Airport Metal Detectors Market Size, Growth, Global Trends, Forecast 2034

Airport Metal Detectors Market By Product Type (Walk-Through Metal Detectors, Handheld Metal Detectors, and Ground Search Metal Detectors), By Application (Passenger Screening, Baggage and Parcel Inspection, Staff and Crew Screening, and Perimeter Security), By End-User (International Airports, Domestic Airports, Private & Charter Airports, and Military & Government Terminals), By Distribution Channel (Direct Government Procurement, System Integrators and Contractors, Security Equipment Distributors, and Online Procurement Platforms), and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

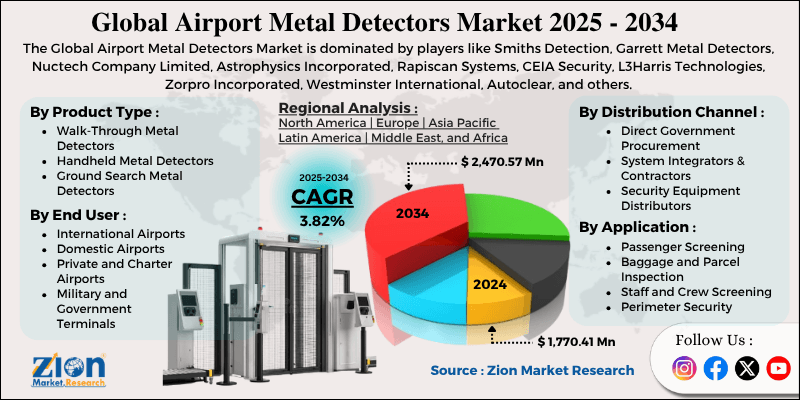

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 1,770.41 Million | USD 2,470.57 Million | 3.82% | 2024 |

Airport Metal Detectors Industry Perspective:

What will be the size of the airport metal detectors market during the forecast period?

The global airport metal detectors market size was worth approximately USD 1,770.41 million in 2024 and is projected to grow to around USD 2,470.57 million by 2034, with a compound annual growth rate of roughly 3.82% between 2025 and 2034.

Key Insights

- As per the analysis shared by our research analyst, the global airport metal detectors market is estimated to grow annually at a compound annual growth rate of around 3.82% over the forecast period from 2025 to 2034.

- In terms of revenue, the global airport metal detectors market size was valued at approximately USD 1,770.41 million in 2024 and is projected to reach USD 2,470.57 million by 2034.

- The airport metal detectors market is expected to grow at a strong pace, driven by rising global air passenger traffic, stricter aviation security mandates, ongoing airport construction and renovation projects, growing adoption of multi-technology screening solutions, and increasing investments in security infrastructure across emerging economies.

- Based on product type, the walk-through metal detectors segment is expected to lead the airport metal detectors market, while the handheld metal detectors segment is anticipated to grow at a notably fast pace due to its flexibility and low cost.

- Based on application, the passenger screening segment is expected to lead the airport metal detectors market, while the staff and crew screening segment is anticipated to grow rapidly as internal security protocols are tightened.

- Based on end-user, the international airports segment is the largest current end-user group, while the domestic airports segment is anticipated to grow most rapidly during the forecast period as smaller airports upgrade aging security infrastructure.

- Based on distribution channel, the direct government procurement segment is expected to lead the airport metal detectors market, while online procurement platforms are anticipated to grow steadily as procurement processes become more digitized.

- Based on region, North America is projected to dominate the global airport metal detectors market during the estimated period, followed by Europe and the Asia Pacific.

Airport Metal Detectors Market: Overview

Airport metal detectors are security machines that scan people and their belongings to find hidden metal items at airport checkpoints. These devices create a magnetic field, and any metal object passing through it disturbs the field, triggering an alarm for further inspection. Walk-through detectors form a gate-like structure that scans the entire body as a person walks through, while handheld detectors are used by security staff to locate the exact position of the metal object on a person. Ground search detectors are primarily used outdoors to check airport surroundings and restricted zones. Modern airport metal detectors are more advanced and efficient compared to older versions. They can identify different types of metals and reduce unnecessary alarms caused by everyday items such as keys, coins, and belt buckles.

