High Purity Piping Systems Market Size, Share, Trends, Growth 2034

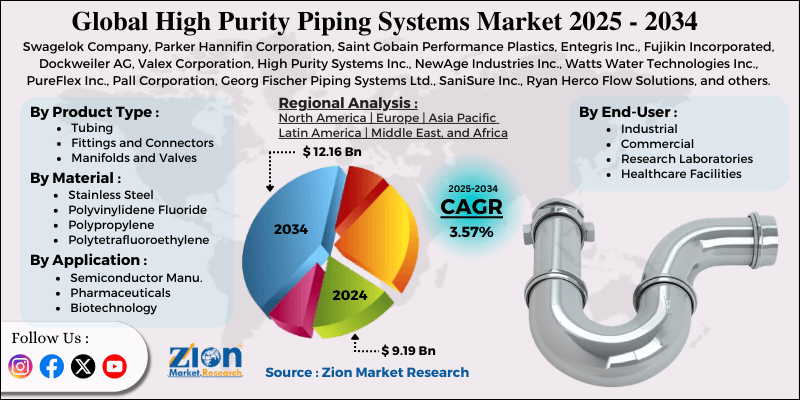

High Purity Piping Systems Market By Product Type (Tubing, Fittings and Connectors, Manifolds and Valves), By Material Type (Stainless Steel, Polyvinylidene Fluoride [PVDF], Polypropylene [PP], Polytetrafluoroethylene [PTFE], and Others), By Application (Semiconductor Manufacturing, Pharmaceuticals, Biotechnology, Food & Beverage, and Others), By End-User (Industrial, Commercial, Research Laboratories, Healthcare Facilities, and Others), and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 9.19 Billion | USD 12.16 Billion | 3.57% | 2024 |

High Purity Piping Systems Industry Perspective:

What will be the size of the global high purity piping systems market during the forecast period?

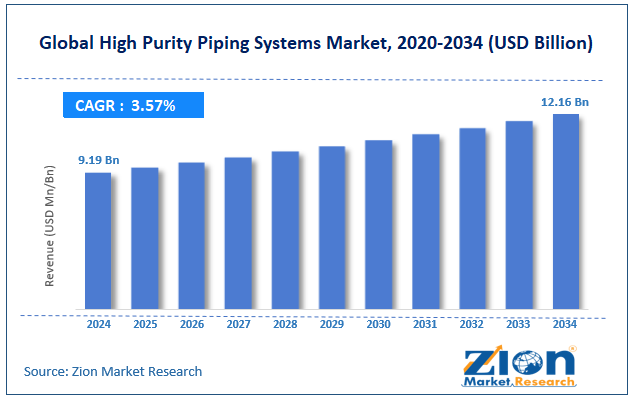

The global high purity piping systems market size was around USD 9.19 billion in 2024 and is projected to reach USD 12.16 billion by 2034, with a compound annual growth rate (CAGR) of roughly 3.57% between 2025 and 2034.

Key Insights:

- As per the analysis shared by our research analyst, the global high purity piping systems market is estimated to grow annually at a CAGR of around 3.57% over the forecast period (2025-2034)

- In terms of revenue, the global high purity piping systems market was valued at approximately USD 9.19 billion in 2024 and is projected to reach USD 12.16 billion by 2034.

- The high purity piping systems market is projected to grow significantly owing to increasing demand from the pharmaceutical manufacturing sector, rising adoption of water treatment technologies, and the expansion of microelectronics fabrication facilities.

- Based on product type, the tubing segment holds a dominant share, while the fittings and connectors segment is expected to witness notable revenue growth over the coming years.

- Based on material type, the stainless steel segment is expected to lead the market, while the Polyvinylidene Fluoride (PVDF) segment is expected to grow considerably.

- Based on application, the pharmaceuticals segment is the largest, while the semiconductor manufacturing segment is projected to record sizeable revenue over the forecast period.

- Based on end-user, the industrial segment is expected to lead the market, followed by the commercial segment.

