ENT Devices Market Size, Share, Growth Analysis, 2032

ENT Devices Market - By Product (Diagnostic ENT Devices, Surgical ENT Devices, Hearing Aids, Hearing Implants, CO2 Lasers, Image-guided Surgery Systems), By End User (Hospitals, ENT Clinics, Home-use, and Others), And By Region - Global Industry Perspective, Comprehensive Analysis, And Forecast, 2024 - 2032

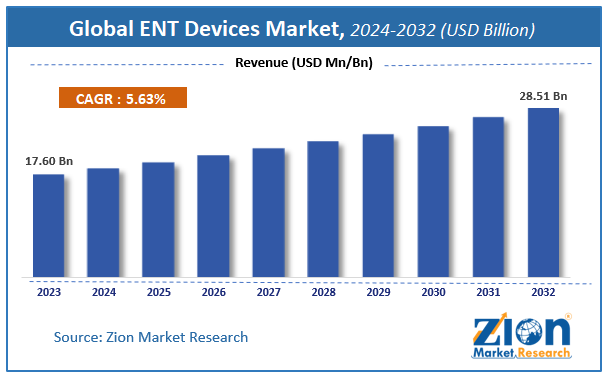

| Market Size in 2023 | Market Forecast in 2032 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 17.60 Billion | USD 28.51 Billion | 5.63% | 2023 |

ENT Devices Market: Industry Perspective

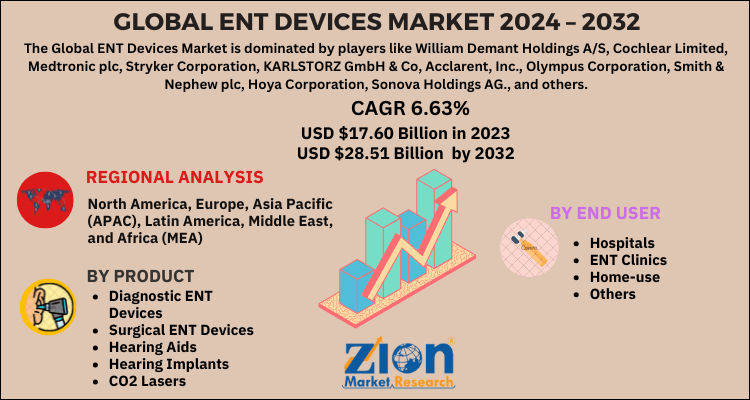

The global ENT devices market size was worth around USD 17.60 billion in 2023 and is predicted to grow to around USD 28.51 billion by 2032 with a compound annual growth rate (CAGR) of roughly 5.63% between 2024 and 2032. The report analyzes the global ENT devices market's drivers, restraints/challenges, and the effect they have on the demands during the projection period. In addition, the report explores emerging opportunities in the retail earplugs industry.

ENT Devices Market Overview

The ENT devices market comprises a wide array of medical instruments and technologies designed for the diagnosis, treatment, and management of disorders affecting the ear, nose, and throat. These devices include diagnostic tools such as endoscopes and hearing screening equipment, surgical instruments like powered handpieces and balloon sinus dilation systems, hearing solutions including aids and implants, and supplies such as nasal splints and packing materials. They are utilized across various healthcare settings to address conditions ranging from hearing loss and sinusitis to more complex issues like sleep apnea and chronic inflammation, facilitating minimally invasive procedures, precise diagnostics, and improved patient outcomes through technological integrations like AI and robotics.

ENT Devices Market: Growth Dynamics

Growth Drivers

The ENT devices market is propelled by the rising prevalence of ear, nose, and throat disorders, particularly among aging populations susceptible to hearing loss, sinusitis, and balance issues, coupled with increasing awareness through educational campaigns that encourage early detection and treatment; technological advancements in minimally invasive techniques, advanced imaging, robotic-assisted surgeries, and digital health solutions like telemedicine further enhance precision, patient engagement, and accessibility; growing investments in healthcare infrastructure, especially in emerging economies, along with the adoption of AI, machine learning, and wireless monitoring devices, drive innovation and expand market reach, while a shift toward patient-centered, personalized medicine supports demand for sophisticated, user-friendly devices.

Restraints

High costs associated with ENT devices and procedures, including substantial research and development expenses, advanced manufacturing, and regulatory compliance, pose significant barriers to adoption, particularly in cost-sensitive regions and among underserved populations where limited healthcare coverage and economic constraints restrict access to cutting-edge treatments like cochlear implants and minimally invasive surgeries, potentially slowing market penetration despite overall demand.

