North America High-Performance Computing (HPC) Market Size, Forecast 2034

North America High-Performance Computing (HPC) Market By Deployment Model (On-Premises, Cloud-Based, Hybrid), By Application (Scientific Computing, Data Analytics and Big Data, Financial Services, Healthcare and Life Sciences, Oil and Gas Exploration, Manufacturing and Engineering), By End-User (Academic and Research Institutions, Government and Defense, Enterprises, SMEs), and By Region - Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 39.09 Billion | USD 66.91 Billion | 6.95% | 2024 |

North America High-Performance Computing (HPC) Industry Perspective:

What will be the size of the North America high-performance computing (HPC) market during the forecast period?

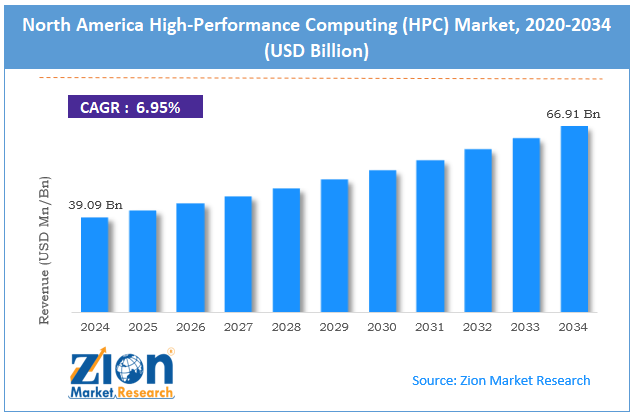

The North America high-performance computing (HPC) market size was around USD 39.09 billion in 2024 and is projected to reach USD 66.91 billion by 2034, with a compound annual growth rate (CAGR) of roughly 6.95% between 2025 and 2034.

Request Free SampleRequest Free SampleRequest Free Sample

Request Free SampleRequest Free SampleRequest Free Sample

Key Insights:

- As per the analysis shared by our research analyst, the North America high-performance computing (HPC) market is estimated to grow annually at a CAGR of around 6.95% over the forecast period (2025-2034)

- In terms of revenue, the North America high-performance computing (HPC) market size was valued at around USD 39.09 billion in 2024 and is projected to reach USD 66.91 billion by 2034.

- The North America high-performance computing (HPC) market is projected to grow significantly owing to rising demand for big data analytics, increasing use in genomics and life sciences, and advancements in quantum computing.

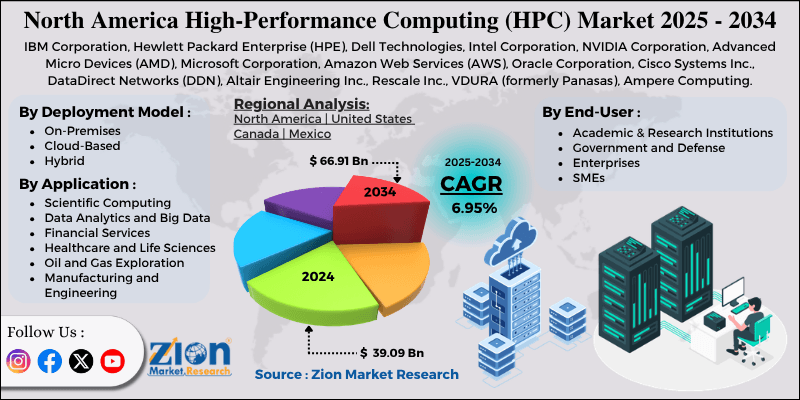

- Based on the deployment model, the on-premises segment is expected to lead the market, while the cloud-based segment is expected to grow considerably.

- Based on application, the scientific computing segment is the dominating segment, while the data analytics and big data segment is projected to witness sizeable revenue over the forecast period.

- Based on end-user, the government and defense segment is expected to lead the market, followed by the enterprises segment.

- By region, the United States is projected to dominate the market during the forecast period, followed by Canada.

North America High-Performance Computing (HPC) Market: Overview

High-performance computing refers to advanced computing systems that enable the processing of massive data and the execution of complex simulations across fields such as AI, science, defense, and climate research. The region leads due to strong investments from tech companies, governments, and institutions, with strong supercomputers and cloud HPC solutions fueling innovation. The North America high-performance computing (HPC) market is poised to expand rapidly, driven by growing demand for high-speed data processing, the integration of ML and AI workloads, and the expansion of cloud-based HPC solutions. The exponential growth of data in industries is fueling the need for real-time analytics and faster computation. HPC systems enable the rapid processing of large datasets, supporting complex simulations and decision-making. This demand is particularly strong in sectors such as healthcare, finance, and scientific research.

