Lung Stent Market Size, Share, Value and Forecast Report 2034

Lung Stent Market By Product Type (Silicone Stents, Metal Stents, Hybrid Stents, and Biodegradable Stents), By Indication (Malignant Airway Obstruction, Benign Airway Stenosis, Tracheobronchomalacia, Fistulas and Perforations, and Post-Transplant Complications), By End User (Hospitals, Ambulatory Surgical Centers, Specialty Clinics, and Academic & Research Institutions), By Material (Nitinol, Stainless Steel, Silicone, Polyurethane, and Biodegradable Polymers), and By Region -Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 235.89 Million | USD 629.86 Million | 11.53% | 2024 |

Lung Stent Industry Perspective:

What are the expected growth rate and market size of the lung stent market during the forecast period?

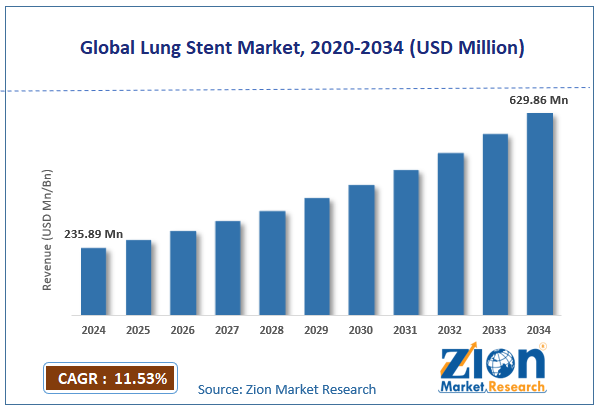

The global lung stent market size was worth approximately USD 235.89 million in 2024 and is projected to grow to around USD 629.86 million by 2034, with a compound annual growth rate of roughly 11.53% between 2025 and 2034.

Request Free SampleRequest Free SampleRequest Free Sample

Request Free SampleRequest Free SampleRequest Free Sample

Key Insights

- As per the analysis shared by our research analyst, the global lung stent market is estimated to grow annually at a compound annual growth rate of around 11.53% over the forecast period from 2025 to 2034.

- In terms of revenue, the global lung stent market size was valued at approximately USD 235.89 million in 2024 and is projected to reach USD 629.86 million by 2034.

- The lung stent market is expected to grow due to the rising global incidence of lung cancer and respiratory diseases, the increasing adoption of minimally invasive bronchoscopic procedures, expanding access to interventional pulmonology services, a growing elderly population, and ongoing innovation in stent materials and designs that improve patient outcomes.

- Based on product type, the metal stents segment is expected to lead growth in the lung stent market, while the biodegradable stents segment is anticipated to expand rapidly as research advances bring dissolvable airway stents closer to widespread clinical use.

- Based on indication, the malignant airway obstruction segment is expected to lead the lung stent market, while the benign airway stenosis segment is anticipated to grow steadily as improved diagnostic tools identify more patients with treatable non-cancerous airway narrowing.

- Based on end user, the hospitals segment is the largest, while the ambulatory surgical centers segment is growing rapidly as less invasive bronchoscopic procedures become suitable for outpatient settings.

- Based on material, the nitinol segment is expected to lead the lung stent market, while the biodegradable polymers segment is anticipated to grow strongly as clinical trials validate the safety and effectiveness of self-dissolving airway stents.

- Based on region, North America is projected to dominate the global lung stent market during the estimated period, followed by Europe.

Lung Stent Market: Overview

A lung stent, also called an airway or bronchial stent, is a small medical tube placed inside the airways to keep them open and help a person breathe easily. Airways can become narrow or blocked due to conditions such as cancer, infections, scarring, or inflammation, making breathing difficult. Doctors place the stent using a simple procedure called bronchoscopy, where a thin flexible tube is inserted through the nose or mouth to reach the lungs without the need for surgery. Once placed, the stent supports the airway walls and allows air to pass normally. Lung stents are made from different materials based on patient needs. Silicone stents are soft and removable, metal stents made from nitinol expand on their own for stronger support, and hybrid stents combine both features.

