Cancer Pain Market Size, Share, Trends, Growth & Forecast 2034

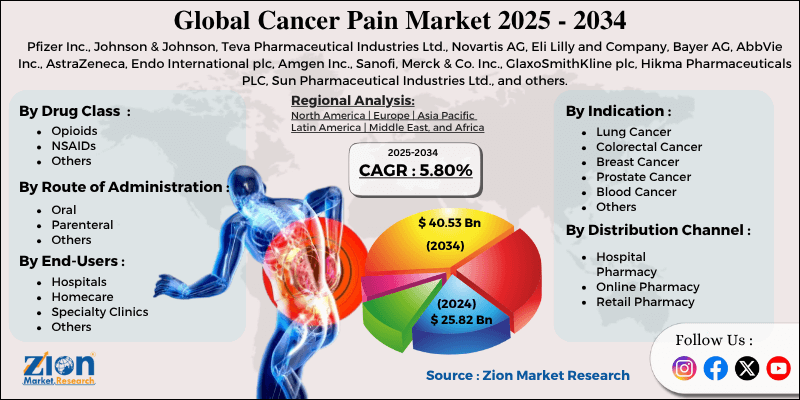

Cancer Pain Market By Drug Class (Opioids, NSAIDs, and Others), By Indication (Lung Cancer, Colorectal Cancer, Breast Cancer, Prostate Cancer, Blood Cancer, and Others), By Route of Administration (Oral, Parenteral, and Others), By End-Users (Hospitals, Homecare, Specialty Clinics, and Others), By Distribution Channel (Hospital Pharmacy, Online Pharmacy, Retail Pharmacy), and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 25.82 Billion | USD 40.53 Billion | 5.80% | 2024 |

Cancer Pain Industry Perspective:

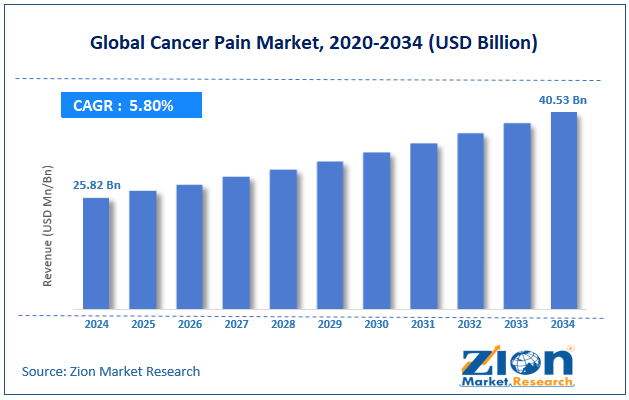

The global cancer pain market size was approximately USD 25.82 billion in 2024 and is projected to reach around USD 40.53 billion by 2034, with a compound annual growth rate (CAGR) of approximately 5.80% between 2025 and 2034.

Cancer Pain Market: Overview

Cancer pain is an often debilitating and complex symptom faced by cancer patients, originating from tumor growth, inflammation, nerve compression, or the side effects of treatments like radiation or chemotherapy. It may change from chronic pain or mild discomfort to acute pain, significantly impacting the quality of life for patients. The global cancer pain market is poised for notable growth, driven by the growing geriatric population, advancements in drug formulations, and increasing awareness of palliative care. Aging is a key risk factor for chronic pain and cancer patients. The global population aged 65 and above is projected to reach 1.5 billion by 2050, resulting in a substantial patient pool. This demographic trend propels the demand for long-term and targeted pain management solutions.

Moreover, improvements in non-opioid and opioid drug delivery, like extended release tablets, transdermal patches, and buccal sprays, are enhancing efficiency. These improved formulations improve clinical outcomes and patient compliance. Pharmaceutical research and development are actively supporting the development of better delivery mechanisms for cancer pain medications.

Additionally, there is an increasing recognition of palliative care's role in enhancing the quality of life for patients with cancer. NGOs and governments are also promoting pain management in oncology. This has broadened access to pain management and reduced global undertreatment of pain.

