Central Nervous System (CNS) Lymphoma Treatment Market Size, Forecast 2034

Central Nervous System (CNS) Lymphoma Treatment Market By Treatment Type (Chemotherapy, Radiation Therapy, Targeted Therapy, Immunotherapy, Stem Cell Transplantation), By Drug Class (Alkylating Agents, Antimetabolites, Monoclonal Antibodies, Corticosteroids, Proteasome Inhibitors), By Patient Type (Primary CNS Lymphoma, Secondary CNS Lymphoma, AIDS-Related CNS Lymphoma), By End-User (Hospitals, Cancer Treatment Centers, Specialty Clinics, Ambulatory Surgical Centers), and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 127.65 Billion | USD 235.07 Billion | 7.02% | 2024 |

Central Nervous System (CNS) Lymphoma Treatment Industry Perspective:

What will be the size of the central nervous system lymphoma treatment market during the forecast period?

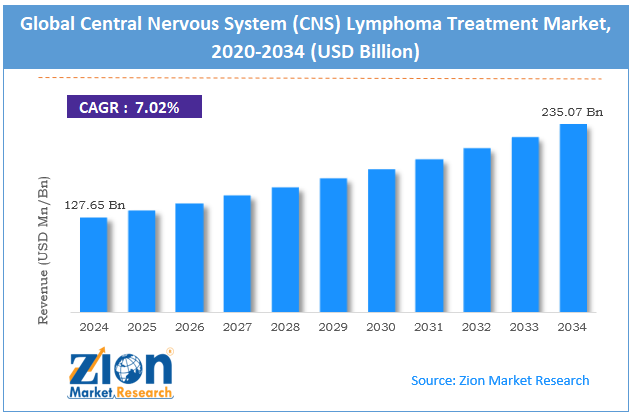

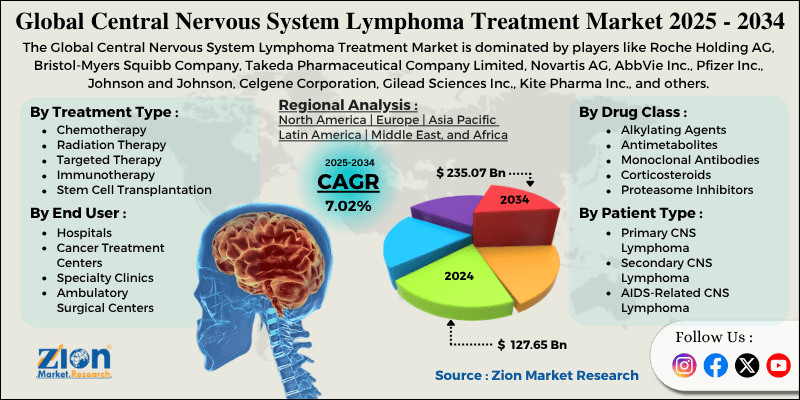

The global central nervous system lymphoma treatment market size was worth approximately USD 127.65 billion in 2024 and is projected to grow to around USD 235.07 billion by 2034, with a compound annual growth rate (CAGR) of roughly 7.02% between 2025 and 2034.

Key Insights

- As per the analysis shared by our research analyst, the global central nervous system lymphoma treatment market is estimated to grow annually at a CAGR of around 7.02% over the forecast period (2025-2034).

- In terms of revenue, the global central nervous system lymphoma treatment market size was valued at approximately USD 127.65 billion in 2024 and is projected to reach USD 235.07 billion by 2034.

- The central nervous system lymphoma treatment market is projected to grow significantly due to rising CNS lymphoma incidence rates, increased awareness of early diagnosis, expanding healthcare expenditure, expanding cancer treatment infrastructure, and the ongoing development of novel therapeutic agents.

- Based on treatment type, the chemotherapy segment is expected to lead the central nervous system lymphoma treatment market, while the immunotherapy segment is anticipated to grow significantly.