Many systems are designed to work alongside other airport security technologies, helping create a smoother, safer screening process. Some detectors are also combined with imaging systems and smart software that help security teams quickly identify possible risks. Airports worldwide are focusing on improving passenger flow while maintaining strict safety standards. As a result, there is a growing demand for metal detectors that are fast, accurate, and reliable, ensuring both traveler convenience and strong airport security.

The growing volume of global air travel, tightening aviation security standards, modernization of airport infrastructure, and increasing government spending on public safety are all contributing to the steady expansion of the airport metal detectors market.

Impact of the USA-Israel War on Iran on the Airport Metal Detectors Market

The ongoing conflict involving the United States, Israel, and Iran is expected to have a notable effect on the airport metal detectors market. Heightened geopolitical tensions generally prompt governments to increase spending on national security and aviation safety infrastructure. Over the longer term, if regional stability improves, reconstruction and infrastructure development in affected areas may create new market opportunities as airports are modernized or rebuilt.

Airport Metal Detectors Market: Technology Roadmap 2025–2034

What is the projected development roadmap of the airport metal detectors market over the forecast period?

The airport metal detectors market is advancing through improvements in detection sensitivity, integration with artificial intelligence and biometric systems, development of multi-threat screening platforms, and the adoption of automated alarm resolution technologies. The market is expected to grow at a compound annual growth rate of around 3.82% over the forecast period, driven by consistent demand from airport operators, aviation regulators, and government security agencies.

The following roadmap outlines key development phases expected through 2034.

2025–2027: Intelligent Detection and Integration Phase

- Airport metal detector manufacturers are expected to use artificial intelligence to interpret alarms better, reducing unnecessary alerts and helping passengers move through security faster.

- Integration with biometric identity systems is likely to grow, enabling smoother, contactless screening at major airports.

- Manufacturers are expected to design lighter handheld detectors with longer battery life and better comfort for security staff.

2028–2031: Multi-Threat Detection and Global Expansion

- Screening systems that can detect both metal and non-metal threats in one pass are expected to become more widely used, reducing the need for multiple checks.

- Airports in Southeast Asia, the Middle East, Africa, and Latin America are likely to increase purchases of modern detection systems as air travel continues to rise.

- Cloud-based platforms are expected to enable real-time monitoring across terminals.

2032–2034: Autonomous Screening and Next-Generation Security

- Fully automated screening lanes combining metal detection, imaging, and smart decision-making are expected to reduce manual checks at routine security points.

- Self-adjusting metal detectors are projected to automatically adjust sensitivity based on the surrounding environment and passenger flow.

- Advanced threat databases and machine learning are likely to be built directly into detectors for instant threat identification without relying on cloud systems.

Airport Metal Detectors Market: Dynamics

Growth Drivers

What is driving the growth of the airport metal detectors market as global aviation expands and security requirements become stricter?

The airport metal detectors market is growing steadily due to rising global air travel and stricter airport security requirements. Increasing passenger traffic across international and domestic routes is pushing airports to upgrade screening systems to handle higher volumes without delays. Governments and aviation authorities are enforcing stricter safety regulations, driving demand for advanced, reliable metal detection technologies. Rapid airport infrastructure development, especially in emerging economies, is another major growth factor for the airport metal detectors market. New airports and terminal expansions require modern security systems that can ensure safety while maintaining smooth passenger flow.

At the same time, older airports are replacing outdated equipment with faster and more accurate detectors. Technological advancements are also playing a key role in market growth. Features such as improved sensitivity, reduced false alarms, and integration with other security systems are making metal detectors more efficient. Growing concerns about terrorism, smuggling, and other illegal activities are further driving investment in airport security. The need for contactless, seamless screening experiences is also encouraging airports to adopt smarter detection systems, thereby supporting continued growth in the airport metal detectors market.

