Foundry Equipment Market Size, Share, Trends, Growth and Forecast 2034

Foundry Equipment Market By Type (Semi-automated Equipment, Manual Equipment and Fully Automated Equipment), By Application (Metal Casting and Metal Heat Treatment), By End User (Automotive, Aerospace, Machinery and Others) and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 17.6 Billion | USD 24.8 Billion | 3.5% | 2024 |

Foundry Equipment Industry Perspective:

What will be the size of the global foundry equipment market during the forecast period?

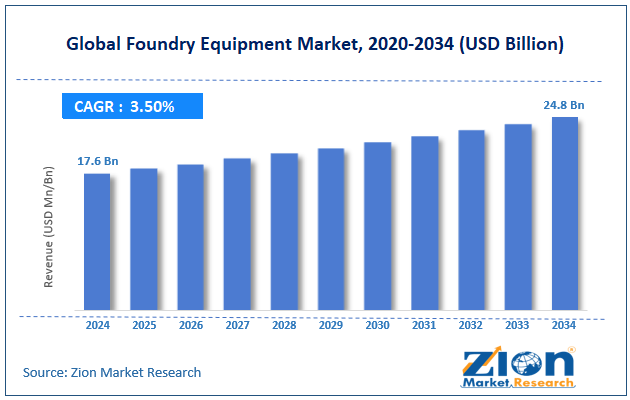

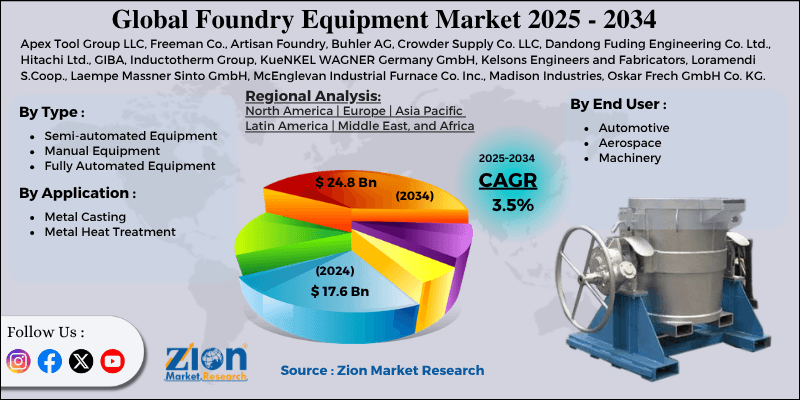

The global foundry equipment market size was worth around USD 17.6 billion in 2024 and is predicted to grow to around USD 24.8 billion by 2034 with a compound annual growth rate Foundry Equipment Market of roughly 3.5% between 2025 and 2034.

Key Insights

- As per the analysis shared by our research analyst, the global foundry equipment market is estimated to grow annually at a CAGR of around 3.5% over the forecast period (2025-2034).

- In terms of revenue, the global foundry equipment market size was valued at around USD 17.6 billion in 2024 and is projected to reach USD 24.8 billion by 2034.

- Infrastructure and construction expansion is expected to propel the foundry equipment market over the projected period.

- Based on the type, the semi-automated equipment segment captures the largest market share in 2024.

- Based on the application, the metal casting segment dominated the market with a highest revenue share in 2024.

- Based on the end user, the automotive segment dominated the market with a highest revenue share in 2024.

- Based on region, the Asia Pacific captures the largest market share in 2024 of 48%.

Foundry Equipment Market: Overview

The foundry equipment market is the industry that deals with the manufacturing, supply, and use of equipment for metal casting operations. Some examples of foundry equipment include melting furnaces, mold-making equipment, core-making equipment, sand preparation equipment, casting equipment, shot blasting equipment, heat treatment equipment, dust collectors, and automatic material handling systems. This equipment is necessary for manufacturing metal castings from materials such as iron, steel, aluminum, and copper alloys. Metal castings produced using the aforementioned equipment are applied in several industries, including the automobile, aerospace, construction, industrial machinery, energy, railway, and heavy engineering industries. The increasing industrialization and demand for lightweight, precision metal parts are the main drivers of the foundry equipment market. Along with this, the growing use of automation and intelligent foundries, as well as increasing manufacturing and infrastructure development activities, are other factors driving the market.

