Semiconductor Assembly And Testing Services Market Size Report 2034

Semiconductor Assembly And Testing Services Market By Application (Consumer Electronics, Automotive Systems, Industrial Equipment, Communications Infrastructure, Computing Devices, Medical Electronics), By Service Type (Wafer Testing, Package Assembly, Final Testing, Failure Analysis, Reliability Testing, Advanced Packaging), By End-User (Fabless Companies, Integrated Device Manufacturers, System Integrators, Original Equipment Manufacturers, Electronic Design Houses, Research Institutions), and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 38.41 Billion | USD 68.14 Billion | 6.58% | 2024 |

Semiconductor Assembly And Testing Services Industry Perspective:

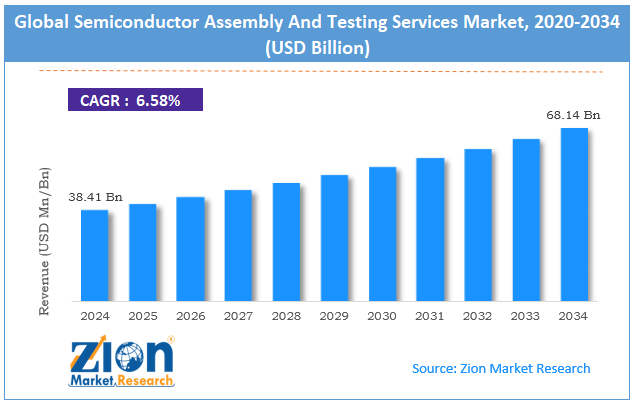

The global semiconductor assembly and testing services market size was worth approximately USD 38.41 billion in 2024 and is projected to grow to around USD 68.14 billion by 2034, with a compound annual growth rate (CAGR) of roughly 6.58% between 2025 and 2034.

Key Insights

- As per the analysis shared by our research analyst, the global semiconductor assembly and testing services market is estimated to grow annually at a CAGR of around 6.58% over the forecast period (2025-2034).

- In terms of revenue, the global semiconductor assembly and testing services market size was valued at approximately USD 68.14 billion in 2024 and is projected to reach USD 38.41 billion by 2034.

- The semiconductor assembly and testing services market is projected to grow significantly due to the expansion of electronics manufacturing activities and the rise of fabless business model adoption.

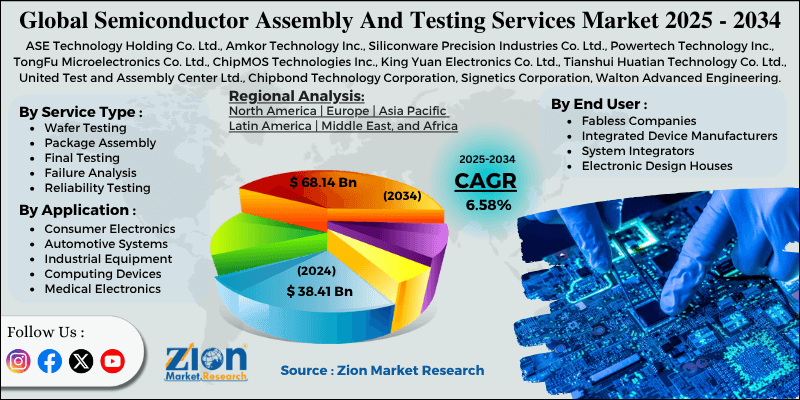

- Based on application, the consumer electronics segment is expected to lead the market, while the automotive systems segment is anticipated to experience significant growth.

- Based on service type, the package assembly segment is the dominating segment, while the advanced packaging segment is projected to witness sizeable revenue over the forecast period.

- Based on end-user, the fabless companies segment is expected to lead the market compared to the research institutions segment.

- Based on region, Asia Pacific is projected to dominate the global semiconductor assembly and testing services market during the estimated period, followed by North America.

