3D Printed Satellite Market Size, Share, Growth, Opportunities 2034

3D Printed Satellite Market By Component (Antenna, Housing, Shield, Bracket and Propulsion), By Material (Polymers, Composites, Metals and Ceramics), By Satellite Type (Nano and Microsatellites, Medium and Large Satellites and Small Satellites), By Application (Communication, Navigation, Earth Observation, Technology Development, Military Surveillance and Scientific Research) and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 135 Million | USD 1,416 Million | 26.5% | 2024 |

3D Printed Satellite Industry Perspective:

What will be the size of the global 3D Printed Satellite market during the forecast period?

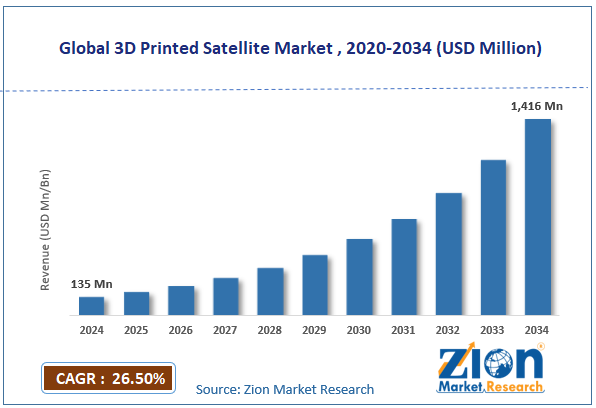

The global 3D printed satellite market size was worth around USD 135 million in 2024 and is predicted to grow to around USD 1416 million by 2034 with a compound annual growth rate (CAGR) of roughly 26.5% between 2025 and 2034.

Request Free SampleRequest Free SampleRequest Free Sample

Request Free SampleRequest Free SampleRequest Free Sample

Key Insights

- As per the analysis shared by our research analyst, the global 3D printed satellite market is estimated to grow annually at a CAGR of around 26.5% over the forecast period (2025-2034).

- In terms of revenue, the global 3D Printed Satellite market size was valued at around USD 135 million in 2024 and is projected to reach USD 1416 million by 2034.

- Increasing defense and surveillance applications are expected to propel the 3D printed satellite market over the projected period.

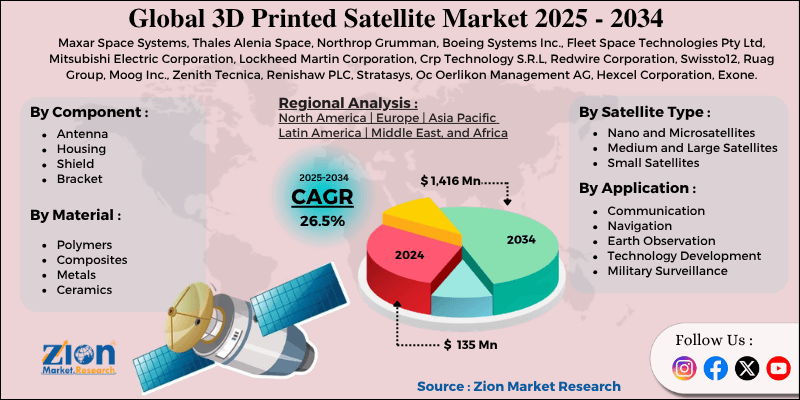

- Based on the component, the antenna segment accounted for the largest revenue share of over 29% in 2024.

- Based on the material, the metals segment holds the largest market share over the projected period.

- Based on the satellite type, the nano and microsatellites segment is expected to hold a prominent market share over the projected period.

- Based on the application, the communication segment holds a prominent revenue share in 2024.

- Based on region, North America captures the largest market share in 2024 of over 37%.

