Oil And Gas Pipeline Fabrication And Construction Market Size, Forecast 2034

Oil And Gas Pipeline Fabrication And Construction Market By Pipeline Type (Transmission Pipelines, Gathering Pipelines, and Distribution Pipelines), By Application (Onshore Pipelines and Offshore Pipelines), By End-Use Industry (Oil Industry and Gas Industry), and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

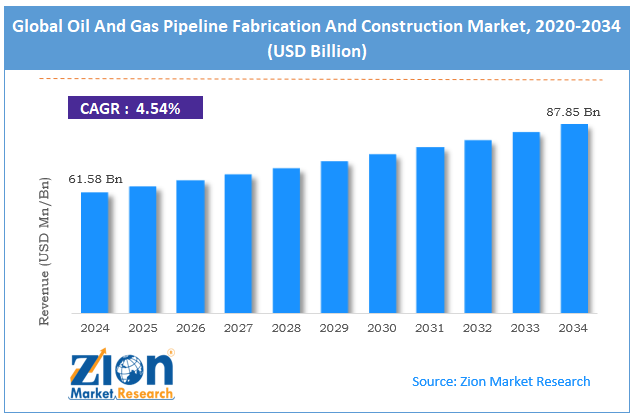

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 61.58 Billion | USD 87.85 Billion | 4.54% | 2024 |

Oil And Gas Pipeline Fabrication And Construction Market: Industry Perspective

What will be the size of the global oil and gas pipeline fabrication and construction market during the forecast period?

The global oil and gas pipeline fabrication and construction market size was around USD 61.58 billion in 2024 and is projected to reach USD 87.85 billion by 2034, with a compound annual growth rate (CAGR) of roughly 4.54% between 2025 and 2034.

Key Insights:

- As per the analysis shared by our research analyst, the global oil and gas pipeline fabrication and construction market is estimated to grow annually at a CAGR of around 4.54% over the forecast period (2025-2034)

- In terms of revenue, the global oil and gas pipeline fabrication and construction market size was valued at around USD 61.58 billion in 2024 and is projected to reach USD 87.85 billion by 2034.

- The oil and gas pipeline fabrication and construction market is projected to grow significantly, driven by the expansion of cross-border pipeline networks, growth in natural gas and LNG projects, and technological advancements in pipeline construction.

- Based on pipeline type, the transmission pipelines segment is expected to lead the market, while the distribution pipelines segment is expected to grow considerably.

- Based on application, the onshore pipelines segment is the dominating segment, while the offshore pipelines segment is projected to witness sizeable revenue over the forecast period.

- Based on end-use industry, the oil industry segment is expected to lead the market, followed by the gas industry segment.

- Based on region, the Asia Pacific is projected to dominate the global market during the estimated period, followed by North America.

Oil And Gas Pipeline Fabrication And Construction Market: Overview

Oil and gas pipeline fabrication involves cutting, welding, and coating pipes in accordance with Mechanical Engineering principles, while construction encompasses laying, joining, and testing pipelines guided by Civil Engineering, with corrosion protection and safety inspections ensuring efficient operation and long-term durability. The global oil and gas pipeline fabrication and construction market is likely to expand rapidly, driven by rising energy demand, technological advancements, and increased exploration and production activities. Growing consumption of oil and gas in households and industries is escalating, and the need for efficient transportation systems is increasing. Expanding economies and growing urbanization are fueling large-scale pipeline projects. This demand directly drives construction and fabrication activities worldwide.

Moreover, innovation in coating, welding, and inspection is enhancing pipeline safety and efficiency. Digital monitoring systems and automation improve construction accuracy and speed. These improvements encourage more investments in pipeline infrastructure. Furthermore, growing upstream activities in oil and gas fields are generating the need for new pipelines. Offshore and remote discoveries need complex pipeline networks. This fuels the demand for specialized construction and fabrication solutions.

Nevertheless, the global market faces limitations due to factors such as high initial investment costs and environmental regulations, and concerns. Pipeline projects require major capital for labor, materials, and technology. Financing such large-scale infrastructure could be challenging. This note slows project approvals and limits market entry. Similarly, stringent environmental regulations may halt or delay pipeline projects. Concerns regarding land disturbance and emissions increase compliance costs. These factors are crucial obstacles to construction. Still, the global oil and gas pipeline fabrication and construction industry benefits from several favorable factors, such as the development of smart pipelines and retrofitting and upgradation projects.