- Based on drug class, the alkylating agents segment is expected to lead the central nervous system lymphoma treatment market, while the monoclonal antibodies segment is anticipated to grow rapidly.

- Based on patient type, the primary CNS lymphoma segment is the dominating segment, while the AIDS-related CNS lymphoma segment is projected to witness sizeable revenue over the forecast period.

- Based on end-user, the hospitals segment is expected to lead the market, followed by the cancer treatment centers segment.

- Based on region, North America is projected to dominate the global central nervous system lymphoma treatment market during the estimated period, followed by Europe.

Central Nervous System (CNS) Lymphoma Treatment Market: Overview

Central nervous system lymphoma treatments are specialized medical therapies used to treat malignant lymphocytes that originate in the brain, spinal cord, or surrounding cerebrospinal tissues. This rare and aggressive type of non-Hodgkin lymphoma affects the central nervous system and requires advanced treatment strategies capable of penetrating the blood-brain barrier. Effective management depends on structured, combination-based oncology treatment protocols designed to control tumor progression and improve overall survival outcomes. High-dose chemotherapy remains a primary treatment approach because selected anticancer drugs can reach brain tissue and destroy rapidly dividing lymphoma cells. Radiation therapy uses precisely directed energy beams to target specific brain regions, reducing tumor mass while protecting nearby healthy neural structures. Targeted therapy focuses on molecular markers and specific proteins expressed on lymphoma cells to deliver more accurate and personalized cancer treatment. Immunotherapy enhances immune response mechanisms to identify and eliminate malignant cells within the nervous system. Stem cell transplantation may be used after intensive chemotherapy to restore bone marrow function and support immune recovery. These therapies are applied in primary CNS lymphoma, secondary CNS involvement, and immunocompromised patient cases within specialized oncology centers and tertiary care hospitals.

The increasing incidence of CNS lymphoma cases and advancing treatment technologies are expected to drive significant expansion in the central nervous system lymphoma treatment market throughout the forecast period.

Central Nervous System (CNS) Lymphoma Treatment Market: Technology Roadmap 2025–2034

What is the projected development roadmap of the central nervous system lymphoma treatment market over the forecast period?

The central nervous system lymphoma treatment market is entering a phase of rapid growth, driven by advances in research, improved diagnostic methods, personalized treatment approaches, and a better understanding of disease mechanisms. The market is expected to grow at a CAGR of around 7.02% over the forecast period, driven by rising demand for effective therapies, early detection programs, and combination treatment protocols.

The following roadmap outlines key development phases expected through 2034.

2025–2027: Treatment Optimization and Diagnostic Enhancement Phase

- Improved imaging technologies allow earlier and more accurate diagnosis of central nervous system lymphoma, helping doctors design precise treatment plans and closely monitor therapy response.

- Optimized chemotherapy combinations aim to lower side effects while maintaining strong anticancer activity, improving patient safety and overall quality of life during treatment.

- Advanced drug-delivery methods enhance blood-brain barrier penetration, ensuring higher drug levels reach tumor sites and improving clinical outcomes.

2028–2031: Targeted Therapy and Personalized Medicine Phase

- Molecular profiling technologies identify key genetic mutations and protein markers, enabling personalized CNS lymphoma treatment based on individual tumor biology.

- New targeted therapies block specific cancer growth pathways, reducing damage to healthy brain tissue and increasing treatment precision.

- Biomarker-based treatment selection improves response rates by matching patients to therapies most suited to their tumor characteristics.

2032–2034: Immunotherapy Innovation and Long-Term Management Phase

- Next-generation CAR-T cell therapies designed for CNS lymphoma have shown promising results in clinical studies for difficult-to-treat and relapsed cases.

- Improved checkpoint inhibitor combinations strengthen immune recognition of lymphoma cells and expand options for resistant disease.

- Liquid biopsy technologies support the early detection of minimal residual disease, enabling timely intervention before relapse.

