Microfluidic Components Market Size, Share, Analysis, Growth, Forecasts, 2032

Microfluidic Components Market By Product (Valve, Tubing, Nozzle, Microneedles, Pressure Controllers, Micropumps, Connectors, and Others) and By Industrial Application (Healthcare, Oil & Gas, Automotive, Consumer Electronics, Aerospace and Defense, and Others): Global Industry Perspective, Comprehensive Analysis, and Forecast, 2024-2032

| Market Size in 2023 | Market Forecast in 2032 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 4.85 Billion | USD 13.15 Billion | 11.72% | 2023 |

Microfluidic Components Industry Perspective

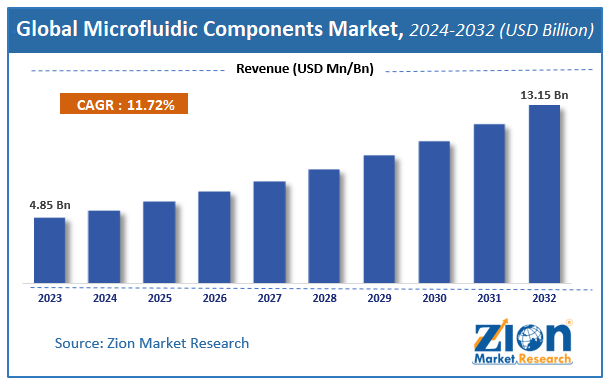

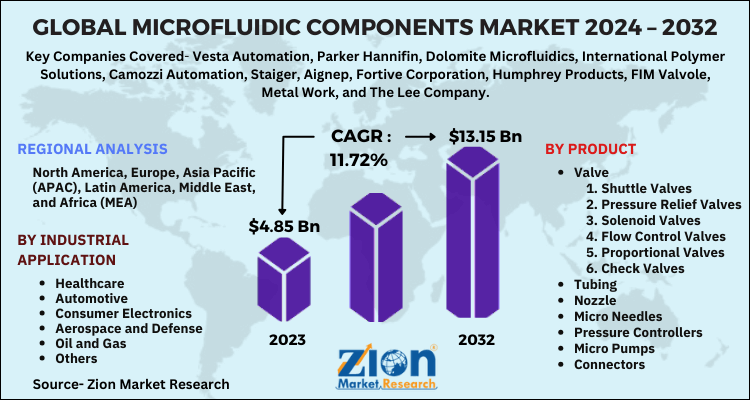

The global microfluidic components market size accrued earnings worth approximately USD 4.85 Billion in 2023 and is predicted to gain revenue of about USD 13.15 Billion by 2032, is set to record a CAGR of nearly 11.72% over the period from 2024 to 2032.

The report covers a forecast and an analysis of the microfluidic components market on a global and regional level. The study provides historical data from 2018 to 2022 along with a forecast from 2024 to 2032 based on revenue (USD Billion). The study includes the drivers and restraints of the microfluidic components market along with their impact on the demand over the forecast period. Additionally, the report includes the study of opportunities available in the microfluidic components market on a global and regional level.

Request Free SampleRequest Free SampleRequest Free Sample

Request Free SampleRequest Free SampleRequest Free Sample

Key Insights

- As per the analysis shared by our research analyst, the global Microfluidic Components market is projected to grow annually at a CAGR of around 11.72% over the forecast period (2024-2032).

- In terms of revenue, the global Microfluidic Components market size was valued at around USD 4.85 Billion in 2023 and is projected to reach USD 13.15 Billion by 2032.

- The market is driven by the rapid expansion of the pharmaceutical and biotechnology sectors and the growing preference for minimally invasive diagnostic procedures.

- Based on product, the market is segmented into valve, tubing, nozzle, microneedles, pressure controllers, micropumps, connectors, and others. Valves are further sub-segmented into shuttle valves, pressure relief valves, solenoid valves, flow control valves, proportional valves, check valves, and others.

- Based on industrial application, the market is segmented into healthcare, oil and gas, automotive, consumer electronics, aerospace and defense, and others.

- North America dominated the market with a share of 42% because of the presence of major biopharmaceutical companies, a robust research infrastructure, and high government funding for advanced medical technologies.