- By region, North America is projected to dominate the global market during the forecast period, followed by Europe.

High Purity Piping Systems Market: Overview

High-purity piping systems are dedicated piping networks that transport ultra-clean chemicals, gases, or liquids without introducing contaminants. They are widely used in sectors such as pharmaceuticals, biotechnology, semiconductor manufacturing, and high-purity chemical processing, where stringent material compatibility and cleanliness are essential. The global high-purity piping systems market is likely to expand rapidly, driven by growth in semiconductor manufacturing, rising biotechnology and pharmaceutical production, and stringent regulatory and quality standards. The rapid growth of semiconductor fabrication plants is driving demand for high-purity piping systems. Chip manufacturing requires ultra-clean environments where even the smallest contaminants can harm wafers. This raises the need for trustworthy contamination-free piping infrastructure.

Moreover, biotech and pharmaceutical facilities require sterile systems to transport sensitive fluids. High-purity piping helps maintain product quality during biologics and drug manufacturing. Rising healthcare demand is driving the adoption of these systems. Furthermore, industries such as food processing and pharmaceuticals should adhere to stringent hygiene standards. Compliance with standards like the FDA and GMP requires contamination-free piping systems. These norms encourage companies to invest in high-purity piping solutions.

Nevertheless, the global market faces limitations, including high initial installation costs and complex installation procedures. High-purity piping systems need premium materials and specialized installation processes. Compared with standard piping, project costs may be higher due to strict contamination control and quality requirements. These high upfront costs usually limit adoption, especially for small manufacturers. Likewise, the installation of high-purity piping comprises specialized fittings, orbital welding, and stringent validation procedures. These complex processes increase the need for skilled professionals and project schedules.

Hence, companies may experience operational delays during installation. Still, the global high-purity piping systems industry benefits from several favorable factors, such as the expansion of semiconductor fabrication facilities and the growth of biopharmaceutical manufacturing. The worldwide drive for semiconductor self-sufficiency is increasing the number of fabrication plants worldwide. These facilities need high-purity piping for transporting gases, ultrapure water, and chemicals. This growth is fueling the demand for specialized piping systems. Additionally, the development of vaccines, biologics, and advanced therapies is accelerating the pace of biopharmaceutical manufacturing. This growth is increasing the need for high-purity piping infrastructure.

High Purity Piping Systems Market: Dynamics

Growth Drivers

How are food & beverage and specialized process applications driving the high-purity piping systems market progress?

Beyond conventional high-tech industries, food and beverage processors are utilizing high-purity piping to prevent contamination and maintain hygiene. Growing consumer demand for food safety, clean labeling, and natural products is fueling upgrades in beverage, dairy, and packaging plants. Research laboratories, clean water treatment plants, and medical device facilities also need ultra-clean piping systems. This diversification expands the overall addressable market for high-purity piping vendors. In addition, developing sectors like specialty chemicals are contributing to incremental demand growth, impacting the progress of the high-purity piping systems market.

How is technological innovation in materials & monitoring fueling the high-purity piping systems market development?

Advances in materials science, including PFA, PVDF, and other advanced fluoropolymers, are enhancing chemical resistance and reducing particle generation. Innovative welding and smart sensors improve installation quality and allow real-time system monitoring. Predictive maintenance and digitalization help reduce lifecycle costs and downtime. These solutions are increasingly being adopted in more sensitive manufacturing environments. Continuous research and development are fueling the development of next-gen high-purity piping systems.

Restraints

Complex technical integration requirements negatively impact the market progress

Integrating high-purity piping into existing process lines usually requires extensive customization and engineering. Legacy systems may lack compatibility with new piping standards, demanding process redesigns. Skilled engineering talent scarcities increase project risk and schedule delays. Regulatory compliance adds pressure on documentation and testing. This complexity hampers speedy adoption in retrofit scenarios.

Opportunities

How do green hydrogen and clean energy projects create promising avenues for the growth of the high-purity piping systems industry?

