Inorganic Corrosion Inhibitors Market Size, Growth, Global Trends, Forecast 2034

Inorganic Corrosion Inhibitors Market By Type (Anodic Inhibitor and Cathodic Inhibitor), By Treatment (Sprays, Coatings, and Others), By Application (Oil & Gas, Chemicals & Petrochemicals, Water Treatment, Construction, Metalworking, and Others), and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

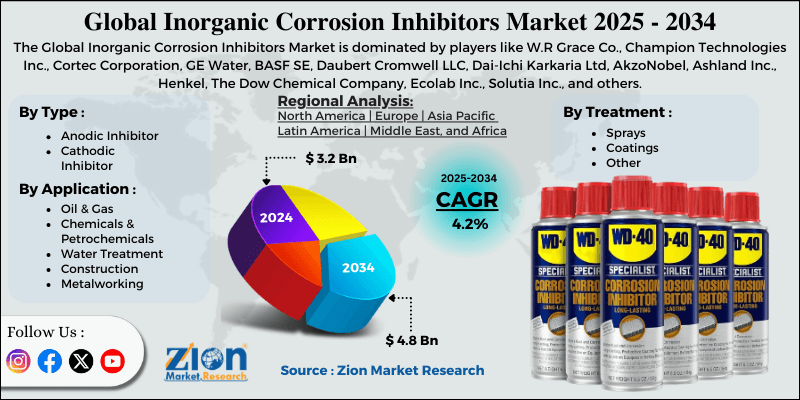

| USD 3.2 Billion | USD 4.8 Billion | 4.2% | 2024 |

Inorganic Corrosion Inhibitors Industry Perspective:

What will be the size of the global inorganic corrosion inhibitors market during the forecast period?

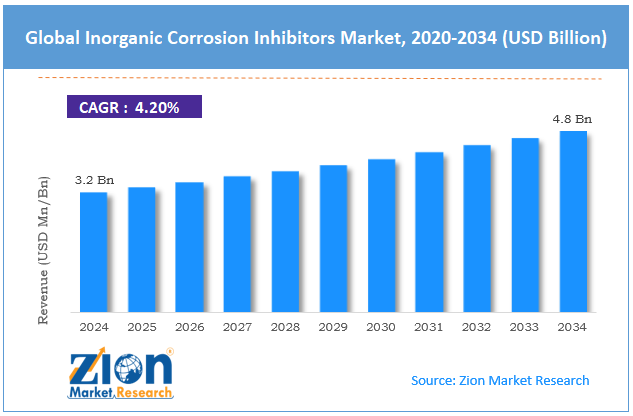

The global inorganic corrosion inhibitors market size was worth around USD 3.2 billion in 2024 and is predicted to grow to around USD 4.8 billion by 2034, with a compound annual growth rate (CAGR) of roughly 4.2% between 2025 and 2034.

Request Free SampleRequest Free SampleRequest Free Sample

Request Free SampleRequest Free SampleRequest Free Sample

Key Insights

- As per the analysis shared by our research analyst, the global inorganic corrosion inhibitors market is estimated to grow annually at a CAGR of around 4.2% over the forecast period (2025-2034).

- In terms of revenue, the global inorganic corrosion inhibitors market size was valued at around USD 3.2 billion in 2024 and is projected to reach USD 4.8 billion by 2034.

- Increasing demand from the end-use industry is expected to drive the inorganic corrosion inhibitors market.

- Based on the type, the anodic inhibitor captures the largest revenue share in 2024.

- Based on the treatment, the coatings dominate the industry growth.

- Based on the application, the oil & gas dominate the industry growth.

- Based on region, North America captures the largest revenue share in 2024.

Inorganic Corrosion Inhibitors Market: Overview

Inorganic corrosion inhibitors are chemical additives formed from mineral-based or other non-carbon sources that are included in water systems, cooling towers, and other distribution systems, boiler feeds, and oil and gas pipelines that will lessen corrosion of metal structures and components. These commonly contain nitrites, phosphates, molybdates, silicates, and chromates that create a passive film on the surface and neutralize the electrochemical interaction between the environment and the metal. This results in less oxidation or sloughing of metal ions and extends the useful life of equipment, cutting operating costs. These inorganic additives are particularly prevalent in power plant applications, petrochemical refineries, and many other manufacturing and process industries, as well as in water treatment. They are also prized for their simplicity, affordability, and durability; however, because of toxicity concerns, some systems are regulated.

