Healthcare Provider Network Management Market Size, Share and Forecast 2034

Healthcare Provider Network Management Market By Solution Type (Network Analytics, Claims Management, Provider Data Management, Contract Management, and Performance Management), By Deployment Mode (Cloud-Based, On-Premise, and Hybrid), By End User (Health Plans and Insurers, Hospitals and Health Systems, Third-Party Administrators, and Government and Public Health Agencies), By Organization Size (Large Enterprises, and Small and Medium Enterprises), and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

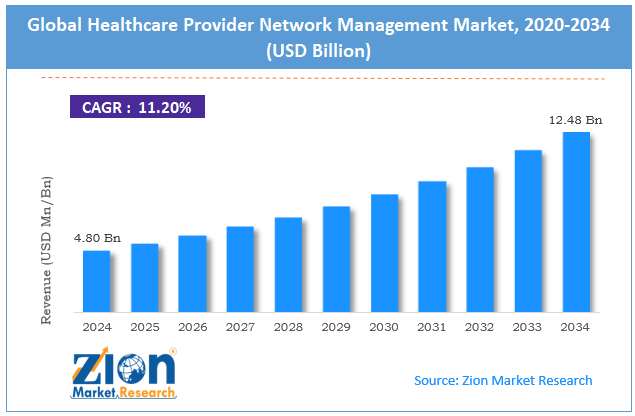

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 4.80 Billion | USD 12.48 Billion | 11.20% | 2024 |

Healthcare Provider Network Management Industry Perspective:

What are the expected growth rate and market size of the healthcare provider network management market during the forecast period?

The global healthcare provider network management market size was worth approximately USD 4.80 billion in 2024 and is projected to grow to around USD 12.48 billion by 2034, with a compound annual growth rate of roughly 11.20% between 2025 and 2034.

Request Free SampleRequest Free Sample

Request Free SampleRequest Free Sample

Key Insights

- As per the analysis shared by our research analyst, the global healthcare provider network management market is estimated to grow annually at a compound annual growth rate of around 11.20% over the forecast period from 2025 to 2034.

- In terms of revenue, the global healthcare provider network management market size was valued at approximately USD 4.80 billion in 2024 and is projected to reach USD 12.48 billion by 2034.

- The market is expected to grow due to complex provider networks, stricter regulations, cloud adoption, rising managed care enrollment, and increased healthcare IT investments.

- Based on solution type, the provider data management segment is expected to lead growth in the healthcare provider network management market, while the network analytics segment is anticipated to expand rapidly as health plans invest more in data-driven decision making for network design and optimization.

- Based on deployment mode, the cloud-based segment is expected to lead the market, while the hybrid deployment segment is anticipated to grow steadily as organizations seek a balance between data security and operational flexibility.

- Based on end user, the health plans and insurers segment is the largest, while the third-party administrators segment is growing rapidly as outsourced plan administration becomes more common across employer-sponsored and government-funded health programs.

- Based on organization size, the large-enterprise segment is expected to lead the market, while the small- and medium-sized enterprise segment is anticipated to grow strongly as affordable cloud solutions make advanced network management tools more accessible to smaller health plans and regional insurers.

- Based on region, North America is projected to dominate the global healthcare provider network management market during the estimated period, followed by Europe.

Healthcare Provider Network Management Market: Overview

Healthcare provider network management is the process of organizing and managing doctors, hospitals, clinics, and other care providers within a health insurance network. It ensures that patients have access to the right healthcare services in their area. The process includes verifying provider qualifications, managing contracts, updating provider information, and ensuring services are available when needed. Accurate network data helps patients find in-network doctors easily and avoid unexpected costs. Health insurers need clear details about each provider, including services offered, location, and agreed pricing. Providers must be regularly verified to maintain quality and compliance. If information is outdated or incorrect, it can lead to claim issues, delays, and poor patient experience.

Technology plays an important role by using software systems to manage data, automate tasks, and improve efficiency. Cloud-based platforms allow easier access and scalability, while analytics tools help identify gaps, improve planning, and support better decision-making. The healthcare provider network management market is growing as health plans focus on accurate provider data, regulatory compliance, cost reduction, and improved patient experience.

Impact of the USA-Israel War on Iran on the Healthcare Provider Network Management Market

The conflict involving the United States and Israel against Iran is expected to have a moderate but noticeable effect on the healthcare provider network management market in both the short and long term. In the near term, regional instability may disrupt healthcare operations, cause workforce shifts, and slow technology adoption in affected areas, while making it harder for organizations to maintain accurate provider data and network continuity. Over the longer term, rebuilding healthcare systems will drive investment in administrative infrastructure and network management tools, creating recovery opportunities and supporting steady demand for scalable and resilient solutions.

Healthcare Provider Network Management Market: Technology Roadmap 2025 to 2034

What key trends and future developments will drive the healthcare provider network management market during the forecast period?

