Digital Infrastructure Market Size, Share, Trends, Growth and Forecast 2034

Digital Infrastructure Market By Deployment Model (On-Premise, Public Cloud IaaS, Edge/Far-Edge, Hybrid/Multi-Cloud, and Colocation), By Infrastructure Layer (Data Center Facilities, Cloud Compute and Storage, Network Connectivity (Fiber, 5G, Satellite), AI Accelerators and Specialized Chips, Infrastructure Software and Management, and Others), By Enterprise Size (Small and Medium Enterprises (SMEs) and Large Enterprises), By Industry Vertical (IT and Telecom, Manufacturing and Industrial, BFSI, Retail and E-commerce, Government and Defense, Healthcare and Life Sciences, Media and Entertainment, Energy and Utilities, and Others), and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2026 - 2034

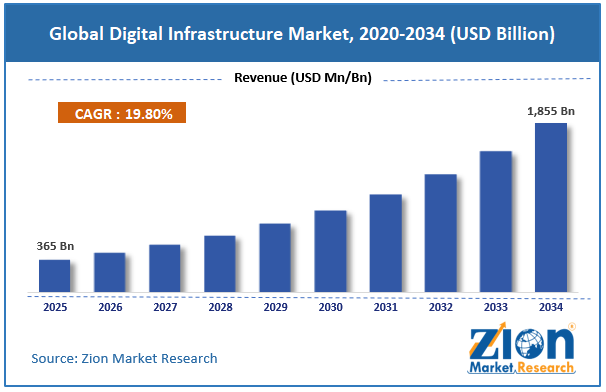

| Market Size in 2025 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 365 Billion | USD 1,855 Billion | 19.8% | 2025 |

Digital Infrastructure Industry Perspective:

What will be the size of the global digital infrastructure market during the forecast period?

The global digital infrastructure market size was worth around USD 365 billion in 2025 and is predicted to grow to around USD 1,855 billion by 2034, with a compound annual growth rate (CAGR) of roughly 19.8% between 2026 and 2034.

Key Insights

- As per the analysis shared by our research analyst, the global digital infrastructure market is estimated to grow annually at a CAGR of around 19.8% over the forecast period (2026-2034).

- In terms of revenue, the global digital infrastructure market size was valued at around USD 365 billion in 2025 and is projected to reach USD 1,855 billion by 2034.

- Increasing digital transformation across industries is expected to propel the digital infrastructure market over the projected period.

- Based on the deployment model, the colocation segment holds a significant market share in 2025 of 36%.

- Based on the infrastructure layer, the AI accelerators and specialized chips segment held the largest revenue share in 2025 of 30%.

- Based on the enterprise size, the large enterprises segment held the prominent market share of 59% in 2025.

- Based on the industry vertical, the IT and telecom segment captures a significant revenue share in 2025 of 25%.

- Based on region, North America dominates the market with a major revenue share of 39% in 2025.

Digital Infrastructure Market: Overview

Digital Infrastructure refers to the basic framework that enables the generation, storage, processing, transfer, and management of digital information and services. Some elements of digital infrastructure include data centers, cloud computing centers, communication infrastructure such as fiber optics and 5G, edge computing, Internet of Things (IoT), cybersecurity, and software infrastructure for managing digital processes. Digital infrastructure lays the foundation for digital transformation through connectivity, fast data transmission, automation, and the availability of digital services. In view of the increased use of artificial intelligence, cloud computing, smart devices, and digital government services, along with the growing need for high-speed connectivity and IT infrastructure, digital infrastructure has become increasingly significant.

Impact of the USA-Israel War on Iran on the Digital Infrastructure Market

The US-Israeli spat over Iran has had a mixed impact on the digital infrastructure market. In the short term, increased hacking risks, concerns about the security of data centers, telecommunications networks, and other vital digital resources are being exacerbated by escalating geopolitical tensions, disrupting internet connectivity in affected areas. These developments are driving governments and companies to invest more in cybersecurity, network resilience, sovereign cloud infrastructure, disaster recovery, and the protection of key infrastructure, creating new growth opportunities for digital infrastructure providers. But the violence has also led to supply chain disruptions, stalled infrastructure projects in parts of the Middle East, and increased operational, security, and risk management costs.

Digital Infrastructure Market: Dynamics

Growth Drivers

Why does the rapid adoption of cloud computing and data centers drive the digital infrastructure market?

