Fiber Optic Components Market Size, Share, Trends, Growth 2034

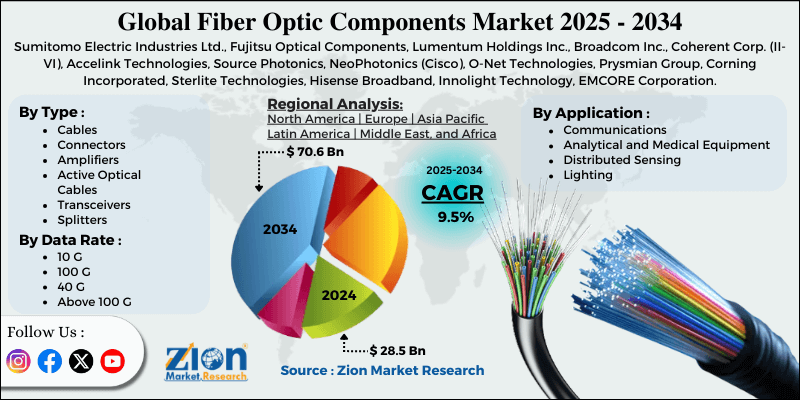

Fiber Optic Components Market By Type (Cables, Connectors, Amplifiers, Active Optical Cables, Transceivers, Splitters, and Others), By Data Rate (10G, 100G, 40G, and Above 100G), By Application (Communications, Analytical and Medical Equipment, Distributed Sensing and Lighting) and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 28.5 Billion | USD 70.6 Billion | 9.5% | 2024 |

Fiber Optic Components Industry Perspective:

What will be the size of the global fiber optic components market during the forecast period?

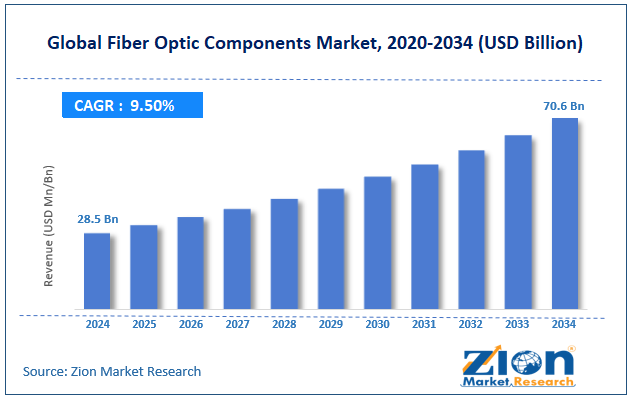

The global fiber optic components market size was worth around USD 28.5 billion in 2024 and is predicted to grow to around USD 70.6 billion by 2034, with a compound annual growth rate (CAGR) of roughly 9.5% between 2025 and 2034.

Key Insights

- As per the analysis shared by our research analyst, the global fiber optic components market is estimated to grow annually at a CAGR of around 9.5% over the forecast period (2025-2034).

- In terms of revenue, the global fiber optic components market size was valued at around USD 28.5 billion in 2024 and is projected to reach USD 70.6 billion by 2034.

- Government initiatives & smart infrastructure is expected to drive the fiber optic components market.

- Based on the type, the cables segment is expected to dominate the market during the forecast period.

- Based on the data rate, the 100 G holds the largest market share over the forecast period.

- Based on the application, in 2024, the communications had the greatest market share, more than 40%.

- Based on region, the Asia Pacific captures the largest market share of 39% in 2024.

Fiber Optic Components Market: Overview

Fiber-optic components are specialized hardware and equipment used in optical communication systems to send, receive, control, and amplify light signals over fiber optic cables. The network infrastructure of contemporary high-speed communication systems depends on these components. They convert electrical signals into optical signals, which they reverse when needed. This technology enables rapid data transmission, supporting high bandwidth while maintaining low latency over long distances. The fundamental components of fiber-optic networks include optical fibers, transceivers, connectors, splitters, amplifiers, couplers, multiplexers, and switches. Each component functions according to its designated role. The telecommunications, data center, cable TV network, enterprise networking, industrial automation, and defense industries make extensive use of their products. Fiber-optic components are particularly crucial for building communication systems worldwide that can grow, be reliable, and handle a lot of traffic. The upcoming decade will see these developments unfold as internet connectivity improves, 5G networks expand, widespread cloud computing grows, and Internet of Things (IoT) deployments increase.

Fiber Optic Components Market: Dynamics

Growth Drivers

How does the rising demand for high-speed internet & data traffic drive the growth of the fiber optic components market?

