Industrial PC Market Size, Growth, Global Trends, Forecast 2034

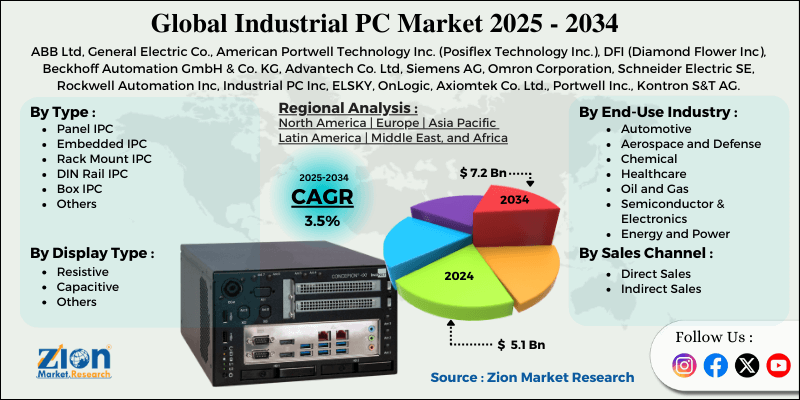

Industrial PC Market By Type (Panel IPC, Embedded IPC, Rack Mount IPC, DIN Rail IPC, Box IPC, and Others), By Display Type (Resistive, Capacitive, and Others), By End-Use Industry (Automotive, Aerospace and Defense, Chemical, Healthcare, Oil and Gas, Semiconductor and Electronics, Energy and Power, and Others), By Sales Channel (Direct Sales and Indirect Sales), and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 5.1 Billion | USD 7.2 Billion | 3.5% | 2024 |

Industrial PC Industry Perspective:

What will be the size of the global Industrial PC market during the forecast period?

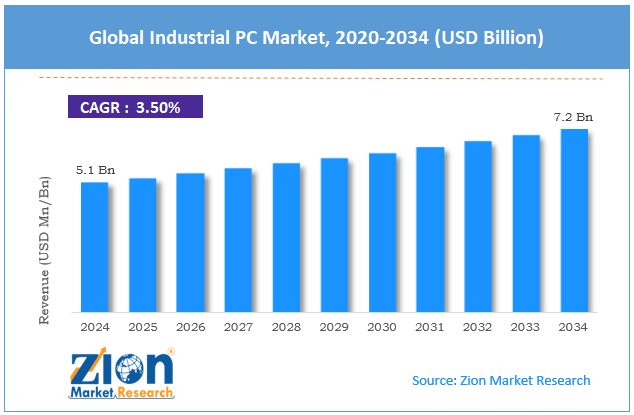

The global industrial PC market size was worth around USD 5.1 billion in 2024 and is predicted to grow to around USD 7.2 billion by 2034, with a compound annual growth rate (CAGR) of roughly 3.5% between 2025 and 2034.

Key Insights

- As per the analysis shared by our research analyst, the global Industrial PC market is estimated to grow annually at a CAGR of around 3.5% over the forecast period (2025-2034).

- In terms of revenue, the global Industrial PC market size was valued at around USD 5.1 billion in 2024 and is projected to reach USD 7.2 billion by 2034.

- The rapid industrialization in emerging markets is expected to drive the Industrial PC market.

- Based on the type, in 2024, the Panel IPC held the largest market share of 29%.

- Based on the display type, capacitive holds the largest market share at 55% in 2024.

- Based on the end-use industry, in 2024, the automotive industry had the greatest market share, more than 22%.

- Based on the sales channel, in 2024, the direct sales held a significant revenue share of 82.5%.

- Based on region, the Asia Pacific captures the largest market share of 39% in 2024.

Industrial PC Market: Overview

The Industrial PC is an essential computing device that factories, oil and gas facilities, power plants, transportation systems, and automated control systems rely on to perform their operations. The hardware of industrial PCs enables them to operate under extreme environmental conditions because they withstand high temperatures, dust, vibration, humidity, and electromagnetic interference, which standard office and home computers cannot handle. The system controls machine operations while automating processes, gathering data, displaying information to users, and executing digital monitoring of activities. Industrial PCs offer three installation methods: panel mounting, rack installation, and DIN rail mounting. The products maintain high performance standards throughout their extended operational life. Smart manufacturing systems that operate in accordance with Industry 4.0 standards depend on these components because they support continuous system operation, enable immediate data processing, and provide quick industrial network access.

Industrial PC Market: Dynamics

Growth Drivers

Does harsh-environment reliability drive the growth of the industrial PC market?