Advances in cloud, AI, data interoperability, and regulatory technology are making provider network management faster, more accurate, and better at handling complex administrative tasks. The market is expected to grow at a compound annual growth rate of around 11.20% over the forecast period, supported by rising demand from health plans, government health agencies, and third-party administrators, as well as growing pressure from regulators to maintain accurate and accessible provider directories.

The following roadmap outlines the key development phases expected during the forecast period.

2025 to 2027: Platform Modernization and Regulatory Compliance Growth

- Cloud-based provider data platforms are expected to rapidly replace legacy systems, enabling real-time updates, higher scalability, and more cost-efficient operations.

- Automated credentialing powered by machine learning is expected to reduce manual effort while significantly improving accuracy and compliance tracking.

- Evolving government regulations around provider data accuracy and network adequacy are expected to push health plans toward advanced governance frameworks and automated compliance ecosystems.

2028 to 2031: Interoperability and Predictive Analytics Expansion

- API-driven data exchange is expected to become the backbone of seamless connectivity among providers, insurers, and regulatory systems, improving the reliability of real-time data.

- Predictive analytics tools are expected to proactively identify network gaps and guide strategic provider onboarding in underserved regions.

- Value-based care models are expected to expand further, with digital tools enabling outcome-based payment structures and performance-linked reimbursement systems.

2032 to 2034: Intelligent and Member-Centric Network Management

- Artificial intelligence is expected to power adaptive provider networks that continuously evolve based on patient behavior, demographics, and healthcare demand patterns.

- Real-time provider availability systems are expected to deliver highly accurate and dynamic access information, improving transparency and reducing patient friction.

- Fully integrated network management platforms are expected to unify credentialing, contracting, analytics, and member engagement into intelligent, automated ecosystems.

Healthcare Provider Network Management Market: Dynamics

Growth Drivers

The growing managed care complexity and enrollment are driving the healthcare provider network management market.

The healthcare provider network management market is growing steadily as health plans become larger and more complex, driven by rising enrollment in managed care programs worldwide. Expanding insurance coverage across regions such as North America, Europe, and Asia is increasing the number of providers and members within each network, making management more challenging. Strict government regulations are driving demand for accurate provider directories, proper network coverage, and regular compliance reporting. Healthcare organizations are adopting advanced software solutions to meet these requirements efficiently and avoid penalties. Ongoing mergers among hospitals and physician groups are also increasing the need for better tools to manage changing provider networks and contracts.

In addition, patients expect clear, reliable information when choosing healthcare providers, which is prompting insurers to maintain up-to-date, transparent directories. Avoiding billing issues and improving the patient experience further encourage investment in modern network management systems, supporting consistent market growth.

What role does the shift toward value-based care play in driving the healthcare provider network management market?

The healthcare provider network management market is growing as insurers shift from fee-based payments to value-based care that focuses on patient outcomes, quality, and cost efficiency. Health plans need better tools to track how providers perform, how patients respond to treatment, and how efficiently care is delivered. Such changes are increasing demand for advanced software that can manage provider data, along with performance metrics such as patient satisfaction, readmission rates, and preventive care outcomes. More complex payment models, such as shared savings and bundled payments, require accurate tracking and detailed reporting.

Large health systems and insurers managing many providers are investing in digital platforms that simplify contract management and improve decision-making. Growing focus on quality care and better healthcare outcomes is driving the adoption of modern network management solutions, supporting steady market expansion.

Restraints

High implementation costs, and resistance to technological change are slowing growth in the healthcare provider network management market.

The healthcare provider network management market faces several restraints, including costs, data accuracy, and system challenges. Setting up advanced network management software requires high investment in technology, training, and system integration, which can be difficult for smaller insurers. Keeping provider information accurate is also a major issue, as doctors frequently change locations, roles, and licenses, leading to outdated data. Many organizations still depend on manual processes, increasing the risk of errors. Resistance from staff used to older systems can slow adoption, while providers may not always update their information on time.

In addition, the lack of standard data formats across healthcare systems makes it difficult to share and update information smoothly. These challenges can reduce efficiency and delay digital transformation, limiting the overall growth speed of the healthcare provider network management market.

Opportunities

What opportunities does the expansion of telehealth and virtual care networks create for the healthcare provider network management market?

The healthcare provider network management market is gaining significant opportunities from the rapid growth of telehealth and virtual care services worldwide. Healthcare providers can treat patients through video calls and remote monitoring, reducing the need for location-based networks and expanding access to care. Health plans are building hybrid networks that include both in-person and virtual providers, increasing the need for advanced tools to manage these complex systems. Software solutions are helping track virtual services, verify licenses across different regions, and ensure compliance with healthcare regulations. Demand is rising for platforms that can manage both physical and digital provider networks while maintaining accurate directories.

