Potato Flake Market Size, Share, Trends, Growth and Forecast 2034

Potato Flake Market By Product Type (Whole Potato Flakes, Granulated Potato Flakes, Dehydrated Mashed Potato Flakes, Specialty Flavored Potato Flakes), By Nature (Conventional, Organic), By Application (Food Service and Catering, Retail and Household Use, Food Processing and Manufacturing, Animal Feed), By End-User (Food and Beverage Manufacturers, Hotels and Restaurants, Retail Consumers, Animal Feed Producers), By Distribution Channel (Direct Sales, Supermarkets and Hypermarkets, Convenience Stores, Online Retail), and By Region – Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034-

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 2.38 Billion | USD 3.58 Billion | 4.63% | 2024 |

Potato Flake Industry Perspective:

What will be the size of the potato flake market during the forecast period?

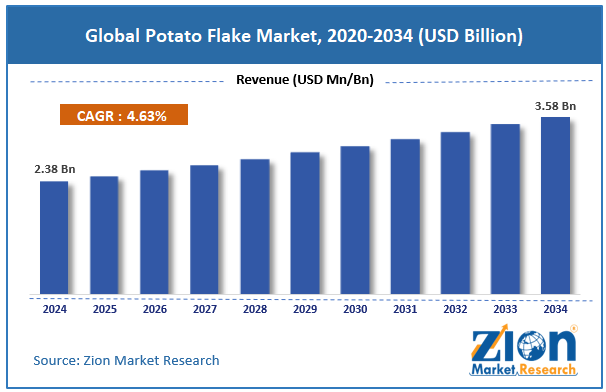

The global potato flake market size was worth approximately USD 2.38 billion in 2024 and is projected to grow to around USD 3.58 billion by 2034, with a compound annual growth rate (CAGR) of roughly 4.63% between 2025 and 2034.

Key Insights

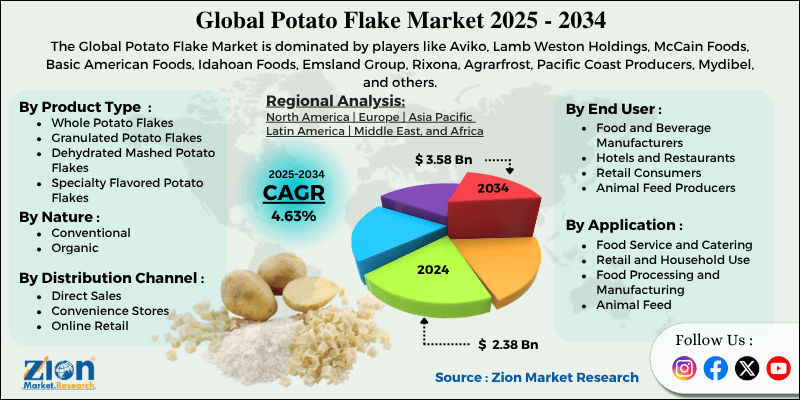

- As per the analysis shared by our research analyst, the global potato flake market is estimated to grow annually at a CAGR of around 4.63% over the forecast period (2025–2034).

- In terms of revenue, the global potato flake market size was valued at approximately USD 2.38 billion in 2024 and is projected to reach USD 3.58 billion by 2034.

- The potato flake market is projected to grow significantly due to rising consumer demand for convenient and quick-preparation food products, expanding use of potato flakes as a functional ingredient in food processing and manufacturing, growing food service industry globally driving bulk ingredient demand, increasing popularity of organic and clean-label food products creating new premium market segments, and expanding middle-class populations in developing countries driving greater consumption of packaged and processed food products.

- Based on product type, the dehydrated mashed potato flakes segment is expected to lead the potato flake market. In contrast, the specialty flavored potato flakes segment is anticipated to grow at a notable rate.

- Based on nature, the conventional segment is expected to lead the potato flake market, while the organic segment is anticipated to grow at the fastest rate.

- Based on application, the food processing and manufacturing segment is expected to lead the potato flake market, while the retail and household use segment is anticipated to grow significantly.

- Based on end-user, the food and beverage manufacturers segment is the largest current end-user group, while the retail consumers segment is anticipated to grow most rapidly.

