Silicon As A Platform Market Size, Share, Trends, Growth 2034

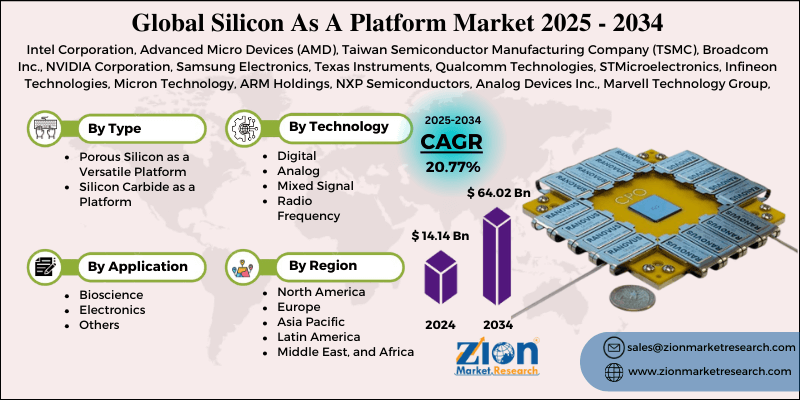

Silicon As A Platform Market By Type (Porous Silicon as a Versatile Platform, Silicon Carbide as a Platform), By Technology (Digital, Analog, Mixed Signal, Radio Frequency), By Application (Bioscience, Electronics, and Others), and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 14.14 Billion | USD 64.02 Billion | 20.77% | 2024 |

Silicon As A Platform Industry Perspective:

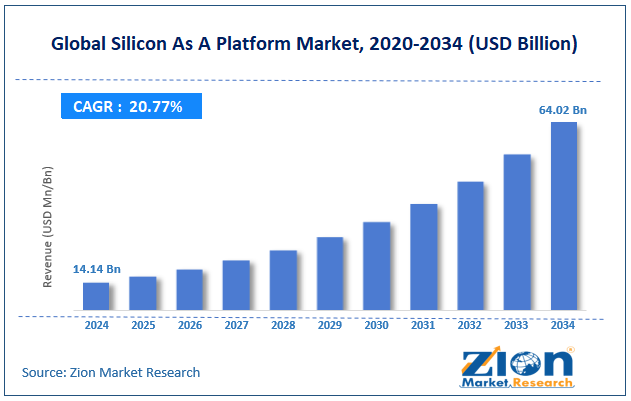

The global Silicon as a platform market size was worth around USD 14.14 billion in 2024 and is predicted to grow to around USD 64.02 billion by 2034, with a compound annual growth rate (CAGR) of roughly 20.77% between 2025 and 2034.

Request Free SampleRequest Free SampleRequest Free Sample

Request Free SampleRequest Free SampleRequest Free Sample

Silicon As A Platform Market: Overview

Silicon as a platform integrates silicon-based technologies, such as sensors, semiconductors, and microprocessors, to facilitate advanced functionalities across diverse industries. It serves as a foundation for innovations in IoT, AI, cloud computing, and 5G by offering energy efficiency, high performance, and scalability. The global Silicon as a platform market is projected to witness substantial growth driven by the growing adoption of ML and AI, the rise of smart devices and IoT, and the expansion of 5G infrastructure. ML and AI workloads require platforms with high processing power, speed, and energy efficiency, which are key attributes facilitated by silicon platforms. These are extensively adopted in voice assistants, predictive analytics tools, and autonomous vehicles. As AI integration increases, silicon platforms remain the core of hardware support.

Moreover, the proliferation of wearables, industrial IoT, and smart homes is producing enormous demand for low-power, high-performance, and compact chips. Silicon platforms allow unified device communication, edge processing, and data collection. Furthermore, silicon-based platforms are vital for facilitating high data rates and ultra-low latency needed by 5G. Telecom firms are primarily investing in 5G deployment worldwide, mainly in the Asia Pacific and North America. This is fueling the demand for advanced silicon components in user devices and network equipment.

Although drivers exist, the global market is challenged by factors like complex integration, manufacturing, and supply chain disturbances. The intricacy of integrating digital, analog, memory components, and RF on a single platform may present design challenges. Production problems during fabrication also complicate production. These technical challenges slow product commercialization. Additionally, global chip scarcity and geopolitical stresses disturb silicon supply chains. The restricted availability of raw materials like rare earth metals and silicon wafers affects production capacity. This raises costs and lead times.

