Semiconductor Equipment Manufacturing Market Size, Share Report 2034

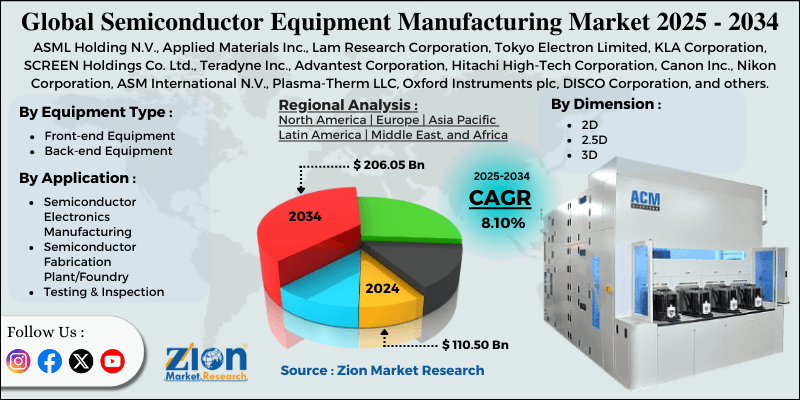

Semiconductor Equipment Manufacturing Market By Equipment Type (Front-end Equipment, Back-end Equipment), By Dimension (2D, 2.5D, 3D), By Application (Semiconductor Electronics Manufacturing, Semiconductor Fabrication Plant/Foundry, Testing & Inspection), and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 110.50 Billion | USD 206.05 Billion | 8.10% | 2024 |

Semiconductor Equipment Manufacturing Industry Perspective:

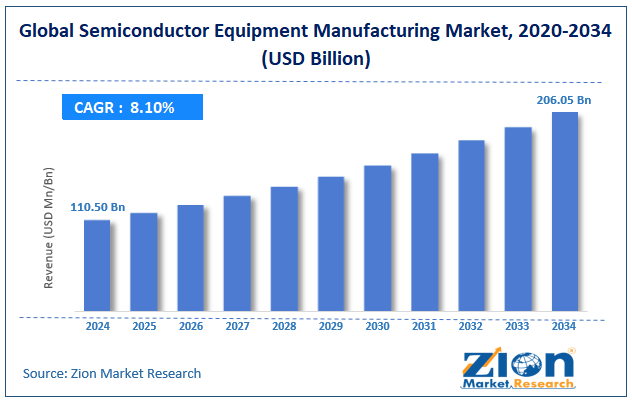

The global semiconductor equipment manufacturing market size was approximately USD 110.50 billion in 2024 and is projected to reach around USD 206.05 billion by 2034, with a compound annual growth rate (CAGR) of approximately 8.10% between 2025 and 2034.

Request Free SampleRequest Free SampleRequest Free Sample

Request Free SampleRequest Free SampleRequest Free Sample

Semiconductor Equipment Manufacturing Market: Overview

Semiconductor equipment manufacturing encompasses the production and design of tools and machines used to fabricate semiconductor devices, such as integrated circuits and chips. This sector is vital to the global electronics supply chain, providing equipment for processes such as photolithography, deposition, etching, testing, and wafer fabrication. The global semiconductor equipment manufacturing market is projected to experience substantial growth, driven by increasing demand for consumer electronics, advancements in 5G, AI, and IoT technologies, and the electrification of the automotive industry. The increasing adoption of laptops, smartphones, smart home devices, and wearables is driving up semiconductor demand.

In 2024, global smartphone shipments surpassed 1.3 billion units, triggering significant investments in semiconductor equipment and production. IoT and AI need high-performing chips with complex frameworks. With the growth of the 5G network, advanced chipsets are gaining significance. These trends are driving the demand for advanced equipment, such as high-end packaging machines and EUV lithography.

Moreover, autonomous driving systems and electric vehicles utilize a substantial amount of semiconductors for infotainment, ADAS, and battery management. The global electric vehicle market is expected to reach 17 million units by 2025, primarily driving demand for automotive-grade semiconductors.

Although drivers exist, the global market is challenged by factors such as the complexity of equipment integration and disruptions to the global supply chain. Novel technologies need precise configuration between different processes and tools. Integration complexity increases with node shrinkage, initially resulting in production delays and reduced efficiency.

