Centrifugal Pump Market Size, Share, Growth, Opportunities 2034

Centrifugal Pump Market By Type (Single Stage Pumps, Multi Stage Pumps, Axial Split Pumps, Radial Split Pumps, Vertical Pumps), By Capacity (Low-Capacity, Medium-Capacity, High-Capacity), By Application (Water and Wastewater, Oil and Gas, Chemical Processing, Power Generation, Food and Beverage, Pharmaceuticals, Mining), By End-User (Industrial, Municipal, Agricultural, Commercial), and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 42.98 Billion | USD 75.77 Billion | 6.50% | 2024 |

Centrifugal Pump Industry Perspective:

What will be the size of the centrifugal pump market during the forecast period?

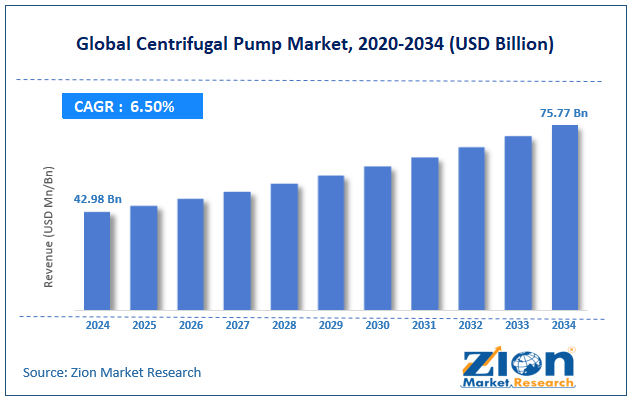

The global centrifugal pump market size was worth approximately USD 42.98 billion in 2024 and is projected to grow to around USD 75.77 billion by 2034, with a compound annual growth rate (CAGR) of roughly 6.50% between 2025 and 2034.

Key Insights

- As per the analysis shared by our research analyst, the global centrifugal pump market is estimated to grow annually at a CAGR of around 6.50% over the forecast period (2025-2034).

- In terms of revenue, the global centrifugal pump market size was valued at approximately USD 42.98 billion in 2024 and is projected to reach USD 75.77 billion by 2034.

- The centrifugal pump market is projected to grow significantly due to rising water and wastewater treatment needs, increasing industrial production, expanding oil and gas exploration, expanding power generation capacity, and technological advancements in pump efficiency and reliability.

- Based on type, the single-stage pumps segment is expected to lead the centrifugal pump market, while the multi-stage pumps segment is anticipated to grow significantly.

- Based on capacity, the medium-capacity segment is expected to lead the centrifugal pump market, while the high-capacity segment is anticipated to grow rapidly.

- Based on application, the water and wastewater segment is the dominating segment, while the oil and gas segment is projected to witness sizeable revenue over the forecast period.

- Based on end-user, the industrial segment is expected to lead the market, followed by the municipal segment.

- Based on region, Asia Pacific is projected to dominate the global centrifugal pump market during the estimated period, followed by North America.

Centrifugal Pump Market: Overview

Centrifugal pumps are mechanical devices that move liquids by using a rapidly rotating impeller to convert motor energy into fluid flow. The spinning action pushes the liquid outward toward the discharge outlet, maintaining a steady, continuous flow during operation. Centrifugal pumps are used to handle water, chemicals, oil products, wastewater, and many other industrial liquids. Their design is simple and contains fewer moving parts than many other pump types. Because of this simple structure, maintenance needs are lower, and operating costs remain more affordable. These pumps are suitable for moving large volumes of liquid at moderate pressure levels. Their compact structure allows installation in limited spaces with both horizontal and vertical mounting options. Centrifugal pumps operate quietly and with minimal vibration, making them suitable for commercial and residential environments. They respond quickly to flow-control adjustments via valves or speed changes. Modern designs focus on improving energy efficiency while maintaining required flow performance. These pumps are widely used across industries such as water treatment, agriculture, power generation, and manufacturing.

The increasing demand for water infrastructure development and industrial expansion is expected to drive growth in the centrifugal pump market over the forecast period.

Centrifugal Pump Market: Technology Roadmap 2025–2034

What is the projected development roadmap of the centrifugal pump market over the forecast period?