Airport construction and modernization projects worldwide are generating significant equipment demand.

The airport metal detectors industry is also growing due to the increasing number of airport construction and modernization projects worldwide, which are driving strong demand for new security equipment. Large investments in smart airport initiatives are driving the adoption of connected, automated screening systems that improve overall operational efficiency. The rising focus on passenger experience is pushing airports to install faster, less intrusive security solutions that reduce waiting times. Airports are also adopting standardized global security protocols, increasing the need for uniform, high-performance metal detection systems across regions. The expansion of low-cost carriers and regional airlines is leading to the development of smaller airports, further boosting equipment demand.

In addition, public-private partnerships in airport development are accelerating the procurement of advanced security technologies. Sustainability goals are also influencing purchasing decisions, with airports preferring energy-efficient and durable detection systems. The growing adoption of data-driven security management and predictive maintenance tools is further supporting the adoption of modern metal detectors, strengthening overall market growth.

Restraints

How do high equipment costs and long procurement cycles create challenges for suppliers in the airport metal detectors market?

The airport metal detectors market faces several challenges that slow down its growth despite rising demand for better security. One major problem is the high cost of advanced metal detection systems. Modern detectors with artificial intelligence, imaging features, and network connectivity are much more expensive than basic models, making them difficult for smaller airports and those in developing regions to afford. Limited budgets often force these airports to delay upgrades or continue using older systems. Another key restraint is the complex and time-consuming government procurement process. Airports usually follow strict rules that involve multiple approvals, detailed checks, and long bidding procedures before purchasing equipment. These processes can take months or even years, delaying the adoption of new technology. As a result, manufacturers face long, uncertain sales cycles, while airports continue to rely on outdated systems that may not meet modern security standards.

Opportunities

Smart airports and expanding aviation networks in developing regions are creating new growth opportunities in the airport metal detectors market.

The airport metal detectors market is poised for strong growth as airports focus on smarter, more efficient security systems. One major opportunity comes from the global shift toward smart airports, where security equipment is expected to do more than just detect metal. Airports are looking for systems that can share data in real time, connect to central monitoring platforms, and integrate seamlessly with passenger identity and boarding systems. Companies that offer such connected, intelligent solutions are more likely to win contracts in modern airport projects. Another important opportunity lies in the rapid growth of aviation in developing regions like Africa, South Asia, and Southeast Asia.

Rising middle-class populations and increasing air travel demand are pushing governments to build new airports, creating new demand for comprehensive security systems. In addition, the growth of private aviation, including charter services and business jet terminals, is increasing demand for smaller, flexible, high-performing metal detection systems that fit into compact spaces. Growing focus on passenger convenience and faster security checks is further boosting demand for advanced detection solutions.

Challenges

What challenges does the airport metal detectors market face in balancing accuracy, passenger convenience, and evolving threats?

The airport metal detectors industry faces several ongoing challenges that require constant improvement and careful management. A major issue is balancing detection accuracy with the risk of false alarms. Highly sensitive detectors often flag harmless items like coins or keys, causing delays and frustration for passengers, while less sensitive systems may miss real threats. Finding the right balance remains a difficult task for manufacturers. Another challenge is keeping up with evolving security threats, as new methods for concealing prohibited items continue to emerge. This requires regular updates in technology, software, and detection systems, increasing research costs and putting pressure on pricing.

In addition, ensuring smooth coordination between different security systems is becoming more complex. Many airports use equipment from multiple suppliers, and ensuring all systems work together efficiently with central monitoring platforms requires strong technical integration, which adds to operational difficulties across the airport metal detectors market.

