Global Frozen Vegetables Market Size, Share, Trends and Forecast Analysis 2032

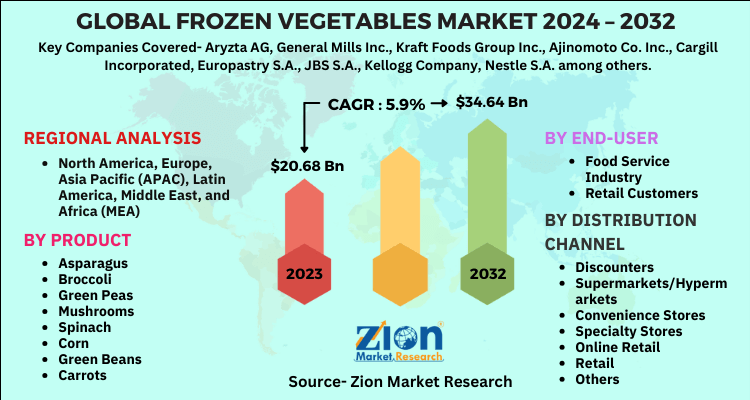

Frozen Vegetables Market by Product (Asparagus, Broccoli, Green Peas, Mushrooms, Spinach, Corn, Green Beans, Carrots, Cauliflower, Bell Peppers, Spring Onion, Tomatoes, Onion, Others), End- User (Food Service Industry, Retail Customers), Distribution Channel (Discounters, Supermarkets/Hypermarkets, Convenience Stores, Specialty Stores, Online Retail, Retail, Others): Global Industry Perspective, Comprehensive Analysis and Forecast, 2024-2032

| Market Size in 2023 | Market Forecast in 2032 | CAGR (in %) | Base Year |

|---|---|---|---|

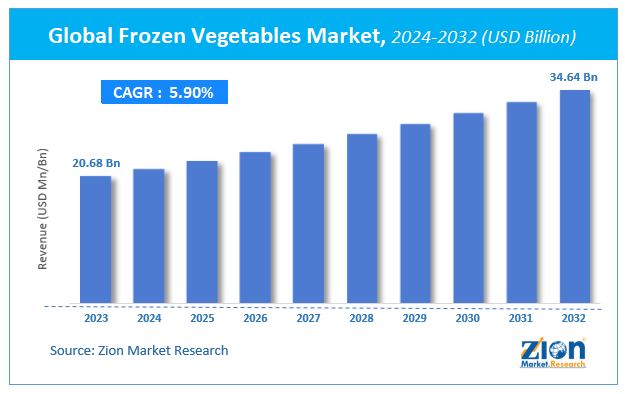

| USD 20.68 Billion | USD 34.64 Billion | 5.9% | 2023 |

Global Frozen Vegetables Market Insights

Zion Market Research has published a report on the global Global Frozen Vegetables Market, estimating its value at USD 20.68 Billion in 2023, with projections indicating that it will reach USD 34.64 Billion by 2032. The market is expected to expand at a compound annual growth rate (CAGR) of 5.9% over the forecast period 2024-2032. The report explores the factors fueling market growth, the hitches that could hamper this expansion, and the opportunities that may arise in the Global Frozen Vegetables Market industry. Additionally, it offers a detailed analysis of how these elements will affect market demand dynamics and market performance throughout the forecast period.

Market Overview

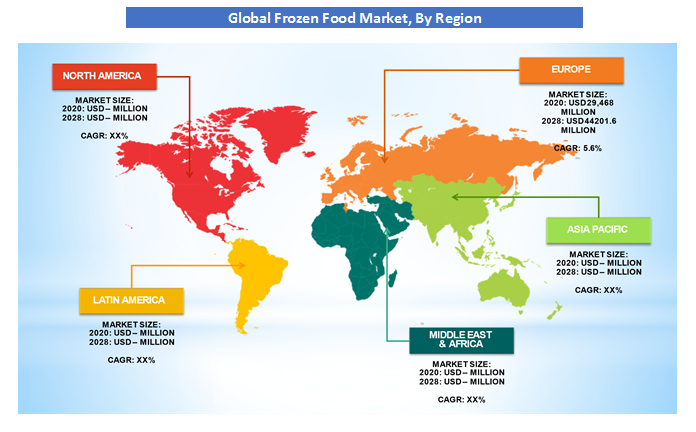

The global frozen vegetable market accounted for USD 29.47 Billion in 2020 and is expected to reach USD 44.20 Billion by 2028, growing at a CAGR of 5.6% from 2021 to 2028.