Impact of the USA-Israel War on Iran on the Foundry Equipment Market

The tension between the USA-Israel partnership and Iran has introduced significant unpredictability into the international foundry equipment market, driven by logistical problems, higher energy and raw material prices. Foundries require electricity, coke, scrap metals, pig iron, aluminum, and many different types of industrial chemicals; hence, the rising prices of oil and logistics would further increase the cost of producing and distributing foundry equipment.

Also, the blockage of vital channels, such as the Strait of Hormuz, would delay the transportation of machinery and industrial components, thereby delaying investments in foundry machinery. Unpredictable economic conditions and rising costs of living in the automotive, construction, and engineering industries would deter expenditure on modern foundry equipment. Yet, some foundries in certain locations, particularly in Asia, would be favored by the shift in international logistics.

Foundry Equipment Market: Dynamics

Growth Drivers

Why does the growing automotive industry drive the foundry equipment market?

One important factor driving growth in the market for foundry equipment is the rapidly expanding automotive industry. Automobile manufacturers need strong metal castings for engines, transmissions, cylinder heads, brakes, chassis, and other components of electric cars. Global trends toward increased vehicle production, especially electric cars, mean foundries need to focus on producing lightweight castings. This trend is leading foundries to purchase improved molders, dies, pouring equipment, and efficient furnaces, which help increase production and improve casting precision and mass production. At the same time, ongoing trends in fuel economy, safety, and emissions reduction in automobiles mean that new technological developments in foundry technology are increasingly being adopted by the automotive industry.

As per the European Automobile Manufacturers' Association (ACEA), Global car markets experienced positive developments in 2025, despite regional variations in growth. Global registrations increased 3.5% year-on-year to 77.6 million units, with China showing significant growth of 5.5%, largely attributable to scrappage incentives and new energy vehicle policies. North America experienced modest growth of 1% amid an uncertain and volatile economic situation. Following a sluggish start to the year, overall registrations in Europe increased 1.4%.

Restraints

High initial capital investment hinders the growth of the foundry equipment industry

The high investment required for increased adoption in the foundry equipment market can be considered an important hurdle. This is mainly because modern foundry equipment, such as automated molding machines, induction furnaces, robotic foundry systems, and digital systems for modeling and monitoring, requires a significant investment in capital for refurbishing the foundry system. Large investments are also needed for installation, infrastructure modification, maintenance, training, and energy management systems. Therefore, the foundry equipment market will witness sluggish growth due to the large investments required, particularly in emerging economies, as well as in the cost-sensitive manufacturing segment.

Opportunities

Why does the rising collaboration offer a lucrative opportunity for the foundry equipment market?

The rising collaboration is expected to offer a lucrative opportunity to the foundry equipment market. For instance, in June 2025, Siemens Digital Industries Software announced a significant enhancement in its relationship with Samsung Foundry, including the expansion of certification for many of Samsung's most advanced process technologies across the Siemens EDA product portfolio. The certifications include advanced process technologies such as FinFET and MBCFET from Samsung, spanning 14 nm to 2 nm nodes (SF2/SF2P). This allows customers to use Siemens Calibre® software, Solido™ software, and Aprisa™ software with full confidence to design semiconductor devices for manufacture at Samsung Foundry. In addition to certification, both companies today also disclosed several innovations to help customers overcome design challenges in domains such as power integrity, silicon photonics, analog mixed-signal reliability verification, and more.

Challenges

Why does the shortage of skilled workforce pose a significant challenge to the foundry equipment market?

