Lab-Grown Diamond Jewellery Market Size, Share, Trends, Growth 2034

Lab-Grown Diamond Jewellery Market By Product Category (Rings, Earrings, Necklaces, Pendants, Bracelets & Bangles, Bridal Jewellery Sets, Chains, Nose Pins, Men's Jewellery, and Others), By Diamond Size (Below 0.50 Carat, 0.50–1.00 Carat, 1.01–2.00 Carat, and Above 2.00 Carat), By Metal Type (Gold (14K), Gold (18K), Gold (22K), Platinum, Silver, and Other Metals), By Price Range (Economy, Mid-Range, Premium, and Luxury), By Consumer Age Group (Gen Z (18–24 Years), Young Millennials (25–34 Years), Older Millennials (35–44 Years), Gen X (45–60 Years), and Above 60 Years), By Gender (Women, Men, and Unisex), By Distribution Channel (Brand-Owned Stores, Multi-brand Jewellery Stores, Online Brand Websites, E-commerce Marketplaces, Omnichannel Retail, and Others), and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034-

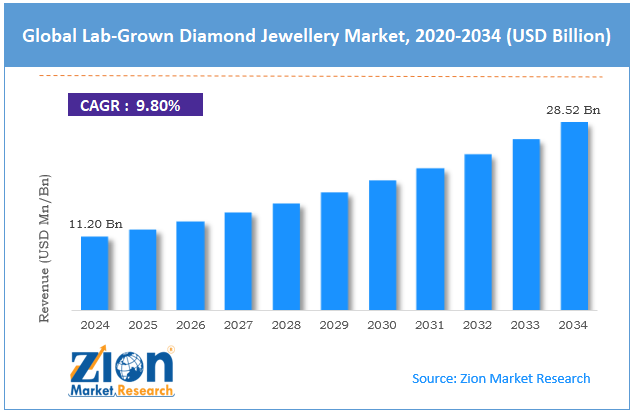

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 11.20 Billion | USD 28.52 Billion | 9.80% | 2024 |

Global Lab-Grown Diamond Jewellery Industry Perspective:

What will be the global Lab-Grown Diamond Jewellery market size during the forecast period?

The global Lab-Grown Diamond Jewellery market size was worth around USD 11.20 billion in 2024 and is predicted to reach around USD 28.52 billion by 2034, with a compound annual growth rate (CAGR) of roughly 9.80% between 2025 and 2034. The Lab-Grown Diamond Jewellery Market is driven by growing consumer preference for sustainable, ethical, and affordable luxury jewellery among millennials and Gen Z.

Key Insights

- As per the analysis shared by our research analyst, the Lab-Grown Diamond Jewellery market is projected to expand annually at a CAGR of around 9.80% over the forecast period (2025-2034).

- In terms of revenue, the market size was valued at nearly USD 11.20 billion in 2024 and is anticipated to reach USD 28.52 billion by 2034.

- The market is driven by the significant affordability factor allowing consumers to purchase larger carat stones for standard budgets, alongside a heavy demographic alignment with millennial and Gen Z ethical purchasing trends.

- Based on the Product Category, the Rings segment dominated the market with a share of over 45% because engagement and wedding bands act as the primary structural gateway for fine diamond purchases globally.

- Based on the Diamond Size, the 1.01–2.00 Carat segment held the largest share of approximately 38% due to providing the ideal balance of visual scale and optimized retail pricing for modern couples.

- Based on the Metal Type, the Gold (18K) segment dominated with a share of 42% because it offers the classic structural density and chemical stability expected of premium fine jewellery settings.

- Based on the Price Range, the Mid-Range segment dominated with a share of 52% as it precisely hits the mass-affordability sweet spot that attracts everyday fashion consumers and middle-income bridal buyers.

- Based on the Consumer Age Group, the Young Millennials (25–34 Years) segment dominated with a share of 48% because this specific cohort represents the peak marrying demographic seeking high-value alternatives to natural stones.