Cloud computing and hyperscale data centers are rapidly becoming key drivers of growth in the digital infrastructure market as businesses continue to shift their workloads to cloud platforms for AI, big data analytics, and digital transformation. To keep up with the growing demand for computing power, major tech companies are investing in developing cloud infrastructure. Specifically, Oracle announced plans to raise US$45-50 billion by 2026 to expand the capacity of Oracle Cloud Infrastructure (OCI) for major AI companies such as OpenAI, NVIDIA, Meta, and xAI. Furthermore, Meta has announced an investment of approximately C$13 billion (US$9.17 billion) to build its first AI data center in Alberta, Canada. This is a major move that will help develop cloud infrastructure, boost data center capacity, and increase the deployment of digital services.

Restraints

High capital investment requirements hamper the growth of the digital infrastructure industry

The need for significant capital investment remains a major factor limiting the digital infrastructure industry, as the creation and upgrade of data centers, fiber-optic networks, 5G infrastructure, edge computing resources, and power and cooling systems require substantial upfront investment. Apart from the cost of infrastructure creation, there is also the cost of purchasing powerful servers, networking infrastructure, security tools, and energy-saving technology, as well as other expenses related to the operation and maintenance of such infrastructure. Financial constraints could slow the development of digital infrastructure, especially for SMEs and companies in developing countries with limited access to finance.

Opportunities

How does increasing investment by key market players present a lucrative opportunity for the digital infrastructure market?

The increasing investment by key market players is expected to create opportunities for the digital infrastructure market. For instance, in July 2026, Tata Communications, a top-tier global communications technology company, invested strategically in subsea cable capacity by acquiring major fiber capacity along the subsea cable link to support its connectivity services connecting the AI hotspots of Mumbai and Chennai in India and Singapore, Asia's leader in the cloud and AI ecosystem. This investment has been made to meet the rising bandwidth and AI-driven data requirements of enterprises in Asia and beyond. The subsea link connecting India and Singapore will emerge as one of the world's most important digital corridors, providing high-capacity, low-latency connectivity for the transit of critical enterprise, cloud, and hyperscaler traffic from India, Southeast Asia, and other global destinations. With its investment in expanding the capacity of its TGN network, Tata Communications will be able to offer better, diverse, agile, and high-performing connectivity to its customers. Overall, these investments will help to meet the increasing needs of the Data Center (DC) ecosystem for enterprises.

Challenges

How does the shortage of skilled IT and network professionals pose a significant challenge for the digital infrastructure market?

A shortage of experienced IT and networking professionals is one of the problems hindering the digital infrastructure market, as companies may lack the skills to develop, operate, secure, and manage increasingly complex digital infrastructure. Indeed, the rapid rise of cloud computing, AI technologies, 5G networks, edge computing, cybersecurity measures, and hyperscale data centers is creating a need for specialists in cloud architecture, network engineering, cybersecurity, data center operations, and AI infrastructure. There are not enough experts to perform such tasks and meet this demand, leading to a shortage of talent, higher costs, and longer project implementation periods. As a consequence, enterprises and service providers experience delays in implementing their infrastructure, higher risks in their activities, and higher outsourcing costs.

Digital Infrastructure Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Digital Infrastructure Market |

| Market Size in 2025 | USD 365 Billion |

| Market Forecast in 2034 | USD 1,855 Billion |

| Growth Rate | CAGR of 19.8% |

| Number of Pages | 228 |

| Key Companies Covered | Amazon Web Services, Google LLC (Alphabet), Alibaba Cloud, Microsoft Corporation, Huawei Technologies Co. Ltd., IBM Corporation, Cisco Systems Inc., Equinix Inc., Oracle Corporation, Schneider Electric SE, Digital Realty Trust, Nokia Corporation, Vertiv Holdings Co., CoreWeave Inc., NTT Ltd., Cloudflare Inc., NVIDIA Corporation, Arista Networks Inc., Dell Technologies Inc., Ericsson AB, and others. |

| Segments Covered | By Deployment Model, By Infrastructure Layer, By Enterprise Size, By Industry Vertical, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 to 2024 |

| Forecast Year | 2026 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Digital Infrastructure Market: Segmentation

Deployment Model Insights

Why does the colocation segment hold a prominent position in the digital infrastructure market?