Opportunities

Expansion opportunities in the ENT devices market arise from the growing demand for cosmetic procedures like rhinoplasty and the development of sustainable, biodegradable materials for devices, alongside the integration of AI-driven diagnostics for early detection and telehealth services for remote consultations; emerging markets offer potential through increased healthcare spending, regulatory support for over-the-counter hearing aids, and partnerships that facilitate technology transfer, while innovations in outpatient and home-care solutions cater to shifting preferences for convenient, non-invasive care.

Challenges

The ENT devices market faces challenges from a fragmented competitive landscape with numerous local and global players, requiring continuous investments in partnerships, mergers, and product differentiation to capture share; social stigma around hearing disorders delays treatment-seeking behavior, while stringent regulatory frameworks and high procedural costs in low-income areas hinder broader adoption, compounded by the need to address supply chain vulnerabilities and ensure affordability without compromising quality.

ENT Devices Market: Segmentation

The study provides a decisive view on the ENT Devices Market by segmenting the market based by product, by end user, and regions. All the segments have been analyzed based on present and future trends and the market is estimated from 2024 to 2032.

Based on the by product, the market is segmented into diagnostic ent devices, surgical ent devices, hearing aids, hearing implants, co2 lasers, image-guided surgery systems.

On the basis of the end user, the market is segmented into hospitals, ent clinics, home-use, and others.

The regional, segmentation includes the current and forecast demand for North America, Europe, Asia Pacific, Latin America and the Middle East & Africa with its further bifurcation into major countries.

ENT Devices Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | ENT Devices Market |

| Market Size in 2023 | USD 17.60 Billion |

| Market Forecast in 2032 | USD 28.51 Billion |

| Growth Rate | CAGR of 5.63% |

| Number of Pages | 245 |

| Key Companies Covered | William Demant Holdings A/S, Cochlear Limited, Medtronic plc, Stryker Corporation, KARLSTORZ GmbH & Co, Acclarent, Inc., Olympus Corporation, Smith & Nephew plc, Hoya Corporation, Sonova Holdings AG., and others. |

| Segments Covered | By Product, By End User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, The Middle East and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2022 |

| Forecast Year | 2024 - 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

What is the Regional Analysis of the ENT Devices Market?

North America stands as the dominant region in the ENT devices market, characterized by advanced healthcare infrastructure, high prevalence of ENT disorders like hearing loss among its aging population, and strong adoption of minimally invasive technologies and AI-integrated devices; the United States leads as the dominating country, fueled by substantial R&D investments, frequent product launches, favorable reimbursement policies, and a robust regulatory environment from bodies like the FDA, which collectively drive innovation and market accessibility, positioning the region for sustained leadership through collaborations and technological advancements.

Europe represents a significant market for ENT devices, supported by high healthcare standards, rising awareness of ENT health, and increasing demand for minimally invasive surgeries and digital solutions like telemedicine; Germany emerges as the dominating country, driven by its strong medical technology sector, emphasis on R&D partnerships between universities and manufacturers, and policies promoting early diagnosis and smart devices, which enhance market growth amid an aging demographic and prevalent conditions such as sinusitis.

Asia Pacific is the fastest-growing region in the ENT devices market, propelled by expanding healthcare infrastructure, a large geriatric population, and rising incidences of ENT disorders due to urbanization and pollution; China dominates as the leading country, benefiting from government initiatives in healthcare spending, regulatory support for new technologies, and a massive patient base that demands affordable hearing aids and surgical tools, accelerating adoption through local manufacturing and awareness campaigns.

Latin America exhibits steady growth in the ENT devices market, driven by investments in diagnostic and surgical infrastructure, increasing awareness of hearing and sinus disorders, and an aging population; Brazil leads as the dominating country, supported by regulatory modernizations from ANVISA, government funding for advanced equipment, and a high burden of ENT conditions like hearing loss, fostering demand for minimally invasive procedures and innovative devices.

The Middle East and Africa region is emerging in the ENT devices market, with growth attributed to strengthening local manufacturing, rising elderly populations, and government initiatives for AI, telemedicine, and hearing care programs; Saudi Arabia dominates as the key country, aided by Vision 2030 investments in health development, public-private partnerships, and digital awareness campaigns that promote advanced ENT solutions and infrastructure improvements.

What are the Recent Developments in the ENT Devices Market?