- Based on the Gender, the Women segment dominated with a share of 68% due to historic luxury alignment and the ongoing surge in self-purchasing female fashion consumers.

- Based on the Distribution Channel, the Omnichannel Retail segment dominated with a share of 35% as modern jewellery shoppers demand seamless integration between online digital discovery and secure in-store physical consultation.

- North America dominated the global market with a share of 44% in 2024 due to extraordinarily high consumer awareness levels, a robust bridal industry, and deep corporate retail penetration across regional shopping centers.

Global Lab-Grown Diamond Jewellery Market: Overview

The lab-grown diamond jewellery market encompasses the manufacturing, retail distribution, and commercial sales of ornamental pieces utilizing diamonds cultivated through controlled advanced scientific methods. These diamonds carry the exact physical, optical, and chemical compositions of mined stones but are structured within specialized laboratory conditions using advanced technological techniques. The finished products are beautifully integrated into premium luxury settings, including bridal rings, necklaces, and custom everyday fashion pieces, establishing a new paradigm within fine jewellery markets.

The market dynamics are heavily shaped by structural shifts in modern luxury spending habits worldwide. Broad macro-environmental drivers center around evolving consumer demographics and rapid technological optimizations in gemstone manufacturing processes. Conversely, the rapid inflation of production capacities and subsequent downward shifts in loose gemstone prices present a continuous structural restraint to long-term inventory valuations. High-growth avenues emerge from specialized designer collections and the creation of highly branded omnichannel luxury footprints. At the same time, maintaining long-term consumer trust while defending brand differentiation against generic clothing accessories stands as a prominent market challenge.

Global Lab-Grown Diamond Jewellery Market: Dynamics

Growth Drivers

How is the distinct affordability profile transforming consumer access to luxury jewellery?

The significant price differential between lab-cultivated stones and historically mined diamonds acts as the most aggressive engine driving current market adoption rates. Lab-grown diamonds consistently retail at a fraction of the cost of natural counterparts with identical visual clarity, allowing consumer budgets to go much further. Buyers who would typically be constrained to small fractions of a carat can comfortably buy multi-carat premium rings, fundamentally shifting consumer expectations within the fine jewellery market.

Furthermore, this financial accessibility expands the target consumer base beyond classic special occasions and formal bridal engagements into the rapid self-purchasing fashion category. Modern buyers are increasingly incorporating diamond earrings, pendants, and tennis bracelets into their standard rotating wardrobes. The dramatic lowering of entry-level pricing structures encourages repeat purchases, boosting total volume consumption across modern global distribution networks.

Restraints

Are rapid reductions in generic gemstone prices challenging long-term store valuations?

The continuous advancement of technology has dramatically optimized lab manufacturing throughput, leading to a massive increase in loose diamond supply volumes globally. This abundant production capacity creates intense price competition among generic producers, putting downward pressure on the per-carat wholesale value of lab-created stones. Traditional luxury consumers who view fine jewelry as a long-term asset store may hesitate to purchase items that display a depreciating wholesale price curve.

Additionally, retail operations must handle complex inventory management hurdles due to these rapidly changing price points. Jewelry brands risk holding stock that depreciates before retail fulfillment, compressing structural margins if they do not manage supply lines effectively. This ongoing price volatility can alienate traditional luxury retailers, who may limit showcase space to protect overall store profitability.

Opportunities

Can the expansion of custom designer collections unlock hidden premium margins?

The unique flexibility of lab-grown diamonds allows designers to push past the geometric limits of traditional mined stones. Laboratories can grow bespoke crystalline shapes and specialized custom tints that would be rare or expensive to source from nature. This creates a lucrative opportunity for luxury fashion houses to curate exclusive capsule collections featuring unique colors and cuts, shifting consumer focus from raw carat value to creative artistry.

Moreover, the expansion of high-profile, celebrity-backed sustainable fashion partnerships creates a powerful tool to elevate brand status. By anchoring lab-grown collections within high-end designer contexts, brands can distance their items from generic bulk commodities. This shift from simple stone replication to dedicated luxury branding helps companies capture healthy premium margins from affluent, style-conscious consumers.

