U.S. Integrated Delivery Network Market Is Predicted to Grow Around USD 2239.12 Billion By 2030

31-May-2023 | Zion Market Research

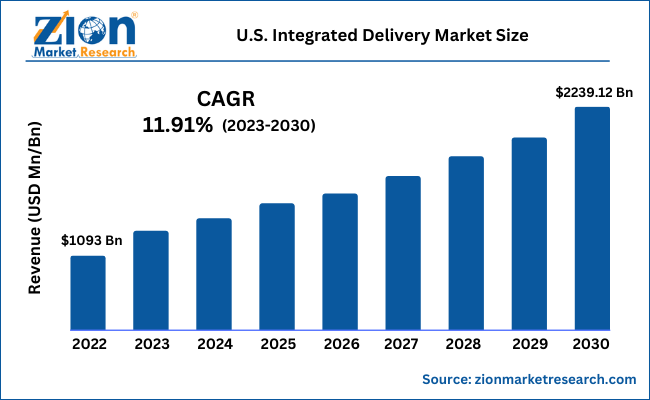

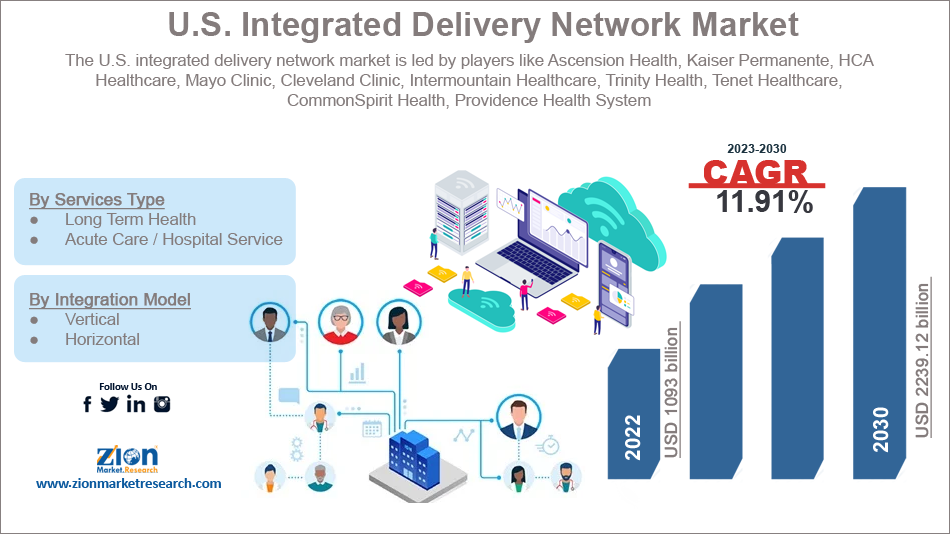

The U.S. integrated delivery network market size was worth around USD 1093 Billion in 2022 and is predicted to grow to around USD 2239.12 Billion by 2030 with a compound annual growth rate (CAGR) of roughly 11.91% between 2023 and 2030.

The integrated delivery network market refers to the segment of the healthcare industry that consists of integrated healthcare organizations. They are responsible for providing a range of coordinated and comprehensive healthcare services. An integrated delivery network (IDN) is a functional network of healthcare providers, including hospitals, physician groups, post-acute care facilities, outpatient clinics, and other healthcare entities that are aligned to work together in a collaborative effort with the end goal of delivering integrated care to patients. IDN systems aim to improve the quality, efficiency, and coordination of healthcare delivery.

This can be achieved by creating a seamless continuum of care for patients. In recent times, the U.S. integrated delivery network industry has registered significant growth due to several factors with the growing demand for value-based care acting as the main source of growth.

The U.S. integrated delivery network market is projected to grow owing to the growing adoption of care coordination and integration systems. IDN architecture ensures that patients have access to seamless and well-coordinated care by reducing the impact of fragmented healthcare systems. Medical facilities can improve patient outcomes by coordinating services, sharing information, and streamlining care transitions. IDNs tend to focus on population health management and the growing emphasis on this aspect of health management is expected to fuel market growth during the forecast period.

With the aid of technologies such as data analytics, predictive modeling, and care management strategies, it will become easier for stakeholders operating in an IDN structure to proactively identify and address the health needs of specific populations. Such an approach is likely to improve health outcomes, reduce hospital admissions, and lower healthcare costs. It becomes possible for healthcare facilities to achieve economies of scale by consolidating resources, negotiating favorable contracts, and leveraging their size to implement cost-saving initiatives. Cost efficiencies can be achieved by centralizing administrative functions, standardizing protocols, and optimizing supply chains which are all aided by IDN.