- In March 2024, Cochlear Limited acquired the Oticon Medical cochlear implant division from Demant A/S, strengthening its portfolio in implantable hearing solutions and expanding its global reach to better serve patients with severe hearing loss through enhanced innovation and distribution channels.

- In April 2024, PENTAX Medical launched the Digital Capture Module 9380 for ENT and speech-language pathology applications, improving recording and visualization capabilities to support precise diagnostics and treatments in clinical settings.

- In February 2024, Sonova opened a new operations facility in Mexico dedicated to producing cochlear implants and hearing instruments, aiming to increase accessibility and affordability in emerging markets while bolstering supply chain efficiency.

- In Q2 2024, Medtronic received FDA approval for its Hugo robotic-assisted surgery system for ENT procedures, enabling greater surgical precision and minimally invasive options that enhance patient outcomes and surgeon capabilities.

- In Q3 2024, Stryker acquired OtoNexus Medical Technologies to expand its diagnostic tools for ENT conditions, integrating advanced ultrasound technology to improve middle ear infection detection and treatment planning.

What are the Market Trends in the ENT Devices Market?

- Integration of AI and machine learning for improved diagnostic accuracy, surgical precision, and predictive analytics in ENT care.

- Shift toward minimally invasive procedures, reducing recovery times and complications with advanced tools like robotic systems and endoscopes.

- Rising adoption of digital health solutions, including telemedicine, mobile apps, and remote monitoring for enhanced patient engagement.

- Increasing focus on sustainable practices, such as using biodegradable materials in device manufacturing.

- Growth in cosmetic ENT treatments and over-the-counter hearing aids, driven by consumer preferences and regulatory approvals.

- Miniaturization of components in hearing aids and implants for better comfort and functionality.

- Expansion of outpatient and ambulatory care settings for cost-effective, convenient procedures.

ENT Devices Market: Competitive Analysis

The global ENT devices market is dominated by players like:

- William Demant Holdings A/S

- Cochlear Limited

- Medtronic plc

- Stryker Corporation

- KARLSTORZ GmbH & Co

- AcclarENT, Inc.

- Olympus Corporation

- Smith & Nephew plc

- Hoya Corporation

- Sonova Holdings AG.

The global ENT devices market is segmented as follows:

By Product

- Diagnostic ENT Devices

- Endoscopes

- Rigid Endoscopes

- Otoscopes

- Sinuscopes

- Flexible Endoscopes

- Laryngoscopes

- Pharyngoscopes

- Nasopharyngoscopes

- Rhinoscopes

- Hearing Screening Devices

- Rigid Endoscopes

- Endoscopes

- Surgical ENT Devices

- Powered Surgical Instruments

- Radiofrequency Devices

- Handheld Instruments

- Rhinology Instruments

- Otology Instruments

- Laryngeal Instruments

- Head and Neck Surgical Instruments

- Other Handheld Instruments

- Balloon sinus dilation devices

- ENT Supplies

- Packing Material

- Nasal Splints & Stents

- Ear Tubes

- Hearing Aids

- Hearing Implants

- CO2 Lasers

- Image-guided Surgery Systems

By End User

- Hospitals

- ENT Clinics

- Home-use

- Others

By Region

- North America

- The U.S.

- Canada

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Southeast Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Table Of Content

Methodology

FrequentlyAsked Questions

ENT devices are specialized medical instrumENTs used in ear, nose, and throat (ENT) examinations and procedures. These instrumENTs allow doctors to diagnose and treat a variety of conditions in these areas.

According to a study, the global ENT devices market size was worth around USD 17.60 billion in 2023 and is expected to reach USD 28.51 billion by 2032.

The global ENT devices market is expected to grow at a CAGR of 5.63% during the forecast period.

North America is expected to dominate the ENT devices market over the forecast period.

Leading players in the global ENT devices market include William Demant Holdings A/S, Cochlear Limited, Medtronic plc, Stryker Corporation, KARLSTORZ GmbH & Co, AcclarENT, Inc., Olympus Corporation, Smith & Nephew plc, Hoya Corporation, and Sonova Holdings AG., among others.

The ENT devices market report covers the geographical market along with a comprehensive competitive landscape analysis. It also includes cash flow analysis, profit ratio analysis, market basket analysis, market attractiveness analysis, sENTimENT analysis, PESTLE analysis, trend analysis, SWOT analysis, trade area analysis, demand & supply analysis, Porter’s five forces analysis, and value chain analysis.

HappyClients