Green hydrogen production requires corrosion-resistant, high-purity pathways for gas handling and electrolyzer operation. As governments invest in hydrogen value chains, demand for certified piping systems increases. New standards for energy storage and fuel cell installations create technical openings. Collaborations between energy OEMs and piping vendors accelerate advancement. This energy transition theme presents multi-billion-dollar frameworks in the coming decade, with prospects in the high-purity piping systems industry.

Challenges

Talent shortages in skilled fabrication & inspection restrict the market growth

High-purity system build and installation demand cleanroom technicians, validation engineers, and certified welders. Worldwide shortages of these specialists raise labor costs and delay projects. Training pipelines are limited and often do not meet industry standards. Migration of talent to other high-demand tech industries exacerbates the issue. Workforce barriers directly impact delivery schedules.

High Purity Piping Systems Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | High Purity Piping Systems Market |

| Market Size in 2024 | USD 9.19 Billion |

| Market Forecast in 2034 | USD 12.16 Bllion |

| Growth Rate | CAGR of 3.57% |

| Number of Pages | 224 |

| Key Companies Covered | Swagelok Company, Parker Hannifin Corporation, Saint Gobain Performance Plastics, Entegris Inc., Fujikin Incorporated, Dockweiler AG, Valex Corporation, High Purity Systems Inc., NewAge Industries Inc., Watts Water Technologies Inc., PureFlex Inc., Pall Corporation, Georg Fischer Piping Systems Ltd., SaniSure Inc., Ryan Herco Flow Solutions, and others. |

| Segments Covered | By Product Type, By Material Type, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

High Purity Piping Systems Market: Segmentation

The global high purity piping systems market is segmented by product type, material type, application, end-user, and region.

Why is the Tubing segment projected to dominate the high purity piping systems market?

Based on product type, the global high purity piping systems industry is divided into tubing, fittings and connectors, and manifolds and valves. The tubing segment holds a leading 50%+ share of the worldwide market, serving as the primary pathway for ultra-clean fluid transport in the pharmaceutical and semiconductor industries. With this significant market share, it is in high demand in the fitting- and tube-focused market.

Conversely, the fittings and connectors segment ranks nearly 47% of the market share. They are vital for achieving leak-free joints and modular routing in clean-process piping systems.

What factors help the Stainless Steel segment lead the high purity piping systems market?

Based on material type, the global market is segmented into stainless steel, Polyvinylidene Fluoride (PVDF), Polypropylene (PP), Polytetrafluoroethylene (PTFE), and others. The stainless steel segment holds a dominant 45% market share. It is highly valued for its corrosion resistance, hygiene, and durability, making it well-suited for pharmaceuticals and semiconductors.

On the other hand, the Polyvinylidene Fluoride (PVDF) segment ranks second, with 35% market share. It is valued for its chemical resistance and low permeability, and is widely used in biotech and semiconductor applications.

Which key reasons dominate the Pharmaceuticals segment of the high purity piping systems market?

Based on application, the global high purity piping systems market is segmented into semiconductor manufacturing, pharmaceuticals, biotechnology, food & beverage, and others. The pharmaceuticals and biotechnology segments together rank highest, accounting for nearly 38% of the market share. These industries need ultra-clean piping for biologics and drug production, fueled by stringent regulations and rising demand for therapies and vaccines.

Nonetheless, the semiconductor manufacturing segment holds the second-largest market share at 34%. High-purity piping is vital for ultrapure water, chemicals, and gases in fabs, with demand escalating as new facilities grow worldwide.

What are the key reasons for the leadership of the Industrial segment in the high purity piping systems market?

Based on end-user, the global market is segmented into industrial, commercial, research laboratories, healthcare facilities, and others. The industrial segment is a major end-user, accounting for nearly 70% of market share. Industries such as chemicals, pharmaceuticals, and semiconductors rely heavily on high-purity piping to ensure contamination-free operations.