The U.S. integrated delivery network industry is likely to come across certain growth restrictions driven by the existence of several complex regulations and policies that the US healthcare system is subject to. These policies may differentiate at federal, state, and local levels and it may become challenging to comply with such variations. Another significant limitation is the lack of a robust technological infrastructure that allows data interoperability and seamless information sharing. Although the US is considered one of the most highly advanced countries, its information technology (IT) is still limited to deploying massive undertakings such as IDN.

The growing incidences of chronic diseases could provide several growth opportunities while the concerns over cost-efficiency and return on investment may challenge the regional market growth.

The U.S. integrated delivery network market is segmented based on service type, integration model, and region.

Based on service type, the market is segmented as long term health and acute care /hospital service. In 2022, the industry was dominated by the acute care/hospital service segment. It led to more than 50.1% of the segmental share.

The growth rate was driven by the increasing number of medical services associated with this model. It includes hospital settings for the diagnosis, treatment, and management of severe or life-threatening illnesses or injuries. They also encompass a range of surgical, medical, and diagnostic interventions that may require specialized care and immediate treatment. By incorporating acute care/hospital services, it becomes possible to reduce fragmentation and promote better care coordination. The segment is expected to grow owing to the rising advancements in medical technologies, diagnostic tools, and treatment modalities.

Based on the integration model, the U.S. integrated delivery network industry segments are vertical and horizontal. More than 68.12% of the segmental share was led by the vertical integration model and it involves coordination between organizations that provide different levels of medical care.

This model can take up several forms. For instance, integration between hospitals and physicians involves bringing together the involved parties under common ownership or affiliation. This allows closer collaboration, coordination, and integration of care between hospitals and physicians. Post-acute care integration involves coordination between skilled nursing facilities, rehabilitation centers, and home health agencies. The transition from acute hospital settings to post-acute care becomes easy under this model.

The U.S. integrated delivery network market is projected to witness the highest growth in the Northeastern region consisting of some of the most advanced states in the US such as New York and Massachusetts that are equipped with well-established healthcare-infrastructure and growing inclination toward value-based care driven by favorable regional medical policies and patient awareness. The Midwest region of the US consists of regions such as Illinois, Michigan, and Ohio. The regions have a diverse healthcare landscape which ranges from urban to rural regions and consists of a mix of large integrated health systems and smaller regional IDNs. Southern regions such as Texas, Florida, and Georgia which consist of diverse populations, rapid population growth, and a mix of urban and rural areas may also register higher growth rates.

Browse the full “U.S. Integrated Delivery Network Market By Services Type (Long Term Health and Acute Care / Hospital Service), By Integration Model (Vertical and Horizontal), and By Region - Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2023 – 2030” Report at https://www.zionmarketresearch.com/report/us-integrated-delivery-network-market

Recent Developments:

- In March 2023, Cleveland Clinic Akron General launched a new care model for improving outcomes in pregnant patients. The model is called TeamBirth and will involve the care team to stay in regular touch with the patients

- In January 2020, Union Hospital in Maryland was acquired by ChristianaCare, a major IDN between Baltimore and Philadelphia

The U.S. integrated delivery network market is led by players like:

- Ascension Health

- Kaiser Permanente

- HCA Healthcare

- Mayo Clinic

- Cleveland Clinic

- Intermountain Healthcare

- Trinity Health

- Tenet Healthcare

- CommonSpirit Health

- Providence Health System

- University of Pittsburgh Medical Center (UPMC)

- AdventHealth

- Northwell Health

- NewYork-Presbyterian Hospital

- Advocate Aurora Health

- Banner Health

- Geisinger Health

- Sutter Health

- Cedars-Sinai Health System

- Baylor Scott & White Health

- Bon Secours Mercy Health

- Sanford Health

- Spectrum Health

- Advocate Health Care

- Carolinas HealthCare System (Atrium Health).

The U.S. integrated delivery network market is segmented as follows:

By Services Type

- Long Term Health

- Acute Care / Hospital Service

By Integration Model

- Vertical

- Horizontal

By Region

- U.S.

About Us:

Zion Market Research is an obligated company. We create futuristic, cutting-edge, informative reports ranging from industry reports, the company reports to country reports. We provide our clients not only with market statistics unveiled by avowed private publishers and public organizations but also with vogue and newest industry reports along with pre-eminent and niche company profiles. Our database of market research reports comprises a wide variety of reports from cardinal industries. Our database is being updated constantly in order to fulfill our clients with prompt and direct online access to our database. Keeping in mind the client’s needs, we have included expert insights on global industries, products, and market trends in this database. Last but not the least, we make it our duty to ensure the success of clients connected to us—after all—if you do well, a little of the light shines on us.

Contact Us:

Zion Market Research

244 Fifth Avenue, Suite N202

New York, 10001, United States

Tel: +49-322 210 92714

USA/Canada Toll-Free No.1-855-465-4651

Email: sales@zionmarketresearch.com

Website: https://www.zionmarketresearch.com