Radiopharmaceutical CDMO Market Size, Share, Trends, Growth and Forecast 2034

Radiopharmaceutical CDMO Market By Service Type (Contract Manufacturing, Analytical & Quality Control Services, Contract Development and Packaging, Labeling & Logistics), By Radioisotope Type (Fluorine-18, Gallium-68, Technetium-99m, Lutetium-177, Actinium-225 and Others), By Therapeutic Area (Oncology, Neurology, Cardiology and Others), By Application (Diagnostic Radiopharmaceuticals and Therapeutic Radiopharmaceuticals) and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

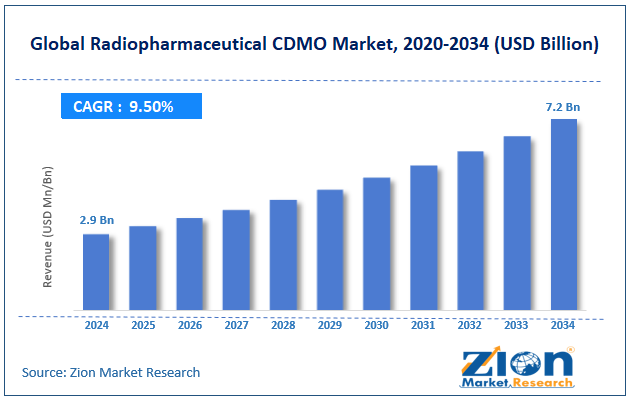

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 2.9 Billion | USD 7.2 Billion | 9.5% | 2024 |

Radiopharmaceutical CDMO Industry Perspective:

What will be the size of the global Radiopharmaceutical CDMO market during the forecast period?

The global Radiopharmaceutical CDMO market size was worth around USD 2.9 billion in 2024 and is predicted to grow to around USD 7.2 billion by 2034 with a compound annual growth rate (CAGR) of roughly 9.5% between 2025 and 2034.

Request Free SampleRequest Free SampleRequest Free Sample

Request Free SampleRequest Free SampleRequest Free Sample

Key Insights

- As per the analysis shared by our research analyst, the global Radiopharmaceutical CDMO market is estimated to grow annually at a CAGR of around 9.5% over the forecast period (2025-2034).

- In terms of revenue, the global Radiopharmaceutical CDMO market size was valued at around USD 2.9 billion in 2024 and is projected to reach USD 7.2 billion by 2034.

- Increasing demand for specialized logistics and distribution is expected to propel the Radiopharmaceutical CDMO market over the projected period.

- Based on the service type, the contract manufacturing segment captures the largest market share in 2024 of over 45%.

- Based on the radioisotope type, the Fluorine-18 segment dominated the market with a highest revenue share in 2024 of 34%.

- Based on the therapeutic area, the oncology segment dominated the market with a highest revenue share in 2024 of over 70%.

- Based on the application, the diagnostic radiopharmaceuticals segment dominated the market with a highest revenue share in 2024 of over 60%.

- Based on region, North America captures the largest market share in 2024 of over 48%.

Radiopharmaceutical CDMO Market: Overview

The radiopharmaceutical CDMO market is an industry comprising third parties that provide services, including research and development, manufacturing, packaging, testing, and distribution of radiopharmaceutical drugs used in nuclear medicine. Radiopharmaceuticals are radioactive substances used for imaging and therapy in oncology, cardiology, and neurology. The main purpose of the collaboration with radiopharmaceutical CDMOs is to obtain specialized services, including radiochemistry, isotopes, regulatory, sterility, and radiation. At present, many factors are driving increased attention to radiopharmaceutical CDMOs, as precision medicine and theranostics using radioactive isotopes for diagnostics and therapy emerge. Collaboration in such conditions leads to more efficient product commercialization and saves money by avoiding the costs of expensive equipment such as a cyclotron, a hot cell, and a radioactive GMP facility. The factors contributing to the growth of the radiopharmaceutical CDMO market include increased demand for PET and SPECT imaging, development of radioligand therapies, innovations in isotope technology, and pharmaceutical outsourcing.

Impact of the USA-Israel War on Iran on the Radiopharmaceutical CDMO Market

In the first place, the controversy between the USA and Israel on one side and Iran on the other is creating significant uncertainty regarding the operations of the CDMO of Radiopharmaceutical due to disruptions in global pharmaceutical logistics, increased shipping costs, and issues related to the source of the isotope. This is because radiopharmaceuticals require prompt delivery, special refrigeration, and radioactive isotopes. Any political instability in the Middle East, particularly around trade routes such as the Strait of Hormuz, can result in delays and increased costs for CDMOs. As a result of this crisis, energy prices, air freight prices, and regulatory concerns are likely to rise, and this may make the processes involved in the production and distribution of nuclear medicines less efficient.

Moreover, sanctions imposed on Iran and conflicts between Iran and other countries can pose challenges to acquiring certain elements required for isotope development or conducting research related to it. Nevertheless, the present controversy may also spur the development of an alternative source of isotope production for research.

