Direct Air Capture System Market Size, Growth, Global Trends, Forecast 2034

Direct Air Capture System Market By Product (Absorption-based DAC, Adsorption-based DAC, Membrane-based DAC, Cryogenic-based DAC), By Scale (Pilot-scale, Demonstration-scale, Commercial-scale), By Application (Carbon Capture and Storage [CCS], Carbon Capture and Utilization [CCU]), and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 220 Million | USD 3,940 Million | 43.80% | 2024 |

Direct Air Capture System Industry Perspective:

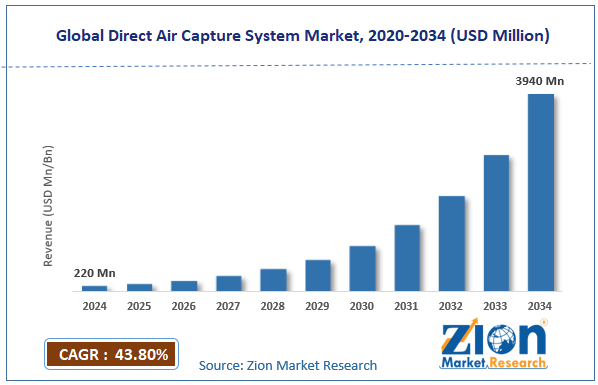

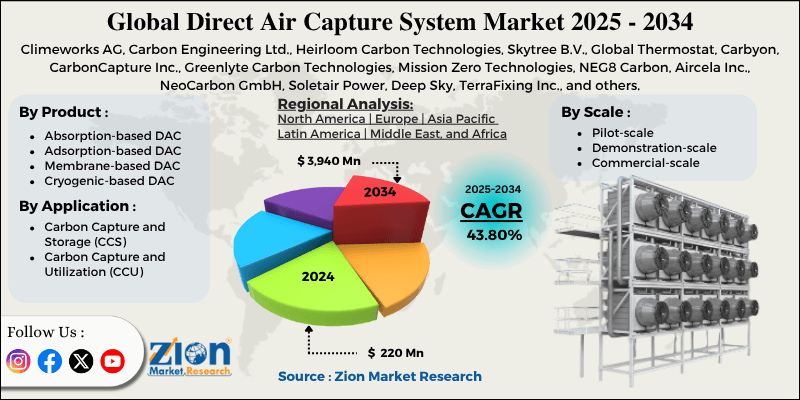

The global direct air capture system market size was approximately USD 220 million in 2024 and is projected to reach around USD 3,940 million by 2034, with a compound annual growth rate (CAGR) of roughly 43.80% between 2025 and 2034.

Key Insights:

- As per the analysis shared by our research analyst, the global direct air capture system market is estimated to grow annually at a CAGR of around 43.80% over the forecast period (2025-2034)

- In terms of revenue, the global direct air capture system market size was valued at around USD 220 million in 2024 and is projected to reach USD 3,940 million by 2034.

- The direct air capture system market is projected to grow significantly due to stricter government regulations and carbon-pricing schemes, technological advancements that improve capture efficiency and reduce costs, and government incentives, subsidies, and funding for DAC deployment.

- Based on product, the adsorption-based DAC segment is expected to lead the market, while the absorption-based DAC segment is expected to grow considerably.

- Based on scale, the commercial-scale segment is the dominating segment, while the demonstration-scale segment is projected to witness sizeable revenue over the forecast period.

- Based on application, the Carbon Capture and Storage (CCS) segment is expected to lead the market compared to the Carbon Capture and Utilization (CCU) segment.

- Based on region, North America is projected to dominate the global market during the estimated period, followed by Europe.

Direct Air Capture System Market: Overview

A direct air capture system captures carbon dioxide directly from the atmosphere with filters or chemical sorbents. The extracted CO2 can then be stored underground or reused in industrial applications. This technology supports global climate goals by reducing atmospheric CO2 levels and complementing other emission reduction strategies for a more sustainable future. The global direct air capture system market is projected to experience substantial growth, driven by global climate mitigation efforts and net-zero commitments, as well as supportive government policies and incentives, alongside technological advancements and cost improvements. Corporations and economies are setting ambitious net-zero targets that require removing CO2 from the atmosphere, driving the demand for direct air capture systems. DAC is becoming a vital tool alongside emission reductions. Elevated awareness of climate change strengthens its adoption.