The integration of digital technologies enables predictive maintenance and real-time monitoring. Smart pipelines enhance efficiency and reduce operational risks. This creates new growth prospects for technology-driven solutions. Additionally, modernizing existing pipelines with advanced materials and technologies is gaining prominence and significance. Retrofitting enhances performance and safety. This creates a steady demand for fabrication services.

Impact of the USA-Israel war on Iran on the Oil And Gas Pipeline Fabrication And Construction Market

The U.S.-Israel ongoing war with Iran is disturbing worldwide oil and gas pipelines by increasing energy prices, geopolitical risks, and supply uncertainties. Supply chain delays, higher costs, and workforce challenges are slowing construction and fabrication projects. This is fueling a shift toward alternative routes, advanced monitoring technologies, and resilient infrastructure for long-term energy security.

Oil And Gas Pipeline Fabrication And Construction Market: Dynamics

Growth Drivers

How is the expansion of LNG & natural gas infrastructure propelling the oil and gas pipeline fabrication and construction market?

LNG trade has advanced remarkably, exceeding 500 million tonnes annually, prompting the construction of new export and import terminals worldwide. Pipelines connecting gas fields to liquefaction facilities and distribution centers are proliferating, especially in Qatar, the U.S., and East Africa. Demand for high-pressure and cryogenic capable pipelines fabrication quantities is increasing. Natural gas’s role as a transition fuel in carbon-reduction strategies accelerates midstream buildouts. State and private players are signing multi-billion-dollar construction contracts to secure long-term gas flows, ultimately fueling the global oil and gas pipeline fabrication and construction market.

How is the global oil and gas pipeline fabrication and construction market driven by the growth in offshore & subsea exploration?

Offshore oil and gas production, mainly in deepwater fields, has experienced increased investment as onshore reserves develop. This trend increases demand for highly specialized subsea pipeline fabrication, comprising high-strength steel systems and flexible risers. Subsea pipelines connect remote production centers to onshore processing facilities, increasing network complexity. Fabrication yards are scaling up capabilities to meet these technically demanding projects. Higher offshore CAPEX supports a premium for dedicated contractors.

Restraints

Competition from alternative energy & transport unfavorably impacts the market progress

Growth in battery storage and renewables is steadily reducing reliance on fossil fuels in some regions. Advanced in rail transport and LNG shipping offer alternatives to pipelines for some markets. Green hydrogen and electrification reduce long-term demand projections for conventional oil and gas infrastructure. This competitive landscape hampers investment in new pipelines. Fabricators experience pressure to diversify into low-carbon sectors.

Opportunities

How are digitalization & smart pipeline systems creating promising avenues for the growth of the oil and gas pipeline fabrication and construction industry?

Adopting digital tools such as automated welding systems, IoT monitoring, and predictive analytics improves safety and productivity. Smart fabrication techniques reduce rework, defects, and downtime. Digital twins of pipeline projects enhance planning and lifecycle management. Technologies that reduce total ownership cost make the pipeline more competitive. Early adopters gain benefits in delivery quality and speed, thus offering opportunities in the oil and gas pipeline fabrication and construction industry.

Challenges

Technical complexity of modern pipelines restricts the market growth

Advanced pipelines such as deepwater subsea, high-pressure gas, and multiphase crude lines require dedicated engineering materials and skills. Fabrication processes are more demanding, with tighter tolerances and improved welding techniques. Skilled labor scarcities constrain execution capacity in specific regions. Quality assurance and non-destructive testing add costs and complexity. These technical demands increase risk and delivery schedules.

Oil And Gas Pipeline Fabrication And Construction Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Oil And Gas Pipeline Fabrication And Construction Market |

| Market Size in 2024 | USD 61.58 Billion |

| Market Forecast in 2034 | USD 87.85 Bllion |

| Growth Rate | CAGR of 4.54% |

| Number of Pages | 227 |

| Key Companies Covered | Saipem S.p.A., McDermott International Ltd., TechnipFMC plc, Subsea 7 S.A., Bechtel Corporation, Fluor Corporation, KBR Inc., Worley Limited, Larsen & Toubro Limited, China Petroleum Pipeline Engineering Co. Ltd., Petrofac Limited, National Petroleum Construction Company (NPCC), Hyundai Engineering & Construction Co. Ltd., Daewoo Engineering & Construction Co. Ltd., Punj Lloyd Limited, and others. |

| Segments Covered | By Pipeline Type, By Application, By End-Use Industry, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 - 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Oil And Gas Pipeline Fabrication And Construction Market: Segmentation

The global oil and gas pipeline fabrication and construction market is segmented based on pipeline type, application, end-use industry, and region.