Radiopharmaceutical CDMO Market: Dynamics

Growth Drivers

Why does the rising demand for precision oncology drive the Radiopharmaceutical CDMO market?

The increasing demand for precision oncology treatments has driven growth in the Radiopharmaceutical CDMO market, as radiopharmaceuticals enable precise detection and treatment of cancers at the molecular level. The principle behind precision oncology is providing customized treatments for patients based on their tumor biology, and using radiopharmaceuticals in this regard is especially effective because of their selectivity for cancer cells, limiting damage to healthy tissue. This has seen greater usage of radioligand therapy and theranostics for certain types of cancers, such as prostate cancer, neuroendocrine cancer, and metastatic cancer.

With the rapid development of new target therapies by pharmaceutical and biotech organizations, there has been an increasing need to outsource for the development of radioligands, procurement of isotopes, GMP manufacturing, fill-finish procedures, and logistics management. The highly specialized nature of radiopharmaceutical production has led to a marked increase in outsourcing, driven by expanding drug pipelines for precision oncology treatments.

Restraints

How do the high capital investment requirements hinder the growth of the Radiopharmaceutical CDMO industry?

The need for high initial investments poses an obstacle to the expansion of the Radiopharmaceutical CDMO market, as setting up and running a radiopharmaceutical production plant requires costly infrastructure, technologies, and safety systems. To start operations, CDMOs should invest heavily in installing cyclotrons, nuclear reactors, hot cells, shielded cleanrooms, automated synthesizers, radiation measurement systems, and GMP-sterile drug production facilities. Furthermore, a significant portion of the budget should be allocated to regulatory compliance, radioactive waste disposal, employee education, and radiation protection programs. Such high expenses pose substantial obstacles to market entry and hinder small players from increasing production capacity. This issue delays facility construction and geographical expansion, which may lead to production shortages and scarcity of isotopes in the market. Thus, only a few financially powerful companies can become market players, limiting the industry's expansion in the Radiopharmaceutical CDMO market.

Opportunities

How do the rising expansion activities of key market players create a lucrative opportunity for the Radiopharmaceutical CDMO market?

The rising expansion activities by the key market players are expected to offer a lucrative opportunity to the Radiopharmaceutical CDMO Market. For instance, in April 2026, under a deal worth up to $4.3 billion, Regeneron Pharmaceuticals seeks to diversify its product pipeline by entering radiopharmaceuticals through a joint venture with Telix Pharmaceuticals to develop and commercialize new precision oncology products and diagnostic tools. In the agreement, both firms have committed to collaborating on the development of new generations of radiopharmaceutical products for up to eight solid tumor targets selected from Regeneron's antibody library, created using its proprietary VelocImmune® technology and based on its mouse model with a genetically humanized immune system.

Challenges

Limited skilled workforce poses a significant challenge to the Radiopharmaceutical CDMO market?

A lack of a competent workforce impedes the development of the Radiopharmaceutical CDMO market due to the expertise required in the industry. Expertise in fields such as radiochemistry, nuclear medicine, radiation protection, sterile pharmaceutical production, and regulatory affairs is important for the production of radioactive products. However, there is a worldwide shortage of such professionals, and CDMOs therefore find it difficult to enhance their capacity and infrastructure to respond to the growing demand for radiopharmaceuticals. Training professionals to work with radioactive materials poses another challenge, as considerable investment will be required. These constraints have been instrumental in slowing down the development of the Radiopharmaceutical CDMO market.

Radiopharmaceutical CDMO Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Radiopharmaceutical CDMO Market |

| Market Size in 2024 | USD 2.9 Billion |

| Market Forecast in 2034 | USD 7.2 Billion |

| Growth Rate | CAGR of 9.5% |

| Number of Pages | 228 |

| Key Companies Covered | ABX advanced biochemical compounds, Cardinal Health Nuclear & Precision Health Solutions, AtomVie Global Radiopharma, Cyclotek, Curium, Eckert & Ziegler Radiopharma, Evergreen Theragnostics, Isotopia Molecular Imaging, ITM Isotope Technologies Munich, Jubilant Radiopharma, Nihon Medi-Physics, Minerva Imaging, NorthStar Medical Radioisotopes, Nucleus RadioPharma, Monrol, SpectronRx, PharmaLogic, SOFIE and Siemens Healthineers PETNET Solutions, and others. |

| Segments Covered | By Service Type, By Radioisotope Type, By Therapeutic Area, By Application, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Radiopharmaceutical CDMO Market: Segmentation

Service Type Insights

Why does the contract manufacturing dominate the Radiopharmaceutical CDMO market?

The contract manufacturing segment captures the largest market share in 2024 of over 45%. This growth is driven by the rising trend of outsourcing radiopharmaceutical manufacturing to pharmaceutical and biotechnology firms. Radiopharmaceutical manufacturing requires sophisticated facilities, such as cyclotrons, hot cells, shielding clean rooms, and sterile production facilities, that conform to Good Manufacturing Practices guidelines. Most drug discovery and development organizations find it easier to partner with radiopharmaceutical manufacturers through contract manufacturing to save on cost while also achieving regulatory compliance.