The fiber optic components market is growing significantly as more people demand fast internet, and more data is transferred worldwide. Digital transformation is affecting more industries, and organizations and consumers are adopting more apps that consume significant bandwidth, such as streaming 4K and 8K video, cloud computing, online gaming, video conferencing, artificial intelligence workloads, and Internet of Things (IoT) ecosystems. These apps need networks that are exceedingly stable, have low latency, and can move data very quickly.

At large scales, standard copper-based networks can't do these tasks well. Transceivers, connectors, amplifiers, and multiplexers are all fiber-optic components that enable high-capacity optical data transmission over long distances with very little transmission loss. Also, the swift development in broadband use, fiber-to-the-home (FTTH), and hyperscale data centers has made the need for stronger optical infrastructure even more urgent. Network operators and organizations are spending heavily on fiber deployments as more people use the internet and more devices connect to it. This is directly driving up demand for fiber-optic components worldwide.

Restraints

High installation and deployment costs hamper the market growth

The fiber optic components industry remains stagnant because installation and setup costs are extremely high. The establishment of fiber-optic networks requires companies to invest substantial funds in optical cables, transceivers, connectors, splitters, amplifiers, and specialized installation tools. The expenses for materials and civil engineering work, which require extensive time and effort to complete trenching and duct installation, right-of-way permitting, and repair work, will become especially expensive in urban areas and locations that are difficult to access.

The implementation costs increase due to the need to employ skilled technicians to perform splicing, testing, and maintenance for fiber networks. The high capital expenses associated with fiber projects will create obstacles that prevent small and medium-sized telecom operators, enterprises, and developing nations from expanding their network reach. The high costs of building fiber networks are the primary challenge preventing companies from expanding their operations despite increasing demand for high-speed internet services.

Opportunities

Why does the increasing acquisition offer a lucrative opportunity for growth of the fiber optic components market?

The fiber-optic components market offers significant business development opportunities, as company acquisitions drive technological progress, business growth, and increased market competitiveness. When big businesses acquire smaller optical component makers, they gain access to advanced technologies such as high-speed transceivers, silicon photonics, coherent optics, and next-generation modules. This process enables companies to develop new products more quickly as they work to meet rising customer demand for high-bandwidth, low-latency connectivity solutions.

For instance, in August 2025, Amphenol Corporation announced its final agreement to acquire CommScope's Connectivity and Cable Solutions division for 10.5 billion dollars in cash. The deal opens up further possibilities for Amphenol's interconnect devices in the rapidly expanding IT datacom industry. The company expands its AI- and data center-related solutions through the acquisition of fiber-optic connectivity devices. The company provides additional products for communications networks through its collection of fiber-optic and interconnect solutions for industrial applications.

Challenges

How does complex, costly maintenance pose a major challenge to the fiber optic components market growth?

The fiber optic components market can't grow because maintenance is hard and expensive. Optical networks require specialized skills, careful handling, and expensive diagnostic tools to keep running continuously. Fiber optic cables are more fragile than typical copper systems. They can bend, break, or be damaged by environmental factors. Damage from construction work, natural disasters, or accidental cuts often requires rapid, expert help, which makes repairs more expensive and takes longer.

To detect signal loss, attenuation, or misalignment in the fiber network, maintenance requires sophisticated technologies, including optical time-domain reflectometers (OTDRs), fusion splicers, and high-precision testing equipment. To keep the signal strong, professional workers must splice and test the fiber, which increases labor costs. In high-speed networks with data rates of 100G, 400G, or higher, even a little dirt on the connectors or misalignment can make the network run much slower. This means the connectors need to be checked and cleaned regularly.

Also, keeping large-scale fiber deployments, such as fiber-to-the-home (FTTH) networks, metro networks, and data center interconnects, running smoothly requires constant monitoring and rapid troubleshooting. These ongoing operational costs (OPEX) can put significant strain on budgets, especially for smaller telecom companies or in less developed countries. Because of this, the complexity and expensive maintenance costs make it hard for more people to use, even though there is a lot of demand for high-speed internet.

Fiber Optic Components Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Fiber Optic Components Market |

| Market Size in 2024 | USD 28.5 Billion |

| Market Forecast in 2034 | USD 70.6 Bllion |

| Growth Rate | CAGR of 9.5% |

| Number of Pages | 221 |

| Key Companies Covered | Sumitomo Electric Industries Ltd., Fujitsu Optical Components, Lumentum Holdings Inc., Broadcom Inc., Coherent Corp. (II-VI), Accelink Technologies, Source Photonics, NeoPhotonics (Cisco), O-Net Technologies, Prysmian Group, Corning Incorporated, Sterlite Technologies, Hisense Broadband, Innolight Technology, EMCORE Corporation, Reflex Photonics, FiberHome Telecommunication, Huawei Technologies, Mwtechnologies LDA, OptiEnz Sensors, and others. |

| Segments Covered | By Type, By Data Rate, By Application, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Fiber Optic Components Market: Segmentation

Type Insights

Why did the cables segment dominate the fiber optic components market during the analysis period?

