Edge Management and Orchestration Platforms Market Size, Share and Forecast 2034

Edge Management and Orchestration Platforms Market By Component (Hardware, Software, and Services), By Deployment Mode (On-Premises and Cloud), By Application (Telecommunications, Energy & Utilities, Manufacturing, Healthcare, Retail, Transportation & Logistics, and Others), By Enterprise Size (Small & Medium Enterprises and Large Enterprises), By End-User (BFSI, Manufacturing, IT & Telecom, Healthcare, Retail, and Others), and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2026 - 2034

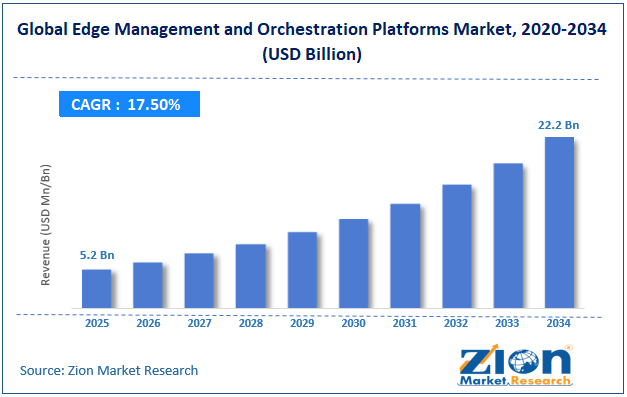

| Market Size in 2025 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 5.2 Billion | USD 22.2 Billion | 17.5% | 2025 |

Edge Management and Orchestration Platforms Industry Perspective:

What will be the size of the global edge management and orchestration platforms market during the forecast period?

The global edge management and orchestration platforms market size was worth around USD 5.2 billion in 2025 and is predicted to grow to around USD 22.2 billion by 2034, with a compound annual growth rate (CAGR) of roughly 17.5% between 2026 and 2034.

Key Insights

- As per the analysis shared by our research analyst, the global edge management and orchestration platforms market is estimated to grow annually at a CAGR of around 17.5% over the forecast period (2026-2034).

- In terms of revenue, the global edge management and orchestration platforms market size was valued at around USD 5.2 billion in 2025 and is projected to reach USD 22.2 billion by 2034.

- Expansion of IoT devices and connected assets is expected to propel the edge management and orchestration platforms market over the projected period.

- Based on the component, the software segment held the largest market share in 2025.

- Based on the deployment mode, the on-premises segment held a prominent market share in 2025.

- Based on the application, telecommunications dominate the market.

- Based on the enterprise size, the large enterprises segment held the largest revenue share in 2025.

- Based on the end user, the BFSI segment held the largest revenue share in 2025.

- Based on region, North America led the edge management and orchestration platforms market in terms of revenue, which is around 36% of the global market.

Edge Management and Orchestration Platforms Market: Overview

The edge management and orchestration platform is a platform that allows an organization to manage applications, devices, and infrastructure deployed at the edge computing level through configuration, monitoring, securing, and deployment from one location. The edge management and orchestration platforms automate the management of resources in the edge environment by orchestrating, provisioning, updating, securing, and monitoring thousands of edge locations. The computing resources at the edge will run efficiently while being coordinated with central cloud or data center resources.

Impact of the USA-Israel War on Iran on the Edge Management and Orchestration Platforms Market

The war between the U.S. and Israel against Iran will have both positive and negative effects in the long term on the edge management and orchestration platforms market. In the short run, the geopolitics involved might cause disruptions in the semiconductor supply chain industry and lead to rising costs of hardware and logistics, and delay any investments in the edge infrastructure of enterprises. But the increased interest in cybersecurity, modernization of defense systems, critical infrastructure protection, and distributed AI will contribute significantly to boosting the edge management and orchestration platforms market.

Edge Management and Orchestration Platforms Market: Dynamics

Growth Drivers

Why does the rapid growth of edge computing deployments drive the edge management and orchestration platforms market?

