Copper Clad Laminate Market Size, Share, Trends, Growth and Forecast 2034

Copper Clad Laminate Market By Type (Rigid and Flexible), By Material (Epoxy, Phenolic, Polyimide, and Others), By End Use Industry (Automotive, Aerospace & Defense, Consumer Electronics, Healthcare, and Others), and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

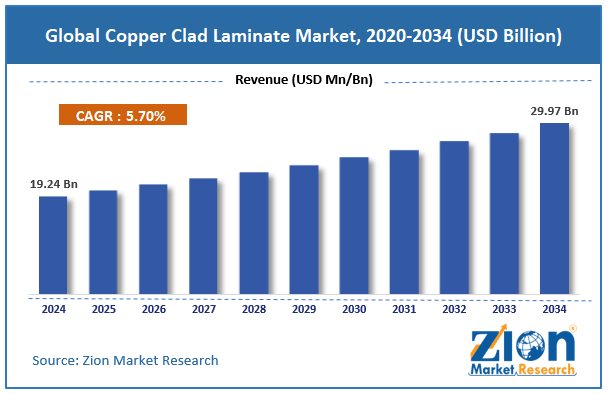

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 19.24 Billion | USD 29.97 Billion | 5.70% | 2024 |

Copper Clad Laminate Industry Perspective:

What will be the size of the global copper clad laminate market during the forecast period?

The global copper clad laminate market size was around USD 19.24 billion in 2024 and is projected to reach USD 29.97 billion by 2034, with a compound annual growth rate (CAGR) of roughly 5.70% between 2025 and 2034.

Request Free SampleRequest Free Sample

Request Free SampleRequest Free Sample

Key Insights:

- As per the analysis shared by our research analyst, the global copper clad laminate market is estimated to grow annually at a CAGR of around 5.70% over the forecast period (2025-2034)

- In terms of revenue, the global copper clad laminate market was valued at around USD 19.24 billion in 2024 and is projected to reach USD 29.97 billion by 2034.

- The copper clad laminate market is projected to grow significantly, driven by the expansion of 5G infrastructure, rising consumer electronics consumption, and industrial automation.

- Based on type, the rigid segment is expected to lead the market, while the flexible segment is expected to grow considerably.

- Based on material, the epoxy segment is the dominating segment, while the polyimide segment is projected to witness sizeable revenue over the forecast period.

- Based on end use industry, the consumer electronics segment is expected to lead the market, followed by the automotive segment.

- Based on region, the Asia Pacific is projected to dominate the global market during the estimated period, followed by North America.

Copper Clad Laminate Market: Overview

Copper-clad laminate is a composite material used as the base for printed circuit boards (PCBs), comprising a dielectric substrate, usually a fiberglass-reinforced epoxy resin, bonded to thin copper foil on one or both sides. It provides electrical insulation, mechanical support, and a conductive surface for circuit patterns, while withstanding heat during assembly and soldering. The global copper clad laminate market is likely to expand rapidly, fueled by rising consumer electronics demand, the growth of automotive electronics, and 5G infrastructure deployment. The global rise in laptops, wearables, home electronics, and smartphones is driving increased PCB production, which relies on high-quality CCL. Multilayer and compact designs need laminates with strong electrical and thermal stability. Growing consumer electronics adoption continues to fuel demand for advanced CCL materials.

Moreover, electric vehicles and modernized driving systems require high-performance, durable PCB laminates. Automotive electronics prefer CCLs that tolerate vibration, heat, and electrical stress. This creates significant demand for specialized laminates in the automotive industry. Furthermore, 5G networks demand PCBs capable of handling high-frequency signals with negligible loss. Low-dielectric and thermally stable CCLs are vital for base stations and network devices. The worldwide deployment of 5G is fueling the adoption of improved laminates in telecommunications.

Nevertheless, the global market faces limitations due to volatile raw-material prices and complex manufacturing requirements. Varying costs of resin, fiberglass, and copper create production uncertainties. Growing material prices reduce profitability for CCL manufacturers. Price volatility hampers continuous investment planning and market growth. Likewise, producing high-performance laminates requires precise equipment, strict quality control, and skilled labor. Smaller producers may struggle to consistently meet technical standards. Manufacturing complexity may hamper industry scalability and participation. Still, the global copper clad laminate industry benefits from several favorable factors, such as advanced high-speed laminates and the growth of flexible and HDI CCLs.