New biodegradable stents can dissolve over time, eliminating the need for removal. These stents are used for both cancer-related and non-cancer airway problems. They can quickly improve breathing and reduce symptoms such as coughing and shortness of breath. Lung stents also improve the quality of life for patients with severe airway obstruction. The lung stent market is growing due to the rising prevalence of lung diseases, greater access to treatment, ongoing medical innovation, minimally invasive procedures, and increasing demand for effective respiratory care solutions.

Impact of the USA-Israel War on Iran on the Lung Stent Market

The conflict involving the United States and Israel against Iran is anticipated to affect the lung stent market in both the short and long term. In the near term, some disruption to regional healthcare supply chains and medical trade in affected areas may create temporary challenges in the availability of stent devices and related equipment, while efforts are expected to focus on stabilizing access to essential care. Over the longer term, rebuilding healthcare systems and increased attention to respiratory care in affected populations are likely to support gradual recovery, creating opportunities for improved access to treatment and steady market growth.

Lung Stent Market: Technology Roadmap 2025 to 2034

What key trends and future developments will drive the lung stent market during the forecast period?

Advances in interventional pulmonology, stent engineering, and minimally invasive procedure technology are shaping the lung stent market, improving the safety and effectiveness of airway treatments while expanding the range of patients who can benefit from these devices. The market is expected to grow at a compound annual growth rate of around 11.53% over the forecast period, supported by rising demand from hospitals, pulmonology centers, and oncology departments, as well as an aging global population facing higher rates of lung cancer and chronic obstructive pulmonary disease.

The following roadmap outlines the key development phases expected during the forecast period.

2025 to 2027: Next-Generation Stent Design and Minimally Invasive Procedure Growth Phase

- Self-expanding metal stents with better coatings will reduce irritation and tissue growth, increasing use in both cancer and non-cancer airway cases.

- Robotic bronchoscopy systems will help doctors reach deeper lung areas, improving accuracy and increasing successful stent placement in difficult airway locations.

- Improved silicone stents with better grip will prevent movement after placement, reducing complications and improving patient comfort during recovery.

2028 to 2031: Biodegradable Technology Expansion and Digital Integration Phase

- Biodegradable airway stents will gain wider use as safety improves and manufacturing advances ensure consistent quality across different healthcare settings.

- Advanced imaging tools will help doctors select the appropriate stent size and position, reducing errors and improving treatment outcomes.

- Drug-eluting stents will be used more widely, releasing medicine into the airways to reduce scar tissue and improve long-term outcomes in selected patients.

2032 to 2034: Personalized and Smart Airway Management Phase

- 3D printing will enable custom stents for each patient, improving fit and reducing complications during airway treatment procedures.

- Smart stents with sensors will monitor airway conditions and send data to doctors, improving follow-up care and patient safety.

- Artificial intelligence tools will help doctors plan procedures, choose stents, and predict outcomes more accurately using advanced systems.

Lung Stent Market: Dynamics

Growth Drivers

The rising global burden of lung cancer and respiratory disease is driving the lung stent market.

The lung stent market is expanding steadily due to the rising number of lung diseases and increasing need for effective airway management solutions across global healthcare systems. Lung cancer remains a major driver, as tumors often block or press against airways, causing severe breathing problems that require immediate relief through stent placement. Lung stents help restore airflow quickly and improve patient comfort, making them essential in supportive and palliative care. Growth is also supported by non-cancer conditions such as chronic obstructive pulmonary disease, tuberculosis-related scarring, and complications after surgery that damage or narrow airways. Increasing air pollution, tobacco consumption, and workplace exposure to harmful particles continue to raise the number of respiratory cases worldwide.

Aging populations further contribute to higher disease burden, as older adults are more prone to chronic lung conditions. Advancements in bronchoscopy procedures and stent design are improving treatment success rates and accessibility. Expanding healthcare infrastructure and growing awareness about minimally invasive treatments are also encouraging adoption, supporting consistent demand for lung stents across both developed and emerging markets.

What role does the growth of interventional pulmonology as a medical specialty play in driving the lung stent market?