- Based on distribution channel, the supermarkets and hypermarkets segment is expected to lead the potato flake market, while the online retail segment is anticipated to grow steadily.

- Based on region, Europe is projected to dominate the global potato flake market during the estimated period, followed by North America.

Potato Flake Market: Overview

Potato flakes are dried potato products made by cooking, mashing, and then drying potatoes into thin flakes that can be quickly rehydrated. They are commonly used to make instant mashed potatoes by simply adding hot water or milk. Potato flakes can also be used in many foods such as soups, snacks, ready meals, and bakery products. They keep most of the nutrients found in fresh potatoes, including carbohydrates, fiber, potassium, and vitamin C. At the same time, they are easy to store, have a long shelf life, and are very convenient to use. Potato flakes were first developed to make cooking easier and save time in the kitchen. Instead of peeling and boiling fresh potatoes, people could quickly prepare mashed potatoes in minutes. Over time, they became widely used not only at home but also in the food industry. Food manufacturers use potato flakes because they are easy to handle, cost-effective, and help improve product texture and taste. The potato flake market serves a wide range of users. Home cooks use them for quick meals, while food companies use them in packaged foods. Restaurants and catering services rely on them for fast and consistent preparation. In some regions, they are also used in animal feed due to their nutritional value.

The growing demand for convenient foods, increased use in food processing, the rising popularity of ready-to-eat meals, and higher investment in food technology are driving steady growth in the potato flake market.

Potato Flake Market: Technology Roadmap 2025–2034

What is the projected development roadmap of the potato flake market over the forecast period?

The potato flake market is evolving due to improved drying technologies, rising demand for clean-label products, increased automation, and growing use in functional and fortified foods. The market is expected to grow at a CAGR of around 4.63% over the forecast period, driven by strong demand across food service, food manufacturing, retail, and emerging specialty food segments.

The following roadmap outlines key development phases expected through 2034.

2025–2027: Processing Efficiency and Clean Label Phase

- Manufacturers are expected to upgrade drying equipment to improve efficiency and produce better quality potato flakes with improved texture and flavor.

- The demand for clean-label products is likely to grow, encouraging the use of natural ingredients without artificial additives.

- Organic potato flake production is projected to expand as consumer interest in healthy, sustainable food grows.

2028–2031: Nutrition and Application Expansion Phase

- Manufacturers are expected to develop fortified potato flakes with added nutrients to meet consumers' health-focused needs.

- New application development in gluten-free baking, plant-based food manufacturing, and protein-enriched snack production is likely to create new demand streams for potato flakes beyond their traditional uses.

- Automated production systems are projected to improve consistency, quality, and food safety standards.

2032–2034: Sustainability and Premium Growth Phase

- Potato flake manufacturers are expected to adopt more sustainable agricultural sourcing practices, working with farmers who use reduced water use, precision farming, and integrated pest management to minimize the environmental footprint of raw material production.

- Premium potato flake products with unique varieties and higher nutritional value are likely to grow in demand.

- Digital supply chains are projected to improve tracking, reduce waste, and ensure better inventory management.

Potato Flake Market: Dynamics

Growth Drivers

Is the growing global demand for convenience foods and quick-preparation meal solutions driving growth in the potato flake market?

The potato flake market is growing steadily as demand for convenient, quick-to-prepare food products rises. Modern urban lifestyles involve long working hours, smaller families, and limited time for cooking, increasing the need for quick meal options. Potato flakes meet this need as they can be prepared quickly using hot water or milk while still providing good taste and nutrition. They are suitable for a wide range of consumers, including families, students, working professionals, and the elderly who prefer simple, filling meals. Their long shelf life also makes them easy to store and helps reduce food waste.

In addition to home use, the food service industry is a major driver of demand. Restaurants, catering services, schools, hospitals, and airlines use potato flakes to prepare meals quickly and consistently. They help reduce cooking time and labor costs and ensure uniform quality across different locations. Overall, convenience, long shelf life, and wide usage across households and commercial kitchens are key factors driving growth in the potato flake industry.

What role is the expanding food processing and manufacturing industry playing in driving demand for potato flakes globally?

