Dermatology Diagnostic Devices Market Size, Share, Value and Forecast 2034

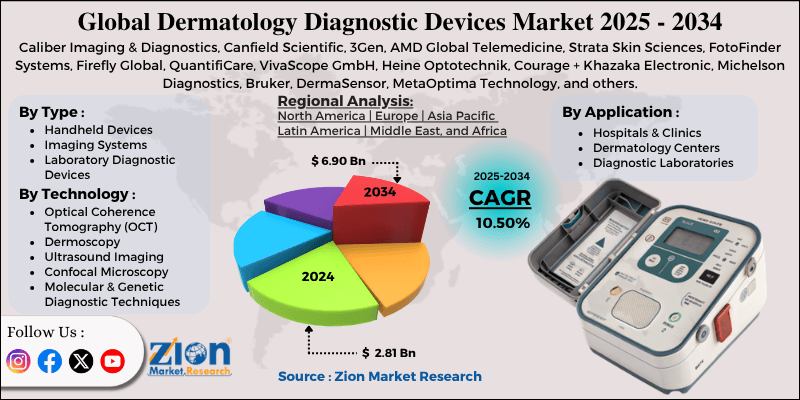

Dermatology Diagnostic Devices Market By Type (Handheld Devices, Imaging Systems, and Laboratory Diagnostic Devices), By Technology (Optical Coherence Tomography (OCT), Dermoscopy, Ultrasound Imaging, Confocal Microscopy, and Molecular & Genetic Diagnostic Techniques), By Application (Hospitals & Clinics, Dermatology Centers, and Diagnostic Laboratories), and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 2.81 Billion | USD 6.90 Billion | 10.50% | 2024 |

Dermatology Diagnostic Devices Industry Perspective:

What will be the expected size of the dermatology diagnostic devices market in the coming years?

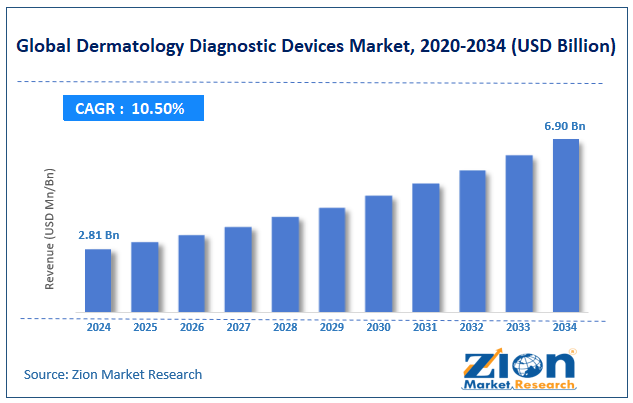

The global dermatology diagnostic devices market was valued at approximately USD 2.81 billion in 2024 and is projected to reach nearly USD 6.90 billion by 2034, expanding at a CAGR of around 10.50% between 2025 and 2034.

Key Insights:

- As per the analysis shared by our research analyst, the global dermatology diagnostic devices market is estimated to grow annually at a CAGR of around 10.50% over the forecast period (2025–2034).

- In terms of revenue, the global dermatology diagnostic devices market size was valued at around USD 2.81 billion in 2024 and is projected to reach USD 6.90 billion by 2034.

- The dermatology diagnostic devices market is projected to grow steadily due to increasing skin cancer screening initiatives and technological advancements in diagnostic imaging.

- Based on the type, the imaging systems segment is growing at a high rate and will continue to dominate the global market, as per industry projections

- Based on the technology, the optical coherence tomography (OCT) segment is anticipated to command the largest market share

- Based on the application, the hospitals & clinics segment is expected to lead the market growth trends

- Based on region, North America is projected to dominate the global market during the forecast period

Dermatology Diagnostic Devices Market: Overview

Dermatology diagnostic devices are advanced medical tools used to detect, monitor, and diagnose skin-related conditions with improved accuracy. These devices include dermatoscopes, digital imaging systems, reflectance confocal microscopes, and laboratory-based diagnostic platforms. Key structural components of the dermatology diagnostic ecosystem include handheld optical examination devices, high-resolution imaging systems, Artificial Intelligence (AI)-integrated lesion analysis software, biopsy and histopathology laboratory equipment, teledermatology platforms, and hospital diagnostic infrastructure. These components collectively support early detection, diagnostic precision, and workflow optimization. The burden of melanoma, basal cell carcinoma, psoriasis, eczema, acne, and fungal infections continues to rise globally. Early detection plays a critical role in improving survival rates, particularly in skin cancer cases. Modern dermatology diagnostics increasingly emphasize non-invasive imaging, real-time lesion mapping, and AI-assisted decision support systems.

During the forecast period, the dermatology diagnostic devices market is expected to grow due to rising prevalence of skin diseases and increasing adoption of AI-driven imaging systems. However, high equipment costs and reimbursement limitations may influence adoption rates in cost-sensitive healthcare settings.

Dermatology Diagnostic Devices Market: Dynamics

Growth Drivers

How is the rising prevalence of skin disorders driving the dermatology diagnostic devices market?