The centrifugal pump market is growing rapidly due to infrastructure investment, industrial automation, sustainability efforts, and advances in materials and digital monitoring technologies. The market is expected to grow at a CAGR of around 6.50% over the forecast period, driven by rising demand across water management, industrial processing, and energy production applications. The following roadmap outlines key development phases expected through 2034.

2025–2027: Efficiency Improvement and Materials Innovation Phase

- New impeller designs help pumps use less electricity while still moving the same amount of liquid, especially in single-stage pumps, which hold nearly 47% market share.

- Stronger materials, such as ceramic coatings and special metals, help pumps last longer when handling dirty or rough liquids in factories.

- Improved sealing systems stop leaks and prevent fluid contamination in industries such as chemicals and pharmaceuticals, where cleanliness is critical.

2028–2031: Smart Monitoring and Predictive Maintenance Phase

- Built-in sensors measure temperature, pressure, vibration, and flow to provide operators with clear, real-time information on pump performance.

- Smart software analyzes pump data and warns maintenance teams before a breakdown, helping prevent sudden shutdowns and costly repairs.

- Remote monitoring systems enable companies to track and manage multiple pumps from a single control center via online dashboards.

2032–2034: Energy Optimization and Sustainable Operation Phase

- Variable-speed drives adjust pump speed in response to actual demand, reducing energy waste and lowering overall energy bills.

- Energy recovery systems capture unused pressure energy and convert it into useful power, improving system efficiency.

- Eco-friendly manufacturing uses recycled materials and renewable energy while promoting repair and reuse programs to reduce environmental impact.

Centrifugal Pump Market: Dynamics

Growth Drivers

How is growing investment in water and wastewater infrastructure driving the expansion of the centrifugal pump market?

The centrifugal pump market is growing quickly as governments invest more money in water supply and wastewater treatment projects. The water and wastewater sector remains the largest sector using these pumps. Growing cities need bigger water systems to deliver clean drinking water from treatment plants to homes and offices. Many developed countries also replace old and damaged pumps to avoid breakdowns and reduce water leakage. Wastewater treatment plants use centrifugal pumps to safely move sewage, sludge, and treated water through various cleaning stages. Factories also install special pumps to handle chemical waste and dirty water produced during manufacturing processes. Farmers depend on centrifugal pumps to draw water from wells, rivers, and lakes for irrigation. In dry regions, desalination plants use high-pressure pumps to turn seawater into fresh water for daily use. Flood control stations rely on large pumps to quickly remove rainwater from streets and low-lying areas. Water transfer projects between regions also use powerful centrifugal pumps to move water over long distances.

Industrial development boosts growth in the centrifugal pump market.

The global centrifugal pump industry is growing steadily as manufacturing activity increases across many industrial sectors that require reliable liquid movement systems. Chemical plants use centrifugal pumps to move raw materials, circulate process liquids, transfer finished products, and safely handle industrial waste. These pumps are built with special materials to resist corrosion and meet strict safety standards. Oil refineries rely heavily on centrifugal pumps to move crude oil through different refining stages and into storage tanks. Petrochemical facilities use these pumps to handle hot liquids, high-pressure fluids, and reactive chemicals during the production of plastics and fertilizers. Power plants use centrifugal pumps to move boiler water, cool equipment, and support fuel systems for electricity generation. Food and beverage factories install sanitary pumps to safely process milk, juices, syrups, and cleaning liquids. Pharmaceutical manufacturers depend on precise pumps to control liquid flow and prevent contamination during the production of medicines. Mining companies use strong pumps to move slurry, remove water from mines, and process minerals. Pulp and paper industries also use centrifugal pumps to move wood pulp, mix chemicals, and treat wastewater during paper manufacturing operations.

Restraints

How is competition from alternative pump technologies limiting the growth of the centrifugal pump market?