Additionally, geopolitical stresses, logistical barriers, and the scarcity of raw materials such as palladium and neon impact equipment production and delivery timelines. This was witnessed during the Russia-Ukraine war and the COVID-19 pandemic. Even so, the global semiconductor equipment manufacturing industry is well-positioned due to the growth of advanced packaging technologies, the rise in compound semiconductor, and sustainability-focused equipment development. With the growing inclination towards 3D packaging and chiplet designs, there is a surging demand for new equipment, such as through-silicon via (TSV) and hybrid bonding tools. This offers opportunities for dedicated equipment makers.

Likewise, the move towards wide-bandgap materials, such as SiC and GaN, for power electronics and the 5G ecosystem raises the demand for specialized deposition, etching, and inspection tools, as well as non-silicon materials. Also, opportunities exist for producers to innovate low-emission and low-energy semiconductor tools. Green fab programs by TSMC and Intel are fueling the demand for sustainable equipment.

Key Insights:

- As per the analysis shared by our research analyst, the global semiconductor equipment manufacturing market is estimated to grow annually at a CAGR of around 8.10% over the forecast period (2025-2034)

- In terms of revenue, the global semiconductor equipment manufacturing market size was valued at around USD 110.50 billion in 2024 and is projected to reach USD 206.05 billion by 2034.

- The semiconductor equipment manufacturing market is projected to grow significantly due to increasing demand for consumer electronics, extensive use of automotive semiconductors, expansion of cloud computing, and the rise in data centers.

- Based on equipment type, the front-end equipment segment is expected to lead the market, while the back-end equipment segment is expected to grow considerably.

- Based on dimension, the 2D is the dominating segment, while the 3D segment is projected to witness sizeable revenue over the forecast period.

- Based on application, the semiconductor fabrication plant/foundry segment is expected to lead the market compared to the semiconductor electronics manufacturing segment.

- Based on region, Asia Pacific is projected to dominate the global market during the estimated period, followed by North America.

Semiconductor Equipment Manufacturing Market: Growth Drivers

Growth of IoT semiconductors and automotive boosts market growth

The automotive industry’s digital transformation is fueling the demand for chips used in infotainment, EV powertrains, V2X connectivity, and ADAS. This demand ultimately impacts the growth of the global semiconductor equipment manufacturing market.

In April 2025, STMicroelectronics and Bosch declared a EUR 3.2 billion investment in a novel SiC fab in Germany, driving orders for deposition, specialty etching, and wafer bonding. In addition, IoT devices, projected to reach 25 billion active units worldwide by 2026, are driving the adoption of wafer-level packaging and the purchase of testing equipment for low-power and smaller devices.

Expansion of fabless and foundry business models notably fuels the market growth

The global shift toward fabless semiconductor models has led to increased investment in specialized foundries, primarily in North America and the Asia-Pacific region. The latest news in May 2025 disclosed TSMC's plans to invest USD 28 billion in novel advanced-node fabs in Arizona, Taiwan, and Japan. This significant capital investment is driving the demand for advanced wafer inspection, etching, and disposition systems. Equipment manufacturers, such as Tokyo Electron and Applied Materials, are ultimately benefiting from this regional growth.

Semiconductor Equipment Manufacturing Market: Restraints

Talent shortage and technological complexity restrain the market's progress

As chiplet integration grows and semiconductor node shrinkage below 3nm, equipment maintenance and design have become complex. Operating atomic layer deposition systems or EUV requires highly specialized semiconductor engineers, mainly in mechatronics, lithography, and software integration.

The IEEE 2025 Semiconductor Workforce Survey revealed that 75% of equipment companies in Germany, Taiwan, and the United States aim to fill advanced technical jobs. This scarcity increases operational costs, delays R&D cycles, and hinders companies' ability to support fab growth projects on a global scale.

Semiconductor Equipment Manufacturing Market: Opportunities

Global fab construction boom and localization initiatives contribute to the market growth

Geopolitical stresses and the pressure for supply chain flexibility have led over 25 economies to introduce localization initiatives in the semiconductor manufacturing sector. This triggers a historic progress in fab construction, building long-term demand for etching, lithography, deposition, and test equipment. This boom eventually propels the semiconductor equipment manufacturing industry.

For example, India approved four novel semiconductor fabs under its USD 10 billion PLI scheme, supported by Micron, Tower Semiconductor, and Tata Electronics. These greenfield projects represent multi-billion-dollar and multi-year equipment procurement opportunities for universal tool suppliers.