Challenges

How does the rise of deceptive product labeling threaten long-term consumer confidence?

As the volume of lab-grown diamonds rising across global trade channels grows, maintaining clear product separation at the retail level has become a critical operational challenge. Incidents of lower-tier suppliers mixing uncertified lab stones into natural diamond shipments can undermine trust across the entire jewelry ecosystem. Retailers must invest heavily in advanced screening tools and verification workflows to ensure that consumers receive completely accurate, transparent product documentation.

At the same time, navigating the crowded marketing landscape presents a major hurdle for new brands. With numerous generic alternatives entering digital marketplaces, simply labeling an item "eco-friendly" is no longer enough to stand out. Brands must work hard to differentiate themselves through superior craftsmanship, unique retail experiences, and verified supply chain tracking to avoid being grouped with low-cost fashion jewelry.

Lab-Grown Diamond Jewellery Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Lab-Grown Diamond Jewellery Market |

| Market Size in 2024 | USD 11.20 Billion |

| Market Forecast in 2034 | USD 28.52 Billion |

| Growth Rate | CAGR of 9.80% |

| Number of Pages | 235 |

| Key Companies Covered | Pandora, Brilliant Earth, Diamond Foundry, VRAI, Blue Nile, James Allen, Lightbox Jewelry, Clean Origin, Aether Diamonds, Novita Diamonds, Lusix, WD Lab Grown Diamonds, Pure Grown Diamonds, Swarovski, Signet Jewelers, and others. |

| Segments Covered | By Product Category, By Diamond Size, By Metal Type, By Price Range, By Consumer Age Group, By Gender, By Distribution Channel, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, The Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 - 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Global Lab-Grown Diamond Jewellery Market: Segmentation

The Lab-Grown Diamond Jewellery market is segmented by product category, diamond size, metal type, price range, consumer age group, gender, distribution channel, and region.

Based on Product Category, the lab-grown diamond jewellery market is divided into rings, earrings, necklaces, pendants, bracelets & bangles, bridal jewellery sets, chains, nose pins, men's jewellery, and others. The Rings segment stands as the absolute dominant category in the market. Its leading market position is driven by its strong connection to the bridal sector, where engagement rings and wedding bands serve as the traditional entry point for diamond purchases. This segment's high volume helps to drive the overall market forward by sustaining high-capacity production orders for raw material chemical suppliers globally. The second most dominant application category is Earrings, driven by the massive deployment of stud and hoop designs that serve as popular entry-level gifts and daily fashion items.

Based on Diamond Size, the lab-grown diamond jewellery market is divided into below 0.50 carat, 0.50–1.00 carat, 1.01–2.00 carat, and above 2.00 carat. The 1.01–2.00 Carat segment is the most dominant in the market. The dominance of this segment is powered by the significant cost-savings of lab-grown stones, which allows middle-class consumers to easily step up to the popular one-and-a-half to two-carat look. This ideal balance of visual scale and optimized retail pricing helps to drive high volume consumption across the value chain. The second most dominant segment is 0.50–1.00 Carat, which remains popular among specialized fashion centers that require specific accents and everyday jewelry pieces.

Based on Metal Type, the lab-grown diamond jewellery market is divided into Gold (14K), Gold (18K), Gold (22K), Platinum, Silver, and Other Metals. The Gold (18K) segment represents the dominant choice for premium settings. Its leading position is driven by its classic density and standard purity, making it the preferred choice for showcasing high-clarity lab stones in engagement and fine jewelry pieces. The second most dominant metal segment is Platinum, which is highly sought after by younger consumers for its hypoallergenic qualities and modern silver-white appearance that highlights colorless gemstones.

Based on Price Range, the lab-grown diamond jewellery market is divided into economy, mid-range, premium, and luxury. The Mid-Range segment is the most dominant as it hits the core value proposition of the industry. This segment provides high-quality, substantial carat stones at prices accessible to standard budgets, capturing the majority of bridal and milestone anniversary purchases. The second most dominant segment is Premium, which features custom cuts and designer branding aimed at more affluent shoppers who appreciate the artistic value over just the raw stone cost.