Central Nervous System (CNS) Lymphoma Treatment Market: Dynamics

Growth Drivers

Rising CNS lymphoma cases and early diagnosis drive market growth.

The central nervous system lymphoma treatment market is expanding as the number of diagnosed cases increases among both healthy individuals and patients with weakened immune systems. Primary CNS lymphoma is one of the most common brain tumors seen in people with advanced HIV or AIDS. Older adults face a higher risk because immune function declines with age and increases vulnerability to lymphoid cancers. Modern diagnostic tools, such as MRI scans, cerebrospinal fluid testing, and brain biopsy, allow doctors to identify the disease at earlier stages. Organ transplant patients who take long-term immunosuppressive drugs remain at increased risk of developing CNS lymphoma. Patients receiving immune suppressing therapy for autoimmune disorders also show higher lymphoma incidence and require careful monitoring. Some HIV patients still develop CNS lymphoma despite antiretroviral treatment. Post-transplant lymphoproliferative disorders affecting the brain require intensive therapy. Increased clinical awareness supports earlier diagnosis.

How is the advancement in treatment protocols driving the growth of the central nervous system lymphoma treatment market?

The global central nervous system lymphoma treatment market is growing steadily as researchers develop improved therapy combinations to improve survival and clinical outcomes. Combination chemotherapy remains the main treatment strategy and forms the core of most CNS lymphoma treatment protocols worldwide. High dose methotrexate based regimens cross the blood-brain barrier effectively and deliver strong tumor reduction in many patients. Adding rituximab to chemotherapy improves response rates and extends progression-free survival in eligible patients. Consolidation treatment using high-dose therapy and autologous stem cell transplantation improves long-term disease control for responding cases. Whole-brain radiation therapy remains important for elderly patients or individuals unable to tolerate intensive chemotherapy regimens. Reduced intensity radiation approaches lower cognitive side effects while maintaining effective tumor control. Clinical trials testing new targeted drugs expand alternative treatment options for relapsed or refractory CNS lymphoma. Improved supportive care, including infection prevention and nutritional management, helps patients complete intensive treatment safely.

Restraints

Limited treatment options and severe side effects limit market growth.

A major challenge in the central nervous system lymphoma treatment market is the limited number of therapies able to cross the blood-brain barrier effectively. Many chemotherapy drugs used for systemic lymphoma fail to reach proper concentrations inside brain tissue, reducing available CNS lymphoma treatment options. High-dose methotrexate regimens provide strong tumor control but often cause kidney injury, mouth ulcers, and severe bone marrow suppression. Whole brain radiation therapy can lead to long-term neurotoxicity, including memory loss, confusion, and reduced cognitive performance in older patients. Treatment complications such as infections, bleeding events, and organ damage increase overall clinical risk during intensive cancer therapy programs. Long-term survivors may experience hormonal imbalance, secondary cancers, and lasting cognitive decline affecting quality of life after treatment. Elderly patients frequently struggle to tolerate aggressive chemotherapy protocols, resulting in limited therapeutic choices and weaker survival outcomes. Limited access to specialized neuro-oncology centers creates treatment gaps for rural and underserved populations.

Opportunities

How is novel drug development creating new opportunities for the central nervous system lymphoma treatment market?

The central nervous system lymphoma treatment market is growing as pharmaceutical companies develop innovative therapies specifically designed for brain lymphoma and advanced cancer care. Targeted and immunotherapy generate greater clinical value than traditional chemotherapy in modern CNS lymphoma treatment strategies. BTK inhibitors such as ibrutinib block survival signaling pathways inside lymphoma cells and show measurable activity in brain-based disease. Immunomodulatory drugs, including lenalidomide, support immune activation and produce anti-tumor effects in patients with relapsed CNS lymphoma. Immune checkpoint inhibitors targeting PD-1 and PD-L1 pathways stimulate an immune response against resistant lymphoma cells. CAR-T cell therapy engineered to recognize lymphoma antigens shows promising early clinical trial results in difficult cases. Small-molecule inhibitors derived from tumor genetic profiling support personalized medicine and precision oncology treatment plans. Blood-brain barrier enhancement technologies improve drug delivery into brain tissue and safely increase therapeutic concentrations. Combination therapy approaches integrate novel agents with chemotherapy to improve response duration and reduce relapse risk.