Even so, the global Silicon as a platform industry is well-positioned due to the growth of neuromorphic computing and edge AI. Edge AI chips with silicon platforms may process data locally in different devices. This reduces latency and enhances privacy. Mimicking human brain functions, neuromorphic chips offer huge unexplored potential. The integration of quantum and photonic technologies is also favorable for market growth. Silicon photonics enables data to be transmitted through light, increasing bandwidth and speed remarkably. Likewise, silicon-based quantum chips are in early deployment stages. These advances offer next-generation computing competencies.

Key Insights:

- As per the analysis shared by our research analyst, the global Silicon as a platform market is estimated to grow annually at a CAGR of around 20.77% over the forecast period (2025-2034)

- In terms of revenue, the global Silicon as a platform market size was valued at around USD 14.14 billion in 2024 and is projected to reach USD 64.02 billion by 2034.

- The Silicon as a platform market is projected to grow significantly owing to the growing integration of innovative technologies and IoT devices, the rising need for energy-efficient processing solutions, and improvements in semiconductor fabrication technologies.

- Based on type, the silicon carbide as a platform segment is expected to lead the market, while the porous Silicon as a versatile platform segment is expected to grow considerably.

- Based on technology, the digital segment is the dominating segment, while the mixed signal segment is projected to witness sizeable revenue over the forecast period.

- Based on application, the electronics segment is expected to lead the market compared to the bioscience segment.

- Based on region, North America is projected to dominate the global market during the estimated period, followed by the Asia Pacific.

Silicon As A Platform Market: Growth Drivers

How is the emergence of machine learning and AI in devices boosting the Silicon as a platform market?

Machine learning and artificial intelligence workloads require high-speed processing, efficient interconnects, and low latency, all of which are facilitated by Silicon as a platform solution, such as chiplet-based designs and 3D stacking. According to reports, the AI chip industry is expected to surpass USD 200 billion by 2032, with SiP platforms playing a crucial role in this growth.

NVIDIA launched a novel AI system-on-platform (SoP) in March 2025 that integrates a GPU, communication interfaces, and memory using the chiplet and an advanced silicon substrate approach.

Wearable technology adoption and miniaturization propel the market growth

Consumer electronics, especially wearables like fitness bands, smartwatches, and VR/AR devices, are compelling lighter, smaller, and more energy-efficient solutions. Silicon as a platform allows the incorporation of multiple functions like communication, sensing, processing, and memory into ultra-compact models.

Apple's supply chain disclosed details of an innovative Apple Watch chipset based on an extensively integrated SiP design with TSV solutions and an advanced silicon interposer in early 2025, reducing form factor and enhancing battery life. This innovation majorly impacts the progress of the Silicon as a platform market.

Silicon As A Platform Market: Restraints

Which is the key restraining factor in the worldwide Silicon as a platform market?

Silicon platforms integrating multiple dies or functionalities onto a single substrate experience many thermal dissipation and power density issues. As more transistors are packed into tight spaces, managing heat becomes challenging, risking performance, failure, or degradation.

As per IEEE Spectrum 2024, more than 35% of failures in SiP modules and densely packed chiplets are associated with insufficient heat management. The intricacy is majorly acute in data centers and AI applications, where chips can produce heat loads of more than 250 W per module.

Silicon As A Platform Market: Opportunities

SiP's role in advanced wireless networks and transition to 6G positively impacts market growth

While 5G adoption increases worldwide, 6G research and trial deployments are gaining immense prominence, fueling the Silicon as a platform industry. These next-generation networks require substantially high bandwidth, low latency, and smart edge processing, all of which demand integrated silicon platforms capable of signal processing and real-time communication.

Ericsson and Samsung announced a joint research and development collaboration to develop SiP-based FR front ends and artificial intelligence edge modules for 6G base stations in May 2025. This transition offers a key opportunity for the SiP vendors to build low-latency, ultra-high-performance platforms for mobile devices and telecom equipment.

Silicon As A Platform Market: Challenges

How does the lack of EDA support and design tool standardization restrict the growth of the Silicon as a platform market?

One major challenge is the ingenuity of (EDA) electronic design automation tools for full-system SiP integration. A majority of design software packages are optimized for conventional SoCs, but adapting them for compound SiP, which involves numerous dies, interconnect protocols, and layers, requires significant retraining and upgrades.

