Global Testing as a Service (TaaS) Market Size, Share, Sales Report 2034

Testing as a Service (TaaS) Market By Test Type (Functionality, Performance, Compatibility, Security, Compliance, and Others), By Deployment Type (Public, Private, Hybrid), By End-Use (IT & Telecommunication, Healthcare, BFSI, Automotive, Manufacturing, Retail & Consumer Goods, Energy & Utilities, and Others), and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 5.28 Billion | USD 14.80 Billion | 13.75% | 2024 |

What is Market Size of Testing as a Service (TaaS) Industry?

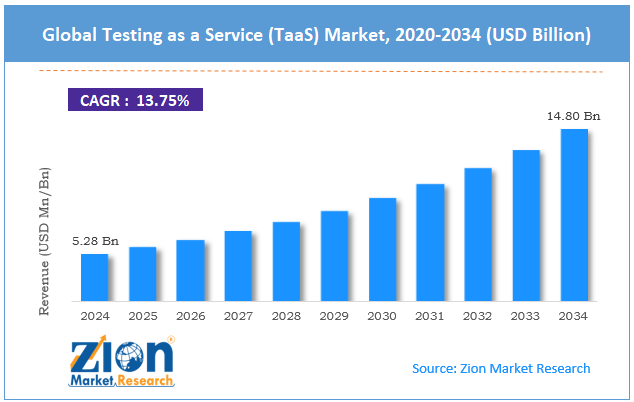

The global Testing as a Service (TaaS) market size was worth around USD 5.28 billion in 2024 and is predicted to reach around USD 14.80 billion by 2034, with a compound annual growth rate (CAGR) of roughly 13.75% between 2025 and 2034. The Testing as a Service (TaaS) Market is driven by rapid adoption of cloud technologies, Agile and DevOps methodologies, integration of AI/ML in testing, cost-effective pay-as-you-go models, and the growing complexity of modern applications including IoT, mobile, and microservices.

Key Insights:

- As per the analysis shared by our research analyst, the global Testing as a Service (TaaS) market is estimated to grow annually at a CAGR of around 13.75% over the forecast period (2025-2034)

- In terms of revenue, the global Testing as a Service (TaaS) market size was valued at around USD 5.28 billion in 2024 and is projected to reach USD 14.80 billion by 2034.

- The Testing as a Service (TaaS) market is projected to grow significantly owing to the rapid adoption of cloud technologies, the broader adoption of Agile and DevOps development methodologies, and demand for faster time-to-market and more frequent release cycles.

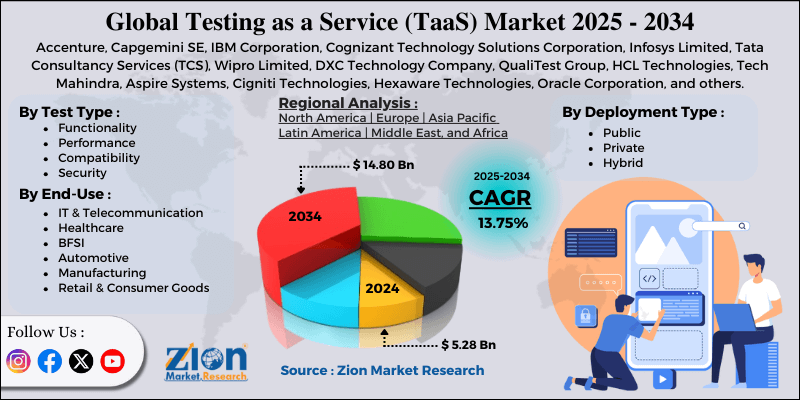

- Based on test type, the functionality segment is expected to lead the market, while the performance segment is expected to grow considerably.

- Based on deployment type, the public segment is the dominating segment, while the private segment is projected to witness sizeable revenue over the forecast period.

- Based on end-use, the IT & telecommunications segment is expected to lead the market, followed by the BFSI segment.

- Based on the region segment, the North America region dominates with approximately 39.2% share & it is dominated due to advanced IT infrastructure, high cloud adoption, significant R&D investments by major tech and BFSI players, and a large number of software development activities.

