunities

Technological advancements and expanding digital subscription ecosystems are reported in the market to offer renewed growth opportunities.

The global direct carrier billing market is expected to generate growth opportunities due to the increasing adoption of recurring subscription models across Over-The-Top (OTT) platforms, gaming ecosystems, and digital media services. DCB enables seamless recurring billing and subscription management. Emerging digital economies in Southeast Asia, Africa, and Latin America present significant untapped potential, driven by high mobile subscriber penetration and limited banking infrastructure.

How is growth in mobile gaming expected to shape the direct carrier billing market during the projection period?

The growing penetration of mobile gaming is projected to create new growth opportunities for market players. Avid gamers rely heavily on fast and secure payments for in-app purchases. They refrain from using credit or debit cards for payments since they are time-consuming and can sometimes lead to payment fraud. Furthermore, growing concerns over data privacy and security may encourage more mobile gamers to use direct carrier billing services, as this method is more secure and less time-consuming.

Challenges

Why will competition from alternative digital payment systems challenge direct carrier billing market expansion during the forecast period?

The global direct carrier billing industry will face competition from mobile wallets, QR code payments, UPI-based systems, and bank-backed mobile apps. These alternatives often provide lower transaction fees and broader merchant acceptance. To remain competitive, DCB providers must enhance fraud monitoring systems, implement advanced authentication layers, and optimize pricing structures.

Direct Carrier Billing Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Direct Carrier Billing Market |

| Market Size in 2024 | USD 49.76 Billion |

| Market Forecast in 2034 | USD 130.42 Bllion |

| Growth Rate | CAGR of 11.30% |

| Number of Pages | 225 |

| Key Companies Covered | Digital Turbine, Boku Inc., DIMOCO Payments GmbH, TPAY Mobile, Telecoming, Adyen, TaurusX, MCP Insight, Fortumo, DOCOMO Digital, Zong, Centili, Comviva, Infomedia Services Limited, Monty Mobile, and others. |

| Segments Covered | By Type, By Application, By End-User Industry, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Direct Carrier Billing Market: Segmentation

The global direct carrier billing market is segmented based on type, application, end-user industry, and region.

Why does the operator-billed direct segment lead the direct carrier billing market?

Based on type, the global market segments are operator-billed SMS and operator-billed direct. In 2024, the highest revenue was listed in the operator-billed direct segment, accounting for over 74% of the global revenue. It is expected to continue to lead the market growth rate, with a CAGR of 11.4% during the projection period, supported by seamless in-app integrations and recurring billing capabilities.

Which application segment dominates the direct carrier billing market?

Based on application, the global market is divided into digital content & media, e-commerce, gaming & apps, and others. In 2024, the digital content & media segment held the largest share of the market, accounting for around 48% of global revenue. It will continue to lead the segment with a CAGR of 10.8% during the forecast period. The growing number of digital content viewers worldwide, driven by smartphone penetration, rising consumer awareness, and increasing disposable income, will drive segmental dominance in the future.

What is the future CAGR for the online gaming & entertainment segment in the direct carrier billing market?

Based on end-user industry, the global market divisions are digital media & streaming services, retail & e-commerce platforms, telecommunications & mobile operators, online gaming & entertainment, and financial services. In 2024, the highest growth rate was listed in the online gaming & entertainment segment, accounting for 43% of global revenue. It is projected to deliver a CAGR of 13% during the forecast period due to a surge in mobile gamers worldwide and the benefits of leveraging DCB over other payment formats.

Direct Carrier Billing Market: Regional Analysis

Why will Asia Pacific continue leading the direct carrier billing market during the forecast period?

The global direct carrier billing market is anticipated to be led by the Asia Pacific during the forecast period. In 2024, the region accounted for approximately 42% of global revenue and is expected to grow at a CAGR of 11.7%. Rapid smartphone penetration in China, India, Japan, and Southeast Asia, along with expanding OTT ecosystems, will facilitate improved revenue generation across the region. For instance, India has more than 149 million active OTT subscribers, and the number is expected to increase in the coming years.