Semiconductor Equipment Manufacturing Market: Challenges

Tool delivery delays and extended lead times limit the growth of market

The semiconductor equipment sector continues to suffer from long lead times, ranging from 12 to 24 months, for vital equipment such as advanced etching systems and EUV lithography. This delay notably affects the fab expansion schedules of chipmakers and restricts the ability of OEMs to scale production speedily.

TSMC confirmed delays in the Arizona fab schedules, partially due to extended tool delivery timelines from major vendors in March 2025. These delays result in deferred profits for equipment suppliers and operational challenges for semiconductor producers.

Request Free SampleRequest Free SampleRequest Free Sample

Request Free SampleRequest Free SampleRequest Free Sample

Semiconductor Equipment Manufacturing Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Semiconductor Equipment Manufacturing Market |

| Market Size in 2024 | USD 110.50 Billion |

| Market Forecast in 2034 | USD 206.05 Billion |

| Growth Rate | CAGR of 8.10% |

| Number of Pages | 211 |

| Key Companies Covered | ASML Holding N.V., Applied Materials Inc., Lam Research Corporation, Tokyo Electron Limited, KLA Corporation, SCREEN Holdings Co. Ltd., Teradyne Inc., Advantest Corporation, Hitachi High-Tech Corporation, Canon Inc., Nikon Corporation, ASM International N.V., Plasma-Therm LLC, Oxford Instruments plc, DISCO Corporation, and others. |

| Segments Covered | By Equipment Type, By Dimension, By Application, By End User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Semiconductor Equipment Manufacturing Market: Segmentation

The global semiconductor equipment manufacturing market is segmented based on equipment type, dimension, application, and region.

Based on equipment type, the global semiconductor equipment manufacturing industry is divided into front-end equipment and back-end equipment. The front-end equipment segment holds a notable market share due to its vital role in wafer fabrication processes. These need capital-intensive steps and are highly complex in semiconductor production. This comprises equipment for photolithography, deposition (PVD, CVD, and ALD), etching, and ion implantation. As of 2024, these tools are crucial for manufacturing advanced nodes, such as 3nm and 5nm, and account for over 65% of the global semiconductor equipment spending.

Based on dimension, the global semiconductor equipment manufacturing market is segmented into 2D, 2.5D, and 3D. 2D remains the dominant segment in terms of revenue and adoption, owing to traditional planar semiconductor manufacturing, which is still broadly used for less complex chips, such as legacy logic devices, analog ICs, and microcontrollers, in mature modes. The 2D fabrication ecosystem is well-developed and continues to lead the global market in various sectors, including IoT, industrial, and automotive.

Based on application, the global market is segmented into semiconductor electronics manufacturing, semiconductor fabrication plant/foundry, and testing & inspection. The semiconductor fabrication plant/foundry segment held a dominant share of the market due to massive investments by foundries such as Samsung, Intel, and TSMC. These facilities need a broader range of front-end equipment for wafer processing, like deposition, etching, ion implantation, and lithography, which are among the equipment- and capital-intensive stages of manufacturing.

Semiconductor Equipment Manufacturing Market: Regional Analysis

Asia Pacific to witness significant growth over the forecast period

Asia Pacific is likely to sustain its leadership in the global semiconductor equipment manufacturing market due to the dominance of leading semiconductor companies, high penetration of manufacturing facilities, and the progressing automotive and consumer electronics market. The Asia Pacific is home to the world's prominent semiconductor foundries, including Samsung Electronics, SMIC, and TSMC. These companies register for more than 70% of the global foundry profit, resulting in elevated demand for advanced fabrication equipment. Their continuous investment in superior nodes, such as 5nm and 3nm, significantly fuels equipment sales in the region.

Additionally, the region boasts a dense cluster of fabrication plants, primarily located in South Korea, Taiwan, Japan, and China. More than 60% of worldwide semiconductor fabs are located in the APAC region, according to SEMI. This penetration of production capacity fuels consistent and strong demand for back-end and front-end equipment. Similarly, the APAC region serves as a significant hub for consumer electronics manufacturing, driven by economies such as those of South Korea, China, and Japan.

The Asia Pacific region accounted for over 50% of global electronics and smartphone production as of 2024, necessitating continuous chip supply and investment in modern equipment. Increasing EV production in China also fuels the demand for automotive-grade manufacturing tools.

North America continues to hold the second-highest share in the semiconductor equipment manufacturing industry, thanks to its strong domestic semiconductor industry, innovative infrastructure, advanced R&D, and the rise of high-performance computing. The United States is home to leading chip design and manufacturing companies, including Texas Instruments, GlobalFoundries, and Intel.