In 2025, a majority of semiconductor companies reported that their present EDA workflows lack modularity and are cost-prohibitive for integrating 3rd party IP. Without improved toolchain standardization, scalability, and time-to-market, it remains constrained.

Request Free SampleRequest Free SampleRequest Free Sample

Request Free SampleRequest Free SampleRequest Free Sample

Silicon As A Platform Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Silicon As A Platform Market |

| Market Size in 2024 | USD 14.14 Billion |

| Market Forecast in 2034 | USD 64.02 Billion |

| Growth Rate | CAGR of 20.77% |

| Number of Pages | 211 |

| Key Companies Covered | Intel Corporation, Advanced Micro Devices (AMD), Taiwan Semiconductor Manufacturing Company (TSMC), Broadcom Inc., NVIDIA Corporation, Samsung Electronics, Texas Instruments, Qualcomm Technologies, STMicroelectronics, Infineon Technologies, Micron Technology, ARM Holdings, NXP Semiconductors, Analog Devices Inc., Marvell Technology Group, and others. |

| Segments Covered | By Type, By Technology, By Application, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Silicon As A Platform Market: Segmentation

The global Silicon as a platform market is segmented based on type, technology, application, and region.

Based on type, the global Silicon as a platform industry is divided into porous Silicon as a versatile platform and silicon carbide as a platform. The silicon carbide as a platform segment registered a maximum share due to its breakdown voltage, high thermal conductivity, and energy efficacy, which are ideal for high-frequency and high-power applications. It is extensively used in 5G base stations, electric vehicles, solar inverters, and industrial drives, where standard Silicon is not enough. Companies like STMicroelectronics, Wolfspeed, and Infineon are largely investing in SiC innovation and production.

Based on technology, the global Silicon as a platform market is segmented into digital, analog, mixed signal, and radio frequency. Digital technology dominates the global market owing to its vital role in powering memory chips, microprocessors, digital signal processors, and AI accelerators. It supports scalable and fast data processing, which is essential for smartphones, data centers, and cloud computing. With the rise of IoT, AI, and edge computing, digital silicon platforms are in remarkably high demand.

Based on application, the global market is segmented into bioscience, electronics, and others. The electronics segment holds leadership, fueled by the substantial demand for silicon platforms in automotive systems, consumer electronics, computing hardware, and telecom infrastructure. Silicon as a platform powers GPUs, CPUs, SoCs, and memory chips used in laptops, IoT devices, EVs, and smartphones. Constant advancements in 5G, AI chips, and edge computing are fueling the segmental growth.

Silicon As A Platform Market: Regional Analysis

Which key factors are aiding North America in holding dominance in the global Silicon as a platform market?

North America is likely to sustain its leadership in the Silicon as a platform market due to the robust presence of major semiconductor companies, heavy investment in Cloud, AI, and Edge infrastructure, and dominance in telecom and 5G innovation. North America houses the leading silicon platform innovators like AMD, Intel, NVIDIA, Broadcom, and Qualcomm, which are forerunners in chip design. These companies highly invest in research and development to support AI-based silicon solutions and high performance.

As per SIA, the United States companies registered 48% of the worldwide semiconductor sales in 2023. The United States is a forerunner in cloud computing, edge technologies, and AI, all of which depend on advanced silicon platforms. Firms like Google Cloud, Amazon Web Services, and Microsoft Azure utilize custom silicon to optimize processing efficacy.

Also, North American leading technology companies like AT&T and Verizon are rigorously deploying 5G infrastructure, producing a need for silicon-based network platforms. Edge devices and 5G chipsets heavily depend on customizable silicon solutions. The United States had encompassed more than 70% of its population with 5G in 2024, according to GSMA.

Asia Pacific continues to secure the second-highest share in the Silicon as a platform industry, driven by the rapid growth in mobile devices and consumer electronics, its status as a leading semiconductor manufacturing hub, and government backing. Asia Pacific is a manufacturing center for laptops, smart TVs, wearable devices, and smartphones, which all depend on integrated silicon platforms. Key OEMs like Xiaomi, Samsung, Sony, and Oppo fuel the demand for power-efficient and compact chips. Asia Pacific registered for more than 50% of the worldwide smartphone shipments in 2023, according to IDC.