The rapid increase in the number of deployments of edge computing is the key factor driving the growth in the edge management and orchestration platforms market. Organizations are now processing data close to the point of generation to ensure better performance of applications, reduced latency, and avoiding unnecessary expenses on bandwidth usage. Several industries, including manufacturing, telecommunications, health care, retail, transportation, and energy, are deploying thousands of edge computing devices across different geographical locations for performing tasks such as real-time analytics, AI inferencing, and IoT. With the increasing complexities in these distributed environments, the need for a centralized platform that helps to manage provisioning of devices, deployment of applications, workload orchestration, monitoring, security, and management of the life cycle is increasing.

Restraints

High deployment and infrastructure costs hamper the growth of the edge management and orchestration platforms industry

Costs associated with high deployment and infrastructure are major constraints to the edge management and orchestration platforms market. There is a high investment involved in setting up an edge computing environment through the deployment of edge servers, edge gateways, networking and storage devices, software licensing, cybersecurity solutions, and integration services. Moreover, there are cost implications for maintenance, remote monitoring, software upgrades, and the manpower required to manage edge infrastructure spread across different geographical locations. Integration of the edge platform with the current IT/OT platforms makes the process difficult and costly. Such high implementation costs can slow down implementation processes and increase the time required to realize returns on investments.

Opportunities

Why does the growing product launch offer a lucrative opportunity for edge management and orchestration platforms market?

The increasing number of product launches is expected to offer a potential opportunity to the edge management and orchestration platforms market. For instance, in September 2025, a leading developer and innovator of compute and connectivity IoT solutions that drive Edge AI apps, Lantronix Inc., announced its innovative no-code development platform – EdgeFabric.ai™ – designed specifically for Lantronix Open-Q™ System-on-Module (SOM) solutions. With EdgeFabric.ai™, organizations can now create and deploy their Edge AI apps in minutes rather than months.

Challenges

How does the shortage of skilled edge computing professionals pose a significant challenge to the edge management and orchestration platforms market?

The lack of professional edge computing experts is a key issue in the edge management and orchestration platforms market, restricting organizations' ability to operate increasingly sophisticated edge infrastructures. In order to manage edge infrastructure, a combination of various skills, including cloud computing, container orchestration, Kubernetes, networking, Internet of Things (IoT), artificial intelligence (AI), cybersecurity, and OT, is required. Nevertheless, many organizations find it hard to attract and retain specialists who possess all the above-mentioned skills.

Consequently, delays in implementing the infrastructure, increased operational costs, errors in its configuration, and additional vulnerabilities to cybersecurity attacks become possible. In addition, the skills shortage limits the implementation of sophisticated orchestration tools and large-scale edge operations, and hinders SMEs from implementing edge management platforms due to the high cost of hiring relevant employees.

Edge Management and Orchestration Platforms Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Edge Management and Orchestration Platforms Market |

| Market Size in 2025 | USD 5.2 Billion |

| Market Forecast in 2034 | USD 22.2 Billion |

| Growth Rate | CAGR of 17.5% |

| Number of Pages | 227 |

| Key Companies Covered | ADLINK Technology Inc., Hewlett Packard Enterprise (HPE), Amazon Web Services (AWS), Cisco Systems Inc., Google LLC, Dell Technologies Inc., FogHorn Systems Inc., Nokia Corporation, Huawei Technologies Co. Ltd., IBM Corporation, Microsoft Corporation, Juniper Networks Inc., Saguna Networks Ltd., Red Hat Inc., VMware Inc., StackPath LLC, EdgeConneX Inc., Zededa Inc., Ericsson AB, and Mavenir Systems Inc., and others. |

| Segments Covered | By Component, By Deployment Mode, By Deployment Mode, By Enterprise Size, By End User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 to 2024 |

| Forecast Year | 2026 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Edge Management and Orchestration Platforms Market: Segmentation

Component Insights

Why does the software segment hold a prominent position in the edge management and orchestration platforms market?