Testing as a Service (TaaS) Market: Overview

Testing as a Service is a cloud-based model in which companies outsource their software testing tasks to an external provider that delivers testing tools, expertise, and environments on demand. It allows organizations to scale testing resources quickly, reduce labor and infrastructure costs, and access different specialized testing capabilities without maintaining them in-house. The global Testing as a Service (TaaS) market is projected to grow substantially, driven by the adoption of Agile/DevOps, cloud migrations, and modern architectures, as well as the shortage of skilled QA professionals. Agile and DevOps practices require continuous, rapid testing to support frequent releases. TaaS offers on-demand environments and scalable automation to meet this speed. It allows faster delivery without compromising quality.

Moreover, cloud-native and microservices systems raise testing complexity. TaaS providers supply ready cloud-based test platforms that reduce setup effort. This accelerates validation of distributed applications. Furthermore, companies struggle to find professionals in security, automation, and performance testing. TaaS solves this gap by offering specialized skills promptly. It improves capability without long-term hiring costs.

Although drivers exist, the global market is challenged by factors like data privacy and security concerns, limited control over testing processes, and integration issues with legacy systems. Outsourcing testing exposes sensitive data and code to external vendors. This increases the risks associated with compliance violations or breaches. Highly regulated industries remain cautious in adopting TaaS.

Working with 3rd party testers may hamper visibility into test execution. Companies usually worry about timely reporting and quality standards. This lack of control restricts adoption. Similarly, proprietary or older systems may not smoothly align with TaaS platforms. Integration needs customization, which may increase cost and time. This slows adoption among legacy-heavy businesses.

Even so, the global Testing as a Service (TaaS) industry is well-positioned due to the growth of cross-platform, IoT, and mobile apps, integration of AI/ML-based Testing, and the growing need for compliance and security testing. Expanding device infrastructure needs extensive compatibility testing. TaaS providers already maintain large fleets of devices and farms. This ranks them suitable to capture surging demand. AI-based test generation and predictive analysis enhance defect detection and speed. TaaS vendors that integrate AI offer more automated, more innovative solutions. This remarkably improves service value. Cyber threats and regulations are growing worldwide. TaaS providers offering dedicated security testing can stand out. This creates high-value service opportunities.

Testing as a Service (TaaS) Market Dynamics

Growth Drivers

How does the integration of automation and AI in Testing drive the Testing as a Service (TaaS) market?

Improvements in machine learning and AI have transformed the testing process. Smart test automation tools can generate test cases, predict areas vulnerable to failure, enhance test packages, and adapt to changing codebases. This automation primarily speeds up Testing, reduces human error, and improves coverage – a factor increasingly vital in modern agile/DevOps pipelines. Subsequently, several businesses have come to prefer TaaS providers that offer AI-powered testing services. As AI-based tools progress, their effectiveness and efficiency make TaaS more valuable and attractive.

How is the demand for cost-effective and scalable QA solutions fueling the Testing as a Service (TaaS) market?

Maintaining in-house testing teams and infrastructure can be expensive, requiring licensing, hardware, ongoing maintenance, and skilled human resources. For several medium or small businesses, or for companies running bursty or periodic development cycles, this cost is usually unjustifiable. TaaS – with its pay-as-you-go model, enables companies to access well-developed testing services as required, scaling up or down depending on project requirements. This flexibility lowers capital expenditure and operational overhead, making QA accessible to a broader range of businesses. This cost efficiency remains a significant incentive for adopting TaaS, thereby propelling the Testing as a Service (TaaS) market.

Restraints

Integration complexity with existing infrastructure and processes unfavorably impacts the market progress

Several businesses use legacy systems, hybrid on-premise + cloud architectures, and custom internal workflows; integrating an external TaaS solution flawlessly into these environments is challenging. These efforts may be significant, as they require aligning environments, tools, CI/CD pipelines, and test data with the provider's infrastructure.

For companies with tightly coupled or bespoke systems, this integration overhead reduces the appeal of TaaS, potentially balancing the time/cost benefits. Therefore, businesses may avoid or delay TaaS adoption, preferring to maintain in-house control rather than invest in integration.

Opportunities

How is the Testing as a Service (TaaS) market opportune to the growing need for security, compliance, and performance testing?

