Cast Iron Cookware Market Size, Share, Trends, Growth and Forecast 2032

Cast Iron Cookware Market - By Product Type (Unseasoned, Enamel Coated, and Seasoned), By Style (Bake Ware, Camp Pots, Dutch Ovens, Skillets/Fryers, Griddles, and Woks), By End-Use/Application (Food Services and Household), and By Region - Global Industry Perspective, Comprehensive Analysis, and Forecast, 2024 - 2032

| Market Size in 2023 | Market Forecast in 2032 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 2.85 Billion | USD 6.00 Billion | 8.63% | 2023 |

Cast Iron Cookware Industry Perspective

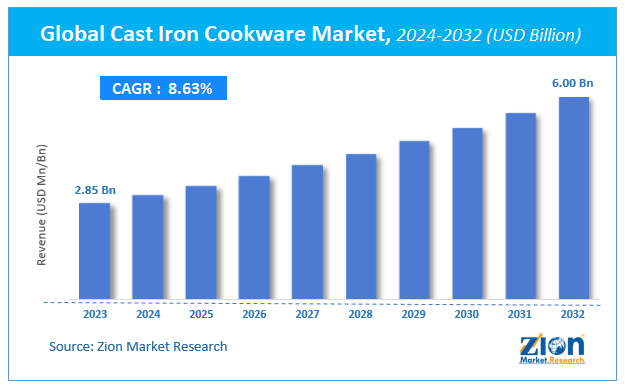

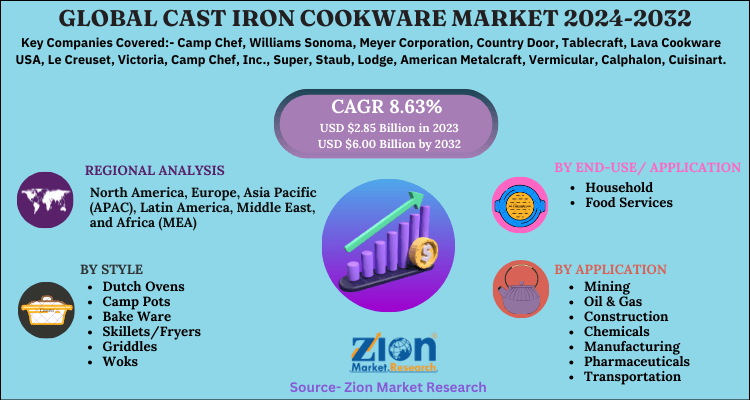

According to Zion Market Research, the global Cast Iron Cookware Market was worth USD 2.85 Billion in 2023. The market is forecast to reach USD 6.00 Billion by 2032, growing at a compound annual growth rate (CAGR) of 8.63% during the forecast period 2024-2032. The report offers a comprehensive analysis of the market, highlighting the factors that will determine growth, potential challenges, and opportunities that could emerge in the Cast Iron Cookware industry over the next decade.

Request Free SampleRequest Free Sample

Request Free SampleRequest Free Sample

Key Insights

- As per the analysis shared by our research analyst, the global Cast Iron Cookware market is projected to grow annually at a CAGR of around 8.63% over the forecast period (2024-2032).

- In terms of revenue, the global Cast Iron Cookware market size was valued at around USD 2.85 Billion in 2023 and is projected to reach 6.00 Billion by 2032.

- The market is driven by the increasing awareness of the health benefits associated with iron fortification in food and the elimination of PFOA/PFAS chemicals found in conventional pans.

- Based on the Product Type, the Unseasoned segment dominated the market with a share of 42.74% because of its lower price point and its appeal to culinary traditionalists who prefer to manage their own seasoning process for a customized cooking surface.

- Based on the Style, the Skillets/Fryers segment dominated the market with a share of 41.6% because of their high versatility in everyday tasks such as searing, sautéing, and baking across various global cuisines.

- Based on the End-Use Application, the Household segment dominated the market with a share of 68.36% as the growing trend of home cooking and social media influencers have popularized "stovetop-to-table" aesthetics for family meals.

- Asia Pacific dominated the market with a share of 40.53% because of its massive manufacturing base in China and India, coupled with a deep-rooted cultural reliance on cast iron for traditional regional cooking techniques.

Cast Iron Cookware Market: Overview

Iron deficiency in children as well as iron deficiency anemia is a key challenge for various countries across the globe with most prominent among them being the low- and middle-income economies. As per NCBI, nearly 1 billion individuals globally are affected due to iron deficiency anemia and 2 billion individuals suffer from iron deficiency without anemia. A large percentage of the population primarily comprise of children & pregnant women as these conditions are majorly observed in children and women attaining the childbearing age or are pregnant. Reportedly, in absence of food fortification, iron deficiency is projected to affect approximately forty percent of preschool children, thirty percent of women attaining reproductive maturity, and thirty eight percent of pregnant women worldwide.