High-frequency communication systems, AI applications, and 5G need low-loss laminates. Manufacturers can develop premium CCL products targeting these high-performances boards. This segment offers major profitability and growth potential. Additionally, flexible laminates and high-density interconnect (HDI) boards are in demand for IoT applications and foldable devices. Specialized laminates cater to the progressing electronics market. This creates opportunities for higher-margin products and differentiation.

Impact of the USA-Israel war on Iran on the Copper Clad Laminate Market

The ongoing U.S-Israel war on Iran has elevated worldwide geopolitical risk, leading to increased raw material and energy prices, longer lead times for electronic components, and supply chain disturbances. These pressures are cascading into the copper clad laminate industry, driving up logistics and production costs, squeezing margins, and potentially slowing electronics and PCB demand as manufacturers deal with trade uncertainties and inflation. These conflict-driven instabilities prompt companies to reassess sourcing tactics and buffer stocks to mitigate risks in the global electronics supply chain.

Copper Clad Laminate Market: Dynamics

Growth Drivers

How is the growth of 5G infrastructure and high-speed connectivity driving the copper clad laminate market?

The deployment of 5G networks worldwide is driving demand for advanced CCL materials with superior transmission properties. By 2025, worldwide 5G connections are projected to exceed 2 billion, demanding extensive telecom infrastructure upgrades. High-frequency laminates are actively used in network equipment and base stations. Economies like the U.S., China, and South Korea are leading aggressive 5G rollouts. This transition is accelerating demand for premium products and innovation in the copper clad laminate market.

How are technological developments in high-performance materials impacting the copper clad laminate market growth?

Ongoing advances in CCL materials, such as high-thermal-resistance and low-loss laminates, are fueling industry evolution. Manufacturers are developing products well-suited for high-speed, high-frequency applications such as autonomous systems and AI hardware. Advanced materials like halogen-free laminates and resin-coated copper are gaining attention. Research and development investments in the electronics materials industry have increased by approximately 8-10% yearly. These advancements are facilitating differentiation and higher margins within the market.

Restraints

Environmental regulations and compliance costs unfavorably impact the market progress

Strict environmental regulations on chemical use and emissions are intensifying compliance pressures. Governments in regions such as Asia and Europe are enforcing stringent waste-disposal and carbon-reduction norms. Manufacturers should invest heavily in environmentally friendly materials and processes to meet these standards. Compliance costs can rise by nearly 10-15% for certifications and production upgrades. These regulatory pressures can restrict growth, mainly for cost-sensitive companies.

Opportunities

How is the escalating demand for high-frequency and high-speed applications presenting favorable prospects for the growth of the copper clad laminate market?

Applications such as AI, 5G, and high-performance computing require advanced laminates with improved electrical properties. Low-loss and high-frequency CCL materials are becoming increasingly essential. These specialized products offer higher margins than conventional laminates. This shift towards faster data processing and transmission is boosting their adoption. This creates a strong opportunity for technological differentiation in the copper clad laminate industry.

Challenges

Environmental and waste management issues limit the market growth

CCL production comprises processes and chemicals that generate perilous waste. Proper treatment and disposal require advanced infrastructure and compliance measures. Environmental concerns are becoming more noticeable among consumers and regulators. Companies should balance sustainability goals with cost-efficiency. Managing waste and reducing ecological impact remain ongoing operational challenges.