How is Europe performing in the direct carrier billing market?

Europe is projected to register a CAGR of 11.1% during the forecast period. Countries such as the UK, Germany, and France are witnessing strong adoption of subscription-based content and telecom digitalization initiatives, helping the regional market flourish. In addition, regional players are rapidly expanding their business presence to new markets. For instance, in August 2025, SLA Digital, a leading Direct Carrier Billing and mobile identity solutions provider, launched carrier billing with Yettel Bulgaria. The move will allow Yettel Bulgaria customers to access seamless mobile payments.

What supports growth in North America in the direct carrier billing market?

North America holds a significant share of the global direct carrier billing market and is projected to grow at a CAGR of 9.6% during the projection period. High app monetization rates, mature telecom infrastructure, and strong OTT subscription penetration contribute to regional expansion. Furthermore, the rapid growth of new mobile video game players and a surge in digital publishing may contribute to overall revenue across North America.

Direct Carrier Billing Market: Competitive Analysis

The global direct carrier billing market is led by players like:

- Digital Turbine

- Boku Inc.

- DIMOCO Payments GmbH

- TPAY Mobile

- Telecoming

- Adyen

- TaurusX

- MCP Insight

- Fortumo

- DOCOMO Digital

- Zong

- Centili

- Comviva

- Infomedia Services Limited

- Monty Mobile

What are the latest key trends in the direct carrier billing market?

Subscription-based monetization expansion

The ongoing integration of recurring billing models across OTT platforms and gaming services is strengthening demand for direct carrier billing solutions. Subscription models provide consistent, predictable revenue for service providers, while users can cancel their subscriptions when the services are no longer required.

Advanced authentication and fraud prevention

Artificial Intelligence (AI)-driven fraud detection systems, tokenization frameworks, and secure identity verification tools are improving transaction security and reliability, thus promoting higher use of DCB services among end users.

The global direct carrier billing market is segmented as follows:

By Type

- Operator Billed SMS

- Operator Billed Direct

By Application

- Digital Content & Media

- E-commerce

- Gaming & Apps

- Others

By End-User Industry

- Digital Media & Streaming Services

- Retail & E-commerce Platforms

- Telecommunications & Mobile Operators

- Online Gaming & Entertainment

- Financial Services

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table Of Content

Methodology

FrequentlyAsked Questions

Direct carrier billing is a mobile payment method that allows users to charge digital purchases directly to their mobile phone bill or prepaid balance. It eliminates the need for credit cards and banking credentials.

The global direct carrier billing market is expected to be driven by rising smartphone penetration, growing subscription-based digital platforms, and increasing financial inclusion initiatives.

According to a study, the global direct carrier billing market size was worth around USD 49.76 billion in 2024 and is predicted to grow to around USD 130.42 billion by 2034.

The CAGR value of the direct carrier billing market is expected to be around 11.30% during 2025-2034.

The global direct carrier billing industry will be challenged by regulatory complexity, revenue-sharing margins, and competition from alternative digital payment systems.

Subscription monetization models and AI-based fraud detection integration are key trends influencing the direct carrier billing market.

The global direct carrier billing market has performed well so far and will offer similar growth trends in the coming years.

The global direct carrier billing market is anticipated to be led by Asia Pacific during the forecast period.

The global direct carrier billing market is led by players Digital Turbine, Boku, Inc., DIMOCO Payments GmbH, TPAY Mobile, Telecoming, Adyen, TaurusX, MCP Insight, Fortumo, DOCOMO Digital, Zong, Centili, Comviva, Infomedia Services Limited, and Monty Mobile.

The report explores crucial aspects of the direct carrier billing market, including a detailed discussion of existing growth factors and restraints, while also browsing future growth opportunities and challenges that impact the market.

HappyClients