The need for reliable computers in harsh environments drives the industrial PC market. Industrial PCs are built to withstand very hot or cold temperatures, vibrations, dust, moisture, grease, and electromagnetic interference. Sometimes, the oil and gas, mining, transportation, energy, and defense industries have to operate in very harsh conditions that would make standard business computers fail. Even in these environments, industrial PCs can run consistently, reducing downtime and maintenance costs while boosting operational efficiency. As companies place greater value on reliability, safety, and continuous output, the need for robust computer systems grows. This is especially vital for applications that are critical to the mission, where a system failure could lead to lost productivity, safety issues, or violations of the law. Because of this, Industrial PCs are far more likely to be used in tough places, which is good for the market as a whole.

Restraints

How does the lack of standardization and integration restrain the industrial PC market expansion?

Standardization and integration problems are slowing down the growth of the Industrial PC industry. In an industrial context, it's common to use equipment from multiple manufacturers. Every provider has its own ways of communicating, connecting hardware, and using software. There are no common standards for automation systems, industrial networks (such as Modbus, PROFIBUS, EtherCAT, and proprietary protocols), or control structures; it's challenging to get them all to function together. This means that occasionally adding Industrial PCs to an already-working system may require bespoke development, middleware, or other technical work.

Many schools also still utilize old computers that weren't built for digital communication. It might be challenging and time-consuming to connect modern industrial PCs to older programmable logic controllers (PLCs), SCADA systems, and factory automation platforms. These integration problems make implementation more expensive, take longer to set up, and make it riskier for operations to modify the system. Because of these concerns, companies, especially small and medium-sized ones, may delay modernization plans, which could limit the growth of the Industrial PC market.

Opportunities

Will increasing product launches offer a lucrative opportunity for the industrial PC market growth?

The Industrial PC market could grow if more devices come out. As businesses around the world accelerate their shift to digital and adopt smart manufacturing methods, they need computing solutions that are more specialized, powerful, and efficient. In response, firms that make industrial PCs are introducing new, faster models, offering more connections, modular, and feature advanced features such as edge computing, AI-ready architectures, compact and rugged form factors, and compatibility with the latest industrial communication standards. These new ideas help address customer needs across a wide range of fields, including healthcare, manufacturing, energy, transportation, and logistics. Vendors can reach more consumers by offering more specialized solutions, such as compact panel PCs for small spaces, fanless systems for quieter operation, and high-performance edge analytics machines that require a lot of data.

Also, providers have to compete with each other to find new items constantly. This drives up pricing and gets more people to use the products. This not only attracts new clients but also encourages current ones to switch to next-generation Industrial PCs to improve connectivity, operational efficiency, and support Industry 4.0 operations.

For instance, in November 2025, Qualcomm Technologies, Inc. released the Qualcomm Dragonwing™ IQ-X Series. These processors are made for PLCs, advanced HMIs, edge controllers, panel PCs, and box PCs. It is designed to operate in harsh conditions and comes in a ruggedized package, supporting a wide range of peripherals. This makes it easy to connect to different types of industrial equipment and use it in a variety of applications. The IQ-X series also features sophisticated multimedia capabilities and a power-efficient design.

Challenges

Rapid technological obsolescence poses a major challenge to market growth

The rapid pace of technological change is a major obstacle to the expansion of the Industrial PC business. In mission-critical settings, industrial PCs are typically designed to last 7 to 15 years. But chip architectures, operating systems, connectivity standards (including 5G and enhanced Ethernet protocols), edge computing frameworks, and cybersecurity needs are all changing quickly. This makes it hard for industrial users to reach their long-term goals because computing technology changes so quickly. When new systems that are faster, more powerful, and use less energy are released regularly, older Industrial PCs may no longer be able to keep up with security, performance, and compatibility standards.

Companies might not want to spend a lot of money on IPC systems if they think the hardware or software platform will become outdated quickly. Also, updating systems sometimes means changing hardware, moving software, retraining workers, and temporarily stopping production, all of which cost more to run. Because of this, rapid technological change can make it hard to decide what to buy, make people hesitant to update, and complicate product lifecycle management, slowing overall market growth.

Industrial PC Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Industrial PC Market |

| Market Size in 2024 | USD 5.1 Billion |

| Market Forecast in 2034 | USD 7.2 Bllion |

| Growth Rate | CAGR of 3.5% |

| Number of Pages | 222 |

| Key Companies Covered | ABB Ltd, General Electric Co., American Portwell Technology Inc. (Posiflex Technology Inc.), DFI (Diamond Flower Inc), Beckhoff Automation GmbH & Co. KG, Advantech Co. Ltd, Siemens AG, Omron Corporation, Schneider Electric SE, Rockwell Automation Inc, Industrial PC Inc, ELSKY, OnLogic, Axiomtek Co. Ltd., Portwell Inc., Kontron S&T AG, and others. |

| Segments Covered | By Type, By Display Type, By End-Use Industry, By Sales Channel, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Industrial PC Market: Segmentation

Type Insights

What factor cause Panel IPC segment to be in a dominating position in the industrial PC market?