3D Printed Satellite Market: Overview

A 3D-printed satellite is a satellite whose components, or even its entire structure, are manufactured using additive manufacturing, also called 3D printing. Instead of manufacturing the satellite parts through traditional machining and assembly, the parts can be built by depositing materials in neighboring layers, using metals like titanium alloys, aluminum, polymers, and advanced composites. Additive manufacturing is used to manufacture various satellite components, such as waveguides, antennas, thermal management parts, brackets, propulsion systems, structural frameworks, and so on. In today’s markets, the use of 3D-printed satellites is very popular in commercial, defense, scientific, and space applications because of the significant benefits of this technology, including lightweight design, shortened production cycles, reduced manufacturing costs, greater design flexibility, and performance optimization. The increasing demand for small satellites, CubeSats, LEO satellite constellations, and space applications is driving rapid adoption of 3D printing in the space industry.

Impact of the USA-Israel War on Iran on the 3D Printed Satellite Market

The war between the USA and Israel with Iran has fueled demand for defense, surveillance, and communication satellites, driving lucrative growth in the 3D-printed satellite market. Due to increased political conflicts, satellite production is accelerating through additive manufacturing technology, which reduces satellite weight, shortens production time, and lowers production costs. But the war is also hampering the supply chain, increasing energy costs, and creating backlogs in the aerospace materials market, which may temporarily increase satellite production costs.

3D Printed Satellite Market: Dynamics

Growth Drivers

Why does the rising demand for small satellites and CubeSats drive the 3D printed satellite market?

The demand for small satellites and CubeSats has been rising significantly, and the growth of the 3D-printed satellite market has been very high, as different additive manufacturing processes can meet the needs in terms of speed, cost, and weight for small satellite systems. Small satellites can be used in many different applications, including earth observation, communication, navigation, scientific research, and IoT, and the number of launch satellites has been increasing. 3D printing is used to manufacture complex designs, including brackets, engines, antennas, and structural frameworks, which can, in turn, reduce the amount of material needed and production time.

In addition, the contribution of 3D elements to the satellite system can also help reduce launch costs for most parts of the system, which is considered the most important benefit for CubeSat or LEO missions. It can also help develop rapid prototypes and customized satellite architectures for space companies.

Restraints

High initial investment costs hamper the growth of the 3D printed satellite industry

The 3D printed satellite industry is currently constrained by high initial investment costs. Specifically, an aerospace-grade additive manufacturing system, sophisticated software, and dedicated post-processing equipment all require a large initial capital outlay. Once set up, companies need to invest in high-quality metal powders, cleanroom facilities, extensive testing infrastructure, and highly trained personnel to satisfy stringent aerospace quality standards. This creates a significant financial barrier for small and medium-sized manufacturers and startups in the satellite industry wishing to adopt 3D printing technology. Finally, lengthy certification and validation procedures for space-qualified components can drive up development costs and delay recovery of the initial equipment investment.

Opportunities

Why does the growing product launch offer a lucrative opportunity for the 3D printed satellite market?

The growing product launch is expected to offer a lucrative opportunity for the 3D printed satellite market over the projected period. For instance, in December 2025, Sidus Space, an innovative space and defense technology company, announced that it has successfully completed bus-level commissioning of the Company’s LizzieSat-3 (LS-3) space vehicle. This experience is another milestone toward the Company’s objective of providing premium space-based data, integrated sensor solutions, and autonomous on-orbit computing to both government and commercial markets. After reaching orbit earlier this year, LS-3 underwent all postlaunch commissioning events, turned on core systems, and executed CUS-GNC’s advanced SpacePilot software to achieve autonomous navigation and refine orbital co-operations. With bus commissioning complete, the Company is performing payload commissioning while supporting numerous customer payloads and upgrading, enhancing, and tailoring its hardware for the mission.

Challenges

Why does the limited availability of space-qualified materials pose a significant challenge to the 3D printed satellite market?