Microfluidic Components Market: Overview

Microfluidic components are tiny devices or systems designed to precisely control and manipulate small volumes of fluids, often at the microliter or nanoliter scale. These components, which can include pumps, valves, mixers, and sensors, are integral parts of microfluidic systems used in a wide range of applications, such as medical diagnostics, drug development, chemical analysis, and biological research. Microfluidic technology enables the miniaturization and automation of laboratory processes, leading to faster, more efficient, and cost-effective experiments. The precise control offered by microfluidic components allows for high-throughput screening, point-of-care testing, and the development of lab-on-a-chip devices, revolutionizing various fields of science and medicine.

The microfluidic components market involves the design, fabrication, and implementation of miniature systems that process or manipulate small amounts of fluids, typically in the range of microliters to picoliters. These systems utilize a variety of precise components such as channels, pumps, valves, and sensors to perform complex laboratory functions on a single chip, often referred to as "Lab-on-a-Chip" technology. By miniaturizing biological and chemical assays, these components enable faster analysis, reduced reagent consumption, and higher sensitivity compared to traditional macroscopic methods. The market is increasingly vital for modern medicine, supporting advancements in genomic sequencing, personalized medicine, and portable diagnostic devices. As the healthcare industry shifts toward decentralized testing and rapid results, microfluidic components serve as the foundational technology for the next generation of medical hardware.

Microfluidic Components Market: Dynamics

Growth Factors

Rise in Chronic Diseases and Demand for Rapid Diagnostics

The increasing demand for intelligent flow meters, smart sensors, and innovative pumps in high-end sectors, escalating technological advances, rising dependence on information precision and accuracy, and growing compact mini devices usage are primary growth factors for the microfluidic components market. The need for a steady replacement of valves, a growing number of refineries and petrochemical plants, and accelerating applications of microfluidics technology will also offer important growth opportunities for the market players.

The microfluidic components market is anticipated to grow, owing to the increasing refineries and petrochemical plants globally. Also, the growing application sectors of microfluidics technology are anticipated to offer substantial growth prospects to the market players. Initiatives taken by various government bodies to assimilate and maximize the use of microfluidic components in the legislation, favorable reimbursements policies, innovative mechanisms, and innovation in the healthcare domain for microfluidic components will also drive the market growth tremendously in the years ahead. However, the high cost of technologically-advanced valves and tubing’s may limit this market. In addition, commercialization and standardization of microfluidic components are major market challenges.

The report provides company market share analysis to give a broader overview of the key players in the microfluidic components market. In addition, the report also covers key strategic developments of the market including acquisitions & mergers, new product launch, agreements, partnerships, collaborations & joint ventures, research& development, regional expansion of major participants involved in the microfluidic components market on a global and regional basis.

Restraints

High Cost of Fabrication and Complex Integration

The manufacturing of microfluidic components, especially those utilizing silicon or glass, requires sophisticated cleanroom facilities and specialized lithography techniques. These high initial capital requirements and the complexity of the fabrication process act as a significant barrier for small-scale manufacturers and research startups. Consequently, the high end-user cost of advanced microfluidic systems can limit their adoption in developing regions with constrained healthcare budgets.

Additionally, integrating multiple microfluidic components into a single, cohesive, and reliable system remains a technical challenge. Issues such as fluid leakage, bubble formation, and component interoperability often lead to high rejection rates during the production phase. These technical bottlenecks and the associated maintenance costs can restrain the rapid commercialization of complex multi-component microfluidic platforms.

Opportunities

Advancements in Organ-on-a-Chip Technology

The emergence of "Organ-on-a-Chip" (OoC) platforms presents a lucrative opportunity for the microfluidic components market. These systems mimic the physiological functions of human organs, providing a more accurate model for drug toxicity testing and disease modeling than traditional animal testing. As pharmaceutical companies seek to reduce the time and cost of drug development, the demand for sophisticated chips, sensors, and micropumps that can replicate human biological environments is expected to skyrocket.

Moreover, the move toward personalized medicine requires diagnostic platforms that can analyze rare cells or specific biomarkers from very small patient samples. Microfluidic components are perfectly suited for these high-precision tasks, offering a path toward customized treatment plans. This alignment with the future of precision healthcare opens new revenue streams for component manufacturers specializing in high-sensitivity detection.