A major challenge for the centrifugal pump market is strong competition from other pump types designed for specific industrial uses. Positive displacement pumps, such as gear, piston, and diaphragm pumps, provide steady flow at high pressure, making them better for thick liquids and accurate dosing tasks. Peristaltic pumps move liquids gently and are preferred in pharmaceutical and biotechnology industries where delicate materials must not be damaged during transfer. Progressive cavity pumps perform better for thick slurries and heavy pastes commonly found in mining, food processing, and wastewater treatment plants. Magnetic-drive pumps prevent leakage by eliminating shaft seals, improving safety when handling hazardous and corrosive chemicals. Rotary lobe pumps allow reversible flow and can draw liquid without priming, giving them flexibility in certain processing systems. Submersible pumps are installed directly inside wells or tanks, reducing installation complexity and improving reliability in water applications. Air-operated diaphragm pumps are portable and safe for transferring flammable liquids in hazardous environments. Many customers continue to use familiar pump technologies rather than switching to centrifugal designs, even when energy savings are possible.

Opportunities

Smart technologies and industrial automation are driving growth in the centrifugal pump market.

The centrifugal pump industry is growing steadily as manufacturers integrate smart technologies into modern pump systems across industrial facilities. Intelligent pumps deliver greater operational value by improving monitoring, control, and overall system performance compared with traditional pump models. Many pumps connect to the Internet of Things to share real-time data with centralized control platforms. These systems transmit information about temperature, vibration, pressure levels, and energy usage to improve operational decision-making. Wireless sensors reduce the need for complex wiring and make installation easier in both new plants and older facilities. Cloud-based software analyzes performance data from multiple sites to identify efficiency improvements and reduce energy waste. Digital twin technology creates virtual models of pumps to simulate operating conditions without performing physical testing. Automated control systems allow pumps to adjust speed or activate backup units when system demand changes. Energy management tools track electricity consumption and help companies lower operating costs through smarter usage planning. Mobile applications provide maintenance teams with remote access to pump status, alerts, and service history.

Challenges

How are raw material costs and supply chain complexity creating challenges for the centrifugal pump industry?

The centrifugal pump industry faces cost challenges due to fluctuating raw material prices, which affect manufacturing expenses. Stainless steel, widely used for corrosion-resistant pumps, depends on nickel and chromium markets, which often experience price fluctuations. Specialized materials such as duplex steel and titanium cost more and increase overall production expenses for heavy-duty pump applications. Cast iron prices also rise and fall with industrial demand, which in turn influences the pricing of standard water pumps. Motor and electrical component costs vary due to movements in copper and rare-earth material prices. Global supply chains sometimes face shipping delays and port congestion, slowing the delivery of important pump components. Shortages of electronic chips affect smart pump production and delay shipments of advanced products. Manufacturers must test parts carefully when sourcing from multiple suppliers to maintain consistent pump quality. Long delivery times during high-demand periods can frustrate customers and create opportunities for competitors.

Centrifugal Pump Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Centrifugal Pump Market |

| Market Size in 2024 | USD 42.98 Billion |

| Market Forecast in 2034 | USD 75.77 Bllion |

| Growth Rate | CAGR of 6.50% |

| Number of Pages | 227 |

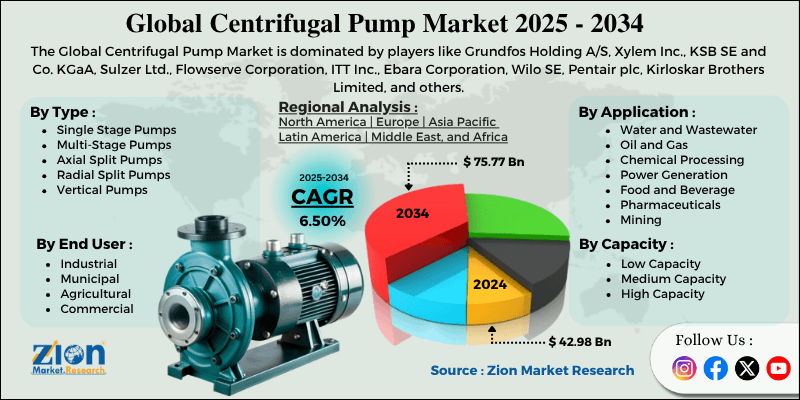

| Key Companies Covered | Grundfos Holding A/S, Xylem Inc., KSB SE and Co. KGaA, Sulzer Ltd., Flowserve Corporation, ITT Inc., Ebara Corporation, Wilo SE, Pentair plc, Kirloskar Brothers Limited, and others. |

| Segments Covered | By Type, By Capacity, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Centrifugal Pump Market: Segmentation

The global centrifugal pump market is segmented based on type, capacity, application, end-user, and region.