The lack of availability of space-ready materials is a major concern for the 3D-printed satellite market, as satellites operate in exceedingly harsh environments in space, subject to radiation, vacuum, extreme weather, and the high mechanical loads of launch. Very few 3D printable materials, such as some aluminum and titanium alloys and high-performance polymers, meet the stringent reliability and durability requirements for space life. This hampers materials choices, thus restricting design variation and the scope of components that can be responsibly manufactured through additive manufacturing.

Furthermore, state-of-the-art space-related materials are costly and available only from a handful of vendors, thereby significantly increasing manufacturing costs and supply chain risks. Moreover, long-duration space qualification validation tests for new printable materials impede the pace of innovation and commercialization in the 3D-printed satellite market.

Request Free SampleRequest Free SampleRequest Free Sample

Request Free SampleRequest Free SampleRequest Free Sample

3D Printed Satellite Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | 3D Printed Satellite Market |

| Market Size in 2024 | USD 135 Million |

| Market Forecast in 2034 | USD 1,416 Million |

| Growth Rate | CAGR of 26.5% |

| Number of Pages | 225 |

| Key Companies Covered | Maxar Space Systems, Thales Alenia Space, Northrop Grumman, Boeing Systems Inc., Fleet Space Technologies Pty Ltd, Mitsubishi Electric Corporation, Lockheed Martin Corporation, Crp Technology S.R.L, Redwire Corporation, Swissto12, Ruag Group, Moog Inc., Zenith Tecnica, Renishaw PLC, Stratasys, Oc Oerlikon Management AG, Hexcel Corporation, Exone, Nano Dimension, Sidus Space, Optisys Inc, Optomec Inc, Dawn Aerospace, Trumpf, Anywaves, and others. |

| Segments Covered | By Component, By Material, By Satellite Type, By Application, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

3D Printed Satellite Market: Segmentation

Component Insights

Why does the antenna dominate the 3D printed satellite market?

The antenna segment accounted for the largest revenue share of over 29% in 2024. This industry is growing, as satellites must transmit information effectively. They provide lightweight, durable solutions that can be easily and quickly adapted and deployed through 3D printing. The use of cutting-edge materials and additive manufacturing provides rugged solutions for space, solidifying the segment's strong position in the 3D-printed satellite sector.

Material Insights

How does the metals segment capture the largest market share in the 3D printed satellite market?

The metals segment holds the largest market share over the projected period. This growth is attributed to the need for technologically advanced satellite components that require high strength, long-term stability, and high thermal resistance. The upsurge in deployments of communication, earth observation, and navigation satellites that demand durable space-rated components to withstand radiation, temperature variations, and mechanical vibrations is driving suppliers and consumers to opt for metallic 3D printing solutions, cementing the segment's dominance in the 3D-printed satellite market.

Satellite Type Insights

Does the nano and microsatellites segment capture the largest market share in the 3D printed satellite market?

The nano and microsatellites segment is expected to hold a prominent market share over the projected period. As demand for satellites continues to increase due to advances in 3D printing technology, enabling the manufacture of lightweight yet strong materials. The reduction in launch costs and factors such as long payload lifespans are set to revolutionize the field of satellite missions. The segments' diverse, cost-effective, and rapid manufacturing time make this sector in the 3D-printed satellite industry the dominant one.

Application Insights

Does the communication segment capture the largest market share in the 3D printed satellite market?

The communication segment holds a prominent revenue share in 2024. This growth is mainly driven by the proliferation of 3D-printed satellites with advanced antenna systems, offering lightweight, low-cost, and highly efficient communications solutions for delivering high-speed data transfer services across remote and urban geographies. Apart from this, government projects to improve satellite-based broadband connectivity services and the increasing demand for real-time data communication in defense and aviation applications are other factors contributing to this trend.

Regional Insights

Why does North America lead the 3D printed satellite market?

North America captures the largest market share in 2024 of over 37%. This growth is primarily propelled by high government investments in space innovation and defense programs. The existence of major aerospace & technology companies is propelling research into the rapid development and commercialization of 3D-printed satellite solutions. State-of-the-art materials and high-performance computing infrastructure further support the deployment of AI-powered analytics & autonomous mechanisms, strengthening North America's prominence in the 3D-printed satellite industry.