Why is the Transmission Pipelines segment projected to dominate the oil and gas pipeline fabrication and construction market?

Based on pipeline type, the global oil and gas pipeline fabrication and construction industry is divided into transmission pipelines, gathering pipelines, and distribution pipelines. The transmission pipelines segment dominates the market, accounting for 48% share, transporting large volumes of natural gas, crude oil, and refined products over long distances. Their strategic significance and high capacity fuel demand for advanced fabrication, construction, and coating technologies. They form the backbone of midstream infrastructure, promising efficient energy flow from production to processing and distribution centers.

Conversely, the distribution pipelines segment holds the second-largest market share, accounting for approximately 35%, and delivers gas from main transmission lines to commercial, residential, and industrial users. Speedy urbanization and expanding city gas networks fuel growth, backed by government initiatives. Their focus on localized energy delivery makes them a fast-growing segment of the industry.

What factors help the Onshore Pipelines segment lead the oil and gas pipeline fabrication and construction market?

Based on application, the global oil and gas pipeline fabrication and construction market is segmented into onshore pipelines and offshore pipelines. The onshore pipelines segment leads with a 69% share due to their broad networks for transporting oil and gas over land, lower maintenance costs, easy access, and lower installation costs for inspection and construction.

Nonetheless, the offshore pipelines segment accounts for a second market share of 33%, driven by increasing offshore production and exploration activities, mainly in deeper waters, which require complex marine and subsea infrastructure despite high costs and technical challenges.

What are the key reasons for the leadership of the Oil Industry segment in the oil and gas pipeline fabrication and construction market?

Based on end-use industry, the global market is segmented into oil industry and gas industry. The oil industry holds a leading market share of nearly 60% since crude oil pipelines remain central to transporting high volumes of liquid hydrocarbons from production fields to refineries and export terminals, underscoring the ongoing worldwide reliance on oil infrastructure.

However, the gas industry ranks second with 45% market share. This is driven by the rapid expansion of natural gas networks, policies favoring gas as a cleaner fuel for the energy transition, and LNG infrastructure, which drives investment in associated pipeline construction and fabrication.

Oil And Gas Pipeline Fabrication And Construction Market: Regional Analysis

What gives Asia Pacific a competitive edge in the global Oil And Gas Pipeline Fabrication And Construction Market?

Asia Pacific is projected to maintain its dominant position in the global oil and gas pipeline fabrication and construction market, with a 6-8% CAGR, owing to speedy urbanization and industrialization, growing energy demand and gasification, and growth of cross-border and offshore projects. Asia Pacific is experiencing rapid industrial growth and expanding urban centers, which are driving increased demand for energy infrastructure. Large-scale industrialization zones and growing megacities require extensive oil and gas transportation networks, driving pipeline construction and fabrication in the region.

Moreover, the region’s energy consumption is rising due to economic expansion and population growth, especially in Southeast Asia, China, and India. Governments are actively investing in natural gas pipelines and city gas distribution projects to meet surging demand, thereby fueling industry growth. Furthermore, translational pipeline projects and offshore exploration are increasing in the region, connecting resources to major consuming centers. Investments in deepwater pipelines and cross-border networks enhance the industry's share, underscoring APAC’s strategic role in global oil and gas transport.

Why does North America rank second in the global Oil And Gas Pipeline Fabrication And Construction Market?

North America maintains its position as the second-largest region, with a 5-7% CAGR in the global oil and gas pipeline fabrication and construction industry, driven by an extensive existing pipeline network, high oil and gas production, technological improvements, and skilled workforce. North America has the world's leading and highly developed oil and gas pipeline network, connecting upstream production fields to storage, refineries, and distribution hubs. Continuous maintenance, replacement, and expansion of these pipelines fuel sustained demand for construction and fabrication services. North America, mainly Canada and the U.S., is a leading producer of natural gas and crude oil, with unconventional resources and shale. High production volumes necessitate current investments in midstream infrastructure, comprising upgrades, new pipelines, and expansions to transport resources effectively.