The potato flake market is also growing due to strong demand from the food processing and manufacturing industry. Potato flakes are widely used as a flexible ingredient in many food products. In the snack industry, they are used to make chips, crisps, and other packaged snacks, as they provide good taste, texture, and consistency. The global snack market is expanding rapidly, especially in the Asia Pacific and Latin America, where changing lifestyles and higher incomes are driving demand. Potato flakes are also used in instant and ready-to-eat meals such as soups and packaged foods that require quick preparation.

As more people choose convenient meal options, demand for reliable, high-quality ingredients like potato flakes continues to rise. In addition, they are used in coatings and breading for meat, fish, and vegetable products, helping improve texture and appearance. This wide range of uses across different food categories ensures steady demand, making the food processing industry a key driver of growth in the potato flake market.

Restraints

Why do raw material uncertainty and strong competition limit growth in the potato flake market?

The potato flake industry faces several challenges, mainly related to the supply and cost of raw materials. Potato flakes depend on fresh potato production, and any change in crop yield directly affects cost and availability. Weather conditions such as drought, heavy rain, or frost can reduce potato output, leading to higher raw material prices and lower profit margins for manufacturers. This instability makes pricing unpredictable and long-term planning difficult for both producers and buyers.

Another key challenge is strong competition from other potato products. Fresh potatoes, frozen items, and other processed forms like potato granules and starch are widely used in the same applications. Many food service providers still prefer fresh or frozen potatoes because of better taste and texture. Potato flakes are often chosen only when convenience is more important than quality. To increase adoption, companies need to improve product quality and raise awareness about the benefits of potato flakes. These factors, together, act as major restraints on the steady growth of the potato flake market.

Opportunities

Growing demand for organic and clean-label foods is creating new opportunities in the potato flake market.

The potato flake market is creating new growth opportunities through the rising demand for organic and clean-label food products. Consumers are becoming more aware of what they eat and prefer simple, natural ingredients free of chemicals and artificial additives. Potato flakes made from organic potatoes and free of preservatives are gaining popularity, especially among health-conscious buyers willing to pay more for better quality. This trend is also influencing food companies, as many brands are changing their recipes to remove artificial ingredients and use natural options.

As a result, demand for clean-label potato flakes is steadily increasing. Another important opportunity comes from nutritional fortification. Manufacturers are developing potato flakes enriched with nutrients like iron, zinc, vitamin D, and fiber to meet specific health needs. These products are useful for children, elderly people, and individuals with nutritional deficiencies. In developing regions, fortified potato flakes can also be used in food programs to improve public health. Overall, growing health awareness, clean-label demand, and nutritional innovation are creating strong opportunities for expansion in the potato flake market.

Challenges

How do consumer perception, sustainability, and price pressure affect the potato flake market?

The potato flake industry faces several challenges related to consumer perception, sustainability, and pricing pressure. Many consumers still believe that dehydrated or instant foods are lower in quality and nutrition compared to fresh products. This makes it harder for companies to promote potato flakes despite their convenience and long shelf life. To overcome this, manufacturers need to improve product quality and clearly communicate nutritional benefits. Sustainability is another growing concern, as potato farming requires water, land, and inputs, while the drying process also uses significant energy. Buyers are increasingly looking for environmentally responsible products, and companies must show efforts to reduce resource use.

In addition, strong price competition in the market puts pressure on profit margins, especially in segments where buyers focus mainly on cost, making it difficult for companies to invest in innovation and quality improvement. Balancing cost, quality, and sustainability remains a key challenge for the potato flake market.

Potato Flake Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Potato Flake Market |

| Market Size in 2024 | USD 2.38 Billion |

| Market Forecast in 2034 | USD 3.58 Bllion |

| Growth Rate | CAGR of 4.63% |

| Number of Pages | 227 |

| Key Companies Covered | Aviko, Lamb Weston Holdings, McCain Foods, Basic American Foods, Idahoan Foods, Emsland Group, Rixona, Agrarfrost, Pacific Coast Producers, Mydibel, and others. |

| Segments Covered | By Product Type, By Nature, By Application, By End-User, By Distribution Channel, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Potato Flake Market: Segmentation

The global potato flake market is segmented by product type, nature, application, end-user, distribution channel, and region.