Based on Consumer Age Group, the lab-grown diamond jewellery market is divided into Gen Z (18–24 Years), young millennials (25–34 Years), older millennials (35–44 Years), Gen X (45–60 Years), and above 60 years. The Young Millennials (25–34 Years) segment represents the dominant consumer base for lab-grown jewelry. This cohort covers the peak marriage demographic and values transparency, sustainability, and smart budget choices, making them highly receptive to lab-grown alternatives. The second most dominant age segment is Gen Z (18–24 Years), an emerging group focused on self-purchasing fashion items that express personal style and values.

Based on Gender, the lab-grown diamond jewellery market is divided into women, men, and unisex. The Women segment is the most dominant due to long-standing luxury habits and the growth of self-purchasing female consumers. This segment's high demand helps drive the market forward by encouraging brands to continually update their design lines. The second most dominant segment is Unisex, which is gaining traction through modern, minimalist designs like tennis bracelets and band rings that appeal across gender demographics.

Based on Distribution Channel, the lab-grown diamond jewellery market is divided into brand-owned stores, multi-brand jewellery stores, online brand websites, E-commerce marketplaces, omnichannel retail, and others. The Omnichannel Retail segment has emerged as the most dominant and fastest-growing deployment mode. Fine jewelry purchases often involve a blend of digital research and hands-on viewing, making a seamless omnichannel approach essential for modern retailers. The second most dominant channel is Online Brand Websites, which offers clear pricing and extensive customization tools for younger consumers who prefer shopping from home.

Global Lab-Grown Diamond Jewellery Market: Regional Analysis

Why will North America continue to dominate the global market during the projection period?

North America is expected to maintain its leading position in the global Lab-Grown Diamond Jewellery market due to high consumer awareness and a strong bridal retail network. The region's dominance is primarily driven by the United States, where major jewelry chains have widely adopted lab-grown options, giving them significant visibility in malls and urban centers. Additionally, strong demand from millennial and Gen Z shoppers for ethical luxury choices supports steady market growth. The region's healthy disposable incomes and established digital shopping habits also encourage regular self-purchasing of fine fashion jewelry.

The Asia-Pacific region is anticipated to experience the highest growth rate during the forecast period. Countries like India and China are major hubs for lab-grown diamond production and are now seeing rapid domestic retail growth. The rising middle class, growing urban populations, and shifting perceptions of lab-grown gems as accessible luxury options drive this demand. Increased government support, including tax incentives and investments in production technology, further strengthens the region's position as both a top manufacturer and an expanding retail market.

Europe exhibits robust growth supported by stringent environmental standards and preference for responsible luxury. Countries like the United Kingdom and Germany emphasise traceability and design innovation in sustainable jewellery.

Latin America shows promising development through increasing urbanisation and interest in affordable luxury, with Brazil and Mexico as key contributors. The Middle East and Africa region benefits from cultural affinity for jewellery and growing investments in sustainable alternatives, particularly in the UAE and South Africa.

Recent Developments

- In April 2026, Limelight Lab Grown Diamonds expanded its retail footprint by opening a new exclusive experience boutique focused entirely on custom-designed 18K gold bridal sets.

- In January 2026, Pandora launched a dedicated lab-grown diamond collection targeting Gen Z consumers with affordable and trendy designs.

- In November 2025, Signet Jewelers updated its online configuration tools to allow shoppers to customize lab-grown diamond rings with multi-angle high-definition previews.

- In September 2025, Swarovski unveiled a new collection of laboratory-created diamonds in vibrant fancy colors, expanding its premium fashion jewelry offerings.