The software segment held the largest share in the edge management and orchestration platforms industry in 2025 and is expected to continue the same pattern over the projected period. This trend is driven by the widespread adoption of edge computing, distributed IoT deployments, and AI-powered applications. Businesses are investing in edge computing management software to centrally manage their thousands of edge computing devices and applications through a single platform. The growing use of containerized workloads, Kubernetes-based orchestration, and multi-cloud edge computing platforms has further increased the need for software to automate scheduling, management, and OTA updates for workloads and applications.

Deployment Mode Insights

How does the on-premises segment capture the largest share in the edge management and orchestration platforms market?

The on-premises segment held a prominent share in the edge management and orchestration platforms industry in 2025. The growth is fueled by the rising need for data security, regulation compliance, and real-time processing in mission-critical settings. The sectors that favor on-premise edge computing include manufacturing, energy and utility companies, healthcare providers, telecoms, military defense, and the finance industry, since they can retain full control over their critical operational and business data while maintaining high standards of data sovereignty and cybersecurity. With on-premises edge management systems, businesses can manage their edge devices and applications even when network connectivity is unavailable.

Application Insights

Does the telecommunications segment capture the largest market share in the edge management and orchestration platforms market?

The telecommunications dominate the edge management and orchestration platforms market. The growth will be fueled by the fast proliferation of 5G networks, multi-access edge computing (MEC), and cloud-native network infrastructures. Telecommunications companies are installing distributed edge infrastructure to deliver ultra-low-latency services, network slicing, analytics, content distribution, and AI-based network optimization. Edge management and orchestration software enable centralized configuration, automated workload deployment, lifecycle management of applications and services, remote monitoring, and cybersecurity for thousands of geographically distributed edge nodes. More and more telecommunications firms are adopting virtualized network functions (VNFs), cloud-native network functions (CNFs), private 5G networks, and Open RAN architectures. Due to continuous investments in advanced connectivity and edge technologies, the telecommunications sector will likely remain the fastest-growing segment of the market.

Enterprise Size Insights

How does the large enterprises segment capture the largest share in the edge management and orchestration platforms market?

The large enterprises segment held the largest revenue share in the edge management and orchestration platforms market in 2025. Growth is fueled by significant investment in edge computing, digital transformation, and enterprise automation projects. Major corporations in the manufacturing, telecommunications, healthcare, retail, energy, transportation, and banking industries have extensive networked infrastructures comprising distributed sites, IoT devices, and edge computing systems that need to be managed centrally. The edge management system allows such companies to provision devices, deploy applications, orchestrate workload, enforce security policies, monitor remotely, and perform software updates at thousands of edge sites.

End User Insights

Why does the BFSI segment capture the largest market share in the edge management and orchestration platforms market?

The BFSI segment held the largest revenue share in the edge management and orchestration platforms industry in 2025. The increase is due to growing demand for real-time transaction processing, cybersecurity, regulatory compliance, and customer satisfaction. Financial firms are using edge computing architecture across their branches, ATMs, payment terminals, and data centers to facilitate low-latency transactions, detect fraud, enable AI-based analysis, and support online banking services. Platforms for managing and orchestrating edge computing provide centralized control over configuration, monitoring, application deployment, policy management, and software upgrades for geographically dispersed financial endpoints.

Regional Insights

Why does North America lead the edge management and orchestration platforms market?

North America led the edge management and orchestration platforms market in terms of revenue, which is around 36% of the global market. The region's growth is attributed to the deployment of edge computing solutions, the development of 5G network infrastructure, and significant investments in AI, IIoT, and cloud-native technologies. Many large cloud computing service providers, telecom operators, and IT vendors rapidly deploy edge computing infrastructure across sectors such as manufacturing, healthcare, retail, financial services, energy, and transportation. The increasing demand for processing real-time data, supporting latency-sensitive applications, and managing distributed edge environments is driving the emergence of edge computing orchestration platforms.