Copper Clad Laminate Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Copper Clad Laminate Market |

| Market Size in 2024 | USD 19.24 Billion |

| Market Forecast in 2034 | USD 29.97 Bllion |

| Growth Rate | CAGR of 5.70% |

| Number of Pages | 229 |

| Key Companies Covered | Kingboard Laminates Holdings Ltd., NAN YA Plastics Corporation, Panasonic Holdings Corporation, ITEQ Corporation, Isola Group, Rogers Corporation, Doosan Corporation, Shengyi Technology Co. Ltd., Taiwan Union Technology Corporation, Grace Electron Corp., Guangdong Chaohua Technology Co. Ltd., Fineline Ltd., Taiwan Elite Material Co. Ltd., Goldenmax International Technology Ltd., Ventec International Group, and others. |

| Segments Covered | By Type, By Material, By End Use Industry, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 - 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Copper Clad Laminate Market: Segmentation

The global copper clad laminate market is segmented based on type, material, end use industry, and region.

Why is the Rigid segment projected to dominate the copper clad laminate market?

Based on type, the global copper clad laminate industry is divided into rigid and flexible. The rigid segment captures a leading market with a 60-80% share. This is backed by its extensive use in standard printed circuit boards in multiple industries. Its strong mechanical properties, cost-effectiveness, and thermal stability make it ideal for mass production in automotive, consumer electronics, and industrial applications. Furthermore, its compatibility with established PCB manufacturing processes promises consistent demand strengthening its leading rank.

Conversely, the flexible segment registers second position in the market with 35% share. Its lightweight structure, ability to support compact and complex circuit designs, and flexibility make it highly suitable for advanced applications like medical devices, foldable electronics, and wearables. Surging demand for miniaturized and high-performance electronic devices continues to fuel their adoption in emerging technology industries.

What factors are driving the Epoxy segment to lead the copper clad laminate market?

Based on material, the global copper clad laminate market is segmented into epoxy, phenolic, polyimide, and others. The epoxy-based segment leads the market with a 55-70% share. This growth is backed by its consistent performance and cost-effectiveness. These laminates are widely used in automotive components, industrial PCBs, and consumer electronics, where electrical and standard thermal properties are required. Their compatibility and mechanical stability with large-scale manufacturing processes make them preferred and in demand for the majority of conventional applications.

However, the polyimide-based segment ranks second in the market with a 20-30% share. They are widely preferred for flexible, high-performance electronics such as wearable devices, aerospace components, and advanced PCB designs. Their chemical stability, superior thermal resistance, and ability to support compact flexible circuits fuel steady adoption in progressing high-tech applications.

What are the key reasons for the leadership of the Consumer Electronics segment in the copper clad laminate market?

Based on end use industry, the global market is segmented into automotive, aerospace & defense, consumer electronics, healthcare, and others. The consumer electronics segment dominates the market with 55% share. This leadership is fueled by the high volume of laptops, smartphones, tablets, and other personal devices that require PCBs. Speedy technological improvements and miniaturization trends continue to sustain strong demand in this industry.

Nevertheless, the automotive segment holds the second-largest share, registering a nearly 20-30% share. The rising adoption of electric vehicles, in-car infotainment, and advanced driver-assistance systems is fueling increased PCB demand. The reliable, durable, and thermally stable CCL materials support steady growth in automotive applications.

Copper Clad Laminate Market: Regional Analysis

What gives Asia Pacific a competitive edge in the global Copper Clad Laminate Market?

Asia Pacific is projected to maintain its dominant position in the global copper clad laminate market, with a 5.8-7% CAGR, driven by high consumer electronics production, rapid EV and automotive growth, and expanding telecommunications infrastructure. APAC leads the worldwide market due to its massive production of consumer electronics. Economies such as South Korea, China, and Japan host major smartphone, home appliance, and laptop manufacturers. This high-volume manufacturing creates continuous demand for CCL materials.

Moreover, the region experiences remarkable growth in the automotive industry, especially in EVs. Advanced automotive electronics, comprising infotainment and ADAS systems, need high-performance laminates. This fuels steady CCL consumption in automotive applications. Furthermore, deployment of high-speed data infrastructure and 5G networks in APAC drives demand for low-loss and high-frequency laminates. Telecom equipment manufacturers heavily rely on advanced CCL materials to ensure network reliability.

Why does North America rank second in the global Copper Clad Laminate Market?