What makes the dehydrated mashed potato flakes segment the expected leader in the potato flake market?

Based on product type, the global potato flake market is segregated into whole potato flakes, granulated potato flakes, dehydrated mashed potato flakes, and specialty-flavored potato flakes. The dehydrated mashed potato flakes segment holds approximately 46% of the global market share and is expected to remain dominant throughout the forecast period. This segment leads because dehydrated mashed potato flakes are the most widely recognized and versatile form of the product, used across retail, food service, and food manufacturing applications. The specialty flavored potato flakes segment holds around 19% of the market share. It is growing at a notable rate, driven by consumer interest in diverse, convenient meal solutions with added seasoning and distinct flavor profiles.

How does the conventional segment maintain its leading position in the potato flake market?

Based on nature, the potato flake industry is classified into conventional and organic segments. The conventional segment accounts for approximately 82% of global market share, driven by lower production costs, widespread availability, well-established supply chains, and its dominant position in both commodity food manufacturing and mainstream retail. The organic segment holds around 18% share. It is the fastest-growing, supported by rising consumer demand for organic food products, expanding retail shelf space for organic ingredients, and expanding organic certification programs among potato growers in Europe, North America, and select parts of Asia.

Why does the food processing and manufacturing application segment lead the potato flake market?

Based on application, the potato flake market is segmented into food service and catering, retail and household use, food processing and manufacturing, and animal feed. The food processing and manufacturing segment leads the market with approximately 41% of global market share, driven by the extensive use of potato flakes as an ingredient in snack foods, instant meals, soups, coatings, and bakery products across the global food industry. The retail and household use segment holds around 29% share. It is growing significantly as consumer awareness of the convenience benefits of potato flakes increases and retail distribution expands in emerging markets.

What drives the dominance of food and beverage manufacturers in the potato flake market?

Based on end-user, the potato flake industry is divided into food and beverage manufacturers, hotels and restaurants, retail consumers, and animal feed producers. The food and beverage manufacturers segment accounts for approximately 44% of the global market share. It continues to lead the market, driven by the enormous volume of potato flakes used as a raw material across the snack food, ready meal, soup, and convenience food manufacturing industries. The retail consumers segment holds around 27% share. It is growing most rapidly, supported by expanding retail distribution in the Asia Pacific and Latin America and by increasing consumer familiarity with instant potato products in new geographies.

How does the supermarket and hypermarkets distribution channel dominate the potato flake market?

Based on distribution channel, the potato flake market is categorized into direct sales, supermarkets and hypermarkets, convenience stores, and online retail. The supermarkets and hypermarkets segment accounts for approximately 47% of the global market share. It is expected to remain dominant throughout the forecast period, as these channels provide the widest consumer reach, the greatest brand visibility, and the most convenient point of purchase for retail potato flake products in both developed and developing markets. The online retail segment holds around 14% share and is growing steadily, particularly as consumers in urban areas increasingly purchase pantry staples through grocery delivery applications and e-commerce platforms.

Potato Flake Market: Regional Analysis

What makes Europe the leading region in the potato flake market?

The potato flake market is led by Europe, which accounts for around 36.2% of the global market and remains the dominant region due to its strong potato consumption and advanced food industry. Potatoes are a staple food in many European countries, and the region has a long history of potato farming. This ensures a steady supply of high-quality raw materials for potato flake production. Countries such as Germany, the Netherlands, Belgium, Poland, and France are major producers and support large-scale processing activities. Germany is the largest market in the region, driven by strong demand for convenient food products and a well-developed food-processing sector. The Netherlands is another key hub, known for advanced processing technology and a strong global presence. Poland and other Eastern European countries are also growing quickly, supported by rising incomes and expanding food industries. European consumers are familiar with potato flake products and widely accept them as part of their diet. The region also has a strong retail network, including supermarkets and discount stores, ensuring easy access to these products. In addition, restaurants, catering services, and hotel chains use potato flakes in large quantities for quick and consistent food preparation. Overall, Europe’s strong production base, high consumption, and well-developed food infrastructure make it the leading region in the potato flake market.

What drives North America’s position as the second-largest region in the potato flake market?