Moreover, the convergence of HPC with ML and AI is a key propeller, as these technologies need massive parallel processing power. HPC systems accelerate deep learning, automation, and predictive analytics in industries. This association is expanding HPC adoption in research and enterprise environments. Furthermore, cloud HPC is reducing barriers to entry by providing on-demand, scalable computing resources. Businesses are actively shifting to cloud and hybrid models to avoid high upfront infrastructure costs. This flexibility is fueling broader adoption in SMEs.

Despite growth, the market is constrained by factors such as complex implementation and maintenance processes, as well as high operational and energy costs. Deploying HPC systems comprises integrating advanced software and hardware into existing IT environments. Optimization and maintenance need specialized expertise. This complexity may delay adoption and raise operational risks. Similarly, HPC systems consumer significant power and need advanced cooling solutions. Maintenance and energy expenses majorly increase operational costs over time. These factors affect the long-term sustainability of businesses.

Nonetheless, the North America high-performance computing (HPC) industry stands to benefit from several key opportunities, such as growth in life sciences and healthcare, and integration with quantum computing. HPC is increasingly used in drug discovery, genomics, and precision medicine. It accelerates by efficiently processing complex biological data. This creates strong growth potential in the healthcare sector. Additionally, the convergence of HPC with emerging technologies, such as quantum computing, offers new avenues. Hybrid systems can solve previously intractable issues in cryptography and science. This represents a transformative future opportunity.

North America High-Performance Computing (HPC) Market: Dynamics

Growth Drivers

How is the North America high-performance computing market driven by accelerating cloud & hybrid deployment models?

Cloud-based HPC adoption is growing rapidly in the region, capturing the leading share of new HPC demand in 2024, with cloud deployments accounting for 42.8% of the total regional market. Hybrid and cloud models offer lower upfront costs, on-demand scalability, and access to high-end compute for smaller businesses. Major providers optimize HPC stacks for performance, AI integration, and security, allowing unified scaling for research and business workloads. This shift towards flexible architectures is augmenting the HPC market’s customer base.

How are advancements in HPC hardware and interconnect technologies driving the North America high-performance computing market?

Innovation in HPC hardware, such as GPU accelerators, faster CPUs, optimized storage, and high-speed interconnects, is fueling the North America high-performance computing (HPC) market. Next-generation architectures in the region deliver high performance per watt, supporting large-scale simulations, AI, and energy-efficient data centers. GPUs now power nearly 47% of HPC systems, enabling previously infeasible computations and advancing sustainability. These improvements strengthen regional dominance in high-performance computing infrastructure.

Restraints

Complex system integration & management slow the market progress

HPC environments are complex to optimize and configure due to numerous hardware layers, specialized interconnects, and different software stacks. Skilled system administrators and DevOps professionals with HPC expertise are in short supply, creating barriers to progress. Integration with business data workflows and legacy systems increases complexity. This complexity also increases operating risk for businesses without sophisticated IT practices. Hence, several potential users delay or downscale HPC deployment plans.

Opportunities

How is the growth in Edge‑to‑Cloud HPC use cases presenting favorable prospects for the North America High-Performance Computing (HPC) market expansion?

Emerging real-time processing needs in applications such as remote sensing, autonomous vehicles, and industrial automation are fueling hybrid HPC models that integrate edge devices with centralized clusters. Distributed HPC frameworks allow low-latency decision-making at the edge without compromising high-precision analysis in core systems. Vendors that simplify unified edge-to-cloud HPC workflows can capture fresh revenue streams. This shift offers opportunities beyond traditional data center deployment, expanding the HPC ecosystem and fueling the North America high-performance computing (HPC) industry.

Challenges

Regulatory & compliance complexities challenge the market growth

HPC users in regulated industries face layers of compliance requirements related to data residency, auditability, and access control. Cloud and hybrid HPC deployments further complicate compliance management. Ensuring that HPC workflows meet sector-specific standards raises administrative overhead. Businesses should align HPC infrastructure with changing regulations without disturbing performance. Navigating this regulatory landscape is still a strategic barrier for IT leaders.