North America maintains its position as the second-largest region, with a 5.5-6% CAGR in the global copper clad laminate industry, driven by advanced electronics and the semiconductor industry, strong aerospace and defense applications, and growth in EV and automotive electronics. North America leads the global market due to its strong semiconductor and electronics industry. High demand for high-performance PCBs in servers, computing, and networking fuels consistent CCL consumption. Superior technology development backs the adoption of premium laminates.

Additionally, the region’s defense and aerospace sector largely relies on CCL for high-reliability electronics. Military communication systems, avionics, and radar need laminates with superior electrical and thermal properties. This sector promises steady demand for specialized CCL materials. Additionally, increasing adoption of advanced automotive electronics and electric vehicles drives CCL usage. Systems such as ADAS, battery management, and in-vehicle infotainment require thermally stable, durable laminates. The trend drives industry growth in the region.

Copper Clad Laminate Market: Competitive Analysis

The leading players in the global copper clad laminate market are:

- Kingboard Laminates Holdings Ltd.

- NAN YA Plastics Corporation

- Panasonic Holdings Corporation

- ITEQ Corporation

- Isola Group

- Rogers Corporation

- Doosan Corporation

- Shengyi Technology Co. Ltd.

- Taiwan Union Technology Corporation

- Grace Electron Corp.

- Guangdong Chaohua Technology Co. Ltd.

- Fineline Ltd.

- Taiwan Elite Material Co. Ltd.

- Goldenmax International Technology Ltd.

- Ventec International Group

What are the key trends in the global Copper Clad Laminate Market?

Growth of flexible and lightweight laminates:

The growing use of wearables, compact electronics, and foldable smartphones is driving demand for ultra-thin, flexible CCL. Flexible laminates enable complex, miniaturized circuit designs without compromising reliability or durability. This trend expands the market for bendable and high-performance materials.

Emphasis on eco-friendly and halogen-free materials:

Environmental regulations and sustainability concerns are driving the adoption of low-emission, halogen-free CCL products. Manufacturers are advancing with greener resins and production processes to comply with global standards. This trend creates opportunities in industries prioritizing environmentally responsible electronics.

The global copper clad laminate market is segmented as follows:

By Type

- Rigid

- Flexible

By Material

- Epoxy

- Phenolic

- Polyimide

- Others

By End Use Industry

- Automotive

- Aerospace & Defense

- Consumer Electronics

- Healthcare

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table Of Content

Methodology

FrequentlyAsked Questions

Copper-clad laminate is a composite material used as the base for printed circuit boards (PCBs), comprising a dielectric substrate, usually a fiberglass-reinforced epoxy resin, bonded to thin copper foil on one or both sides. It provides electrical insulation, mechanical support, and a conductive surface for circuit patterns, while withstanding heat during assembly and soldering.

The global copper clad laminate market is projected to grow due to increasing demand for PCBs in electronics, the expansion of automotive electronics, and adoption in aerospace and defense electronics.

According to study, the global copper clad laminate market size was around USD 19.24 billion in 2024 and is expected to grow to around USD 29.97 billion by 2034.

The CAGR of the copper clad laminate market is expected to be around 5.70% during 2025-2034.

Emerging trends in the Copper Clad Laminate market include flexible, lightweight designs; high-frequency laminates; eco-friendly materials; and innovations for advanced electronics and EVs.

Asia Pacific is expected to lead the global copper clad laminate market during the forecast period.

China is a significant contributor to the global market due to its large-scale PCB production and electronics manufacturing.

The key players profiled in the global copper clad laminate market include Kingboard Laminates Holdings Ltd., NAN YA Plastics Corporation, Panasonic Holdings Corporation, ITEQ Corporation, Isola Group, Rogers Corporation, Doosan Corporation, Shengyi Technology Co., Ltd., Taiwan Union Technology Corporation, Grace Electron Corp., Guangdong Chaohua Technology Co. Ltd., Fineline Ltd., Taiwan Elite Material Co. Ltd., Goldenmax International Technology Ltd., and Ventec International Group.

The market landscape is fragmented, with major global manufacturers and regional players competing on quality, technology, and price.

The report examines key aspects of the copper clad laminate market, including a detailed analysis of current growth factors and restraints, as well as future growth opportunities and challenges that will affect the market.

HappyClients