Request Free SampleRequest Free SampleRequest Free Sample

Request Free SampleRequest Free SampleRequest Free Sample

Challenges

Lack of Standardization and Regulatory Hurdles

A major challenge facing the microfluidic industry is the lack of standardized design and manufacturing protocols. Without universal standards for connectors, flow rates, and materials, it is difficult for components from different manufacturers to be used interchangeably, hindering the expansion of the broader market ecosystem. This fragmentation complicates the supply chain and increases the burden on researchers to develop bespoke solutions.

Furthermore, medical devices incorporating microfluidic components face stringent regulatory approval processes from bodies like the FDA and EMA. Proving the reliability and reproducibility of results at the microscale can be time-consuming and expensive. Navigating these evolving regulatory landscapes while maintaining a rapid pace of innovation remains a constant challenge for companies operating in this space.

Microfluidic Components Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Microfluidic Components Market |

| Market Size in 2023 | USD 4.85 Billion |

| Market Forecast in 2032 | USD 13.15 Billion |

| Growth Rate | CAGR of 11.72% |

| Number of Pages | 110 |

| Key Companies Covered | Vesta Automation, Parker Hannifin, Dolomite Microfluidics, International Polymer Solutions, Camozzi Automation, Staiger, Aignep, Fortive Corporation, Humphrey Products, FIM Valvole, Metal Work, and The Lee Company |

| Segments Covered | By product, By industrial application and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2022 |

| Forecast Year | 2024 - 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Microfluidic Components Market: Segmentation

The study provides a decisive view of the microfluidic components market by segmenting it based on the product, industrial application, and region.

Based on product, the market is segmented into valve, tubing, nozzle, microneedles, pressure controllers, micropumps, connectors, and others. Valves are further sub-segmented into shuttle valves, pressure relief valves, solenoid valves, flow control valves, proportional valves, check valves, and others.

By industrial application, market is segmented into healthcare, oil and gas, automotive, consumer electronics, aerospace and defense, and others.

Recent Developments

- In 2024, a leading biotech company launched a new thermoplastic-based microfluidic chip designed for high-throughput genomic sequencing, significantly reducing the cost per run.

- In 2025, a partnership was formed between a microfluidics specialist and a major pharma firm to develop organ-on-a-chip models for predicting liver toxicity during Phase I clinical trials.

- In 2024, researchers introduced a new 3D-printed microvalve system that can be integrated into flexible wearable devices for continuous sweat analysis and health monitoring.

Microfluidic Components Market: Regional Analysis

The asia pacific dominated the global microfluidic components market with the highest revenue share in 2023

The industrial revolution, flourishing multiple sectors, such as power and energy, chemicals, and aviation, rising investments in water infrastructure, increasing construction initiatives, particularly in China and India, improving living standards of the regional population, and increasing urbanization are the major factors influencing the microfluidic components in the Asia Pacific. The region is estimated to remain at the top position over the forecast time period as well, owing to the increasing government public and private funding for R&D. North America contributed the second-largest revenue share in 2023 to the global microfluidic components market. Wide adoption of technologically-advanced components and increasing focus on data precision and accuracy are major factors driving this regional market. The European microfluidic components market will register the highest CAGR over the forecast timeline.

Microfluidic Components Market: Competitive Analysis

Some key players in the microfluidic components market include

- Vesta Automation

- Parker Hannifin

- Dolomite Microfluidics

- International Polymer Solutions

- Camozzi Automation

- Staiger

- Aignep

- Fortive Corporation

- Humphrey Products

- FIM Valvole

- Metal Work

- The Lee Company.

- And Others

The global microfluidic components market is segmented as follows:

Global Microfluidic Components Market: By Product

- Valve

- Shuttle Valves

- Pressure Relief Valves

- Solenoid Valves

- Flow Control Valves

- Proportional Valves

- Check Valves

- Others

- Tubing

- Nozzle

- Micro Needles

- Pressure Controllers

- Micro Pumps

- Connectors

- Others

Global Microfluidic Components Market: By Industrial Application

- Healthcare

- Automotive

- Consumer Electronics

- Aerospace and Defense

- Oil and Gas

- Others

Global Microfluidic Components Market: By Region

- North America

- The U.S.

- Europe

- UK

- France

- Germany

- Asia Pacific

- China

- Japan

- India

- Latin America

- Brazil

- Middle East and Africa

Table Of Content

Methodology

FrequentlyAsked Questions

HappyClients