The rising demand for specialized security, compliance, and performance testing, driven by increasing cyber threats and stringent regulatory requirements, opens significant avenues for TaaS providers to offer tailored, high-value services. Expansion into emerging technologies such as IoT, AI/ML applications, and 5G-enabled systems requires extensive device fleets, simulation environments, and automated testing capabilities, creating new growth opportunities for innovative TaaS solutions.

Challenges

Variation in quality and lack of standardization across providers restrict the market growth

Lack of standardization and variation in quality across different TaaS providers can lead to inconsistent test coverage, reliability issues, and difficulties in comparing service levels, complicating vendor selection for critical projects. Integration challenges with legacy systems and the need for deep domain expertise in highly regulated sectors such as healthcare and BFSI require continuous investment in tools, training, and customization, increasing operational complexity.

Testing as a Service (TaaS) Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Testing as a Service (TaaS) Market |

| Market Size in 2024 | USD 5.28 Billion |

| Market Forecast in 2034 | USD 14.80 Billion |

| Growth Rate | CAGR of 13.75% |

| Number of Pages | 212 |

| Key Companies Covered | Accenture, Capgemini SE, IBM Corporation, Cognizant Technology Solutions Corporation, Infosys Limited, Tata Consultancy Services (TCS), Wipro Limited, DXC Technology Company, QualiTest Group, HCL Technologies, Tech Mahindra, Aspire Systems, Cigniti Technologies, Hexaware Technologies, Oracle Corporation, and others. |

| Segments Covered | By Test Type, By Deployment Type, By End-Use, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, the Middle East and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 - 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Testing as a Service (TaaS) Market: Segmentation

The global Testing as a Service (TaaS) market is segmented by test type, deployment type, end-use, and region.

Based on test type, the global Testing as a Service (TaaS) industry is divided into functionality, performance, compatibility, security, compliance, and others. The functionality segment holds a dominant share of the market, as almost every software product requires thorough validation of core features before release. It assures that applications behave as intended in workflows, integrations, and user interactions. Businesses prioritize this test type since it directly impacts user experience and defect prevention. Its broad applicability in all industries maintains its rank as the leading one.

Based on deployment type, the global Testing as a Service (TaaS) market is segmented into public, private, and hybrid. The public cloud segment is the most dominant, with the largest share due to its cost-effectiveness, rapid scalability, seamless integration with modern DevOps pipelines, and ability to provide on-demand access to testing environments without significant capital expenditure; the private cloud segment ranks as the second most dominant for organizations requiring enhanced data control and security in regulated industries.

Based on end-use, the global market is segmented into IT & telecommunication, healthcare, BFSI, automotive, manufacturing, retail & consumer goods, energy & utilities, and others. The IT & telecommunication segment is the most dominant with the highest share because of frequent software updates, complex digital ecosystems, and the critical need for continuous testing to ensure service reliability and user experience in fast-evolving technologies; the BFSI segment ranks as the second most dominant due to stringent compliance requirements, high security needs, and the growing digital transformation of financial services.

Testing as a Service (TaaS) Market: Regional Analysis

Why is North America outperforming other regions in the global Testing as a Service (TaaS) Market?

North America continues to dominate the global Testing as a Service (TaaS) market through its highly advanced IT infrastructure, widespread cloud adoption, and the presence of numerous large technology companies and enterprises with substantial software development activities. The United States serves as the primary driver with significant investments in digital transformation, DevOps practices, and AI-driven testing solutions across IT, BFSI, and healthcare sectors.

A mature ecosystem of TaaS providers, combined with high awareness of quality assurance benefits, supports rapid adoption of on-demand testing models. Strong focus on innovation, regulatory compliance, and cybersecurity further accelerates demand for specialized testing services. Collaborative initiatives between technology firms and industry verticals promote the integration of advanced tools for agile and continuous testing. The region's emphasis on speed-to-market and customer experience sustains consistent investment in scalable TaaS solutions.

Europe continues to hold the second-highest share in the Testing as a Service (TaaS) industry, driven by substantial market share, growing regulatory and compliance-driven demand, and developed IT infrastructure and established providers. Europe accounts for nearly a quarter of the global TaaS industry, making it the second-largest region. Businesses are progressively adopting outsourced Testing to ensure reliable, faster software delivery. The steady demand reflects Europe's quality-driven and mature software landscape.