Airport Metal Detectors Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Airport Metal Detectors Market |

| Market Size in 2024 | USD 1,770.41 Million |

| Market Forecast in 2034 | USD 2,470.57 Million |

| Growth Rate | CAGR of 3.82% |

| Number of Pages | 226 |

| Key Companies Covered | Smiths Detection, Garrett Metal Detectors, Nuctech Company Limited, Astrophysics Incorporated, Rapiscan Systems, CEIA Security, L3Harris Technologies, Zorpro Incorporated, Westminster International, Autoclear, and others. |

| Segments Covered | By Product Type, By Application, By End-User, By Distribution Channel, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Airport Metal Detectors Market: Segmentation

The global airport metal detectors market is segmented by product type, application, end-user, distribution channel, and region.

What makes the walk-through metal detectors segment lead in the airport metal detectors market?

Based on product type, the global airport metal detectors market is categorized into walk-through metal detectors, handheld metal detectors, and ground search metal detectors. The walk-through metal detectors segment accounts for approximately 62% of the global market and remains dominant due to its role in primary passenger screening at all airport security checkpoints. The handheld metal detectors segment holds around 28% share. It plays an important supporting role in secondary screening, allowing officers to locate detected objects on a person's body accurately, and its lower cost makes it an attractive procurement choice for budget-conscious operators.

How does the passenger screening application segment maintain its leading position in the airport metal detectors market?

Based on application, the airport metal detectors industry is divided into passenger screening, baggage and parcel inspection, staff and crew screening, and perimeter security. The passenger screening segment accounts for approximately 58% of the global market share, driven by the mandatory requirement to screen every arriving and departing passenger at commercial airports worldwide. The staff and crew screening segment holds around 18% share. It is growing steadily as airports strengthen internal security and tighten employee screening regulations following insider-related incidents.

What helps the international airports segment lead the airport metal detectors end-user market?

Based on end-user, the market is segregated into international airports, domestic airports, private and charter airports, and military and government terminals. The international airports segment leads the market with approximately 54% of global market share, driven by higher passenger volumes and stricter international security requirements. The domestic airports segment holds around 30% share. It is growing rapidly as governments prioritize upgrading security at smaller and regional airports to bring them in line with international standards.

How does direct government procurement dominate the distribution landscape of the airport metal detectors market?

Based on distribution channel, the airport metal detectors market is classified into direct government procurement, system integrators and contractors, security equipment distributors, and online procurement platforms. The direct government procurement segment accounts for around 45% of the global market and is expected to remain dominant, as the majority of large airport security equipment purchases are handled through government-controlled or government-supervised procurement processes. The online procurement platforms segment holds around 9% share. It is growing as smaller operators and developing airports use digital platforms for better pricing and more equipment options.

Airport Metal Detectors Market: Regional Analysis

What factors make North America the leading region in the airport metal detectors market?

The airport metal detectors market is led by North America, which is expected to grow at a CAGR of around 5.1% during the forecast period, due to its large airport network, high security standards, and strong government funding. The region has numerous commercial airports that handle high passenger traffic, creating ongoing demand for reliable, advanced screening equipment. The United States plays the largest role, as the Transportation Security Administration enforces strict security rules at thousands of airport checkpoints. Regular equipment upgrades are required to meet changing regulations, which keeps demand consistent. High government spending on aviation security also supports the growth of the airport metal detectors market in the region.

In addition, North America is quick to adopt new technologies, including smart detection systems and integrated security platforms, which further strengthen its leadership. Canada also contributes significantly through ongoing upgrades and expansions of major airports in cities such as Toronto, Vancouver, and Montreal. Strong focus on passenger safety, advanced research and development, and the presence of leading security equipment manufacturers give North America a clear advantage.

High awareness about security risks and strict compliance requirements further drives continuous investment in advanced screening systems. Strong collaboration between government agencies and private players also supports faster deployment of new technologies. Efficient airport operations and early adoption of modern screening solutions continue to support the region’s leading position in the airport metal detectors market.

What drives Europe’s strong position in the airport metal detectors market?