Governments are offering subsidies, tax credits, and regulations to motivate carbon removal solutions. These incentives mitigate investment risks associated with DAC deployment. Policy support amplifies the commercialization of DAC projects. Furthermore, improvements in system design, sorbents, and energy efficiency are decreasing DAC operational costs. Enhanced technology raises capture scalability and efficiency. This makes DAC more commercially appealing over time.

Although drivers exist, the global market is challenged by factors such as high operational and capital costs, energy intensity, and the risk of carbon footprint. DAC systems require substantial energy inputs, making the removal of one ton of CO2 expensive. High costs restrict commercial adoption. Scaling up needs significant financial investment. Likewise, DAC systems powered by fossil fuels can offset the advantages of CO2 removal. Sustainable deployment needs low-carbon energy sources. Energy-intensive operations can reduce net efficiency.

Even so, the global direct air capture system industry is well-positioned due to scaling CO2 storage ecosystems, CO2 utilization and value creation, and integration with renewables. DAC deployment fuels the demand for storage solutions, such as saline aquifers and depleted reservoirs. Integrated capture and storage business models can capture more value. This progresses the DAC ecosystem. Captured CO2 can be converted into fuels, building materials, and chemicals. Monetizing CO2 creates additional revenue streams. This improves the economic feasibility of DAC. Additionally, coupling the DAC with low-carbon power decreases emissions and operational costs. This raises industry appeal and sustainability. Renewable integration also augments investment potential.

Direct Air Capture System Market Dynamics

Growth Drivers

How is the direct air capture system market driven by technological innovation, modularity, and cost reductions?

Innovation in solvent and sorbent chemistry, modular system design, integration with renewable energy sources, and process engineering is steadily reducing the cost and raising the scalability of DAC systems. Modular units enable faster, smaller-to-deploy plants, which decrease financial risk and help demonstrate the technology's viability. With learning-curve effects, larger commercial plants become more feasible, enhancing economies over time. These improvements make DAC more appealing to industries and investors, amplifying momentum from pilot to commercial scale. This technology propeller highlights long-term market potential.

How does the global imperative drive the direct air capture system market to scale up and meet climate targets?

Meeting worldwide climate goals requires the removal of billions of tons of CO2, making the large-scale deployment of DAC systems specific. This scale-up imperative drives market investment, supply chain development, and infrastructure planning. As more large-scale plants are declared and built, economies of scale increase, investor confidence grows, and costs decline. The sheer magnitude of future demand plays a crucial role as a market pull factor for DAC technologies. Hence, the recognition that massive deployment is needed becomes a catalyst for the worldwide direct air capture system market.

Restraints

Limited commercial track record and immature technology negatively impact the market progress

Several DAC technologies are still in demonstration or pilot stages, with comparatively lower technology-readiness levels than sophisticated industrial processes. The restricted number of large-scale commercial plants and the lack of long-term performance data create uncertainty for investors. This 'valley of death' between full and pilot deployment means that several innovations are delayed or stalled, thus slowing cost reductions and hindering rapid industry growth.

Opportunities

How does the integration with carbon utilization and new revenue models offer advantageous conditions for the development of the direct air capture system market?

Beyond pure sequestration, DAC systems can feed into utilization pathways (for instance, building materials, chemicals, synthetic fuels), opening new revenue streams and business models. For example, a pilot unit by a major company declared that captured CO2 could be used to produce more sustainable chemicals and fuels. This diversification raises the appeal of DAC investments, as it assimilates removal value with product value. As modular carbon-utilization value chains progress, DAC's economic case augments. Hence, utilization integration offers a significant growth opportunity in the direct air capture system industry.