Semiconductor Assembly And Testing Services Market: Overview

Semiconductor assembly and testing services are specialized processes that turn fabricated wafers into fully functional integrated circuits through packaging, interconnection, and quality verification. These services use precise equipment, automated testing systems, and strict quality control to ensure chip reliability and meet performance standards. Delivering effective assembly and testing involves careful attention to thermal management, electrical performance, and validation methods that confirm product functionality. Modern practices include advanced packaging technologies, automated optical inspection systems, and failure analysis tools that balance production speed with quality assurance. To maintain reliability, service providers perform extensive validation testing, apply statistical process control, and follow industry standards to ensure consistent results in large-scale production. Additionally, strict regulations guide semiconductor manufacturing to meet quality certifications, environmental compliance, and export control standards, ensuring product integrity and global market acceptance.

The growing demand for miniaturized electronics and complex semiconductor devices is expected to drive substantial growth in the semiconductor assembly and testing services market throughout the forecast period.

Semiconductor Assembly And Testing Services Market Dynamics

Growth Drivers

How are increasing fabless semiconductor business model adoption and outsourcing trends propelling the semiconductor assembly and testing services market growth?

The semiconductor assembly and testing services market is growing as chip design companies use fabless strategies, removing capital-heavy manufacturing facilities and focusing resources on product innovation and market growth. Technology firms worldwide see the benefits of outsourcing backend processes to specialized service providers offering economies of scale, technical skill, and flexible capacity management. Design houses and system companies seek partners providing complete solutions, strong quality standards, and fast time-to-market support while reducing operational complexity.

Fabless enterprises and integrated device manufacturers use outsourced services to access advanced packaging technologies, lower fixed costs, and keep production flexible. Capabilities such as multi-chip integration, heterogeneous packaging, and wide testing portfolios enable product differentiation and stronger competitive positions. These changing industry trends make assembly and testing services a key part of semiconductor supply chains, product development cycles, and business model optimization.

Miniaturization demand and performance enhancement

The global semiconductor assembly and testing services market is growing as the need for device miniaturization, power efficiency goals, and performance improvement targets gains more importance. Advanced packaging plays a key role in enabling system integration, reducing footprint size, and improving electrical performance in modern electronic products.

Rising consumer expectations, automotive electrification efforts, and artificial intelligence applications demand solutions delivering higher functionality through complex packaging designs and strict testing processes. The evolution of mobile devices and the growth of edge computing create opportunities for advanced assembly technologies that meet both performance and size requirements. Internet of Things expansion and wearable electronics growth also increase demand for miniaturized packages, helping balance functionality needs with physical space limits.

Restraints

How are capital intensity and technology transition complexity restrictions limiting the growth of the semiconductor assembly and testing services market?

A major challenge for the semiconductor assembly and testing services industry is the large investment needed for advanced equipment and process technologies compared to older systems, including lithography tools, bonding machines, and automated testing platforms. Many service providers face financial pressure due to rapid technology changes, equipment aging risks, and constant upgrade demands, making capacity expansion decisions difficult.

To handle these barriers, providers must show technology leadership, keep equipment utilization high, and build strong customer relationships. Investment hurdles persist for operations that serve diverse customer needs or operate in segments with unstable demand, necessitating flexible production approaches. The complexity of handling multiple technology generations and wide differences in customer requirements across application areas also adds more challenges for operational efficiency.

Opportunities

How is integration with artificial intelligence and Industry 4.0 technologies creating opportunities in the semiconductor assembly and testing services market?

The semiconductor assembly and testing services market is expanding with innovations like machine learning optimization, predictive maintenance systems, and automated defect classification, all supporting modern manufacturing excellence. Companies are creating smart factory solutions, real-time process monitoring tools, and data analytics platforms that boost yield performance while keeping production costs controlled. New advanced features such as chiplet integration, wafer-level packaging, and system-in-package assemblies are becoming more common.

Demand for customized services is also growing, with providers offering application-specific solutions, technology node adjustments, and performance-focused processes meeting unique customer needs. These advancements make assembly and testing services more reliable for advanced semiconductor applications and more attractive for innovative product development.

Challenges

Supply chain vulnerabilities and geopolitical considerations

The semiconductor assembly and testing services market faces challenges due to supply chain concentration risks and rising geopolitical tensions influencing manufacturing location strategies. Production capacity remains centered in a few geographic regions, making it difficult for customers to diversify risk and maintain supply stability during disruptions. This affects business continuity planning, inventory strategies, and customer confidence, increasing operational complexity for both service providers and semiconductor companies.