Request Free SampleRequest Free SampleRequest Free Sample

Request Free SampleRequest Free SampleRequest Free Sample

North America High-Performance Computing (HPC) Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | North America High-Performance Computing (HPC) Market |

| Market Size in 2024 | 39.09 Billion |

| Market Forecast in 2034 | 66.91 Billion |

| Growth Rate | CAGR of 6.95% |

| Number of Pages | 230 |

| Key Companies Covered | IBM Corporation, Hewlett Packard Enterprise (HPE), Dell Technologies, Intel Corporation, NVIDIA Corporation, Advanced Micro Devices (AMD), Microsoft Corporation, Amazon Web Services (AWS), Oracle Corporation, Cisco Systems Inc., DataDirect Networks (DDN), Altair Engineering Inc., Rescale Inc., VDURA (formerly Panasas), Ampere Computing, and others. |

| Segments Covered | By Deployment Model, By Application, By End-User, and By Region |

| Regions Covered in North America | The U.S., Canada, Mexico, and Rest of North America |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

North America High-Performance Computing (HPC) Market: Segmentation

The North America high-performance computing (HPC) market is segmented based on deployment model, application, end-user, and region.

Why is the On-Premises segment projected to dominate the North America high-performance computing (HPC) market?

Based on the deployment model, the North America high-performance computing (HPC) industry is divided into on-premises, cloud-based, and hybrid. The on-premises segment accounts for 53% of the market share, as businesses and government/research labs prioritize control, performance, data sovereignty, and security with specialized infrastructure.

However, the cloud-based segment is the second-largest market, accounting for 30% of the market. This is backed by flexibility, scalability, and cost-effectiveness. Cloud HPC is widely adopted for variable compute needs, such as big data analytics and AI/ML training, enabling businesses to avoid high upfront infrastructure costs while accessing impactful computing resources on demand.

What factors help the Scientific Computing segment lead the North America high-performance computing (HPC) market?

Based on application, the North America high-performance computing (HPC) market is segmented into scientific computing, data analytics and big data, financial services, healthcare and life sciences, oil and gas exploration, and manufacturing and engineering. The scientific computing segment captures a dominating 30% market share. This is fueled by its entrenched role in national labs, government agencies, and research institutions, where HPC is vital for compute-intensive simulations and experimentation. This long-standing demand for traditional HPC workloads sustains the segment's leadership in scientific computing.

Nonetheless, the data analytics and big data segment holds a second rank with 25% market share. Businesses are actively leveraging HPC for ML, AI, real-time analytics, and the processing of massive datasets across the commercial, healthcare, and finance industries. These data-driven workloads are becoming central to HPC investments as businesses prioritize predictive modeling and insights at scale.

What are the key reasons for the leadership of the Government and Defense segment in the North America high-performance computing (HPC) market?

Based on end-user, the market is segmented into academic and research institutions, government and defense, enterprises, and SMEs. The government and defense segment dominates with a 32% market share, as defense labs, national agencies, and research institutions are investing heavily in HPC for climate modeling, simulations, strategic R&D, and national security analytics.

Conversely, the enterprises segment ranks second with 30% market share, as corporate users in industries such as energy, healthcare, manufacturing, and finance deploy HPC systems for big data analytics, engineering simulations, product innovation, and AI/ML workloads. Their scale, need for competitive insight, and investment capacity contribute to their strong rank.

North America High-Performance Computing (HPC) Market: Regional Analysis

Why is the United States outperforming other regions in the North America High-Performance Computing (HPC) market?

The United States is anticipated to retain its leading role in the North America high-performance computing (HPC) market, with a 6-8% CAGR, driven by major government investments, the presence of major technology companies, and the concentration of leading research and academic institutions. The U.S. dominates due to major government investments in research and national supercomputing infrastructure. Agencies such as NASA and the Department of Energy fund leading HPC projects. This allows advanced computational capabilities and world-class facilities, supporting industry dominance and innovation. Another major factor is the operation of major technology companies and HPC providers in the country. Their innovations in GPUs, AI-optimized systems, and processors make the United States a center for advanced HPC solutions. This attracts research and enterprise adoption at scale.

Furthermore, the concentration of major academic and research institutions further strengthens the United States ranking. National labs and universities largely rely on HPC for simulations, scientific computing, and data-intensive research, creating consistent demand for high-performance systems and fostering an expert workforce that supports HPC innovation and growth.

Why does Canada rank second in the North America high-performance computing (HPC) Market?

Canada ranks as the second-largest region in the North America high-performance computing (HPC) industry, with a 7.9% CAGR, driven by strong government support and strategic funding programs, a focus on data-intensive research and AI, and collaboration among industry, academia, and cloud/HPC providers. Canada’s dominance in the market is attributed to strong government support and strategic funding programs for AI and scientific computing. Initiatives like the Digital Research Infrastructure Strategy offer resources for advanced HPC facilities, allowing both industry and academia to adopt high-performance systems effectively.