However, the commercial segment holds a second position with 25% of the market. Hospitality, food processing, and other commercial facilities use high-purity piping to meet required safety and hygiene standards.

High Purity Piping Systems Market: Regional Analysis

What gives North America a competitive edge in the global High Purity Piping Systems Market?

North America is projected to maintain its dominant position in the global high purity piping systems market, with a 6.5% CAGR, driven by advanced pharmaceutical and semiconductor industries, strict regulatory standards, and high R&D and infrastructure investments. North America has a strong presence of semiconductor fabs and biotech/pharmaceutical companies, fueling elevated demand for ultra-clean fluid-transfer systems. The region’s leading large-scale and technology production facilities need high-purity piping to maintain regulatory compliance and product quality.

Moreover, strict regulations on product safety, contamination control, and quality, like GMP and FDA guidelines, encourage broader adoption of high-purity piping systems. Companies invest heavily in compliant infrastructure to meet these standards. Furthermore, major investments in development, research, and advanced manufacturing infrastructure support the growth of high-purity piping systems. Growing funding for laboratories, cleanroom facilities, and advanced manufacturing strengthens industry dominance.

Why does Europe rank second in the global High Purity Piping Systems Market?

Europe maintains its position as the second-largest region, with a 5.8-6.8% CAGR in the global high purity piping systems industry, driven by the strong biotechnology and pharmaceutical presence, a stringent regulatory environment, and advanced manufacturing infrastructure. Europe has a well-developed biotechnology and pharmaceutical sector, fueling demand for high-purity piping systems. Facilities need ultra-clean fluid transfer for sterile processing, drug production, and biologics, increasing the region’s significance.

Moreover, strict European norms, comprising ISO and EMA standards, enforce product safety and contamination control. Compliance with these standards encourages broader adoption of high-purity piping solutions. Additionally, Europe’s advanced manufacturing base, comprising the semiconductor, chemical, and food industries, relies on high-purity piping to maintain product integrity and efficiency. Developed infrastructure supports the maintenance and installation of these specialized systems.

High Purity Piping Systems Market: Competitive Analysis

The leading players in the global high purity piping systems market are;

- Swagelok Company

- Parker Hannifin Corporation

- Saint Gobain Performance Plastics

- Entegris Inc.

- Fujikin Incorporated

- Dockweiler AG

- Valex Corporation

- High Purity Systems Inc.

- NewAge Industries Inc.

- Watts Water Technologies Inc.

- PureFlex Inc.

- Pall Corporation

- Georg Fischer Piping Systems Ltd.

- SaniSure Inc.

- Ryan Herco Flow Solutions

What are the key trends in the global High Purity Piping Systems Market?

Prefabricated and modular system adoption:

Prefabricated and modular piping components are gaining prominence because they streamline installation, shorten project schedules, and reduce on-site labor. These systems are pre-validated and easier to integrate into controlled environments and cleanrooms. The trend supports faster deployment in high-growth regions and large-scale industrial facilities.

Integration of IoT and smart monitoring:

High-purity piping systems are being equipped with IoT-enabled sensors and monitoring tools that offer real-time data on flow rates, pressure, and contamination levels. This digital integration allows predictive maintenance, enhances process control, and reduces downtime. As smart manufacturing progresses, the demand for connected piping solutions continues to grow.

The global high purity piping systems market is segmented as follows:

By Product Type

- Tubing

- Fittings and Connectors

- Manifolds and Valves

By Material Type

- Stainless Steel

- Polyvinylidene Fluoride (PVDF)

- Polypropylene (PP)

- Polytetrafluoroethylene (PTFE)

- Others

By Application

- Semiconductor Manufacturing

- Pharmaceuticals

- Biotechnology

- Food & Beverage

- Others

By End-User

- Industrial

- Commercial

- Research Laboratories

- Healthcare Facilities

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table Of Content

Methodology

FrequentlyAsked Questions

Which key factors will influence the growth of the high purity piping systems market over 2025-2034?

HappyClients