Why is the single stage pumps segment expected to lead the centrifugal pump market?

Based on type, the global centrifugal pump industry is categorized into single-stage, multi-stage, axial split, radial split, and vertical pumps. The single-stage pumps segment accounted for approximately 47% of global market share and is expected to remain dominant during the forecast period due to their simple construction, lower cost, ease of maintenance, and suitability for the majority of industrial and municipal water-handling applications. The multi-stage pumps segment follows as the second-largest category, with nearly 28% market share, driven by rising demand for high-pressure applications, including boiler feed water, reverse osmosis systems, and high-rise building water supply requiring pressure beyond single-stage capabilities.

What supports the leadership of the medium capacity segment in the centrifugal pump market during the forecast period?

Based on capacity, the market is divided into low-capacity, medium-capacity, and high-capacity. The medium-capacity segment accounts for around 51% of the total market share. It is expected to lead throughout the forecast period, as these pumps balance flow rate, pressure, and cost-effectiveness for the broadest range of industrial processes and municipal applications. The high-capacity segment ranks second with approximately 31% market share, supported by growing use in power generation cooling systems, large-scale water transfer projects, and major industrial facilities that require massive fluid volumes.

Why does the water and wastewater segment dominate the centrifugal pump market?

Based on application, the global centrifugal pump market is segregated into water and wastewater, oil and gas, chemical processing, power generation, food and beverage, pharmaceuticals, and mining. The water and wastewater segment accounts for nearly 36% of the overall market share. It continues to lead, driven by massive infrastructure investment globally in municipal water systems, treatment facilities, and industrial water management. The oil and gas segment accounts for approximately 22% of the market, driven by upstream exploration and production, midstream pipeline operations, and downstream refining processes, all of which require specialized centrifugal pumps for crude oil, refined products, and chemical handling.

What enables the industrial segment to lead the global centrifugal pump market?

Based on end user, the market is segmented into industrial, municipal, agricultural, and commercial categories. The industrial segment leads with approximately 54% market share and is expected to grow steadily, supported by diverse manufacturing sectors, including chemicals, petroleum, power generation, and processing, which consume large quantities of pumps. The municipal segment holds the second position with nearly 26% market share, driven by public water utilities, wastewater treatment authorities, and city infrastructure departments that maintain and expand water and sewer systems serving growing urban populations.

Centrifugal Pump Market: Regional Analysis

What factors enable the Asia Pacific to dominate the global centrifugal pump market during the forecast period?

Asia Pacific is expected to hold 41.7% of global demand and remain the main production and consumption center in the centrifugal pump market. The region leads due to rapid industrial growth, large-scale infrastructure spending, a rising population, and strong urban expansion. China is the largest producer and consumer of centrifugal pumps, driven by its vast manufacturing base and water projects. Fast city development across the region increases demand for drinking water systems, sewage treatment plants, and flood control facilities. Many new factories in the chemical, steel, cement, and petrochemical industries require pumps for daily production operations. Power plants across the coal, nuclear, and renewable sectors depend on centrifugal pumps for cooling and water movement.

Growing agricultural production in India and Southeast Asia drives demand for irrigation pumps to support food supply needs. Industrial parks and economic zones require water supply and wastewater systems that feature extensive pump networks. Competitive production costs and skilled workers support strong pump manufacturing across the region. Government programs focusing on rural water access and industrial development maintain steady demand. Expanding construction projects, transportation infrastructure, and smart city initiatives further increase the number of pump installations in urban and semi-urban areas. Rising export activities from regional manufacturers also strengthen the Asia Pacific’s position in the global centrifugal pump supply chain. Continued infrastructure investment keeps Asia Pacific at the center of global centrifugal pump growth.

Why is North America expected to be the second leading region in the global centrifugal pump market?