Another problem is the shortage of workforce development programs in emerging manufacturing regions, leading to quality issues and productivity gaps. These concerns show the need for geographic diversification, stronger workforce training, and resilient supply chain structures in the semiconductor industry. Building regional manufacturing strength and adding backup capacity options will boost supply security, lower geopolitical risks, and support long-term market stability.

Semiconductor Assembly And Testing Services Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Semiconductor Assembly And Testing Services Market |

| Market Size in 2024 | USD 38.41 Billion |

| Market Forecast in 2034 | USD 68.14 Billion |

| Growth Rate | CAGR of 6.58% |

| Number of Pages | 212 |

| Key Companies Covered | ASE Technology Holding Co. Ltd., Amkor Technology Inc., Siliconware Precision Industries Co. Ltd., Powertech Technology Inc., TongFu Microelectronics Co. Ltd., ChipMOS Technologies Inc., King Yuan Electronics Co. Ltd., Tianshui Huatian Technology Co. Ltd., United Test and Assembly Center Ltd., Chipbond Technology Corporation, Signetics Corporation, Walton Advanced Engineering Inc., Kyec Inc., Ardentec Corporation, FormFactor Inc., and others. |

| Segments Covered | By Application, By Service Type, By End User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Semiconductor Assembly And Testing Services Market: Segmentation

The global semiconductor assembly and testing services market is segmented based on application, service type, end-user, and region.

Based on application, the global semiconductor assembly and testing services industry is divided into consumer electronics, automotive systems, industrial equipment, communications infrastructure, computing devices, and medical electronics. Consumer electronics lead the market due to substantial production volumes and continuous demand for cost-effective solutions requiring efficient processes and competitive pricing structures.

Based on service type, the global semiconductor assembly and testing services market is classified into wafer testing, package assembly, final testing, failure analysis, reliability testing, and advanced packaging. Package assembly is expected to lead the market during the forecast period due to its essential role in device protection and superior value proposition across various semiconductor products and package complexity levels.

Based on end-user, the global market is segmented into fabless companies, integrated device manufacturers, system integrators, original equipment manufacturers, electronic design houses, and research institutions. Fabless companies hold the largest market share because they rely entirely on outsourced manufacturing and continuously engage with service providers to maintain production capabilities.

Semiconductor Assembly And Testing Services Market: Regional Analysis

What factors are contributing to the Asia Pacific's dominance in the global semiconductor assembly and testing services market?

Asia Pacific leads the global semiconductor assembly and testing services market because of its strong manufacturing infrastructure, competitive cost advantages, and well-developed ecosystem networks. Around 60% of global semiconductor backend operations are based in this region, with Taiwan, China, and Southeast Asian countries driving most activity through their large production capacities and specialized skills. Service providers in the Asia Pacific deliver complete solutions offering cost benefits, fast turnaround, and scalable capacity for both established and new customers.

The region also gains strength from top technical universities producing skilled engineers, experienced workforces, and a solid network of equipment suppliers and material vendors. Government support programs and mature industry clusters further build a strong manufacturing base. Growth is supported by shifting electronics manufacturing, supply chain proximity priorities, and rising fabless design activity. Asian providers lead in packaging innovation, automation technology use, and operational excellence in large-scale production.

Recently, companies have increased focus on quality certifications, automotive qualification programs, and reliability improvement efforts. Advanced analytics, artificial intelligence applications, and predictive maintenance systems are also being added to assembly and testing operations, boosting yield performance and defect detection accuracy.

North America is expected to show strong growth.

In North America, the semiconductor assembly and testing services market is growing as the industry focuses on supply chain resilience, advanced technology growth, and strategic manufacturing partnerships. These services are widely used in automotive, aerospace, and defense electronics because they offer secure supply, advanced capabilities, and compliance with strict security standards. Regional governments have introduced semiconductor manufacturing incentives that support capacity expansion and encourage domestic production, creating strong market conditions. As awareness of supply chain weaknesses increases, adoption extends beyond cost factors to include strategic sourcing, national security goals, and technology leadership priorities. Strict quality rules and high reliability needs are driving North American providers to deliver top-performance, mission-critical solutions.