Challenges

Competition with other carbon removal options & commercial viability restrict the market growth

DAC competes with other removal solutions, such as point-source capture and nature-based solutions, which typically offer perceived risk and low cost. Since the market for carbon removal progresses, DAC should justify its higher costs and energy intensity through unique value (for instance, hard-to-abate sectors, permanent removal). Reports indicate that the 'valley of death' between pilot projects and commercial viability remains substantial. Additionally, resource limitations (land, water, and clean energy) may restrict DAC growth than alternatives. This viability and competition pressure is a fundamental structural challenge.

Direct Air Capture System Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Direct Air Capture System Market |

| Market Size in 2024 | USD 220 Million |

| Market Forecast in 2034 | USD 3,940 Million |

| Growth Rate | CAGR of 43.80% |

| Number of Pages | 215 |

| Key Companies Covered | Climeworks AG, Carbon Engineering Ltd., Heirloom Carbon Technologies, Skytree B.V., Global Thermostat, Carbyon, CarbonCapture Inc., Greenlyte Carbon Technologies, Mission Zero Technologies, NEG8 Carbon, Aircela Inc., NeoCarbon GmbH, Soletair Power, Deep Sky, TerraFixing Inc., and others. |

| Segments Covered | By Product, By Scale, By Application, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Direct Air Capture System Market: Segmentation

The global direct air capture system market is segmented based on product, scale, application, and region.

Based on product, the global direct air capture system industry is divided into absorption-based DAC, adsorption-based DAC, membrane-based DAC, and cryogenic-based DAC. The adsorption-based DAC segment has registered a leading share, as it utilizes liquid or solid sorbents to capture CO2 directly from the air. They are currently the most extensively deployed due to their easier regeneration and higher efficiency. These systems are scalable, flexible, and compatible with renewable energy sources. Their growing adoption in industrial and commercial projects boosts their market rank.

Based on scale, the global direct air capture system market is segmented into pilot-scale, demonstration-scale, and commercial-scale. The commercial-scale segment held leadership in the market because larger plants (capturing thousands of tons of CO2 per year or more) are now planned or underway, denoting the transition from pilot/demonstration to full-scale operations.

Based on application, the global market is segmented into Carbon Capture and Storage (CCS) and Carbon Capture and Utilization (CCU). The Carbon Capture and Storage (CCS) segment held a dominant share of the market, as several DAC projects are oriented towards capturing CO2 and permanently storing it underground or in geological formations. It appeals to governments and industries seeking a durable carbon-removal solution and supports regulatory mandates for reducing harmful emissions.

Direct Air Capture System Market: Regional Analysis

What enables North America to have a strong foothold in the global Direct Air Capture System Market?

North America is likely to maintain its leadership in the direct air capture system market due to its substantial market share and revenue dominance, supportive government policies and financial incentives, and the presence of leading technology providers and an R&D ecosystem. North America registered for nearly 48.3% of the worldwide industry in 2024, making it the leading regional contributor. The sizable share reflects a concentration of investment, infrastructure, and deployment relative to other regions. The early dominance creates a virtuous cycle; more projects result in more experience, which reduces barriers to entry.

Moreover, in the United States, legislation such as tax credits, including the 45Q incentive and the Inflation Reduction Act, has offered substantial funding and subsidies for DAC and carbon capture and removal solutions. For instance, funding programs accounting for billions of dollars have been committed to regional DAC hubs. These policies reduce investment risk and appeal to public and private sector involvement, allowing for large deployments ahead of many regions.

Furthermore, North America hosts a large population of the world's active DAC companies; nearly half of the startups in the field are situated in Canada and the United States. This concentrated network amplifies pilot-to-commercial scale transitions, innovation, and technology cost reductions. The presence of premier research institutions and corporate associations makes the region a hub for innovation in DAC.

Europe continues to hold the second-highest share in the direct air capture system industry, driven by the growing size of the industry, rapid growth forecasts, existing infrastructure, industrial demand, and innovation ecosystems, as well as its dominance in DAC-specific companies. Europe's DAC industry is expected to experience strong growth; for instance, it is projected to reach USD 607.9 million by 2030, implying a compound annual growth rate of nearly 61.5% between 2025 and 2030. This rapid growth underscores the region's standing as a leading and growing market for DAC technology. Nations such as the Nordic region, the Netherlands, and the UK are actively involved in pilot and demonstration DAC projects.