The lung stent market is growing as interventional pulmonology expands rapidly and demand for minimally invasive lung treatments rises across modern healthcare systems. Advanced bronchoscopic tools, such as flexible and rigid scopes, allow doctors to view airways clearly and perform procedures with high precision. Navigation systems and robotic assistance help reach deeper lung regions that were previously difficult to access without surgery. These improvements enable safer, quicker stent placement, reducing hospital stays and recovery time for patients. Increasing preference for non-surgical treatments is encouraging more hospitals to adopt these technologies. Growth in specialized training programs is also preparing more doctors to perform complex airway procedures.

Professional medical societies and clinical guidelines are spreading awareness about the benefits of early airway intervention. Rising patient awareness and better referral systems are further supporting treatment adoption, creating strong demand for lung stents across both urban and developing healthcare markets.

Restraints

Device-related complications and limited reimbursement policies slow growth in the lung stent market.

The lung stent industry faces several restraints, including clinical risks, high costs, and limited access to advanced treatment facilities across many regions. Stent-related complications, such as movement out of position, scar tissue formation, and mucus buildup, can affect breathing and require repeat procedures. Regular follow-up care is necessary, which increases treatment complexity and long-term cost for patients. The risk of infection and blockage also raises concerns among doctors and patients, slowing adoption in some cases. Limited insurance coverage in many countries makes procedures expensive and reduces patient access. High device costs add further pressure on healthcare budgets, especially in developing regions.

A lack of advanced bronchoscopy equipment and trained specialists limits availability in smaller hospitals and rural areas. Awareness about stent treatment options remains low in several markets, affecting early diagnosis and timely care. These challenges collectively limit widespread adoption and create barriers to consistent growth in the lung stent market.

Opportunities

What opportunities does the growing elderly population and increasing awareness of palliative respiratory care create for the lung stent market?

The lung stent market is creating strong opportunities driven by the rising elderly population and the increasing focus on improving the quality of life for patients with serious lung conditions. People aged 65 and above face a higher risk of lung cancer and chronic respiratory diseases, which often require airway support for better breathing. Growing life expectancy across regions such as North America, Europe, and Japan is increasing the number of patients who may benefit from stent treatment. Expanding focus on palliative care is also driving demand, as lung stents help reduce breathlessness and improve daily comfort in critical cases. Healthcare systems are placing greater emphasis on symptom relief and patient-centered care, thereby supporting wider adoption of airway stents.

Emerging markets across Asia Pacific, Latin America, and the Middle East are improving healthcare infrastructure and access to advanced treatments. Rising investments in hospitals, better diagnostic capabilities, and increasing awareness about respiratory care are further supporting growth, creating new opportunities for lung stent adoption globally.

Challenges

How do stent migration, granulation tissue formation, and training shortages challenge the lung stent market?

The lung stent industry faces several challenges, including clinical risks, limited expertise, and slow adoption of newer technologies across healthcare systems. Stent movement inside the airway remains a key concern, especially with silicone stents, as it can block other areas and require another procedure. Scar tissue formation around the stent can also reduce airflow over time, leading to breathing problems. Managing such complications requires skilled doctors and advanced medical facilities, which are not widely available in many regions. Shortage of trained interventional pulmonologists further limits access to treatment, especially in smaller hospitals and developing markets.

Limited long-term data on newer options, such as biodegradable stents, make some doctors cautious about using them. Regulatory approval processes for new designs often take time, delaying market entry of advanced products. These factors slow adoption rates and create barriers for consistent growth in the lung stent market across global healthcare environments.

Request Free SampleRequest Free SampleRequest Free Sample

Request Free SampleRequest Free SampleRequest Free Sample

Lung Stent Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Lung Stent Market |