Emerging markets in the Asia Pacific, Latin America, the Middle East, and Africa are also creating new growth opportunities as healthcare coverage expands and new systems are developed. Adoption of cloud-based technologies in these regions is making implementation easier and more cost-effective, supporting long-term growth of the healthcare provider network management market.

Challenges

How do regulatory fragmentation, and workforce shortages challenge the healthcare provider network management market?

The healthcare provider network management market faces several challenges, including data accuracy, regulatory requirements, workforce limitations, and technological constraints. Keeping provider directories up to date is difficult, as doctors frequently change details, leading to incorrect or outdated information that affects patient access and billing. Managing diverse regulatory requirements across regions adds complexity, as health plans must comply with multiple rules and reporting standards. Shortage of skilled professionals, such as credentialing experts and network analysts, also slows system adoption and reduces efficiency.

In addition, consolidation among software providers is raising concerns about higher costs, limited flexibility, and slower innovation. Many organizations hesitate to upgrade systems due to these issues, continuing to rely on outdated tools. These challenges make it harder for healthcare organizations to fully benefit from advanced network management solutions, affecting overall market growth and efficiency.

Healthcare Provider Network Management Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Healthcare Provider Network Management Market |

| Market Size in 2024 | USD 4.80 Billion |

| Market Forecast in 2034 | USD 12.48 Billion |

| Growth Rate | CAGR of 11.20% |

| Number of Pages | 228 |

| Key Companies Covered | Availity, Verity Solutions Group, Phynd Technologies, Kyruus, LexisNexis Risk Solutions, Quest Analytics, Symplr, The Council for Affordable Quality Healthcare, Salesforce Health Cloud, Cognizant Healthcare, and others. |

| Segments Covered | By Solution Type, By Deployment Mode, By End User, By Organization Size, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Healthcare Provider Network Management Market: Segmentation

The global healthcare provider network management market is segmented based on solution type, deployment mode, end user, organization size, and region.

What makes provider data management the leading solution type in the healthcare provider network management market?

Based on solution type, the global healthcare provider network management market is divided into network analytics, claims management, provider data management, contract management, and performance management. The provider data management segment accounts for about 35% of the market and leads because accurate and current provider data is the foundation of every other network management function, making it the highest-priority investment for health plans of all sizes. The network analytics segment holds around 22% of the market. It is growing rapidly as health plans adopt tools to identify network gaps and support better network planning decisions.

Why does the cloud-based deployment mode lead the healthcare provider network management market?

Based on deployment mode, the market is divided into cloud-based, on-premise, and hybrid. The cloud-based segment accounts for about 58% of the market and leads due to its lower upfront cost, faster deployment timelines, automatic software updates, and ability to scale alongside growing networks without significant additional infrastructure investment. The hybrid segment holds around 24% of the market. It is growing as organizations shift from on-premise systems to cloud solutions while maintaining control over sensitive data.

What helps health plans and insurers lead the end-user segment in the healthcare provider network management market?

Based on end user, the healthcare provider network management industry is classified into health plans and insurers, hospitals and health systems, third-party administrators, and government and public health agencies. The health plans and insurers segment holds about 47% of the market and leads because these organizations are directly responsible for building and maintaining provider networks as a core business function. The third-party administrators segment holds about 21% of the market. It is growing as employers and government programs outsource plan administration, increasing demand for efficient network management tools.

Why do large enterprises lead the organization size segment in the healthcare provider network management market?

Based on organization size, the healthcare provider network management market is categorized into large enterprises and small and medium enterprises. The large enterprises segment holds about 64% of the market share, driven by complex provider networks and strong demand for advanced management platforms. The small- and medium-sized enterprise segment accounts for around 36% of the market. It is growing quickly as cloud-based, modular pricing makes network management tools affordable for smaller health plans and insurers.

Healthcare Provider Network Management Market: Regional Analysis

Why does North America lead the global healthcare provider network management market?

The healthcare provider network management market is led by North America, accounting for about 41% of global demand due to its advanced healthcare system and strong adoption of digital technologies. The United States plays a major role, with a large number of insurers, managed care programs, and employer-based health plans operating under complex federal and state regulations. High healthcare spending and early adoption of advanced IT systems give the region a strong advantage in implementing modern network management solutions. Strict rules around provider data accuracy, network coverage, and compliance reporting are increasing the need for advanced network management software.

Healthcare organizations rely on these tools to manage provider information, meet regulatory requirements, and improve efficiency. The presence of leading technology providers and continuous innovation further strengthens North America’s leadership position. The region also has a well-developed healthcare IT industry, offering a wide range of solutions that support innovation and better system performance. Canada also contributes to growth, as healthcare authorities and insurers invest in modern systems to improve operations and service quality.