Edge Management and Orchestration Platforms Market: Competitive Analysis

The global edge management and orchestration platforms market is dominated by players like:

- ADLINK Technology Inc.

- Hewlett Packard Enterprise (HPE)

- Amazon Web Services (AWS)

- Cisco Systems Inc.

- Google LLC

- Dell Technologies Inc.

- FogHorn Systems Inc.

- Nokia Corporation

- Huawei Technologies Co. Ltd.

- IBM Corporation

- Microsoft Corporation

- Juniper Networks Inc.

- Saguna Networks Ltd.

- Red Hat Inc.

- VMware Inc.

- StackPath LLC

- EdgeConneX Inc.

- Zededa Inc.

- Ericsson AB

- Mavenir Systems Inc

The global edge management and orchestration platforms market is segmented as follows:

By Component

- Hardware

- Software

- Services

By Deployment Mode

- On-Premises

- Cloud

By Application

- Telecommunications

- Energy & Utilities

- Manufacturing

- Healthcare

- Retail

- Transportation & Logistics

- Others

By Enterprise Size

- Small and Medium Enterprises

- Large Enterprises

By End User

- BFSI

- Manufacturing

- IT & Telecom

- Healthcare

- Retail

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table Of Content

Methodology

FrequentlyAsked Questions

The edge management and orchestration platform is a platform that allows an organization to manage applications, devices, and infrastructure deployed at the edge computing level through configuration, monitoring, securing, and deployment from one location.

The edge management and orchestration platforms market is primarily driven by the rapid expansion of edge computing deployments, increasing adoption of IoT devices, and growing demand for low-latency, real-time data processing across industries such as manufacturing, telecommunications, healthcare, retail, transportation, and energy.

The major challenges restraining the growth of the edge management and orchestration platforms market include high deployment and infrastructure costs, which make large-scale edge implementations expensive, particularly for small and medium-sized enterprises (SMEs). Organizations also face the complexity of managing heterogeneous edge environments that include diverse hardware, operating systems, communication protocols, and applications from multiple vendors.

Based on the application, the telecommunications segment is expected to dominate the edge management and orchestration platforms market growth during the projected period.

The edge management and orchestration platforms market is being shaped by several emerging trends and innovations, including the rapid adoption of AI-powered edge computing, 5G-enabled multi-access edge computing (MEC), and cloud-native architectures based on containers and Kubernetes. Organizations are increasingly deploying AI inference at the edge to enable real-time decision-making while reducing latency and bandwidth consumption. The growing use of zero-touch provisioning, policy-based automation, and AIOps is simplifying the deployment, monitoring, and lifecycle management of distributed edge infrastructure.

According to the report, the global edge management and orchestration platforms market size was worth around USD 5.2 billion in 2025 and is predicted to grow to around USD 22.2 billion by 2034.

The global edge management and orchestration platforms market is expected to grow at a CAGR of 17.5% during the forecast period.

The global edge management and orchestration platforms industry growth is expected to be led by North America over the forecast period.

The global edge management and orchestration platforms market is dominated by players like ADLINK Technology Inc., Hewlett Packard Enterprise (HPE), Amazon Web Services (AWS), Cisco Systems Inc., Google LLC, Dell Technologies Inc., FogHorn Systems Inc., Nokia Corporation, Huawei Technologies Co. Ltd., IBM Corporation, Microsoft Corporation, Juniper Networks Inc., Saguna Networks Ltd., Red Hat Inc., VMware Inc., StackPath, LLC, EdgeConneX Inc., Zededa Inc., Ericsson AB, and Mavenir Systems Inc., among others.

The edge management and orchestration platforms market report covers the geographical market along with a comprehensive competitive landscape analysis. It also includes cash flow analysis, profit ratio analysis, market basket analysis, market attractiveness analysis, sentiment analysis, PESTLE analysis, trend analysis, SWOT analysis, trade area analysis, demand & supply analysis, Porter’s five forces analysis, and value chain analysis.

HappyClients