Challenges

How are high treatment costs and limited insurance coverage creating challenges for the central nervous system lymphoma treatment industry?

The central nervous system lymphoma treatment market faces significant cost challenges, driven by high drug prices, complex medical procedures, and long treatment periods. High-dose methotrexate therapy often requires hospital admission for hydration, close monitoring, and supportive rescue medication. Targeted therapy and immunotherapy drugs carry very high monthly prices, creating financial pressure for many patients and healthcare providers. Stem cell transplantation requires advanced medical facilities, specialized staff, and long hospital stays, resulting in very high overall costs. Supportive care, such as antibiotics, blood transfusions, and growth factor injections, adds further expenses during extended cancer treatment programs. Long-term follow-up requires regular brain imaging, laboratory testing, and specialist consultations for several years. Insurance policies vary widely and may restrict access to newer cancer therapies or delay approval for advanced treatments. Out-of-pocket expenses, including travel and copayments, increase financial stress and may affect treatment adherence.

Central Nervous System (CNS) Lymphoma Treatment Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Central Nervous System (CNS) Lymphoma Treatment Market |

| Market Size in 2024 | USD 127.65 Billion |

| Market Forecast in 2034 | USD 235.07 Bllion |

| Growth Rate | CAGR of 7.02% |

| Number of Pages | 226 |

| Key Companies Covered | Roche Holding AG, Bristol-Myers Squibb Company, Takeda Pharmaceutical Company Limited, Novartis AG, AbbVie Inc., Pfizer Inc., Johnson and Johnson, Celgene Corporation, Gilead Sciences Inc., Kite Pharma Inc., and others. |

| Segments Covered | By Treatment Type, By Drug Class, By Patient Type, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Central Nervous System (CNS) Lymphoma Treatment Market: Segmentation

The global central nervous system lymphoma treatment market is segmented based on treatment type, drug class, patient type, end-user, and region.

Why is the chemotherapy segment expected to lead the central nervous system lymphoma treatment market?

Based on treatment type, the global central nervous system lymphoma treatment industry is categorized into chemotherapy, radiation therapy, targeted therapy, immunotherapy, and stem cell transplantation. The chemotherapy segment accounted for approximately 52% of the global market share and is expected to remain dominant during the forecast period due to its proven effectiveness in achieving remission, established treatment protocols, and essential role in first-line therapy for most CNS lymphoma patients. The immunotherapy segment is the second-largest, with nearly 19% market share, driven by rising adoption of monoclonal antibodies, checkpoint inhibitors, and emerging CAR-T cell therapies, which offer new hope for patients with relapsed or refractory disease.

What supports the leadership of the alkylating agents segment in the central nervous system lymphoma treatment market during the forecast period?

Based on drug class, the market is divided into alkylating agents, antimetabolites, monoclonal antibodies, corticosteroids, and proteasome inhibitors. The alkylating agents segment holds around 29% of the total market share and is expected to lead throughout the forecast period, as these drugs form the foundation of many combination chemotherapy regimens used in the treatment of CNS lymphoma. The antimetabolites segment ranks second with approximately 34% market share, supported by widespread use of high-dose methotrexate as the cornerstone drug in primary CNS lymphoma treatment protocols worldwide.

Why does the primary CNS lymphoma segment dominate the central nervous system lymphoma treatment market?

Based on patient type, the global central nervous system lymphoma treatment market is segregated into primary CNS lymphoma, secondary CNS lymphoma, and AIDS-related CNS lymphoma. The primary CNS lymphoma segment leads the market, accounting for nearly 64% of the overall market share, driven by higher incidence among immunocompetent elderly patients and the need for intensive treatment protocols. The secondary CNS lymphoma segment accounts for approximately 23% of the market, driven by increasing survival of systemic lymphoma patients who subsequently develop CNS involvement requiring specialized treatment approaches.