| Market Size in 2024 | USD 235.89 Million |

| Market Forecast in 2034 | USD 629.86 Million |

| Growth Rate | CAGR of 11.53% |

| Number of Pages | 227 |

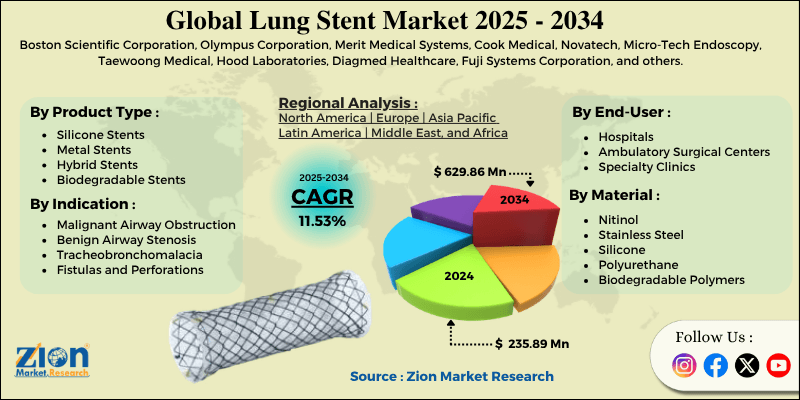

| Key Companies Covered | Boston Scientific Corporation, Olympus Corporation, Merit Medical Systems, Cook Medical, Novatech, Micro-Tech Endoscopy, Taewoong Medical, Hood Laboratories, Diagmed Healthcare, Fuji Systems Corporation, and others. |

| Segments Covered | By Product Type, By Indication, By End User, By Material, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Lung Stent Market: Segmentation

The global lung stent market is segmented based on product type, indication, end user, material, and region.

What makes metal stents the leading product type in the lung stent market?

Based on product type, the global lung stent market is divided into silicone stents, metal stents, hybrid stents, and biodegradable stents. The metal stents segment accounts for about 44% of the market and leads due to their self-expanding design, strong support for narrow airways, and easier placement via flexible bronchoscopy. The silicone stents segment holds around 32% of the market. It remains widely used because silicone stents are easy to adjust or remove, making them suitable for temporary use or changing clinical conditions.

Why does malignant airway obstruction lead the indication segment in the lung stent market?

Based on indication, the market is divided into malignant airway obstruction, benign airway stenosis, tracheobronchomalacia, fistulas and perforations, and post-transplant complications. The malignant airway obstruction segment accounts for about 52% of the market and leads, as cancers often block or press on airways, causing severe breathlessness that requires prompt treatment. The benign airway stenosis segment holds around 26% of the market. It is growing steadily as more patients with airway scarring, infections, and inflammatory conditions are diagnosed and referred for stent treatment.

What helps hospitals lead the end-user segment in the lung stent market?

Based on end user, the lung stent industry is classified into hospitals, ambulatory surgical centers, specialty clinics, and academic and research institutions. The hospitals segment holds about 61% of the market and leads because most lung stent procedures require inpatient care, advanced support, and teams of specialized doctors. The ambulatory surgical centers segment holds about 19% of the market. It is growing as improvements in stent technology and bronchoscopic technique allow selected lower-risk patients to undergo stent procedures safely in outpatient settings with shorter recovery times.

Why does nitinol lead the material segment in the lung stent market?

Based on material, the lung stent market is categorized into nitinol, stainless steel, silicone, polyurethane, and biodegradable polymers. The nitinol segment holds about 41% of the market and leads because it expands on its own after placement, providing strong and reliable airway support. The biodegradable polymers segment holds around 11% of the market. It is growing quickly as research focuses on dissolvable stents that remove the need for follow-up removal procedures in patients with non-cancer airway conditions.

Lung Stent Market: Regional Analysis

Why does North America lead the global lung stent market?

The lung stent market is led by North America, accounting for about 38% of global demand and expected to remain the top region throughout the forecast period. The region has a high number of patients with lung cancer and chronic respiratory diseases, which increases the need for airway management solutions such as lung stents. The United States plays a major role, supported by well-established hospitals, specialized cancer centers, and a strong presence of trained interventional pulmonologists. Advanced bronchoscopy systems, including robotic and navigation-assisted technologies, are widely used, allowing precise and safe stent placement. Favorable reimbursement policies and insurance coverage also make these procedures more accessible to patients compared to many other regions. Continuous research and development by leading medical device companies support innovation in stent design, including drug-eluting and biodegradable options.

Clinical trials and regulatory support further strengthen market growth. High healthcare spending and focus on improving patient outcomes drive the adoption of minimally invasive treatments. Strong collaboration between hospitals, research institutions, and device manufacturers ensures faster introduction of new technologies. Rising elderly population and increasing focus on palliative care also contribute to sustained demand, making North America the dominant region in the lung stent market.

What supports Europe's strong position in the global lung stent market?