Moreover, stringent data protection and regulatory standards fuel businesses to adopt strong testing practices. TaaS providers guarantee compliance, security, and reliability across healthcare, finance, and other regulated industries. This regulatory pressure sustains robust demand for professional testing services. Europe's advanced IT infrastructure, DevOps practices, and broader cloud adoption aid TaaS deployment. Several regional and global service providers offer enterprise-grade testing solutions. This supportive ecosystem strengthens the region's strong market rank.

Recent Developments

- In 2025, several leading TaaS providers enhanced their platforms with deeper AI/ML capabilities for intelligent test automation and predictive defect analysis.

- In 2025, strategic collaborations between TaaS vendors and cloud hyperscalers expanded support for hybrid and multi-cloud testing environments.

- In 2025, a growing focus on security and compliance testing services emerged in response to rising cyber threats and regulatory updates across industries.

Testing as a Service (TaaS) Market: Competitive Analysis

The leading players in the global Testing as a Service (TaaS) market are:

- Accenture

- Capgemini SE

- IBM Corporation

- Cognizant Technology Solutions Corporation

- Infosys Limited

- Tata Consultancy Services (TCS)

- Wipro Limited

- DXC Technology Company

- QualiTest Group

- HCL Technologies

- Tech Mahindra

- Aspire Systems

- Cigniti Technologies

- Hexaware Technologies

- Oracle Corporation

Testing as a Service (TaaS) Market: Key Market Trends

Growing demand for security and compliance testing:

Growing cyber threats and stringent requirements are fueling the demand for compliance and security testing in TaaS. Providers offer regulatory validation and vulnerability assessments as core services. This assures applications are reliable, secure, and legally compliant.

Shift to cloud-based and cloud-native Testing:

Cloud adoption and microservices require cloud-native, scalable testing environments. TaaS allows elastic resource allocation and continuous integration with DevOps pipelines. This allows global teams to test applications effectively in diverse conditions.

The global Testing as a Service (TaaS) market is segmented as follows:

By Test Type

- Functionality

- Performance

- Compatibility

- Security

- Compliance

- Others

By Deployment Type

- Public

- Private

- Hybrid

By End-Use

- IT & Telecommunication

- Healthcare

- BFSI

- Automotive

- Manufacturing

- Retail & Consumer Goods

- Energy & Utilities

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table Of Content

Methodology

FrequentlyAsked Questions

Testing as a Service is a cloud-based model in which companies outsource their software testing tasks to an external provider that delivers testing tools, expertise, and environments on demand. It allows organizations to scale testing resources quickly, reduce labor and infrastructure costs, and access different specialized testing capabilities without maintaining them in-house.

The global Testing as a Service (TaaS) market is projected to grow due to the increasing complexity of software applications and systems, the growing integration of AI and machine learning into Testing, and the escalating use of IoT, mobile, and cross-platform applications.

According to a study, the global Testing as a Service (TaaS) market size was around USD 5.28 billion in 2024 and is projected to reach USD 14.80 billion by 2034.

The CAGR value of the Testing as a Service (TaaS) market is expected to be around 13.75% during 2025-2034.

The value chain of the global TaaS industry includes requirement analysis, test planning, test environment setup, test execution, defect management, and reporting/feedback.

Macroeconomic factors such as economic slowdowns, currency volatility, and fluctuations in IT spending may affect TaaS pricing, adoption, and investment in new testing technologies.

North America is expected to lead the global Testing as a Service (TaaS) market during the forecast period.

The United States is a significant contributor to the global Testing as a Service (TaaS) market, driven by high cloud adoption, a mature IT industry, and the presence of leading TaaS providers.

The key players profiled in the global Testing as a Service (TaaS) market include Accenture, Capgemini SE, IBM Corporation, Cognizant Technology Solutions Corporation, Infosys Limited, Tata Consultancy Services (TCS), Wipro Limited, DXC Technology Company, QualiTest Group, HCL Technologies, Tech Mahindra, Aspire Systems, Cigniti Technologies, Hexaware Technologies, and Oracle Corporation.

The report examines key aspects of the Testing as a Service (TaaS) market, including a detailed analysis of existing growth factors and restraints, as well as an examination of future growth opportunities and challenges that will impact the market.

HappyClients