Furthermore, key countries like Japan, China, Taiwan, and South Korea host leading semiconductor fabrication facilities. Samsung and TSMC dominate the worldwide chip manufacturing, supplying silicon platforms to prominent technology companies. In 2024, Asia registered for more than 70% share of the global semiconductor fabrication capacity, as per SEMI.

Additionally, nations like India and China are investing in domestic semiconductor infrastructure. China allocated over USD 150 billion to expand its chip industry, while India announced USD 10 billion in incentives for chip manufacturing. These policies support the development of a local silicon platform.

Silicon As A Platform Market: Competitive Analysis

The leading players in the global Silicon as a platform market are:

- Intel Corporation

- Advanced Micro Devices (AMD)

- Taiwan Semiconductor Manufacturing Company (TSMC)

- Broadcom Inc.

- NVIDIA Corporation

- Samsung Electronics

- Texas Instruments

- Qualcomm Technologies

- STMicroelectronics

- Infineon Technologies

- Micron Technology

- ARM Holdings

- NXP Semiconductors

- Analog Devices Inc.

- Marvell Technology Group

Silicon As A Platform Market: Key Market Trends

Custom silicon for cloud and AI workloads:

Leading technology companies, such as Microsoft, Amazon (Graviton), and Google (TPU), are designing custom silicon tailored to specific ML, AI, and cloud computing tasks. These chips offer energy efficiency and performance gains over general-purpose processors. This trend is boosting the inclination towards workload-specific silicon platforms.

Emphasis on green and energy-efficient computing:

As sustainability becomes a priority, silicon platforms are designed to decrease power consumption while maintaining the same performance. Methods like silicon photonics and near-threshold computing are gaining prominence. Enterprises are using energy-efficient chips for embedded systems and data centers.

The global Silicon as a platform market is segmented as follows:

By Type

- Porous Silicon as a Versatile Platform

- Silicon Carbide as a Platform

By Technology

- Digital

- Analog

- Mixed Signal

- Radio Frequency

By Application

- Bioscience

- Electronics

- Others

By Region

- North America

- The U.S.

- Canada

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Southeast Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Table Of Content

Methodology

FrequentlyAsked Questions

Silicon as a platform integrates silicon-based technologies, such as sensors, semiconductors, and microprocessors, to facilitate advanced functionalities across diverse industries. It serves as a foundation for innovations in IoT, AI, cloud computing, and 5G by offering energy efficiency, high performance, and scalability.

The global Silicon as a platform market is projected to grow due to increasing demand for high-performance computing, rising deployment of 5G infrastructure, and proliferation of edge computing systems.

According to study, the global Silicon as a platform market size was worth around USD 14.14 billion in 2024 and is predicted to grow to around USD 64.02 billion by 2034.

The CAGR value of the Silicon as a platform market is expected to be around 20.77% during 2025-2034.

North America is expected to lead the global Silicon as a platform market during the forecast period.

The key players profiled in the global Silicon as a platform market include Intel Corporation, Advanced Micro Devices (AMD), Taiwan Semiconductor Manufacturing Company (TSMC), Broadcom Inc., NVIDIA Corporation, Samsung Electronics, Texas Instruments, Qualcomm Technologies, STMicroelectronics, Infineon Technologies, Micron Technology, ARM Holdings, NXP Semiconductors, Analog Devices, Inc., and Marvell Technology Group.

The competitive landscape in the Silicon as a Platform market is fragmented, with key players like TSMC, Intel, ASE Group, and AMD dominating advanced integration and packaging technologies. Competition is driven by innovation in heterogeneous integration, chiplet design, and strategic partnerships in EDA tool providers and foundries.

Stringent environmental regulations on semiconductor manufacturing—particularly regarding chemical disposal, water usage, and energy consumption—are impacting SiP production scalability. Moreover, geopolitical tensions and export controls are disrupting global technology transfers and supply chains.

Pricing trends in the Silicon as a Platform market present a steady increase due to chiplet integration, high costs of advanced packaging, and substrate materials. Nonetheless, economies of scale and modular chiplet reuse are starting to offset some of these costs in high-volume segments.

The report examines key aspects of the Silicon as a platform market, including a detailed analysis of existing growth factors and restraints, as well as an examination of future growth opportunities and challenges that will impact the market.

HappyClients