3D Printed Satellite Market: Competitive Analysis

The global 3D printed satellite market is dominated by players like:

- Maxar Space Systems

- Thales Alenia Space

- Northrop Grumman

- Boeing Systems Inc.

- Fleet Space Technologies Pty Ltd

- Mitsubishi Electric Corporation

- Lockheed Martin Corporation

- Crp Technology S.R.L

- Redwire Corporation

- Swissto12

- Ruag Group

- Moog Inc.

- Zenith Tecnica

- Renishaw PLC

- Stratasys

- Oc Oerlikon Management AG

- Hexcel Corporation

- Exone

- Nano Dimension

- Sidus Space

- Optisys Inc

- Optomec Inc

- Dawn Aerospace

- Trumpf

- Anywaves

The global 3D printed satellite market is segmented as follows:

By Component

- Antenna

- Housing

- Shield

- Bracket

- Propulsion

By Material

- Polymers

- Composites

- Metals

- Ceramics

By Satellite Type

- Nano and Microsatellites

- Medium and Large Satellites

- Small Satellites

By Application

- Communication

- Navigation

- Earth Observation

- Technology Development

- Military Surveillance

- Scientific Research

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table Of Content

Methodology

FrequentlyAsked Questions

A 3D-printed satellite is a satellite whose components, or even its entire structure, are manufactured using additive manufacturing, also called 3D printing. Instead of manufacturing the satellite parts through traditional machining and assembly, the parts can be built by depositing materials in neighboring layers, using metals like titanium alloys, aluminum, polymers, and advanced composites.

Key growth drivers for the 3D printed satellite market include rising demand for small satellites and CubeSats, increasing defense and space exploration investments, reduced manufacturing time and launch costs, and advancements in additive manufacturing materials and technologies.

Major challenges restraining the growth of the 3D printed satellite market include high initial investment costs, limited availability of space-qualified materials, strict aerospace certification requirements, structural reliability concerns, complex post-processing needs, and supply chain disruptions for advanced printing materials and electronic components.

Based on the application, the communication segment is expected to dominate the 3D Printed Satellite market growth during the projected period.

Emerging trends and innovations impacting the 3D printed satellite market include the growing use of metal additive manufacturing for lightweight satellite components, AI-assisted satellite design optimization, development of advanced space-grade materials, adoption of reusable and modular satellite architectures, integration of hybrid manufacturing systems, and increasing focus on rapid production of small satellites and CubeSats for commercial and defense applications.

According to the report, the global 3D printed satellite market size was worth around USD 135 million in 2024 and is predicted to grow to around USD 1416 million by 2034.

The global 3D printed satellite market is expected to grow at a CAGR of 26.5% during the forecast period.

The global 3D printed satellite industry growth is expected to be led by North America over the forecast period.

The global 3D printed satellite market is dominated by players like Maxar Space Systems, Thales Alenia Space, Northrop Grumman, Boeing, Systems, Inc., Fleet Space Technologies Pty Ltd, Mitsubishi Electric Corporation, Lockheed Martin Corporation, Crp, Technology S.R.L, Redwire Corporation, Swissto12, Ruag Group, Moog Inc., Zenith Tecnica, Renishaw PLC, Stratasys, Oc Oerlikon Management AG, Hexcel Corporation, Exone, Nano Dimension, Sidus Space, Optisys Inc, Optomec Inc, Dawn Aerospace, Trumpf and Anywaves among others.

The market report covers the geographical market along with a comprehensive competitive landscape analysis. It also includes cash flow analysis, profit ratio analysis, market basket analysis, market attractiveness analysis, sentiment analysis, PESTLE analysis, trend analysis, SWOT analysis, trade area analysis, demand & supply analysis, Porter’s five forces analysis, and value chain analysis.

HappyClients