The cables segment is expected to dominate the market during the forecast period. The segment expansion is owing to the growing number of product launches. For instance, at Connected Britain 2025 in September 2025, Sterlite Technologies Limited (STL) showcased its Unitube Single Jacket Indoor Fiber Optic Cable, which uses 4-core Multi-Core Fiber (MCF) technology. The cable has four cores in the same cladding diameter as ordinary single-mode fiber. This increases the amount of data that can be sent without increasing the space required.

According to CPR EuroClass Cca-s2, d1, and a1, it is fire-resistant, making it ideal for data centers and commercial buildings. The cable offers more secure Quantum Key Distribution, suitable bandwidth for the future, high efficiency, and a high return on investment. STL was one of the first to illustrate real-world MCF installations in underground and duct networks.

Data Rate Insights

Why does 100 G hold the largest share in the fiber optic components industry?

The 100 G holds the largest market share over the forecast period. The rise is due to increased demand for high-bandwidth, low-latency connections in data centers and telecom networks. Network operators are upgrading their infrastructure from 10G and 40G systems to 100G solutions to handle greater data traffic and operate more efficiently. This is happening because of cloud computing, video streaming, AI workloads, and the digitization of the workplace. Hyperscale data centers are rapidly deploying 100G optical transceivers and modules to support high-speed server-to-server and data center interconnect (DCI) applications.

Also, the growth of 4G LTE upgrades and 5G backhaul networks has accelerated the adoption of 100G technology for long-distance and metro transmission. The 100G platform is a great mix of speed, cost, and scalability, which is why many operators are upgrading to higher speeds like 200G and 400G. This, along with strong demand from telecom companies, cloud service providers, and businesses, is driving rapid growth in the 100G fiber-optic components market.

Application Insights

Why does the communications capture a significant share in 2024 in the fiber optic components market?

In 2024, the communications had the highest market share, exceeding 40%. Because there is an ever-growing need for fast, high-capacity connections. Telecommunications companies are spending heavily on fiber infrastructure to support the growth of broadband services, fiber-to-the-home (FTTH) deployments, and the worldwide rollout of 5G networks. All of these things need reliable optical transmission systems. The rise of mobile data traffic, video streaming, cloud-based services, and digital transformation in businesses has made networks that can scale and offer low latency more in demand.

Regional Insights

Why does the Asia Pacific hold the largest market share in the fiber optic components market?

The Asia Pacific captures the largest market share of 39% in 2024. The area is booming because people are quickly adopting digital technology, telecommunications infrastructure is expanding, and the government is making major investments in broadband access. China, India, Japan, and South Korea are swiftly establishing fiber-to-the-home (FTTH) networks and adding to their 5G networks. This needs a lot of fiber backhaul and optical parts that can hold a lot of data. More people in the area, more internet users, and more smartphone users are all driving up data traffic. This is prompting telecom businesses to upgrade their networks from older copper systems to newer fiber-optic technologies.

Asia Pacific is a popular region for building data centers worldwide, driven by the growth of e-commerce, cloud computing, artificial intelligence, and hyperscale infrastructure. Fiber rollout speeds up when the government funds projects that help smart cities, the digital economy, and internet access in rural areas. The regional supply chain is stronger because it has major optical component makers and can produce these components at a lower cost. This will help the fiber-optic parts market in the Asia-Pacific region grow over time.

Fiber Optic Components Market: Competitive Analysis

The global fiber optic components market is dominated by players like:

- Sumitomo Electric Industries Ltd.

- Fujitsu Optical Components

- Lumentum Holdings Inc.

- Broadcom Inc.

- Coherent Corp. (II-VI)

- Accelink Technologies

- Source Photonics

- NeoPhotonics (Cisco)

- O-Net Technologies

- Prysmian Group

- Corning Incorporated

- Sterlite Technologies

- Hisense Broadband

- Innolight Technology

- EMCORE Corporation

- Reflex Photonics

- FiberHome Telecommunication

- Huawei Technologies

- Mwtechnologies LDA

- OptiEnz Sensors

The global fiber optic components market is segmented as follows:

By Type

- Cables

- Connectors

- Amplifiers

- Active Optical Cables

- Transceivers

- Splitters

- Others

By Data Rate

- 10 G

- 100 G

- 40 G

- Above 100 G

By Application

- Communications

- Analytical and Medical Equipment

- Distributed Sensing

- Lighting

By Region

- North America

- The U.S.

- Canada

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Southeast Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Table Of Content

Methodology

FrequentlyAsked Questions

HappyClients