Nevertheless, the global market faces limitations due to factors such as underreporting and undertreatment of pain, as well as a stringent regulatory approval process. Several cancer patients, mainly in low-income regions, underreport pain because of a lack of awareness of the stigma. Therefore, pain remains inadequately managed. This restricts the global reach and efficiency of cancer pain therapies. Additionally, gaining regulatory approval for novel cancer pain drugs could be time-consuming and costly. Efficiency, safety, and long-term use may delay market entry. This impacts product innovation and product launch schedules for pharmaceutical companies.

Still, the global cancer pain industry benefits from several favorable factors, including personalized pain management solutions and the development of non-opioid therapeutics. Advances in patient profiling and genomics may support the development of personalized medicine for cancer pain. Modified regimens enhance treatment precision and reduce side effects. This opens fresh avenues for biotech advancements. There is a key industry potential for non-opioid and safer alternatives like antidepressants, cannabinoids, and nerve growth factor inhibitors. These alternatives are gaining notable demand because of opioid-associated issues. Biopharma players are actively investing in new drug discovery.

Key Insights:

- As per the analysis shared by our research analyst, the global cancer pain market is estimated to grow annually at a CAGR of around 5.80% over the forecast period (2025-2034)

- In terms of revenue, the global cancer pain market size was valued at around USD 25.82 billion in 2024 and is projected to reach USD 40.53 billion by 2034.

- The cancer pain market is projected to grow significantly owing to mounting demand for palliative care, growing cancer incidences worldwide, and government funding support and initiatives.

- Based on drug class, the opioids segment is expected to lead the market, while the NSAIDs segment is expected to grow considerably.

- Based on the indication, the lung cancer segment is the largest, while the breast cancer segment is projected to experience substantial revenue growth over the forecast period.

- Based on route of administration, the oral segment is expected to lead the market, while the parenteral segment is expected to grow considerably.

- Based on end-users, the hospitals segment is the largest, while the homecare segment is projected to experience substantial revenue growth over the forecast period.

- Based on the distribution channel, the hospital pharmacy segment is expected to lead the market, followed by the retail pharmacy segment.

- Based on region, North America is projected to dominate the global market during the estimated period, followed by Europe.

Cancer Pain Market: Growth Drivers

The growing integration of supportive and palliative care services drives the market growth

Oncology centers and hospitals are actively integrating palliative care in mainstream cancer treatment, fueling the demand for improved pain management facilities. Over 61% of cancer patients in developed nations are receiving specialized pain care as a key unit of their treatment protocol, according to the Lancet Commission on Palliative Care 2024.

This incorporation enhances quality of life and also allows early intervention for pain symptoms, mainly in cases of chemotherapy-induced neuropathy, bone metastases, or tumor compression.

Modernization in drug delivery technologies considerably fuels the market growth

Technological improvements in drug delivery systems are changing the outlook for cancer pain treatment. New formulations, such as sublingual sprays, transdermal patches, targeted nanoparticles, and infusion pumps, are enhancing drug bioavailability, ease of use, and safety. These advancements support quality of care and better compliance, ultimately impacting the cancer pain market.

Boston Scientific and Medtronic are increasing implantable infusion systems for long-standing spinal administration of opioids, aiding localized pain relief in the advanced cancer patient pool.

Cancer Pain Market: Restraints

The risk of drug dependency and severe side effects hinders the market's progress

Long-term use of NSAIDs and opioids for cancer patients is usually associated with several side effects, including sedation, constipation, nausea, increased risk of dependency, and tolerance. These complications, mainly the risk of addiction, create hesitancy among both healthcare providers and patients, creating a psychological and clinical barrier to pain management and restricting the cancer pain market demand.

Cancer Pain Market: Opportunities

Rising awareness and global advocacy for pain relief access favorably impact market growth

International organizations, such as Human Rights Watch and the International Association for Hospice and Palliative Care, are rigorously campaigning for global access to essential pain medications. The WHO introduced a Global Pain Relief Initiative in 2024, aiming to enhance opioid access in 22 low-income and resource-constrained countries by 2030. These advocacy efforts are compelling pharmaceutical companies and governments to increase supply, refine regulatory frameworks, and foster private-public partnerships, thereby creating sustained opportunities for impact and growth, ultimately advancing the cancer pain industry.