Additionally, North America benefits from advanced pipeline technologies, such as real-time monitoring systems, automated welding, and corrosion-resistant coatings. Combined with a skilled workforce and well-developed engineering, procurement, and construction (EPC) capabilities, this allows large-scale pipeline projects and backs industry dominance.

Oil And Gas Pipeline Fabrication And Construction Market: Competitive Analysis

The leading players in the global oil and gas pipeline fabrication and construction market are:

- Saipem S.p.A.

- McDermott International Ltd.

- TechnipFMC plc

- Subsea 7 S.A.

- Bechtel Corporation

- Fluor Corporation

- KBR Inc.

- Worley Limited

- Larsen & Toubro Limited

- China Petroleum Pipeline Engineering Co. Ltd.

- Petrofac Limited

- National Petroleum Construction Company (NPCC)

- Hyundai Engineering & Construction Co. Ltd.

- Daewoo Engineering & Construction Co. Ltd.

- Punj Lloyd Limited

What are the key trends in the global Oil And Gas Pipeline Fabrication And Construction Market?

Rise of hydrogen and energy transition infrastructure:

With worldwide decarbonization efforts, there is a surging interest in repurposing or building pipelines for hydrogen transport and blending with natural gas. This trend is encouraging innovation in coatings, design standards, and materials for handling alternative fuels, creating new market segments beyond traditional oil and gas transport.

Focus on Environmental, Social, and Governance (ESG) compliance:

Social and environmental concerns are influencing pipeline planning and execution more than ever. Regulatory frameworks now need thorough impact assessments, stringent emissions control, and community engagement programs. Pipeline projects that promise minimal ecological disturbance and high safety standards are largely prioritized by investors.

The global oil and gas pipeline fabrication and construction market is segmented as follows:

By Pipeline Type

- Transmission Pipelines

- Gathering Pipelines

- Distribution Pipelines

By Application

- Onshore Pipelines

- Offshore Pipelines

By End-Use Industry

- Oil Industry

- Gas Industry

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table Of Content

Methodology

FrequentlyAsked Questions

Oil and gas pipeline fabrication comprises cutting, welding, and coating pipes according to principles of Mechanical Engineering, while construction encompasses laying, joining, and testing pipelines guided by Civil Engineering, with corrosion protection and safety inspections promising efficient operation and long-term durability.

The global oil and gas pipeline fabrication and construction market is projected to grow due to rising global energy demand, increased investments in oil & gas infrastructure, and aging pipeline replacement and modernization.

According to study, the global oil and gas pipeline fabrication and construction market size was around USD 61.58 billion in 2024 and is projected to reach USD 87.85 billion by 2034.

The CAGR value of the oil and gas pipeline fabrication and construction market is expected to be around 4.54% during 2025-2034.

Macroeconomic factors like global GDP growth, inflation, energy demand, and investment cycles will directly influence pipeline construction project timelines, spending, and market expansion.

Asia Pacific is expected to lead the global oil and gas pipeline fabrication and construction market during the forecast period.

The United States is a significant contributor to the global oil and gas pipeline fabrication and construction market, driven by its midstream infrastructure and extensive production.

The key players profiled in the global oil and gas pipeline fabrication and construction market include Saipem S.p.A., McDermott International Ltd., TechnipFMC plc, Subsea 7 S.A., Bechtel Corporation, Fluor Corporation, KBR Inc., Worley Limited, Larsen & Toubro Limited, China Petroleum Pipeline Engineering Co., Ltd., Petrofac Limited, National Petroleum Construction Company (NPCC), Hyundai Engineering & Construction Co., Ltd., Daewoo Engineering & Construction Co., Ltd., and Punj Lloyd Limited.

The competitive landscape is fragmented, featuring regional fabrication firms, major multinational EPC contractors, and specialized service providers competing on technology, capacity, and project expertise.

The report examines key aspects of the oil and gas pipeline fabrication and construction market, including a detailed analysis of current growth factors and restraints, as well as future growth opportunities and challenges that will affect the market.

HappyClients