Frozen vegetables are those vegetables whose temperature is reduced and is maintained below the freezing point for packaging, storage, and transportation purpose. There is a wide variety of frozen vegetable market which is sold in stores, hypermarkets, and supermarkets. Various frozen vegetables are peas, broccoli, spinach, corn, and cauliflower which are mostly sold in Asia. Various popular brands are Green Giant, Birds Eye, and Sunbulah. Frozen vegetables are sold across the year and they have very high life expectancy. Since the freezing process stops bacterial growth, frozen vegetables have an advantage over canned vegetables in that certain products contain little to no added salt.

COVID-19 Impact Analysis

The epidemic of COVID-19 has had a significant impact on customer behavior. Consumers are stockpiling shelf-stable produce, such as dried fruits and vegetables, on the demand side. The tradition of stockpiling has resulted in a sharp increase in the market value of global frozen fruits and vegetables in 2020, which will return to normal after the epidemic situation has stabilized. Restaurants and takeaway services are now only available in a few countries, so consumers prefer to eat at home and prepare their own meals. The shopping habits of consumers all over the world had changed as a result of these changes. Healthy food consumption is becoming more popular among consumers. Because frozen fruits and vegetables have a longer shelf life and are easier to prepare at home, the outbreak has resulted in a surge in demand. In addition, preparing frozen products takes less time and effort than preparing fresh products.

Growth Factors

Increasing demand and easy availability of the frozen market is driving the market. People now don’t have to cook for hours killing all the nutrients and minerals, they simply have to opt for frozen vegetables which retain all the nutrients and minerals. Also, the accretion in retail networks across the globe is also one of the major growth drivers. People are now getting more health conscious and these frozen vegetables help them in acquiring all the necessary nutrients. There is an increased demand for frozen food among the population. With the development and technological advancement in the freezing technologies over time led to the rise in the consumption of frozen vegetables.

Product Segment Analysis Preview

The corn segment had the highest share in the frozen vegetable industry because of the widespread availability of corn around the world and the widespread use of corn and corn-based food items in quick-service restaurants and food outlets. The Broccoli is projected to witness a substantial growth of CAGR 7.4% in the forecast period due to the rise in health-conscious and fitness-driven people across the globe. Mushroom in the given forecast period is expected to witness a CAGR of 1.83%. Increased mushroom consumption in quick-service restaurants and food outlets, on the other hand, may provide ample opportunities in the future. Asparagus, Broccoli, Green Peas, Mushrooms, Spinach, Green Beans, Carrots, Cauliflower, Bell Peppers, Spring Onion, Tomatoes, Onion, and others forms the product segment.

Product Segment Analysis Preview

During the forecast period, Retail Customers held the largest share in the frozen vegetable market. The retail sector has witnessed a major drawback too during the forecast period. Covid has impacted the labor and logistics capacities. The second type of product segment is Food Service Industry.

Distribution Channel Segment Analysis Preview

During the forecast period, the supermarket/hypermarket dominated the distribution channel segment in the frozen vegetable market because these retail formats provide an enhanced shopping experience. Furthermore, these retail formats provide a one-stop solution to a variety of shopping needs, boosting their global popularity. Because of the increasing number of convenience stores, the other segment, which includes convenience stores and mom & pop stores, is expected to grow at a steady rate during the forecast period. Convenience stores and mom-and-pop shops are also typically located near residential areas, requiring less effort on the part of the customer when purchasing goods. This ease of purchase contributes to the popularity of other segments and serves as a driving force for the global frozen vegetable market. Discounters, Convenience Stores, Specialty Stores, Online Retail, Retail, and others forms the product segment.