Cancer Pain Market: Challenges

High development costs and regulatory barriers for new therapies restrict the growth of market

Developing new pain management devices or drugs, especially in non-opioid therapies, requires significant investment in research and development, compliance, and regulatory trials. Pharma and biotech companies face development costs exceeding $1 billion per accepted drug, a

ccording to PhRMA 2024 data. Moreover, a lengthy approval process by agencies like the FDA and EMA delays market entry and restricts advancement. This increases the risk and cost for new entrants in the cancer pain domain.

Cancer Pain Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Cancer Pain Market |

| Market Size in 2024 | USD 25.82 Billion |

| Market Forecast in 2034 | USD 40.53 Billion |

| Growth Rate | CAGR of 5.80% |

| Number of Pages | 215 |

| Key Companies Covered | Pfizer Inc., Johnson & Johnson, Teva Pharmaceutical Industries Ltd., Novartis AG, Eli Lilly and Company, Bayer AG, AbbVie Inc., AstraZeneca, Endo International plc, Amgen Inc., Sanofi, Merck & Co. Inc., GlaxoSmithKline plc, Hikma Pharmaceuticals PLC, Sun Pharmaceutical Industries Ltd., and others. |

| Segments Covered | By Drug Class, By Indication, By Route of Administration, By End-Users, By Distribution Channel, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Cancer Pain Market: Segmentation

The global cancer pain market is segmented based on drug class, indication, route of administration, end-users, distribution channel, and region.

Based on drug class, the global industry is divided into opioids, NSAIDs, and others. The opioids segment registered a substantial share of the market because of their efficiency in managing severe and moderate cancer pain, mainly in advanced-stage patients—the broader clinical preference for strong opioids like oxycodone, morphine, and fentanyl fuels the segmental growth.

Based on indication, the global market is segmented into lung cancer, colorectal cancer, breast cancer, prostate cancer, blood cancer, and others. The lung cancer segment holds a notable market share, with growth attributed to its high global incidence and the intense, often late-stage pain it causes.

Based on the route of administration, the global cancer pain industry is divided into oral, parenteral, and other routes. The oral administration route captured a substantial share due to its cost-effectiveness, ease of use, and patient preference, particularly in home care and outpatient settings.

Based on end-users, the global cancer pain market is segmented into hospitals, homecare, specialty clinics, and others. The hospitals segment accounted for a larger market share due to the exhaustive oncology and pain management facilities they offer, comprising palliative, surgical, and pharmacological care.

Based on distribution channel, the global market is segmented into hospital pharmacy, online pharmacy, and retail pharmacy. The hospital pharmacy segment has dominated the global market, as it directly dispenses medications for inpatients undergoing surgery, cancer treatment, or palliative care.

Cancer Pain Market: Regional Analysis

North America to witness significant growth over the forecast period

North America is projected to maintain its dominant position in the global cancer pain market due to high cancer incidence rates, a growing geriatric population, a robust healthcare ecosystem, and supportive reimbursement and insurance coverage. North America, especially the United States, reports higher cancer cases across the globe, with more than 2 million new cancer cases projected in the United States alone in 2025, according to the American Cancer Society. A majority of these patients face moderate to severe pain, needing medical intervention. The aging population, anticipated to reach 95 million, aged 65 and above in the U.S. by 2060, further fuels this demand.

Moreover, the region boasts a well-developed healthcare infrastructure, including dedicated oncology and palliative care centers, which facilitate comprehensive pain management and support. Hospitals are equipped with superior technologies and trained staff to administer interventional and pharmacological treatment. This strong setup promises that cancer patients are treated, diagnosed, and monitored consistently and efficiently.

Additionally, cancer pain management is encompassed by private and public insurance plans, comprising Medicaid, Medicare, and private insurers in the United States. This coverage extends to home-based and hospital treatments, reducing the cost of extra hospitalizations for patients. Reimbursement policies incentivize the use of enhanced therapies and drugs, driving industry value in the region.