Global Lab-Grown Diamond Jewellery Market: Competitive Analysis

The global lab-grown diamond jewellery market is dominated by players:

- Pandora

- Brilliant Earth

- Diamond Foundry

- VRAI

- Blue Nile

- James Allen

- Lightbox Jewelry

- Clean Origin

- Aether Diamonds

- Novita Diamonds

- Lusix

- WD Lab Grown Diamonds

- Pure Grown Diamonds

- Swarovski

- Signet Jewelers

What are the key trends in the Lab-Grown Diamond Jewellery Market?

The Rising Demand for Fancy Colored Lab Diamonds

A notable trend is the growing popularity of fancy colored lab diamonds, such as pinks, blues, and yellows. Because these colors are exceptionally rare in nature, laboratory production offers a predictable, accessible way for consumers to enjoy vibrant custom gemstones at affordable prices.

The Integration of Blockchain Verification Tech

Modern brands are increasingly using blockchain technology to provide transparent tracking for their jewelry. This setup allows buyers to scan a digital code and trace their diamond's journey from the initial laboratory growth phase through cutting, polishing, and final setting, reinforcing consumer trust.

The global lab-grown diamond jewellery market is segmented as follows:

By Product Category

- Rings

- Earrings

- Necklaces

- Pendants

- Bracelets & Bangles

- Bridal Jewellery Sets

- Chains

- Nose Pins

- Men's Jewellery

- Others (Brooches, Anklets, Charms, Cufflinks, etc.)

By Diamond Size

- Below 0.50 Carat

- 0.50–1.00 Carat

- 1.01–2.00 Carat

- Above 2.00 Carat

By Metal Type

- Gold (14K)

- Gold (18K)

- Gold (22K)

- Platinum

- Silver

- Other Metals

By Price Range

- Economy

- Mid-Range

- Premium

- Luxury

By Consumer Age Group

- Gen Z (18–24 Years)

- Young Millennials (25–34 Years)

- Older Millennials (35–44 Years)

- Gen X (45–60 Years)

- Above 60 Years

By Gender

- Women

- Men

- Unisex

By Distribution Channel

- Brand-Owned Stores

- Multi-brand Jewellery Stores

- Online Brand Websites

- E-commerce Marketplaces

- Omnichannel Retail

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table Of Content

Methodology

FrequentlyAsked Questions

Lab-Grown Diamond Jewellery refers to fine decorative ornaments that feature diamonds grown in controlled laboratory settings using high-end technological processes. These diamonds share the exact chemical, physical, and visual traits of mined diamonds, offering an identical look with an eco-conscious profile.

The primary growth drivers include the cost savings over natural diamonds, growing consumer interest in ethical and sustainable sourcing, expanding retail availability, and a strong affinity among younger generations for accessible luxury.

The global market size was valued at approximately USD 11.20 billion in 2024 and is projected to reach around USD 28.52 billion by the end of 2034.

The market is expected to grow at a compound annual growth rate (CAGR) of approximately 9.80% during the forecast period from 2025 to 2034.

Key challenges include declining wholesale prices due to expanding production capacities, the potential risk of mixed or uncertified stock, and the need to differentiate brands in a highly competitive fashion jewelry landscape.

Emerging trends highlight the rising popularity of fancy colored lab diamonds, custom geometric cuts, and the use of blockchain verification systems to offer transparent supply chain tracking to consumers.

The value chain includes diamond seed sourcing and laboratory growth, precise cutting and polishing, jewelry design and metal setting, brand marketing, and final retail distribution through online and physical channels.

North America will continue to contribute a major share of market value due to established consumer adoption, while the Asia-Pacific region is anticipated to achieve the fastest growth rate.

Pandora, Brilliant Earth, Diamond Foundry, VRAI, Blue Nile, James Allen, Lightbox Jewelry, Clean Origin, Aether Diamonds, Novita Diamonds, Lusix, WD Lab Grown Diamonds, Pure Grown Diamonds, Swarovski, Signet Jewelers.

The report delivers a detailed overview of revenue trends, key growth factors, and market challenges. It includes segment breakdowns, regional projections, competitive landscape analyses, and insights into future consumer trends.

HappyClients