Inorganic Corrosion Inhibitors Market: Dynamics

Growth Drivers

Why does the growth in the end-use sector stimulate the expansion of the inorganic corrosion inhibitors market?

Growth in end-use industry sectors will also drive market growth, as it directly increases demand for products, materials, and services required to support that sector. For instance, as production capacity, infrastructure, and operational activities in oil & gas, power & water treatment, manufacturing, and construction industries increase, a greater number of supporting inputs are needed to maintain efficient operations and to safeguard assets and machinery.

Also, expanding pipeline systems, oil and gas processing plants, cooling towers, and storage facilities results in an increased area of exposed metal components, which in turn creates a higher need for corrosion protection. Increased production levels also translate into increased hours of operation of equipment and associated increased wear and tear, thereby increasing the demand for chemicals and protective systems.

Restraints

Environmental & health concerns are hindering the industry’s growth

Environmental and health issues can be significant restrictions for industry growth. Such concerns include regulatory restrictions, higher costs of compliance, and market acceptance of innovative products. For instance, many industries that rely heavily on chemical solutions, such as inorganic corrosion inhibitors, may face constraints due to certain chemicals being classified as heavy metals or toxic materials, which negatively impact aquatic and soil fauna/flora, as well as adversely affect human health.

Moreover, with the added knowledge of the importance of preserving the environment and protecting workers, government agencies and organizations have implemented stricter regulations concerning environmental laws, use restrictions, and waste disposal. Industries that regulate many of these chemicals, therefore, have to deal with reformulation, testing, certification, and waste disposal, which in turn increases cost and decreases profit. The customers for many industries, such as water treatment, food processing, and infrastructure, are also demanding environmentally safer, non-toxic options.

Opportunities

How do the technological advancements in formulations offer a potential opportunity for the inorganic corrosion inhibitors market growth?

Innovations in formulations represent a significant opportunity for market growth, as improvements in corrosion protection deliver significant benefits to end users. Benefits include the extension of application scope, enhanced corrosion rates, and increased equipment life, which overcome many of the regulatory and environmental restrictions historically placed on the use of certain chemicals to combat corrosion. In addition, new formulations can maintain or improve performance by formulating more effective corrosion inhibitors.

For instance, improved inorganic corrosion inhibitors with increased solubility because of superior film-forming characteristics and increased protection over a wider range of temperatures, metals, and pH levels. Such innovations can make the corrosion inhibitor easier to apply in an industrial environment and reduce costs. Advanced formulations can also enhance corrosion protection by reducing toxicity levels to either comply with regulatory directives or make the product more attractive to the end user in terms of environmental impact or cost-performance ratio. This phenomenon, in turn, opens up new geographic markets, since previously restricted areas become available.

Challenges

Why are high raw material costs & supply fluctuations hampering the inorganic corrosion inhibitors industry expansion?

High raw material costs and supply and demand fluctuations make it difficult for the industry to expand, as the instability affects production levels, pricing, and profitability. Industrial products, such as inorganic corrosion inhibitors, rely on the prices of certain mineral-based chemicals and metal salts, which, in turn, are affected by the availability of supplies, energy prices, the location and economics of mining, geopolitical factors, and world trade policies. When raw material prices become volatile, production costs rise, squeezing profit margins and pushing up the product's purchase price. This increased product price may put customers off, particularly in demand-oriented markets, resulting in sluggish growth in demand. On the supply side, fluctuations tend to slow down manufacturing schedules and prevent prompt delivery.