Moreover, the country’s focus on data-intensive research and AI, especially through institutions such as national labs and the Vector Institute, is a key driver. HPC is essential for climate modeling, machine learning, and genomics, creating sustained demand for high-tech computing infrastructure in the country.

Also, collaboration between cloud/HPC providers, industry, and academia strengthens the country’s HPC network. Associations enable knowledge sharing, innovation, and access to cloud and hybrid HPC resources. This makes the country an appealing market for researchers and enterprises seeking high-performance and scalable computing solutions.

North America High-Performance Computing (HPC) Market: Competitive Analysis

The leading players in the North America high-performance computing (HPC) market are:

- IBM Corporation

- Hewlett Packard Enterprise (HPE)

- Dell Technologies

- Intel Corporation

- NVIDIA Corporation

- Advanced Micro Devices (AMD)

- Microsoft Corporation

- Amazon Web Services (AWS)

- Oracle Corporation

- Cisco Systems Inc.

- DataDirect Networks (DDN)

- Altair Engineering Inc.

- Rescale Inc.

- VDURA (formerly Panasas)

- Ampere Computing

What are the key trends in the North America high-performance computing (HPC) Market?

Emphasis on energy efficiency and green HPC:

With growing focus on sustainability, data centers and vendors are emphasizing energy-efficient HPC cooling and hardware technologies. Power-optimized architectures and liquid-cooling solutions reduce the carbon footprint and operating costs. This shift is influencing purchase decisions and long-term infrastructure planning in industries.

Growth of cloud‑based and hybrid HPC deployment:

Cloud HPC adoption continues to grow as businesses seek scalable, on-demand compute power without the heavy upfront investment. Hybrid models that blend on-premises infrastructure with cloud resources are gaining appeal, offering cost-effectiveness and flexibility. This trend allows businesses to manage peak workloads and optimize the total cost of ownership.

The North America high-performance computing (HPC) market is segmented as follows:

By Deployment Model

- On-Premises

- Cloud-Based

- Hybrid

By Application

- Scientific Computing

- Data Analytics and Big Data

- Financial Services

- Healthcare and Life Sciences

- Oil and Gas Exploration

- Manufacturing and Engineering

By End-User

- Academic and Research Institutions

- Government and Defense

- Enterprises

- SMEs

By Region

- North America

- United States

- Canada

- Mexico

Table Of Content

Methodology

FrequentlyAsked Questions

High-performance computing refers to advanced computing systems that enable the processing of massive data and the execution of complex simulations across fields such as AI, science, defense, and climate research. The region leads due to strong investments from tech companies, governments, and institutions, with strong supercomputers and cloud HPC solutions fueling innovation.

The North America high-performance computing (HPC) market is projected to grow due to the expansion of artificial intelligence and machine learning workloads, increased adoption of cloud computing, and growth in the financial services industry for risk modeling.

According to study, the North America high-performance computing (HPC) market size was around USD 39.09 billion in 2024 and is expected to grow to around USD 66.91 billion by 2034.

The CAGR value of the North America high-performance computing (HPC) market is expected to be around 6.95% during 2025-2034.

The major challenges restraining North America’s HPC market include high costs, deployment complexity, energy consumption, data security concerns, and talent shortages.

The North America high-performance computing (HPC) market is widely projected to reach its peak potential around 2030, when growth forecasts and key market sizes are expected to plateau after a decade of expansion.

The United States leads the North America HPC market due to substantial government funding, the presence of major technology companies driving innovation, and advanced research infrastructure.

The key players profiled in the North America high-performance computing (HPC) market include IBM Corporation, Hewlett Packard Enterprise (HPE), Dell Technologies, Intel Corporation, NVIDIA Corporation, Advanced Micro Devices (AMD), Microsoft Corporation, Amazon Web Services (AWS), Oracle Corporation, Cisco Systems, Inc., DataDirect Networks (DDN), Altair Engineering Inc., Rescale, Inc., VDURA (formerly Panasas), and Ampere Computing.

The industry's value chain includes research & development, software development, hardware manufacturing, deployment & implementation, system integration, and maintenance & support.

The report examines key aspects of the North America high-performance computing (HPC) market, including a detailed analysis of current growth factors and restraints, as well as future growth opportunities and challenges that will affect the market.

List of Contents

North America High-Performance Computing (HPC)Industry Perspective:Key Insights:OverviewDynamicsReport ScopeSegmentationRegional AnalysisCompetitive AnalysisWhat are the key trends in the North America high-performance computing (HPC) Market?The North America high-performance computing (HPC) market is segmented as follows:HappyClients