One of the major issues affecting the development of the foundry equipment market is the shortage of skilled labor. With the introduction of modern techniques in the foundry industry, such as automation, robotic systems, computer controls, and precision casting, the need for a skilled workforce is critical to effectively manage this sophisticated equipment. Skilled laborers with knowledge in metallurgy, automation technology, and computer systems are needed for the operation and maintenance of such complex machines. The shortage of skilled labor could be due to the disinterest in traditional jobs or the aging of the workforce in some regions.

Request Free Sample

Request Free Sample

Foundry Equipment Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Foundry Equipment Market |

| Market Size in 2024 | USD 17.6 Billion |

| Market Forecast in 2034 | USD 24.8 Billion |

| Growth Rate | CAGR of 3.5% |

| Number of Pages | 228 |

| Key Companies Covered | Apex Tool Group LLC, Freeman Co., Artisan Foundry, Buhler AG, Crowder Supply Co. LLC, Dandong Fuding Engineering Co. Ltd., Hitachi Ltd., GIBA, Inductotherm Group, KueNKEL WAGNER Germany GmbH, Kelsons Engineers and Fabricators, Loramendi S.Coop., Laempe Massner Sinto GmbH, McEnglevan Industrial Furnace Co. Inc., Madison Industries, Oskar Frech GmbH Co. KG, Morgan Advanced Materials Plc, MESH Automation Inc., Norican Group, Nabertherm GmbH, and others. |

| Segments Covered | By Type, By Application, By End User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Foundry Equipment Market: Segmentation

Type Insights

Why does the semi-automated equipment dominate the foundry equipment market?

The semi-automated equipment segment captures the largest market share in 2024. This is attributed to the fact that such technologies are cost-effective, flexible, and suitable for small and medium-sized foundries. The trend among many companies is to embrace semi-automated molding machines, sand-handling equipment, pouring machines, and core-making machines as an alternative to full automation, particularly in developing countries where labor costs remain favorable. This technology will enable manufacturers to increase efficiency, improve casting consistency, and enhance safety in the work environment, with reduced investment costs.

Application Insights

How does the metal casting segment capture the largest market share in the foundry equipment market?

The metal casting segment dominated the market with a highest revenue share in 2024. This growth is driven by increased demand for durable, lightweight, and complex metallic castings across sectors such as automotive, aircraft, construction, machinery, rail transportation, and power plants. Increased production of vehicles, machinery, and equipment for infrastructure development has necessitated the use of advanced casting technologies capable of producing large volumes of precision castings. Advanced furnaces for melting, molding machines, die casting, and material-handling technologies are increasingly adopted in foundry operations.

End User Insights

How does the automotive segment capture the largest market share in the foundry equipment market?

The automotive segment dominated the market with a highest revenue share in 2024. Growth is attributed to the rise in vehicle production worldwide, coupled with increased demand for lightweight, efficient metal components. The automotive industry uses numerous cast parts to make engines, transmissions, cylinder heads, brakes, suspension, and electric vehicle battery casings, among other components. This has led to the increased demand for foundry machinery and tools. The rise in the number of electric and hybrid cars is adding to the demand for precision aluminum and magnesium castings, which would enhance vehicle fuel economy and lightness. Foundries have thus invested in advanced foundry technologies, including automation in molding and die casting, induction furnaces, and robotics.

Regional Insights

Why does the Asia Pacific lead the foundry equipment market?

The Asia Pacific captures the largest market share in 2024 of 48%. The region's growth is driven by high levels of industrialization, increased manufacturing, and expansion in the automotive, construction, machinery, and infrastructure industries. Nations like China, India, Japan, and South Korea are manufacturing centers with increased demand for metal castings for automobiles, industrial machinery, railway systems, power-generating machines, and consumer goods. Increased investments in smart factories, industrial automation, and advanced metal-casting processes are driving foundries to adopt modern molding machines, induction furnaces, die-casting machines, and robotic material-handling equipment.