The global dermatology diagnostic devices market is expected to grow due to the rising incidence of skin cancer and chronic dermatological disorders, driven by ageing populations, increased UV exposure, environmental pollution, and lifestyle changes. Early-stage melanoma detection has become a healthcare priority, leading to expanded screening programs and hospital investments in advanced imaging systems. Public awareness campaigns and preventive healthcare initiatives are further increasing patient visits to dermatology clinics worldwide.

Technological advancements and AI integration to support market growth during the forecast period

Artificial intelligence and machine learning technologies are transforming dermatology diagnostics. AI-enabled imaging systems can analyze lesion patterns, color distribution, and border irregularities to assist clinicians in early and accurate diagnosis. Teledermatology platforms integrated with cloud-based imaging systems are expanding access to specialists in rural and underserved regions. These digital innovations are improving workflow efficiency and diagnostic confidence.

Restraints

How will high equipment costs and reimbursement limitations affect the dermatology diagnostic devices market expansion?

Advanced imaging systems, such as confocal microscopes and AI-integrated platforms, require substantial capital investment, which may limit the global dermatology diagnostic devices market revenue. Inconsistent reimbursement policies and limited insurance coverage for advanced dermatology imaging procedures may further restrict the widespread implementation, particularly in developing economies.

Opportunities

Growing demand for portable and point-of-care dermatology devices is reported to create new growth avenues.

The global dermatology diagnostic devices industry is expected to benefit from increasing adoption of compact dermatoscopes and smartphone-connected imaging systems. These tools support faster screening and are highly suitable for outreach programs and telehealth environments. Strategic collaborations between device manufacturers and telemedicine providers are anticipated to unlock additional revenue opportunities in emerging markets.

What are the expansion possibilities for dermatology diagnostic devices market players in emerging economies?

Emerging countries such as the Asia-Pacific, Latin America, and Africa are witnessing increased demand for quality healthcare. Rising regional population, growing prevalence of skin conditions, and favorable government policies supporting healthcare expansion are some of the leading growth propellers for medical and diagnostic devices in these countries. For instance, in February 2025, the African Centers for Disease Control and Prevention (CDC) called on member states to allocate 15% of their national budgets to health. Africa bears more than 25% of the global disease burden but has also 3% of the global health workforce.

Challenges

Competition from low-cost diagnostic alternatives challenges market growth

The global dermatology diagnostic devices market is expected to face challenges due to the availability of low-cost alternatives. Traditional visual examination tools and standard microscopy systems remain widely used in cost-sensitive healthcare settings due to affordability. Although they lack advanced imaging capabilities, they continue to serve as practical diagnostic options. Consumer-grade skin analysis applications may also influence early-stage screening behavior, potentially delaying professional clinical consultations.

How will concerns over counterfeit devices impact the dermatology diagnostic devices industry revenue?

Over the years, cases concerning counterfeit diagnostic tools have increased worldwide. According to the World Health Organization (WHO), around 1 in 10 medical devices in low- and middle-income countries are falsified or substandard. These counterfeit medical equipment pose a serious risk to the patient’s health and also lead to severe economic losses to the country. It is a prominent challenge for market players, requiring strict action against counterfeit medical device sellers and distributors.

Dermatology Diagnostic Devices Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Dermatology Diagnostic Devices Market |

| Market Size in 2024 | USD 2.81 Billion |

| Market Forecast in 2034 | USD 6.90 Bllion |

| Growth Rate | CAGR of 10.50 |

| Number of Pages | 226 |

| Key Companies Covered | Caliber Imaging & Diagnostics, Canfield Scientific, 3Gen, AMD Global Telemedicine, Strata Skin Sciences, FotoFinder Systems, Firefly Global, QuantifiCare, VivaScope GmbH, Heine Optotechnik, Courage + Khazaka Electronic, Michelson Diagnostics, Bruker, DermaSensor, MetaOptima Technology, and others. |

| Segments Covered | By Type, By Technology, By Application, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Dermatology Diagnostic Devices Market: Segmentation

The global dermatology diagnostic devices market is segmented based on type, technology, application, and region.

Why do imaging systems lead the dermatology diagnostic devices market?

Based on type, the global market segments are handheld devices, imaging systems, and laboratory diagnostic devices. In 2024, imaging systems accounted for nearly 46% of total revenue due to high diagnostic accuracy and growing AI integration. The segment is expected to continue growing at a strong pace during the forecast period, with a CAGR of 8.8%, driven by rising demand for accurate diagnosis of complex medical conditions.

What is the projected CAGR for OCT in the dermatology diagnostic devices market during the projection period?

Based on technology, the global dermatology diagnostic devices industry is fragmented into optical coherence tomography (OCT), dermoscopy, ultrasound imaging, confocal microscopy, and molecular & genetic diagnostic techniques. In 2024, the optical coherence tomography (OCT) segment accounted for around 36% of global revenue and will continue to lead the market with a CAGR of 10.01% during the forecast period. The segmental revenue is driven by OCT’s capability to deliver accurate cross-sectional images of skin layers, allowing accurate diagnosis.

Which application segment dominates the dermatology diagnostic devices market?