Regional Analysis Preview

Europe accounted for a share of 40% in 2020. This is due to the fact that people in Europe prefer buying frozen vegetables rather buying fresh ones. This also attributable to the rapid changes in consumption habits and lifestyles. They do not prefer cooking for hours rather opt for Meal Ready to Eat (MREs) which are also part of concentrated frozen food. Additionally, due to the hectic work schedules and improved per capita income also played a major role in the growth of frozen food market in the region.

Asia Pacific is projected to grow at a CAGR of over 7.4% during the forecast period. Frozen vegetables are readily available and provide consumers with a wide range of options because they are available in a variety of brands. Frozen food is commercially available all year, eliminating the problem of seasonal shortages and addressing the issue of food security. Fresh fruits and vegetables present supply chain efficiency challenges due to seasonality and wastage. Freezing also preserves food without adding any unwanted additives. Fresh fruits and vegetables are thrown away due to natural deterioration and poor storage conditions. Frozen fruits and vegetables, on the other hand, can be stored for a longer period of time and have a longer shelf life.

Global Frozen Vegetables Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Global Frozen Vegetables Market |

| Market Size in 2023 | USD 20.68 Billion |

| Market Forecast in 2032 | USD 34.64 Billion |

| Growth Rate | CAGR of 5.9% |

| Number of Pages | 130 |

| Key Companies Covered | Aryzta AG, General Mills Inc., Kraft Foods Group Inc., Ajinomoto Co. Inc., Cargill Incorporated, Europastry S.A., JBS S.A., Kellogg Company, Nestle S.A. among others |

| Segments Covered | By Product, By End-User, By Distribution Channel, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2022 |

| Forecast Year | 2024 - 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Key Market Players & Competitive Landscape

Some of key players in the frozen vegetables market are

- Aryzta AG

- General Mills Inc.

- Kraft Foods Group Inc.

- Ajinomoto Co. Inc.

- Cargill Incorporated

- Europastry S.A.

- JBS S.A.

- Kellogg Company

- Nestle S.A. among others.

To improve their product portfolio, overcome competition, and maintain or improve their share in the global frozen vegetables market, key players in the frozen vegetables market rely on new product launches as a primary strategy. The global frozen vegetable market is highly fragmented, and major players have used a variety of strategies to expand their footprints in this market, including new product launches, expansions, agreements, joint ventures, partnerships, acquisitions, and others.

The global frozen vegetables market is segmented as follows:

By Product

- Asparagus

- Broccoli

- Green Peas

- Mushrooms

- Spinach

- Corn

- Green Beans

- Carrots

- Cauliflower

- Bell Peppers

- Spring Onion

- Tomatoes

- Onion

- Others

By End-User

- Food Service Industry

- Retail Customers

By Distribution Channel

- Discounters

- Supermarkets/Hypermarkets

- Convenience Stores

- Specialty Stores

- Online Retail

- Retail

- Others

By Region

- North America

- The U.S.

- Canada

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Southeast Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Table Of Content

Methodology

FrequentlyAsked Questions

The global frozen vegetables market was valued at USD 29,468 Million in 2020.

The global frozen vegetables market is expected to reach USD 44,201.6 Million by 2028, growing at a CAGR of 5.6% between 2021 to 2028.

Some of the key factors driving the global frozen vegetables market growth are changing lifestyles, retail sector prominent growth, technological advancements and development in freezing technology and easy availability of the frozen vegetables are some major driving factors.

Europe held a substantial share of the frozen vegetables market in 2020.This is due to the rapid changes in consumption habits and lifestyles. Asia Pacific region is projected to grow at a significant rate of 7.4% during the forecast period owing to the rising demand for frozen vegetables in developing economies such as China and India.

Some of key players in frozen vegetables market are Aryzta AG, General Mills Inc., Kraft Foods Group Inc., Ajinomoto Co. Inc., Cargill Incorporated, Europastry S.A., JBS S.A., Kellogg Company, Nestle S.A. among others.

List of Contents

Global Market InsightsMarket Overview COVID-19 Impact Analysis Growth FactorsProduct Segment Analysis PreviewProduct Segment Analysis PreviewDistribution Channel Segment Analysis PreviewRegional Analysis Preview Report ScopeKey Market Players Competitive LandscapeThe global frozen vegetables market is segmented as follows:By ProductBy End-User By Distribution Channel By RegionHappyClients