Moreover, iron deficiency anemia results in low academic achievement, reduced cognition, rise in rate of mortality & illness in children, reduction in working ability in adults, and poor pregnancy results. Hence, cast iron cookware is utilized for purpose of cooking in order to reduce iron deficiency anemia in both children & women attaining child-bearing age. Apparently, cast iron cookware is durable and comprises of iron that can trickle into the food, thereby helping those persons, who have iron deficiency or anemia, to absorb iron.

The cast iron cookware market involves the manufacturing and sale of heavy-duty kitchen vessels known for their exceptional heat retention, durability, and natural non-stick properties when properly seasoned. These products are typically produced using sand casting techniques, resulting in a robust material that can withstand high temperatures and transition seamlessly from stovetop to oven. The market serves both domestic home cooks seeking healthy cooking solutions and professional chefs in the food service industry who value the material's ability to provide consistent searing and slow-cooking performance. As modern consumers move away from "disposable" kitchenware, cast iron has seen a significant resurgence due to its lifecycle longevity, often lasting for generations. The scope of this market includes traditional bare cast iron, pre-seasoned varieties, and aesthetically pleasing enamel-coated versions that offer vibrant colors and ease of maintenance.

Cast Iron Cookware Market: Dynamics

Growth Drivers

Health and Wellness Consciousness Among Consumers

The global push toward healthy living is a primary driver as consumers become wary of the potential health risks associated with synthetic non-stick coatings like Teflon. Cast iron offers a naturally safe alternative that does not leach chemicals at high temperatures; instead, it can provide a supplemental source of dietary iron. This "toxin-free" narrative has resonated strongly with millennial and Gen Z demographics, who prioritize clean labels and functional benefits in their household purchases.

Furthermore, the ability of cast iron to cook with less oil while maintaining superior flavor profiles aligns with the global trend of reduced-fat diets. As health experts continue to advocate for traditional, unprocessed cooking methods, the demand for cast iron continues to expand beyond specialty stores into mainstream retail environments, further propelling market growth.

Restraints

Significant Weight and High Maintenance Requirements

The primary factor hindering mass-market adoption is the substantial physical weight of cast iron vessels, which makes them difficult for some elderly or mobility-impaired individuals to handle. Unlike lightweight aluminum or stainless steel, a full-sized cast iron skillet requires significant effort to wash and maneuver. This physical limitation often pushes casual home cooks toward lighter alternatives that offer easier handling.

Additionally, bare cast iron requires a dedicated maintenance routine, including seasoning with oil and avoiding harsh soaps or dishwashers. For busy urban consumers seeking convenience and "quick-cleanup" solutions, the labor-intensive nature of maintaining a cast iron pan can be a deterrent. These maintenance barriers keep the material positioned as a specialized tool for enthusiasts rather than a universal commodity.

Request Free SampleRequest Free Sample

Request Free SampleRequest Free Sample

Opportunities

Advancements in Enameling and Pre-Seasoning Technology

There is a massive opportunity for manufacturers to innovate by creating lighter-weight cast iron alloys and improving the durability of enamel coatings. Enameled cast iron eliminates the need for seasoning and offers a non-reactive surface, making it ideal for acidic foods. By offering products that combine the performance of iron with the convenience of modern finishes, brands can capture the segment of consumers who are currently intimidated by traditional "bare" iron.

The expansion of e-commerce also provides a platform for niche and premium brands to reach global audiences directly. Influencer marketing and "how-to" videos on platforms like TikTok and Instagram help demystify the maintenance process, turning a perceived challenge into a rewarding culinary skill. This educational outreach represents a significant growth lever for the market over the next decade.

Challenges

Volatility in Raw Material Costs and Energy Prices

The production of cast iron is an energy-intensive process that relies heavily on the prices of pig iron, scrap metal, and coke. Fluctuations in the global commodities market can lead to sudden spikes in manufacturing costs, which are often passed on to the consumer. In a market where price sensitivity remains high, especially in developing regions, these cost increases can slow down the replacement cycle and market penetration.

Moreover, the rising cost of energy required to run foundries poses a challenge to maintaining competitive pricing. Manufacturers must balance the need for high-quality, heavy-duty construction with the pressure to offer affordable products. Ensuring a stable supply chain while adhering to increasingly strict environmental regulations regarding industrial emissions adds another layer of complexity to the competitive landscape.