Based on application, the global market is divided into hospitals & clinics, dermatology centers, and diagnostic laboratories. In 2024, hospitals & clinics accounted for approximately 52% market share, supported by integrated diagnostic infrastructure and higher patient inflow. According to industry research, hospitals & clinics will continue to lead the market with a CAGR of 8.51%, driven by the expansion of hospital infrastructure worldwide through government-backed and private investments.

Dermatology Diagnostic Devices Market: Regional Analysis

Why does North America dominate the dermatology diagnostic devices market?

The global dermatology diagnostics devices market will be led by North America during the forecast period. North America accounted for around 39% of global revenue in 2024 and is projected to grow at 8.61% CAGR. The region benefits from advanced healthcare infrastructure, strong reimbursement frameworks, and early adoption of AI-enabled diagnostic systems. Additionally, the high disposable income of the general population and medical tourism further help the regional market thrive.

How is Europe performing in the dermatology diagnostic devices market?

Europe accounted for nearly 27% of global revenue in 2024 and is expected to grow at a CAGR of 8.21% in the coming years. Countries such as Germany, the UK, and France are investing in non-invasive imaging technologies and digital health platforms, supporting steady regional market growth. Rising healthcare expenditure, access to promising national health insurance programs, and a stronger focus on improving medical care for people of all economic backgrounds will support Europe’s growth trends in the future.

Why is Asia-Pacific the fastest-growing region in the dermatology diagnostic devices market?

Asia-Pacific accounted for approximately 21% of the market in 2024 and is projected to grow at a CAGR of 8.7%. Increasing dermatology awareness, expanding healthcare access, and growing demand for aesthetic procedures are driving regional expansion. China, India, and South Korea will lead the regional industry growth trends. South Korea hosts several domestic and international patients seeking aesthetic procedures. According to the Korea Health Industry Development Institute, more than 705,000 foreign patients received dermatological treatments in the country in 2024.

Dermatology Diagnostic Devices Market: Competitive Analysis

The global dermatology diagnostic devices market is led by:

- Caliber Imaging & Diagnostics

- Canfield Scientific

- 3Gen

- AMD Global Telemedicine

- Strata Skin Sciences

- FotoFinder Systems

- Firefly Global

- QuantifiCare

- VivaScope GmbH

- Heine Optotechnik

- Courage + Khazaka Electronic

- Michelson Diagnostics

- Bruker

- DermaSensor

- MetaOptima Technology

What are the latest key trends in the dermatology diagnostic devices market?

Connected diagnostic procedures

The growing investments in developing connected diagnostic procedures represent a promising trend in the dermatology diagnostic devices market. It includes cloud-based imaging sharing between medical experts and patients, smartphone-based dermatoscopes, and other solutions that offer an integrated patient experience.

Non-invasive diagnostic tools

Patients are actively seeking non-invasive diagnostic tools, creating demand for procedures such as Reflectance Confocal Microscopy (RCM) and high-frequency ultrasound. Non-invasive dermatology diagnostic devices are poised for significant growth in the coming years.

The global dermatology diagnostic devices market is segmented as follows:

By Type

- Handheld Devices

- Imaging Systems

- Laboratory Diagnostic Devices

By Technology

- Optical Coherence Tomography (OCT)

- Dermoscopy

- Ultrasound Imaging

- Confocal Microscopy

- Molecular & Genetic Diagnostic Techniques

By Application

- Hospitals & Clinics

- Dermatology Centers

- Diagnostic Laboratories

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table Of Content

Methodology

FrequentlyAsked Questions

Dermatology diagnostic devices are advanced medical tools used to detect, monitor, and diagnose skin-related conditions with improved accuracy.

The global dermatology diagnostic devices market is expected to grow due to the rising incidence of skin cancer and chronic dermatological disorders, which are increasing due to ageing populations, higher UV exposure, environmental pollution, and lifestyle changes.

According to study, the global dermatology diagnostic devices market size was worth around USD 2.81 billion in 2024 and is predicted to grow to around USD 6.90 billion by 2034.

The CAGR value of the dermatology diagnostic devices market is expected to be around 10.50% during 2025-2034.

Competition from low-cost diagnostic alternatives and concerns over counterfeit devices are the major challenges restraining the growth of the dermatology diagnostic devices market.

Connected diagnostic procedures and non-invasive diagnostic tools are the emerging trends and innovations impacting the dermatology diagnostic devices market.

The global dermatology diagnostic devices market has performed well so far and will offer similar trends in the coming years.

The global dermatology diagnostics devices market will be led by North America during the forecast period.

The global dermatology diagnostic devices market is led by players like Caliber Imaging & Diagnostics, Canfield Scientific, 3Gen, AMD Global Telemedicine, Strata Skin Sciences, FotoFinder Systems, Firefly Global, QuantifiCare, VivaScope GmbH, Heine Optotechnik, Courage + Khazaka Electronic, Michelson Diagnostics, Bruker, DermaSensor, and MetaOptima Technology.

The report explores crucial aspects of the dermatology diagnostic devices market, including a detailed discussion of existing growth factors and restraints, while also browsing future growth opportunities and challenges that impact the market.

HappyClients