The U.S. semiconductor industry was estimated to be worth over $275 billion in 2024, making it a prominent hub for equipment usage and chip production. Fab expansions by Micron and Intel are mounting equipment demand in North America. Furthermore, North America leads in semiconductors with institutions like SEMATECH. MIT and Stanford are collaborating on next-gen lithography, material science, and AI integration. This strong research environment fuels advancement in automation and equipment design.

As of 2024, the United States accounted for more than 50% of overall semiconductor equipment R&D spending. In addition, the rapid advancement of cloud computing, autonomous systems, and generative AI in North America is driving the demand for high-performance chips. Hence, more fabs are upgraded or being built with advanced equipment capable of generating AI processors and GPUs. This digital transformation has a direct impact on the regional equipment industry.

Semiconductor Equipment Manufacturing Market: Competitive Analysis

The major operating players in the global semiconductor equipment manufacturing market include:

- ASML Holding N.V.

- Applied Materials Inc.

- Lam Research Corporation

- Tokyo Electron Limited

- KLA Corporation

- SCREEN Holdings Co. Ltd.

- Teradyne Inc.

- Advantest Corporation

- Hitachi High-Tech Corporation

- Canon Inc.

- Nikon Corporation

- ASM International N.V.

- Plasma-Therm LLC

- Oxford Instruments plc

- DISCO Corporation

Semiconductor Equipment Manufacturing Market: Key Market Trends

Boom in heterogeneous integration and advanced packaging:

As traditional Moore’s Law scaling lowers, chipmakers are shifting to 3D and 2.5D packaging, heterogeneous integration, and chiplets. This inclination is surging the demand for die-stacking, wafer bonding, and TSV equipment. Packaging is now becoming a performance propeller, thus building opportunities for specialized toolmakers.

Increased focus on sustainable manufacturing and ESG:

Ecological concerns are fueling tool and fabs manufacturers to adopt energy-efficient and low-emission machines. Companies like TSMC and Intel are committed to achieving net-zero emissions by 2040-2050, triggering a wave of environmentally friendly advancements in water recycling, reduced chemical use, and energy-saving process tools.

The global semiconductor equipment manufacturing market is segmented as follows:

By Equipment Type

- Front-end Equipment

- Back-end Equipment

By Dimension

- 2D

- 2.5D

- 3D

By Application

- Semiconductor Electronics Manufacturing

- Semiconductor Fabrication Plant/Foundry

- Testing & Inspection

By Region

- North America

- The U.S.

- Canada

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Southeast Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Table Of Content

Methodology

FrequentlyAsked Questions

Semiconductor equipment manufacturing encompasses the production and design of tools and machines used to fabricate semiconductor devices, such as integrated circuits and chips. This sector is vital to the global electronics supply chain, providing equipment for processes such as photolithography, deposition, etching, testing, and wafer fabrication.

The global semiconductor equipment manufacturing market is projected to grow due to the growth of IoT, AI, and 5G technologies, the rise of advanced packaging technologies, and government incentives and national chip programs.

According to study, the global semiconductor equipment manufacturing market size was worth around USD 110.50 billion in 2024 and is predicted to grow to around USD 206.05 billion by 2034.

The CAGR value of the semiconductor equipment manufacturing market is expected to be around 8.10% during 2025-2034.

Asia Pacific is expected to lead the global semiconductor equipment manufacturing market during the forecast period.

The key players profiled in the global semiconductor equipment manufacturing market include ASML Holding N.V., Applied Materials Inc., Lam Research Corporation, Tokyo Electron Limited, KLA Corporation, SCREEN Holdings Co., Ltd., Teradyne Inc., Advantest Corporation, Hitachi High-Tech Corporation, Canon Inc., Nikon Corporation, ASM International N.V., Plasma-Therm LLC, Oxford Instruments plc, and DISCO Corporation.

The report examines key aspects of the semiconductor equipment manufacturing market, including a detailed analysis of existing growth factors and restraints, as well as an examination of future growth opportunities and challenges that will impact the market.

List of Contents

Semiconductor Equipment ManufacturingIndustry Perspective:OverviewKey Insights:Growth DriversRestraintsOpportunitiesChallengesReport ScopeSegmentationRegional AnalysisCompetitive AnalysisKey Market TrendsThe global semiconductor equipment manufacturing market is segmented as follows:HappyClients