Moreover, the region has developed carbon storage and CO2 Transport infrastructure, and major industrial sectors with residual emissions require negative-emission solutions. Europe is home to pioneering companies in the DAC domain, primarily the Swiss firm Climeworks AG, and boasts a robust research and development (R&D) ecosystem for modular systems, sorbents, and permanent storage solutions.

According to the sources, nearly 13% of active DAC startups are situated in the Netherlands and the UK each, with Germany accounting for 8%. This concentration of advancement supports the region's role as a strong secondary market for DAC deployment.

Direct Air Capture System Market: Competitive Analysis

The leading players in the global direct air capture system market are:

- Climeworks AG

- Carbon Engineering Ltd.

- Heirloom Carbon Technologies

- Skytree B.V.

- Global Thermostat

- Carbyon

- CarbonCapture Inc.

- Greenlyte Carbon Technologies

- Mission Zero Technologies

- NEG8 Carbon

- Aircela Inc.

- NeoCarbon GmbH

- Soletair Power

- Deep Sky

- TerraFixing Inc.

Direct Air Capture System Market: Key Market Trends

Technology improvements and cost reduction:

Improvements in sorbent materials, energy efficiency, and system designs are reducing both operational and capital costs. Solid sorbents and modular systems are becoming more scalable and efficient. These advancements are making DAC progressively commercially viable and competitive.

Integration with renewables and diversified applications:

DAC systems are increasingly coupled with renewable energy to reduce their carbon footprint. Flexible and modular designs enable deployment in varied locations. Captured CO2 is being utilized not only for storage but also for generating fuels, construction materials, and chemicals, thereby creating new revenue streams.

The global direct air capture system market is segmented as follows:

By Product

- Absorption-based DAC

- Adsorption-based DAC

- Membrane-based DAC

- Cryogenic-based DAC

By Scale

- Pilot-scale

- Demonstration-scale

- Commercial-scale

By Application

- Carbon Capture and Storage (CCS)

- Carbon Capture and Utilization (CCU)

By Region

- North America

- The U.S.

- Canada

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Southeast Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Table Of Content

Methodology

FrequentlyAsked Questions

A direct air capture system captures carbon dioxide directly from the atmosphere with filters or chemical sorbents. The extracted CO2 can then be stored underground or reused in industrial applications. This technology supports global climate goals by reducing atmospheric CO2 levels and complementing other emission reduction strategies for a more sustainable future.

The global direct air capture system market is projected to grow due to increasing global net-zero and carbon-neutrality targets, growth in carbon utilization markets (CO₂ to fuels, building materials, and chemicals), and integration opportunities with renewable and low-carbon energy systems.

According to study, the global direct air capture system market size was worth around USD 220 million in 2024 and is predicted to grow to around USD 3,940 million by 2034.

The CAGR value of the direct air capture system market is expected to be approximately 43.80% from 2025 to 2034.

Emerging trends in DAC include modular systems, advanced sorbents, renewable integration, expanded CO₂ utilization, and new capture technologies.

North America is expected to lead the global direct air capture system market during the forecast period.

The United States is a major contributor to the global direct air capture system market.

The key players profiled in the global direct air capture system market include Climeworks AG, Carbon Engineering Ltd., Heirloom Carbon Technologies, Skytree B.V., Global Thermostat, Carbyon, CarbonCapture Inc., Greenlyte Carbon Technologies, Mission Zero Technologies, NEG8 Carbon, Aircela Inc., NeoCarbon GmbH, Soletair Power, Deep Sky, and TerraFixing Inc.

The competitive landscape in the global direct air capture system market is moderately fragmented and highly dynamic, featuring a mix of major industrial players, specialist technology innovators, and strategic partnerships that compete through innovation, alliances, and cost-reduction efforts.

The report examines key aspects of the direct air capture system market, including a detailed analysis of existing growth factors and restraints, as well as an examination of future growth opportunities and challenges that will impact the market.

HappyClients