The potato flake market ranks North America as the second-largest region, accounting for about 28.3% of the global market due to strong demand for convenient food products. The region has a well-developed market for ready-to-eat and easy-to-prepare foods, where potato-based items are widely consumed. The United States is the largest market, supported by a large and diverse food processing industry that uses potato flakes in many products, such as instant meals, soups, and snacks. Consumers in the U.S. have a strong preference for potato-based comfort foods, and potato flakes are widely available in retail stores and commonly used in commercial kitchens. The food service sector is a major driver, with restaurants, hotels, and catering services using potato flakes in large quantities for quick and consistent preparation. Canada also contributes significantly, with similar food habits and a strong food processing sector. Mexico is an emerging market where demand is increasing due to the growth of packaged food products and the expansion of food manufacturing. Overall, the region’s strong consumer demand, advanced food industry, and widespread use of convenience foods make North America the second-largest market for potato flakes.

Recent Market Developments

- In August 2025, McCain Foods announced a major investment of approximately INR 3,800 crore to set up a new potato processing facility in India, including potato flakes production, to expand its global supply capacity and meet rising demand.

- In August 2025, Shivashrit Foods launched its IPO to raise around INR 70 crore, aiming to expand production capacity and strengthen its position in the growing potato flake export market.

Potato Flake Market: Competitive Analysis

The leading players in the global potato flake market are:

- Aviko

- Lamb Weston Holdings

- McCain Foods

- Basic American Foods

- Idahoan Foods

- Emsland Group

- Rixona

- Agrarfrost

- Pacific Coast Producers

- Mydibel

The global potato flake market is segmented as follows:

By Product Type

- Whole Potato Flakes

- Granulated Potato Flakes

- Dehydrated Mashed Potato Flakes

- Specialty Flavored Potato Flakes

By Nature

- Conventional

- Organic

By Application

- Food Service and Catering

- Retail and Household Use

- Food Processing and Manufacturing

- Animal Feed

By End-User

- Food and Beverage Manufacturers

- Hotels and Restaurants

- Retail Consumers

- Animal Feed Producers

By Distribution Channel

- Direct Sales

- Supermarkets and Hypermarkets

- Convenience Stores

- Online Retail

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table Of Content

Methodology

FrequentlyAsked Questions

The potato flake market covers the production, distribution, and sale of dehydrated potato products made by cooking, mashing, and drum-drying fresh potatoes into thin, shelf-stable flakes that can be rehydrated quickly for use as mashed potatoes or incorporated as a functional ingredient in soups, snacks, ready meals, coatings, and other food products across retail, food service, and food manufacturing applications worldwide.

The global potato flake market is projected to grow due to rising demand for convenient foods, increased use in food processing and snacks, expanding food service activity, and growing interest in clean-label products.

According to a study, the global potato flake market size was worth around USD 2.38 billion in 2024 and is predicted to grow to around USD 3.58 billion by 2034.

The CAGR value of the potato flake market is expected to be around 4.63% during 2025–2034.

Europe is expected to lead the global potato flake market during the forecast period, supported by its strong potato farming heritage, world-class food processing industry, and high consumer familiarity with potato-based food products.

The major players in the global potato flake market include Aviko, Lamb Weston Holdings, McCain Foods, Basic American Foods, Idahoan Foods, Emsland Group, Rixona, Agrarfrost, Pacific Coast Producers, and Mydibel.

The report examines key aspects of the potato flake market, including a detailed analysis of current growth drivers and restraints, emerging market opportunities, key challenges facing producers and distributors, competitive landscape analysis, detailed regional market breakdowns, and a forward-looking outlook across all major product types, applications, and geographies.

The potato flake market faces challenges such as raw material price fluctuations, weather-dependent potato supply, competition from fresh and frozen products, and consumer perception that instant foods are lower in quality and nutrition.

The potato flake market is moderately competitive, with a mix of large global players and regional manufacturers. Companies compete on price, quality, and product innovation while focusing on expanding production capacity, improving supply chains, and offering clean-label and specialty products to gain a competitive edge.

The potato flake market is shifting toward convenient, clean-label, and healthy food options, driven by growing demand for organic products, fortified ingredients, and wider use in snacks, ready meals, and foodservice applications.

HappyClients