Request Free SampleRequest Free SampleRequest Free Sample

Request Free SampleRequest Free SampleRequest Free Sample

Inorganic Corrosion Inhibitors Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Inorganic Corrosion Inhibitors Market |

| Market Size in 2024 | USD 3.2 Billion |

| Market Forecast in 2034 | USD 4.8 Bllion |

| Growth Rate | CAGR of 4.2% |

| Number of Pages | 221 |

| Key Companies Covered | W.R Grace Co., Champion Technologies Inc., Cortec Corporation, GE Water, BASF SE, Daubert Cromwell LLC, Dai-Ichi Karkaria Ltd, AkzoNobel, Ashland Inc., Henkel, The Dow Chemical Company, Ecolab Inc., Solutia Inc., and others. |

| Segments Covered | By Type, By Treatment, By Application, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 - 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Inorganic Corrosion Inhibitors Market: Segmentation

Type Insights

Why does anodic inhibitor hold the dominant position in the inorganic corrosion inhibitors market?

The anodic inhibitor captures the largest revenue share in 2024. This growth is supported by the presence of anodic inhibitors, like nitrites, chromates, molybdates, and phosphates, which are very efficient in generating a passive protective film on the metallic surface and avoiding local corrosion. Anodic inhibitors work by alleviating the anodic transfer, encouraging the formation of an adherent thin oxide film, which acts as an effective barrier to further dissolution of the metal. Their proven ability to control corrosion in cooling water systems, boilers, pipelines, and reinforced concrete structures has led to their widespread use in several end markets, including power, oil and gas, water treatment, and construction. Sales growth in the anodic inhibitors segment has been driven by trends including infrastructure development, increased asset integrity management, and extended equipment and facility lifetimes at minimal operating costs.

Treatment Insights

Why do coatings hold the largest share in the inorganic corrosion inhibitors industry?

The coatings dominate the industry growth. This growth was primarily driven by growing applications of corrosion inhibitors in the construction industry for durable and long-term protection of infrastructural and industrial surfaces. Inorganic corrosion inhibitors are widely used in industrial coatings, primers, and other protective coatings because they stick well, provide strong protection, and last a long time even in tough conditions like moisture, chemicals, and salt spray.

Application Insights

Why does oil & gas hold the largest share in the inorganic corrosion inhibitors market?

The oil & gas dominate the industry growth. Revenue growth stems from the industry's steady growth and its high susceptibility to corrosion damage. Drilling, exploration, refining, and transportation activities leave pipes, tanks, offshore platforms, and processing equipment vulnerable to highly corrosive environments, which include water, salts, hydrogen sulfide, and carbon dioxide. Common corrosion inhibitors for inorganic materials are nitrites, phosphates, and molybdates, which are topcoats applied to metal surfaces to prevent degradation of the structure by forming a passive film on the surface.

Regional Insights

Why does North America lead the Inorganic corrosion inhibitors market?

North America captures the largest revenue share in 2024. The regional expansion is driven by robust industrial activity, aging facilities, and narrow regulatory requirements in terms of asset protection as well as environmental health and safety. The region has a mature oil & gas industry, large power and manufacturing operations, and the world's largest municipally owned wastewater treatment plants—necessitating comprehensive corrosion management to enhance operational efficiencies and equipment lifespan. Additionally, the old pipelines, refineries, and industrial facilities have increased the need for maintenance programs, leading to a demand for long-lasting inorganic corrosion inhibitors.

Inorganic Corrosion Inhibitors Market: Competitive Analysis

The global inorganic corrosion inhibitors market is dominated by players like:

- W.R Grace Co.

- Champion Technologies Inc.

- Cortec Corporation

- GE Water

- BASF SE

- Daubert Cromwell LLC

- Dai-Ichi Karkaria Ltd

- AkzoNobel

- Ashland Inc.

- Henkel

- The Dow Chemical Company

- Ecolab Inc.

- Solutia Inc.

The global inorganic corrosion inhibitors market is segmented as follows:

By Type

- Anodic Inhibitor

- Cathodic Inhibitor

By Treatment

- Sprays

- Coatings

- Other

By Application

- Oil & Gas

- Chemicals & Petrochemicals

- Water Treatment

- Construction

- Metalworking

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table Of Content

Methodology

FrequentlyAsked Questions

HappyClients