What enables the hospitals segment to lead the global central nervous system lymphoma treatment market?

Based on end-user, the market is segmented into hospitals, cancer treatment centers, specialty clinics, and ambulatory surgical centers. The hospitals segment leads with approximately 58% market share. It is expected to grow steadily, supported by the availability of comprehensive oncology services, intensive care capabilities, and multidisciplinary teams needed for the management of complex CNS lymphoma. The cancer treatment centers segment holds the second position with nearly 27% market share, driven by specialized expertise in neuro-oncology, access to clinical trials, and dedicated resources for treating rare brain tumors, including CNS lymphoma.

Central Nervous System (CNS) Lymphoma Treatment Market: Regional Analysis

What factors enable North America to dominate the global central nervous system lymphoma treatment market during the forecast period?

North America is expected to account for 43.8% of global market revenue and serve as the primary hub for CNS lymphoma treatment innovation, clinical research, and advanced therapeutic protocols. The region leads due to well-established cancer treatment infrastructure, robust research funding, access to novel therapies, and comprehensive insurance coverage supporting expensive treatment regimens. The United States dominates the market, with numerous specialized neuro-oncology centers, extensive clinical trial networks, and early access to emerging therapies through compassionate-use programs. High healthcare spending enables patients to receive intensive treatment protocols, including high-dose chemotherapy, stem cell transplantation, and novel targeted agents. Advanced imaging technologies, including high-resolution MRI and PET scanning, facilitate early diagnosis, accurate treatment planning, and detailed response monitoring throughout therapy.

A strong pharmaceutical industry presence accelerates drug development, with many novel CNS lymphoma therapies undergoing testing at American cancer centers before reaching global availability. Academic medical centers drive treatment innovation through clinical trials testing new drug combinations, novel agents, and optimized supportive care strategies. Comprehensive cancer registries track outcomes, support epidemiological research, and guide the development of evidence-based treatment guidelines for rare cancers, including CNS lymphoma. Insurance coverage for expensive therapies, though variable, generally provides better access than in many other regions of the world, enabling more patients to receive optimal treatment. Multidisciplinary care teams, including neuro-oncologists, neurosurgeons, radiation oncologists, and supportive care specialists, deliver coordinated treatment at major medical centers. Patient advocacy organizations raise awareness, fund research, connect patients with clinical trials, and provide support services, improving overall care quality.

What factors are contributing to Europe's significant growth in the central nervous system lymphoma treatment industry?

Europe is projected to account for 28.4% of the global central nervous system lymphoma treatment market and remain the second-largest region. The region shows steady growth as national health systems expand coverage for novel therapies and cancer treatment centers enhance specialized neuro-oncology services. Universal healthcare systems in most countries ensure basic access to CNS lymphoma treatment regardless of patient financial status or insurance coverage. Collaborative research networks, including European clinical trial groups, advance treatment knowledge through multinational studies testing novel approaches in larger patient populations.

Regulatory frameworks supporting compassionate use programs provide patients lacking other treatment options access to investigational therapies before formal drug approval. Regional differences exist in treatment approaches, with some countries emphasizing intensive chemotherapy while others incorporate radiation therapy more routinely in standard protocols. Academic centers in Germany, France, the United Kingdom, and Switzerland lead European CNS lymphoma research, contributing important clinical trial data and treatment innovations.

Pharmaceutical companies based in Europe develop targeted therapies and immunotherapies, contributing to the global pipeline of novel CNS lymphoma treatments. Patient registries collecting real-world treatment data inform clinical practice, support outcomes research, and guide healthcare policy decisions on optimal treatment approaches. Growing elderly populations increase CNS lymphoma incidence, driving steady demand for age-appropriate treatment protocols balancing effectiveness with tolerability in frailer patients.