Rising demand for secure, trusted, and locally sourced services highlights the industry’s focus on resilience and technology independence. Government funding and industry collaborations are boosting capability development and building advanced manufacturing ecosystems. Technology companies are working with North American providers for cutting-edge packaging, specialized testing, and joint development programs. Established service providers are teaming up with equipment makers to improve process technologies, optimize production, and show strong performance leadership.

Recent Market Developments

- In October 2025, Amkor Technology broke ground on a new advanced packaging and test campus in Peoria, Arizona, expanding its investment to $7 billion to support future capacity for AI, high-performance computing, and domestic supply chain resilience.

Semiconductor Assembly And Testing Services Market: Competitive Analysis

The leading players in the global semiconductor assembly and testing services market are:

- ASE Technology Holding Co. Ltd.

- Amkor Technology Inc.

- Siliconware Precision Industries Co. Ltd.

- Powertech Technology Inc.

- TongFu Microelectronics Co. Ltd.

- ChipMOS Technologies Inc.

- King Yuan Electronics Co. Ltd.

- Tianshui Huatian Technology Co. Ltd.

- United Test and Assembly Center Ltd.

- Chipbond Technology Corporation

- Signetics Corporation

- Walton Advanced Engineering Inc.

- Kyec Inc.

- Ardentec Corporation

- and FormFactor Inc.

The global semiconductor assembly and testing services market is segmented as follows:

By Application

- Consumer Electronics

- Automotive Systems

- Industrial Equipment

- Communications Infrastructure

- Computing Devices

- Medical Electronics

By Service Type

- Wafer Testing

- Package Assembly

- Final Testing

- Failure Analysis

- Reliability Testing

- Advanced Packaging

By End User

- Fabless Companies

- Integrated Device Manufacturers

- System Integrators

- Original Equipment Manufacturers

- Electronic Design Houses

- Research Institutions

By Region

- North America

- The U.S.

- Canada

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Southeast Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Table Of Content

Methodology

FrequentlyAsked Questions

Semiconductor assembly and testing services are specialized processes that turn fabricated wafers into fully functional integrated circuits through packaging, interconnection, and quality verification.

The global semiconductor assembly and testing services market is projected to grow due to increasing fabless business model adoption, rising demand for advanced packaging technologies, and growing emphasis on supply chain flexibility and specialized manufacturing expertise.

According to a study, the global semiconductor assembly and testing services market size was worth around USD 38.41 billion in 2024 and is predicted to grow to around USD 68.14 billion by 2034.

The CAGR value of the semiconductor assembly and testing services market is expected to be around 6.58% during 2025-2034.

Asia Pacific is expected to lead the global semiconductor assembly and testing services market during the forecast period.

The major players profiled in the global semiconductor assembly and testing services market include ASE Technology Holding Co., Ltd., Amkor Technology Inc., Siliconware Precision Industries Co., Ltd., Powertech Technology Inc., TongFu Microelectronics Co., Ltd., ChipMOS Technologies Inc., King Yuan Electronics Co., Ltd., Tianshui Huatian Technology Co., Ltd., United Test and Assembly Center Ltd., Chipbond Technology Corporation, Signetics Corporation, Walton Advanced Engineering Inc., Kyec Inc., Ardentec Corporation, and FormFactor Inc.

The report examines key aspects of the semiconductor assembly and testing services market, including a detailed analysis of existing growth factors and restraints, as well as an examination of future growth opportunities and challenges impacting the market.

The semiconductor assembly and testing services market is observing pricing trends where advanced capabilities, such as heterogeneous integration, chiplet packaging, and comprehensive testing protocols, command premium pricing compared to conventional services, creating cost considerations but highlighting value through performance enhancement and time-to-market advantages.

To stay competitive in the semiconductor assembly and testing services market, stakeholders should focus on technology leadership demonstrations, expand advanced packaging capabilities, invest in automation and artificial intelligence integration, and collaborate with equipment suppliers to validate next-generation processes and develop customized solutions for emerging application requirements.

The semiconductor assembly and testing services market will see significant growth opportunities in automotive systems and communications infrastructure, as vehicle electrification and network modernization initiatives prioritize reliable, high-performance, and quality-assured semiconductor solutions for safety-critical automotive applications and demanding telecommunications deployments.

HappyClients