Strong regulatory enforcement and focus on patient experience are also key reasons behind regional dominance. Increasing focus on value-based care is encouraging the use of tools that track provider performance and improve patient outcomes. High healthcare spending, strong digital adoption, and availability of skilled professionals further support market growth, making North America the leading region in the healthcare provider network management market.

What supports Europe's strong position in the global healthcare provider network management market?

The healthcare provider network management market sees Europe as the second leading region, accounting for about 26% of global demand due to its strong healthcare systems and growing need for efficient administration. Countries such as Germany, the United Kingdom, France, and the Netherlands play a major role, supported by well-structured public healthcare systems and expanding private insurance services. Healthcare organizations across Europe are focusing on improving coordination between general doctors, specialists, and hospitals, which increases the need for better network management tools. Digital platforms help manage provider data, contracts, and performance, making healthcare delivery more organized and efficient. Efforts within the European Union to standardize data sharing and improve system compatibility are also supporting market growth by making it easier to adopt scalable solutions across multiple countries.

Strict data privacy laws, such as GDPR, are encouraging the adoption of secure, compliant technology systems. Rising cases of chronic diseases, along with an aging population, are increasing the demand for well-managed healthcare networks. The growing focus on integrated care and better patient outcomes is further driving the adoption of advanced network management solutions, strengthening Europe’s position in the healthcare provider network management market.

Recent Market Developments

- In April 2025, Veeva Systems introduced Veeva AI, embedding generative AI tools into its cloud platform to enhance provider data insights, automation, and decision-making in network and CRM systems.

- In August 2025, IQVIA and Veeva Systems announced a long-term global partnership to integrate data and software platforms, improving provider data management and network coordination capabilities for healthcare and pharmaceutical clients.

Healthcare Provider Network Management Market: Competitive Analysis

The leading players in the global healthcare provider network management market are;

- Availity

- Verity Solutions Group

- Phynd Technologies

- Kyruus

- LexisNexis Risk Solutions

- Quest Analytics

- Symplr

- The Council for Affordable Quality Healthcare

- Salesforce Health Cloud

- Cognizant Healthcare

The global healthcare provider network management market is segmented as follows:

By Solution Type

- Network Analytics

- Claims Management

- Provider Data Management

- Contract Management

- Performance Management

By Deployment Mode

- Cloud-Based

- On-Premise

- Hybrid

By End User

- Health Plans and Insurers

- Hospitals and Health Systems

- Third-Party Administrators

- Government and Public Health Agencies

By Organization Size

- Large Enterprises

- Small and Medium Enterprises

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table Of Content

Methodology

FrequentlyAsked Questions

Healthcare provider network management is the process of organizing and managing doctors, hospitals, clinics, and other care providers within a health insurance network. It ensures that patients have access to the right healthcare services in their area.

The global healthcare provider network management market is growing due to rising managed care enrollment, stricter regulations, cloud adoption, telehealth expansion, and increased use of AI and analytics to improve network efficiency.

According to the study, the global healthcare provider network management market size was approximately USD 4.80 billion in 2024 and is expected to reach USD 12.48 billion by 2034.

The compound annual growth rate value of the healthcare provider network management market is expected to be around 11.20% from 2025 to 2034.

North America is expected to lead the global healthcare provider network management market due to its large and complex managed care environment, strict regulatory requirements around provider directory accuracy and network adequacy, widespread adoption of healthcare information technology, and the presence of major network management software vendors based in the United States.

Which are the major players driving the growth of the healthcare provider network management market?

The major players profiled in the global healthcare provider network management market include Availity, Verity Solutions Group, Phynd Technologies, Kyruus, LexisNexis Risk Solutions, Quest Analytics, Symplr, The Council for Affordable Quality Healthcare, Salesforce Health Cloud, and Cognizant Healthcare.

The report provides a detailed analysis of the healthcare provider network management market, covering growth drivers, restraints, technology trends, regional performance, and competition. It also offers a future outlook across solution types, deployment modes, end users, and organization sizes in key regions.

Healthcare provider network management market trends are evolving toward digital platforms, real-time data accuracy, and AI-driven insights, while consumers increasingly expect transparent provider information, easy access to care, and improved service experiences.

Healthcare provider network management market opportunities are growing across telehealth integration, value-based care management, provider analytics, and cloud-based solutions supporting insurers, hospitals, and managed care organizations.

Healthcare provider network management market innovations include the adoption of artificial intelligence, predictive analytics, cloud platforms, interoperability tools, and automated compliance systems, which improve provider tracking, decision-making, and the efficient management of complex healthcare networks.

List of Contents

Healthcare Provider Network ManagementIndustry Perspective:Key InsightsOverviewTechnology Roadmap 2025 to 2034DynamicsReport ScopeSegmentationRegional AnalysisRecent Market DevelopmentsCompetitive AnalysisThe global healthcare provider network management market is segmented as follows:HappyClients