The airport metal detectors market ranks Europe as the second-largest region, with a CAGR of about 4.8%, driven by its many busy international airports and strong demand for reliable screening systems. Countries such as Germany, the United Kingdom, France, and the Netherlands operate major airport hubs with high traffic and stringent security measures, underscoring the need for advanced metal detectors. European Union aviation regulations require high security standards, which encourage airports to upgrade their screening equipment regularly. The growing focus on smooth, fast passenger movement is also driving investment in modern, digitally connected security systems. The rise of low-cost airlines has increased the number of travelers across the region, adding more pressure on airports to manage security efficiently.

Expansion and renovation of airport infrastructure across Europe are further supporting equipment demand. Strong emphasis on passenger safety, technology adoption, and regulatory compliance helps Europe maintain its position as the second-largest region. The presence of leading security technology providers in Europe also supports innovation and regular product upgrades. Increasing cross-border travel within the region underscores the need for consistent, high-quality screening systems. Continuous improvements in airport operations and increasing travel demand keep the region’s growth steady in the airport metal detectors market.

Recent Market Developments

- In January 2026, Smiths Detection announced the deployment of advanced HI-SCAN 6040 CTiX 3D X-ray and automated screening technologies as part of a major airport upgrade program, improving security efficiency and passenger throughput at high-traffic international hubs.

Airport Metal Detectors Market: Competitive Analysis

The leading players in the global airport metal detectors market are;

- Smiths Detection

- Garrett Metal Detectors

- Nuctech Company Limited

- Astrophysics Incorporated

- Rapiscan Systems

- CEIA Security

- L3Harris Technologies

- Zorpro Incorporated

- Westminster International

- Autoclear

The global airport metal detectors market is segmented as follows:

By Product Type

- Walk-Through Metal Detectors

- Handheld Metal Detectors

- Ground Search Metal Detectors

By Application

- Passenger Screening

- Baggage and Parcel Inspection

- Staff and Crew Screening

- Perimeter Security

By End-User

- International Airports

- Domestic Airports

- Private and Charter Airports

- Military and Government Terminals

By Distribution Channel

- Direct Government Procurement

- System Integrators and Contractors

- Security Equipment Distributors

- Online Procurement Platforms

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table Of Content

Methodology

FrequentlyAsked Questions

An airport metal detectors are security machines that scan people and their belongings to find hidden metal items at airport checkpoints. These devices create a magnetic field, and any metal object passing through it disturbs the field, triggering an alarm for further inspection.

The global airport metal detectors market is expected to grow, driven by rising air passenger volumes, stricter aviation security regulations, ongoing airport construction worldwide, growing adoption of intelligent multi-threat screening systems, and increasing security investment in emerging aviation markets across Asia, Africa, and Latin America.

According to a study, the global airport metal detectors market size was worth around USD 1,770.41 million in 2024 and is predicted to grow to around USD 2,470.57 million by 2034.

The compound annual growth rate value of the airport metal detectors market is expected to be around 3.82% during 2025–2034.

North America is expected to lead the global airport metal detectors market during the forecast period, driven by its large network of commercial airports, strong government investment in aviation security programs, and consistently stringent screening requirements across the region.

The major players in the global airport metal detectors market include Smiths Detection, Garrett Metal Detectors, Nuctech Company Limited, Astrophysics Incorporated, Rapiscan Systems, CEIA Security, L3Harris Technologies, and Westminster International.

The report examines key aspects of the airport metal detectors market, including growth drivers, restraints, emerging opportunities, challenges, a competitive landscape analysis, regional breakdowns, and a detailed future outlook across all major product types, applications, end users, and geographies.

The airport metal detectors market is primarily driven by direct government procurement, as airport authorities and regulatory bodies purchase equipment through official tenders and contracts to ensure compliance with quality standards and long-term security requirements.

The airport metal detectors market value chain includes raw material and component sourcing, detector design and manufacturing, software development and integration, quality testing and regulatory certification, distribution through government procurement or specialist channels, installation and commissioning at airport facilities, and ongoing maintenance and technical support services.

Technological advancements are driving the airport metal detectors market by improving detection accuracy, reducing false alarms, and enabling integration with smart security systems, artificial intelligence, and real-time data monitoring to enable faster, more efficient screening processes.

HappyClients