Recent Market Developments

- In October 2025, Memorial Sloan Kettering Cancer Center reported strong Phase 2 clinical results showing that ibrutinib combined with the R-MPV chemotherapy regimen achieved exceptionally high response rates and durable tumor control in patients newly diagnosed with primary CNS lymphoma, expanding treatment possibilities for this difficult-to-treat cancer.

Central Nervous System (CNS) Lymphoma Treatment Market: Competitive Analysis

The leading players in the global central nervous system lymphoma treatment market are:

- Roche Holding AG

- Bristol-Myers Squibb Company

- Takeda Pharmaceutical Company Limited

- Novartis AG

- AbbVie Inc.

- Pfizer Inc.

- Johnson and Johnson

- Celgene Corporation

- Gilead Sciences Inc.

- Kite Pharma Inc.

The global central nervous system lymphoma treatment market is segmented as follows:

By Treatment Type

- Chemotherapy

- Radiation Therapy

- Targeted Therapy

- Immunotherapy

- Stem Cell Transplantation

By Drug Class

- Alkylating Agents

- Antimetabolites

- Monoclonal Antibodies

- Corticosteroids

- Proteasome Inhibitors

By Patient Type

- Primary CNS Lymphoma

- Secondary CNS Lymphoma

- AIDS-Related CNS Lymphoma

By End-User

- Hospitals

- Cancer Treatment Centers

- Specialty Clinics

- Ambulatory Surgical Centers

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table Of Content

Methodology

FrequentlyAsked Questions

Central nervous system lymphoma treatments are specialized medical therapies used to treat malignant lymphocytes that originate in the brain, spinal cord, or surrounding cerebrospinal tissues.

The global central nervous system lymphoma treatment market is projected to grow due to increasing CNS lymphoma incidence rates, rising awareness about early diagnosis, growing healthcare expenditure, expanding cancer treatment infrastructure, and continuous development of novel therapeutic agents.

According to a study, the global central nervous system lymphoma treatment market size was worth around USD 127.65 billion in 2024 and is predicted to grow to around USD 235.07 billion by 2034.

The CAGR value of the central nervous system lymphoma treatment market is expected to be around 7.02% during 2025-2034.

North America is expected to lead the global central nervous system lymphoma treatment market during the forecast period.

The major players profiled in the global central nervous system lymphoma treatment market include Roche Holding AG, Bristol-Myers Squibb Company, Takeda Pharmaceutical Company Limited, Novartis AG, AbbVie Inc., Pfizer Inc., Johnson and Johnson, Celgene Corporation, Gilead Sciences Inc., and Kite Pharma Inc.

The report examines key aspects of the central nervous system lymphoma treatment market, including a detailed analysis of current growth drivers and constraints, as well as future growth opportunities and challenges.

In the central nervous system lymphoma treatment market, patients increasingly seek less toxic therapies, oral medications, outpatient treatment options, and personalized approaches based on tumor genetics. Healthcare providers respond by developing targeted therapies, immunotherapies, and optimized supportive care protocols, reducing treatment-related side effects and improving quality of life.

In the central nervous system lymphoma treatment market, key emerging trends include targeted therapy development, CAR-T cell therapy research, biomarker-based treatment selection, and improved blood-brain barrier drug delivery systems.

In the central nervous system lymphoma treatment market, technological advancement improves early diagnosis and personalized treatment through advanced MRI imaging, genomic sequencing, liquid biopsy tools, and digital monitoring systems that enhance therapy precision and patient outcome tracking.

List of Contents

Central Nervous System (CNS) Lymphoma TreatmentIndustry Perspective:Key InsightsOverviewTechnology Roadmap 20252034DynamicsReport ScopeSegmentationRegional AnalysisRecent Market DevelopmentsCompetitive AnalysisThe global central nervous system lymphoma treatment market is segmented as follows:HappyClients