Cast Iron Cookware Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Cast Iron Cookware Market |

| Market Size in 2023 | USD 2.85 Billion |

| Market Forecast in 2032 | USD 6.00 Billion |

| Growth Rate | CAGR of 8.63% |

| Number of Pages | 110 |

| Key Companies Covered | Camp Chef, Williams Sonoma, Meyer Corporation, Country Door, Tablecraft, Lava Cookware USA, Le Creuset, Victoria, Camp Chef, Inc., Super, Staub, Lodge, American Metalcraft, Vermicular, Calphalon, Cuisinart, and Tramontina |

| Segments Covered | By Product Type, By Style, By End-Use And By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2022 |

| Forecast Year | 2024 - 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Cast Iron Cookware Market: Segmentation

The Cast Iron Cookware market is segmented by product type, style, end-use application, and region.

Based on Product Type Segment, the Cast Iron Cookware market is divided into Unseasoned, Enamel Coated, and Seasoned. The Unseasoned segment is the most dominant as it represents the core traditional market, offering the most durable and cost-effective entry point for consumers who value longevity and natural surfaces. The Seasoned (pre-seasoned) segment is the second most dominant and is the fastest-growing category, as it caters to modern convenience by providing a ready-to-use non-stick surface straight out of the box, significantly lowering the barrier to entry for new users.

Based on Style Segment, the Cast Iron Cookware market is divided into Dutch Ovens, Camp Pots, Bake Ware, Skillets/Fryers, Griddles, and Woks. Skillets/Fryers are the most dominant segment because they are the "workhorse" of the kitchen, used for everything from breakfast eggs to dinner steaks. Dutch Ovens are the second most dominant segment, driven by their dual-purpose role as a functional slow-cooker and a stylish piece of oven-to-table serveware, particularly popular in the premium enameled market for stews and sourdough baking.

Based on the End-Use Application Segment, the Cast Iron Cookware market is divided into Household and Food Services. The Household segment is the most dominant, supported by the global surge in home-based culinary hobbies and the aesthetic appeal of cast iron in modern kitchen decor. The Food Services (Commercial) segment is the second most dominant, but it is expanding rapidly as professional chefs increasingly use mini-cast iron skillets and individual-serving Dutch ovens to enhance the presentation and heat retention of dishes in casual dining and steakhouse environments.

Recent Developments

- In 2024, a leading US manufacturer introduced a "Carbon Steel-Iron Hybrid" line designed to offer the heat retention of cast iron at approximately 30% less weight, targeting younger urban dwellers.

- In 2025, a major kitchenware brand launched a series of smart, induction-compatible enameled cast iron pots featuring embedded thermal sensors to provide real-time temperature data via a mobile app.

- During late 2024, several European foundries announced a shift to 100% recycled scrap metal and renewable energy sources for their casting processes to meet the growing demand for sustainable "green" kitchen products.

Regional Insights

Asia Pacific to dominate the global market

The Asia Pacific region leads the global market share, largely fueled by the massive domestic consumption and manufacturing dominance of China and India. In these countries, cast iron is not just a trend but a traditional staple used for high-heat wok cooking and regional flatbreads. The region benefits from lower production costs and a well-established network of foundries that supply both the local mass market and international brands.

North America is the second-largest market and is characterized by a high demand for premium and heritage brands. In the United States, the resurgence of outdoor cooking, camping, and "rustic" lifestyle trends has kept demand high for both skillets and camp pots. The presence of iconic historical brands and a robust e-commerce infrastructure allows for high consumer engagement and frequent product refreshes.

Europe is witnessing steady growth, particularly in the premium enameled segment. Countries like France and Germany are major centers for high-end cast iron production, where the product is marketed as a luxury culinary investment. The European market is increasingly focused on the sustainability aspect of cast iron, promoting it as an eco-friendly alternative to disposable non-stick pans that end up in landfills.

Cast Iron Cookware Market: Competitive Analysis

The global Cast Iron Cookware market is dominated by players like:

- Camp Chef

- Williams Sonoma

- Meyer Corporation,

- Country Door

- Tablecraft

- Lava Cookware USA

- Le Creuset

- Victoria

- Camp Chef, Inc.

- Super

- Staub

- Lodge

- American Metalcraft

- Vermicular

- Calphalon

- Cuisinart

- Tramontina

The global cast iron cookware market is segmented as follows:

By product type

- Unseasoned

- Enamel Coated

- Seasoned

By style

- Dutch Ovens

- Camp Pots

- Bake Ware

- Skillets/Fryers

- Griddles

- Woks

By end-use/ application

- Household

- Food Services

By Region

- North America

- The U.S.

- Canada

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Southeast Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Table Of Content

Methodology

FrequentlyAsked Questions

HappyClients