The colocation segment holds a significant share of the digital infrastructure market in 2025, of 36%. The increase in segment growth is due to the increasing need for scalable, secure, and cost-effective IT infrastructure, driven by cloud migration, artificial intelligence (AI), hybrid cloud, and edge computing implementations in enterprises. Rather than setting up a privately owned data center, enterprises have started opting for colocation services, which help them save on capital expenditures and provide access to high-end networking, reliable power, cooling systems, and connections to different cloud providers. The rise in demand from hyperscale cloud companies, banks, hospitals, and digital service providers for highly resilient, low-latency infrastructure will drive revenue growth in this segment.

There are additional product innovations that would drive revenue growth in this segment. For instance, Equinix announced the launch of its new IBX data center, HK6, which is ready to accommodate AI applications in Hong Kong in June 2026. The new data center is equipped with liquid cooling technology and high-density AI infrastructure.

Furthermore, it offers low-latency connectivity to the Hong Kong–Shenzhen Innovation and Technology Park and was built with an investment of US$124 million. In addition, Equinix launched its Distributed AI Hub and Fabric Intelligence platform, enabling enterprises to safely set up and operate their distributed AI infrastructure using AI-driven network automation across cloud, edge, and colocation environments.

Infrastructure Layer Insights

Why do AI accelerators and specialized chips capture the largest share in the digital infrastructure market?

The AI accelerators and specialized chips segment held the largest revenue share of the digital infrastructure industry in 2025, of 30%. The growth is being fueled by the rapid adoption of generative AI, LLMs, HPC, and data analytics solutions across companies, CSPs, and research organizations. AI tasks require much more processing power than existing computing hardware can provide. There is a growing need for GPUs, TPUs, NPUs, AI inference accelerators, and AI chips that can deliver enhanced performance, reduced latency, and power efficiency. The rise of the hyperscale data centers, AI factories, edge AI projects, and sovereign AI efforts is also accelerating the demand for semiconductor solutions.

Enterprise Size Insights

Does the large enterprises segment capture the largest share in the digital infrastructure market?

The large enterprises segment held the prominent digital infrastructure market share of 59% in 2025. The growth in the segment is due to significant investment in cloud computing, artificial intelligence (AI), big data analytics, cybersecurity, and digital transformation initiatives. Enterprises create and process large volumes of data, making it essential for them to have high-performance data centers, hybrid & multi-clouds, edge computing, high-performance network services, and secure digital infrastructure to carry out critical functions. Enterprises have more financial resources available to deploy hyperscale infrastructure, private clouds, AI-enabled computing systems, and business continuity measures.

Additionally, the growing use of automation, IoT, ERP, and real-time analytics across verticals such as finance, healthcare, manufacturing, retail, and telecommunications is driving demand for robust, energy-efficient digital infrastructure. With ongoing efforts towards modernizing IT infrastructure to enhance efficiency and security and deliver a superior customer experience, the large enterprises segment is likely to register significant revenue growth in the global digital infrastructure market.

Industry Vertical Insights

Does the IT and telecom segment capture the largest share in the digital infrastructure market?

The IT and telecom segment captures a significant revenue share of the digital infrastructure industry in 2025 of 25%. This trend is spurred by the fast growth of cloud computing services, 5G networks, fiber broadband networks, edge computing, and increased worldwide data flow. Companies in information technology and telecommunications need scalable and secure infrastructure for digital communication, cloud-native apps, artificial intelligence (AI), the Internet of Things (IoT), and real-time data processing.

Moreover, the development of SDN (software-defined networking), NFV (network function virtualization), and open networks leads to increased investment in advanced data centers, high-performance networking equipment, and AI-powered network management systems.

Regional Insights

Why does North America lead the digital infrastructure market?

North America dominates the digital infrastructure market, accounting for 39% of revenue in 2025. The key drivers of the regional market growth are the region's advanced cloud ecosystem, AI, the growth of hyperscale data centers, 5G, and government-supported policies for broadband and digital connectivity. The United States and Canada continue to make significant investments in upgrading their digital infrastructure, increasing the availability of high-speed internet, enhancing cybersecurity, and driving economic growth through AI.

One significant factor in this matter is the U.S. government's BEAD Program, which will distribute US$42.45 billion to expand high-speed broadband infrastructure in unserved and underserved areas. By 2026, most states and territories in the United States will have received approval for their deployment plans, thereby accelerating broadband development and stimulating investment in fiber-optic networks, data centers, and digital connectivity.