The lung stent market ranks Europe as the second-largest region, contributing about 28% of the market share. Countries such as Germany, the United Kingdom, and France contribute significantly due to their well-developed medical infrastructure and availability of skilled specialists. Increasing cases of lung diseases, including cancer and chronic respiratory conditions, are driving demand for airway stents across the region. Public healthcare systems in many European countries provide access to essential treatments, supporting patient adoption of lung stent procedures. The growing emphasis on early diagnosis and minimally invasive techniques is driving the adoption of advanced bronchoscopy and stenting solutions.

Europe is also known for strict regulatory standards that ensure high-quality, safe medical devices on the market. Continuous research activities and collaborations between universities and medical device companies are supporting innovation in stent materials and design. An aging population and rising environmental concerns, such as air pollution, further increase the burden of respiratory diseases. The expansion of specialized pulmonary care centers and the increase in medical training programs are improving access to treatment. These factors collectively position Europe as a strong and stable second-leading market for lung stents.

Recent Market Developments

- In September 2025, Merit Medical Systems strengthened its interventional pulmonology segment through product development initiatives focused on minimally invasive airway treatments, supporting broader clinical adoption of lung stents.

Lung Stent Market: Competitive Analysis

The leading players in the global lung stent market are;

- Boston Scientific Corporation

- Olympus Corporation

- Merit Medical Systems

- Cook Medical

- Novatech

- Micro-Tech Endoscopy

- Taewoong Medical

- Hood Laboratories

- Diagmed Healthcare

- Fuji Systems Corporation

The global lung stent market is segmented as follows:

By Product Type

- Silicone Stents

- Metal Stents

- Hybrid Stents

- Biodegradable Stents

By Indication

- Malignant Airway Obstruction

- Benign Airway Stenosis

- Tracheobronchomalacia

- Fistulas and Perforations

- Post-Transplant Complications

By End User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Clinics

- Academic & Research Institutions

By Material

- Nitinol

- Stainless Steel

- Silicone

- Polyurethane

- Biodegradable Polymers

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table Of Content

Methodology

FrequentlyAsked Questions

A lung stent, also called an airway or bronchial stent, is a small medical tube placed inside the airways to keep them open and help a person breathe easily. It is placed during a bronchoscopy procedure and is used to treat breathing difficulties caused by cancer, scar tissue, structural airway problems, or other conditions.

The global lung stent market is expected to grow due to rising lung cancer incidence, increasing prevalence of respiratory diseases, growing adoption of minimally invasive bronchoscopic procedures, expanding interventional pulmonology services, and ongoing innovation in stent materials and designs that make treatment safer and more effective.

According to the study, the global lung stent market size was worth around USD 235.89 million in 2024 and is predicted to grow to around USD 629.86 million by 2034.

The compound annual growth rate value of the lung stent market is expected to be around 11.53% from 2025 to 2034.

North America is expected to lead the global lung stent market due to high lung cancer incidence rates, a well-developed interventional pulmonology specialty, advanced bronchoscopy infrastructure, strong reimbursement support, and significant research investment in airway stent technology.

The major players profiled in the global lung stent market include Boston Scientific Corporation, Olympus Corporation, Merit Medical Systems, Cook Medical, Novatech, Micro-Tech Endoscopy, Taewoong Medical, Hood Laboratories, Diagmed Healthcare, and Fuji Systems Corporation.

The report provides a detailed analysis of the lung stent market, including a thorough review of key growth drivers and market restraints, clinical technology trends, advances in stent design and materials, regional market performance, competitive landscape analysis, and a comprehensive forward-looking outlook covering all major product types, indications, end users, and materials across every key geography.

Pricing trends in the lung stent market show moderate increases driven by advanced materials, higher manufacturing costs, and premium pricing for innovative stents, such as biodegradable and drug-eluting designs.

Emerging trends in the lung stent market include 3D-printed patient-specific stents, biodegradable materials, and drug-eluting coatings that reduce complications, along with growing adoption of minimally invasive procedures and advanced bronchoscopy technologies.

Technological advancements in the lung stent market are improving precision, safety, and outcomes through better bronchoscopy systems, innovative stent designs, and minimally invasive techniques, thereby increasing adoption and supporting steady global market growth.

HappyClients