In 2024, the Panel IPC held the largest market share of 29%. Industrial panel PCs are computers that can do both industrial and high-performance computing. They have strong touch interfaces and fast processing, which are vital in fields such as healthcare, manufacturing, energy, and automotive. People like panel IPCs because they are small, reliable, and easy to operate. This makes it simple for humans and robots to work together, even when situations get rough. These IPCs are connected to automation systems that make things operate more smoothly and let one see and work with data right away. As Industry 4.0 grows, so does the need for smart factories and digitalization. This is making the panel IPC market flourish.

Display Type Insights

Why does capacitive hold the largest share in the industrial PC industry?

Capacitive holds the largest market share at 55% in 2024. Industrial PCs with capacitive displays are very sensitive to touch, can handle multiple touches at once, and can withstand long-term use. Resistive touch counterparts are slower and less accurate because they rely on the electrical properties of human touch to determine what's being done.

Because of this, they are well-suited for industries that need quick engagement, such as healthcare, manufacturing, transportation, and energy. Capacitive displays are becoming increasingly common in industrial settings because they are easy to use and perform well. They are also appealing because they can be seen clearly even in strong light or outdoors, and they can withstand wear and tear. Capacitive displays are important for making sure that people and machines can work together smoothly as firms embrace automation, smart systems, and digital transformation. They also help the worldwide industrial PC market flourish.

End-Use Industry Insights

Why does the automotive segment capture the largest revenue share in the industrial PC market in 2024?

In 2024, the automotive sector had the greatest market share, more than 22%. As it relies more and more on cutting-edge digital tools to make goods and operate the business. Industrial PCs are needed for automotive tasks such as automating assembly lines, checking quality, running diagnostics, and integrating robotics. Making cars more efficient and accurate is easier because they can operate in tough conditions, interpret data in real time, and enable machines to communicate with one another.

The need for industrial PCs in this industry is expanding as car companies focus on smart factories and connected systems. This is because new technologies such as the Internet of Things (IoT) and artificial intelligence (AI) are becoming increasingly common. There is a growing need for high-performance computers to tackle complicated design and testing jobs as more and more automobiles become electrified and self-driving. This trend underscores the importance of the automotive industry in accelerating the adoption of new ideas and driving growth in the global market for industrial PCs.

Sales Channel Insights

Why does direct sales capture a significant share in 2024 in the industrial PC industry?

In 2024, the direct sales held a significant revenue share of 82.5%. Direct sales channels offer personalized, relationship-based approaches to fulfill the specific demands of industrial clients. Direct sales enable manufacturers to provide clients with specific solutions, technical support, and in-depth product expertise, helping them build deeper relationships and trust. This channel does a better job of delivering the product's benefits by meeting demanding industrial needs.

Businesses like manufacturing, health care, and energy that require specialized solutions rely heavily on direct sales. Direct sales also give manufacturers a chance to gather valuable customer feedback that can help them improve their products. Direct sales channels remain a major driver of industry growth worldwide, even as companies seek to make their purchasing processes more accurate and efficient.

Regional Insights

Why does the Asia Pacific hold the largest share in the Industrial PC market?

The Asia Pacific captures the largest market share of 39% in 2024. The growth of regions is caused by more factories, better technology, and the existence of important manufacturing centers. China, Japan, South Korea, and India are some of the first countries to use industrial PCs to improve automation, efficiency, and Industry 4.0 adoption better. The automotive, electronics, and semiconductor industries in the area are growing quickly, which increases the need for strong computer solutions that can work in harsh conditions. The government's efforts to create smart factories and digital transformation assist the market in flourishing.

More money going into building infrastructure and renewable energy projects is making more industrial PCs used for monitoring and control. The Asia-Pacific region is a major driver of global market growth since its economy is growing quickly and it values new ideas.

Industrial PC Market: Competitive Analysis

The global Industrial PC market is dominated by players like:

- ABB Ltd

- General Electric Co.

- American Portwell Technology Inc. (Posiflex Technology Inc.)

- DFI (Diamond Flower Inc)

- Beckhoff Automation GmbH & Co. KG

- Advantech Co. Ltd

- Siemens AG

- Omron Corporation

- Schneider Electric SE

- Rockwell Automation Inc

- Industrial PC Inc

- ELSKY

- OnLogic

- Axiomtek Co. Ltd.

- Portwell Inc.

- Kontron S&T AG

The global Industrial PC market is segmented as follows:

By Type

- Panel IPC

- Embedded IPC

- Rack Mount IPC

- DIN Rail IPC

- Box IPC

- Others

By Display Type

- Resistive

- Capacitive

- Others

By End-Use Industry

- Automotive

- Aerospace and Defense

- Chemical

- Healthcare

- Oil and Gas

- Semiconductor and Electronics

- Energy and Power

- Others

By Sales Channel

- Direct Sales

- Indirect Sales

By Region

- North America

- The U.S.

- Canada

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Southeast Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Table Of Content

Methodology

FrequentlyAsked Questions

HappyClients