Digital Infrastructure Market: Competitive Analysis

The global digital infrastructure market is dominated by players like:

- Amazon Web Services

- Google LLC (Alphabet)

- Alibaba Cloud

- Microsoft Corporation

- Huawei Technologies Co. Ltd.

- IBM Corporation

- Cisco Systems Inc.

- Equinix Inc.

- Oracle Corporation

- Schneider Electric SE

- Digital Realty Trust

- Nokia Corporation

- Vertiv Holdings Co.

- CoreWeave Inc.

- NTT Ltd.

- Cloudflare Inc.

- NVIDIA Corporation

- Arista Networks Inc.

- Dell Technologies Inc.

- Ericsson AB

The global digital infrastructure market is segmented as follows:

By Deployment Model

- On-Premise

- Public Cloud IaaS

- Edge/Far-Edge

- Hybrid/Multi-Cloud

- Colocation

By Infrastructure Layer

- Data Center Facilities

- Cloud Compute and Storage

- Network Connectivity (Fiber, 5G, Satellite)

- AI Accelerators and Specialized Chips

- Infrastructure Software and Management

- Others

By Enterprise Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

By Industry Vertical

- IT and Telecom

- Manufacturing and Industrial

- BFSI

- Retail and E-commerce

- Government and Defense

- Healthcare and Life Sciences

- Media and Entertainment

- Energy and Utilities

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table Of Content

Methodology

FrequentlyAsked Questions

Digital Infrastructure refers to the basic framework that enables the generation, storage, processing, transfer, and management of digital information and services. Some elements of digital infrastructure include data centers, cloud computing centers, communication infrastructure such as fiber optics and 5G, edge computing, Internet of Things (IoT), cybersecurity, and software infrastructure for managing digital processes.

The digital infrastructure market is primarily driven by the rapid adoption of cloud computing, artificial intelligence (AI), big data analytics, and edge computing, which is increasing demand for high-performance data centers and advanced networking infrastructure. The expansion of 5G networks, fiber-optic broadband, and Internet of Things (IoT) deployments is further accelerating investments in digital connectivity.

The digital infrastructure market faces several challenges, including high capital investment requirements for data centers, fiber-optic networks, and 5G infrastructure, which can limit deployment, particularly in developing regions. The market is also constrained by a shortage of skilled IT and network professionals, which increases cybersecurity and data privacy risks, complicates integration with legacy systems, and drives rising energy consumption associated with digital infrastructure.

Based on the industry vertical, the IT and telecom card segment is expected to dominate the Digital Infrastructure market growth during the projected period.

Key emerging trends and innovations in the digital infrastructure market include the rapid deployment of AI-ready data centers, liquid cooling technologies, edge computing, and hyperscale cloud infrastructure to support generative AI and high-performance computing workloads. The market is also witnessing increased adoption of software-defined networking (SDN), network automation, hybrid and multi-cloud architectures, and AI-driven infrastructure management.

According to the report, the global digital infrastructure market size was worth around USD 365 billion in 2025 and is predicted to grow to around USD 1,855 billion by 2034.

The global digital infrastructure market is expected to grow at a CAGR of 19.8% during the forecast period.

The global digital infrastructure industry growth is expected to be led by North America over the forecast period.

The global digital infrastructure market is dominated by players like Amazon Web Services, Google LLC (Alphabet), Alibaba Cloud, Microsoft Corporation, Huawei Technologies Co. Ltd., IBM Corporation, Cisco Systems Inc., Equinix Inc., Oracle Corporation, Schneider Electric SE, Digital Realty Trust, Nokia Corporation, Vertiv Holdings Co., CoreWeave Inc., NTT Ltd., Cloudflare Inc., NVIDIA Corporation, Arista Networks Inc., Dell Technologies Inc., and Ericsson AB, among others.

The digital infrastructure market report covers the geographical market along with a comprehensive competitive landscape analysis. It also includes cash flow analysis, profit ratio analysis, market basket analysis, market attractiveness analysis, sentiment analysis, PESTLE analysis, trend analysis, SWOT analysis, trade area analysis, demand & supply analysis, Porter’s five forces analysis, and value chain analysis.

HappyClients