In addition, government initiatives supporting domestic manufacturing, infrastructure development, and electric vehicle manufacturing are driving demand for energy-efficient foundry equipment in the region. Availability of cheap labor, foreign direct investments, and export-oriented manufacturing operations are driving the robust revenue growth in the Asia Pacific foundry equipment market.

Foundry Equipment Market: Competitive Analysis

The global foundry equipment market is dominated by players like:

- Apex Tool Group LLC

- Freeman Co.

- Artisan Foundry

- Buhler AG

- Crowder Supply Co. LLC

- Dandong Fuding Engineering Co. Ltd.

- Hitachi Ltd.

- GIBA

- Inductotherm Group

- KueNKEL WAGNER Germany GmbH

- Kelsons Engineers and Fabricators

- Loramendi S.Coop.

- Laempe Massner Sinto GmbH

- McEnglevan Industrial Furnace Co. Inc.

- Madison Industries

- Oskar Frech GmbH Co. KG

- Morgan Advanced Materials Plc

- MESH Automation Inc.

- Norican Group

- Nabertherm GmbH

The global foundry equipment market is segmented as follows:

By Type

- Semi-automated Equipment

- Manual Equipment

- Fully Automated Equipment

By Application

- Metal Casting

- Metal Heat Treatment

By End User

- Automotive

- Aerospace

- Machinery

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table Of Content

Methodology

FrequentlyAsked Questions

The foundry equipment market is the industry that deals with the manufacturing, supply, and use of equipment for metal casting operations. Some examples of foundry equipment include melting furnaces, mold-making equipment, core-making equipment, sand preparation equipment, casting equipment, shot blasting equipment, heat treatment equipment, dust collectors, and automatic material handling systems.

Key growth drivers for the foundry equipment market include rising automotive and industrial manufacturing activities, increasing demand for lightweight metal castings, rapid industrial automation, infrastructure development, and growing adoption of energy-efficient and smart foundry technologies.

Major challenges restraining the growth of the foundry equipment market include high initial capital investment, rising energy and raw material costs, stringent environmental regulations, shortage of skilled workforce, equipment maintenance complexity, and competition from alternative manufacturing technologies such as 3D printing and CNC machining.

Based on the application, the metal casting segment is expected to dominate the foundry equipment market growth during the projected period.

Emerging trends and innovations impacting the foundry equipment market include the adoption of smart foundries, AI-driven automation, robotics, IoT-enabled monitoring systems, energy-efficient furnaces, 3D sand printing, digital casting simulation, and sustainable low-emission metal casting technologies.

According to the report, the global foundry equipment market size was worth around USD 17.6 billion in 2024 and is predicted to grow to around USD 24.8 billion by 2034.

The global foundry equipment market is expected to grow at a CAGR of 3.5% during the forecast period.

The global foundry equipment industry growth is expected to be led by the Asia Pacific over the forecast period.

The global foundry equipment market is dominated by players like Apex Tool Group LLC, Freeman Co., Artisan Foundry, Buhler AG, Crowder Supply Co. LLC, Dandong Fuding Engineering Co. Ltd., Hitachi Ltd., GIBA, Inductotherm Group, KueNKEL WAGNER Germany GmbH, Kelsons Engineers and Fabricators, Loramendi S.Coop., Laempe Massner Sinto GmbH, McEnglevan Industrial Furnace Co. Inc., Madison Industries, Oskar Frech GmbH Co. KG, Morgan Advanced Materials Plc, MESH Automation Inc., Norican Group and Nabertherm GmbH among others.

The market report covers the geographical market along with a comprehensive competitive landscape analysis. It also includes cash flow analysis, profit ratio analysis, market basket analysis, market attractiveness analysis, sentiment analysis, PESTLE analysis, trend analysis, SWOT analysis, trade area analysis, demand & supply analysis, Porter’s five forces analysis, and value chain analysis.

HappyClients