Europe maintains its position as the second-leading region in the global cancer pain industry, thanks to strong universal and public healthcare coverage, advanced hospice and palliative care infrastructure, and an increasing senior population. Several European nations offer universal healthcare, which includes cancer pain treatments as part of palliative and oncology care services. Systems like the CNAM (France), NHS (United Kingdom), and GKV (Germany) promise broader access to pain services and medications. This exhaustive public support increases drug uptake and adherence in patient populations.

The region also has an established palliative care ecosystem facilitated by NGOs and government policies. The EAPC has contributed to the development of country-level protocols for cancer pain management. These structured services provide access to dedicated care, primarily in cases involving metastatic and end-of-life care. Furthermore, Europe is facing significant population aging, with over 21% of the population aged 65 and above in 2024. Geriatric patients are prone to both chronic and cancer pain, raising the need for continuous pain therapy. In addition, increasing cancer survival rates create the need for long-standing pain care.

Cancer Pain Market: Competitive Analysis

The key operating players in the worldwide cancer pain market include:

- Pfizer Inc.

- Johnson & Johnson

- Teva Pharmaceutical Industries Ltd.

- Novartis AG

- Eli Lilly and Company

- Bayer AG

- AbbVie Inc.

- AstraZeneca

- Endo International plc

- Amgen Inc.

- Sanofi

- Merck & Co. Inc.

- GlaxoSmithKline plc

- Hikma Pharmaceuticals PLC

- Sun Pharmaceutical Industries Ltd.

Cancer Pain Market: Key Market Trends

Increasing use of adjunctive and non-opioid therapies:

To decrease dependency on opioids, there is a surging adoption of non-opioid therapies like corticosteroids, antidepressants, cannabis-based compounds, and bisphosphonates. Adjunctive therapies, such as spinal pumps, nerve blocks, and transdermal systems, are also gaining prominence. This diversification resolves chronic and breakthrough cancer pain more safely and holistically.

Growth of home-based and palliative care models:

The demand for palliative and home-based cancer care services is increasing globally, driven by patient comfort, cost-effectiveness, and advancements in telehealth. Home infusion services, transdermal and oral drug delivery systems, and remote monitoring aid long-term pain control outside hospital settings. This trend is mainly strong in developed nations and is gaining traction in developing economies.

The global cancer pain market is segmented as follows:

By Drug Class

- Opioids

- NSAIDs

- Others

By Indication

- Lung Cancer

- Colorectal Cancer

- Breast Cancer

- Prostate Cancer

- Blood Cancer

- Others

By Route of Administration

- Oral

- Parenteral

- Others

By End-Users

- Hospitals

- Homecare

- Specialty Clinics

- Others

By Distribution Channel

- Hospital Pharmacy

- Online Pharmacy

- Retail Pharmacy

By Region

- North America

- The U.S.

- Canada

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Southeast Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Table Of Content

Methodology

FrequentlyAsked Questions

Cancer pain is an often debilitating and complex symptom faced by cancer patients, originating from tumor growth, inflammation, nerve compression, or the side effects of treatments like radiation or chemotherapy. It may transition from chronic pain to mild discomfort or even acute pain, which can significantly impact the quality of life for patients.

The global cancer pain market is projected to grow due to the increasing prevalence of a geriatric population, the expansion of healthcare infrastructure in emerging nations, and the growing emphasis on targeted therapies and personalized medicine.

According to study, the global cancer pain market size was worth around USD 25.82 billion in 2024 and is predicted to grow to around USD 40.53 billion by 2034.

The CAGR value of the cancer pain market is expected to be approximately 5.80% from 2025 to 2034.

North America is expected to lead the global cancer pain market during the forecast period.

The key players profiled in the global cancer pain market include Pfizer Inc., Johnson & Johnson, Teva Pharmaceutical Industries Ltd., Novartis AG, Eli Lilly and Company, Bayer AG, AbbVie Inc., AstraZeneca, Endo International plc, Amgen Inc., Sanofi, Merck & Co., Inc., GlaxoSmithKline plc, Hikma Pharmaceuticals PLC, and Sun Pharmaceutical Industries Ltd.

The report examines key aspects of the cancer pain market, including a detailed analysis of existing growth factors and restraints, as well as an examination of future growth opportunities and challenges that will impact the market.

HappyClients