North America is expected to account for about 23.9% of the global centrifugal pump market and remain the second-largest regional contributor. The United States leads the region due to strong industrial activity, large infrastructure spending, and ongoing modernization programs. Canada also supports steady demand through investments in water treatment, mining, and oil sands operations. The market is growing as aging infrastructure across the United States requires pump replacements and system upgrades to meet updated efficiency standards.

Major states such as Texas, California, and Pennsylvania invest heavily in water management and energy projects. Shale oil and gas production in Texas and North Dakota drives strong demand for reliable centrifugal pump systems. Chemical manufacturing hubs along the Gulf Coast are modernizing facilities with advanced, corrosion-resistant pumps. Power generation projects across the Midwest and Southeastern United States maintain steady pump usage for cooling systems. Canada’s mining sector, particularly in provinces like Ontario and Alberta, requires heavy-duty pumping equipment. Municipal water utilities across urban centers continue replacing outdated systems to improve service reliability. Strict environmental policies in both the United States and Canada promote the adoption of leak-proof and energy-efficient pump technologies. A strong regional economy and industrial reshoring trends further sustain long-term demand for centrifugal pumps.

Recent Market Developments

- In August 2025, Ekki Homa, a joint venture between India’s Ekki Group and Germany’s Homa Pumpenfabrik, launched a new sewage pump platform designed to address clogging issues in wastewater infrastructure and support the rapid expansion of sewage treatment projects across the Asia Pacific.

Centrifugal Pump Market: Competitive Analysis

The leading players in the global centrifugal pump market are:

- Grundfos Holding A/S

- Xylem Inc.

- KSB SE and Co. KGaA

- Sulzer Ltd.

- Flowserve Corporation

- ITT Inc.

- Ebara Corporation

- Wilo SE

- Pentair plc

- Kirloskar Brothers Limited

The global centrifugal pump market is segmented as follows:

By Type

- Single Stage Pumps

- Multi-Stage Pumps

- Axial Split Pumps

- Radial Split Pumps

- Vertical Pumps

By Capacity

- Low Capacity

- Medium Capacity

- High Capacity

By Application

- Water and Wastewater

- Oil and Gas

- Chemical Processing

- Power Generation

- Food and Beverage

- Pharmaceuticals

- Mining

By End-User

- Industrial

- Municipal

- Agricultural

- Commercial

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table Of Content

Methodology

FrequentlyAsked Questions

Centrifugal pumps are mechanical devices that move liquids by using a rapidly rotating impeller to convert motor energy into fluid flow. The spinning action pushes the liquid outward toward the discharge outlet, maintaining a steady, continuous flow during operation.

The global centrifugal pump market is projected to grow due to increasing water and wastewater treatment needs, rising industrial production, growing oil and gas exploration, expanding power generation capacity, and technological advancements in pump efficiency and reliability.

According to a study, the global centrifugal pump market size was worth around USD 42.98 billion in 2024 and is predicted to grow to around USD 75.77 billion by 2034.

The CAGR value of the centrifugal pump market is expected to be around 6.50% during 2025-2034.

Asia Pacific is expected to lead the global centrifugal pump market during the forecast period.

The major players profiled in the global centrifugal pump market include Grundfos Holding A/S, Xylem Inc., KSB SE and Co. KGaA, Sulzer Ltd., Flowserve Corporation, ITT Inc., Ebara Corporation, Wilo SE, Pentair plc, and Kirloskar Brothers Limited.

The report examines key aspects of the centrifugal pump market, including a detailed analysis of current growth drivers and constraints, as well as future growth opportunities and challenges.

In the centrifugal pump market, investment opportunities focus on smart pump technologies, energy-efficient systems, water infrastructure projects, and industrial automation partnerships. Companies pursue joint ventures in emerging markets, digital monitoring platforms, and aftermarket service networks to expand their global presence and secure long-term revenue streams.

In the global centrifugal pump market, the value chain covers raw material sourcing, manufacturing, assembly, testing, distribution, installation, and aftermarket maintenance and spare parts services.

In the centrifugal pump market, emerging trends include IoT-enabled smart pumps, predictive maintenance systems, digital twin technology, energy optimization solutions, and sustainable manufacturing practices. Manufacturers adopt advanced materials and cloud-based monitoring tools to improve efficiency and lower total operating costs.

HappyClients