Radioisotope Type Insights

How does the Fluorine-18 segment capture the largest market share in the Radiopharmaceutical CDMO market?

The Fluorine-18 segment dominated the market with a highest revenue share in 2024 of 34%. This growth can be attributed to the widespread use of fluorine-18 in PET scans, as well as its importance in the diagnosis and treatment of cancers, neurological disorders, and heart ailments. Some advantages of fluorine-18 include a moderate half-life of approximately 110 minutes, good imaging, and good radiolabeling. Thus, it becomes one of the most commonly employed isotopes for diagnostic radiopharmaceuticals. The rise in cases of cancer and neurological disorders necessitates more PET scans.

Therapeutic Area Insights

How does the oncology segment capture the largest market share in the Radiopharmaceutical CDMO market?

The oncology segment dominated the market with a highest revenue share in 2024 of over 70%. This development is mainly driven by the growing use of radiopharmaceuticals for cancer diagnosis and treatment. Due to the growing prevalence of cancer cases, including prostate cancer, breast cancer, neuroendocrine tumors, and metastasis, there has been an increased need for precision oncology treatments that can help detect and treat cancer with little impact on other body parts. Radiopharmaceutical products used in oncology include PET scans and radioligand therapy. With the adoption of these drugs increasing, pharmaceutical manufacturers have been forced to manufacture radiopharmaceuticals for oncology, thereby boosting demand for CDMOs.

Application Insights

How does the diagnostic radiopharmaceuticals segment capture the largest market share in the Radiopharmaceutical CDMO market?

The diagnostic radiopharmaceuticals segment dominated the market with a highest revenue share in 2024 of over 60%. This growth can be attributed to the growing need for molecular imaging and early disease detection worldwide. Diagnostic radiopharmaceuticals are widely used in PET and SPECT imaging to diagnose cancers, cardiovascular diseases, neurodegenerative diseases, and many other chronic conditions. With the rising incidence of these diseases and the increasing awareness about early and accurate diagnosis, there is an increased usage of nuclear medicine globally. Moreover, the rise of personalized and precision medicine has driven demand for targeted radiopharmaceuticals, such as those labeled with Fluorine-18, Gallium-68, and Technetium-99m. The pharmaceutical and biotech industries have been outsourcing their diagnostic radiopharmaceutical development and manufacturing to CDMOs because radiopharmaceutical production is complex and requires specialized facilities.

Regional Insights

Why does North America lead the Radiopharmaceutical CDMO market?

North America captures the largest market share in 2024 of over 48%. The regional expansion is owing to the presence of major players and increasing number of agreements in the area. For instance, in November 2024, Clarity Pharmaceuticals, an Australian clinical stage radiopharmaceutical company with a mission to develop next generation products that deliver superior treatment outcomes for children and adults with cancer, is pleased to announce it has executed a Material Supply Agreement and Clinical Manufacturing Agreement for 67Cu-SAR-bisPSMA, with Nucleus RadioPharma, an innovative contract development and manufacturing organisation (CDMO) focused on the radiopharmaceutical industry who are dedicated to the development and manufacturing of targeted radiotherapies. This follows the earlier execution of the Material Supply Agreement and Clinical Supply Agreements with NorthStar for the manufacture of 67Cu-SAR-bisPSMA 1 and, in addition to building Clarity’s supply chain capacity in advance of a Phase III trial and commercialization, will facilitate the distribution of the product throughout all 50 states in the US. Nucleus RadioPharma’s Minnesota facility will be used to manufacture and distribute 67Cu-SAR-bisPSMA, and their recent expansion plans to build additional manufacturing capacity in Arizona and Pennsylvania are also consistent with the timelines for development of Clarity’s 67Cu-SAR-bisPSMA product.

Radiopharmaceutical CDMO Market: Competitive Analysis

The global Radiopharmaceutical CDMO market is dominated by players like:

- ABX advanced biochemical compounds

- Cardinal Health Nuclear & Precision Health Solutions

- AtomVie Global Radiopharma

- Cyclotek

- Curium

- Eckert & Ziegler Radiopharma

- Evergreen Theragnostics

- Isotopia Molecular Imaging

- ITM Isotope Technologies Munich

- Jubilant Radiopharma

- Nihon Medi-Physics

- Minerva Imaging

- NorthStar Medical Radioisotopes

- Nucleus RadioPharma

- Monrol

- SpectronRx

- PharmaLogic

- SOFIE and Siemens Healthineers PETNET Solutions

The global Radiopharmaceutical CDMO market is segmented as follows:

By Service Type

- Contract Manufacturing

- Analytical & Quality Control Services

- Contract Development

- Packaging, Labeling & Logistics

By Radioisotope Type

- Fluorine-18

- Gallium-68

- Technetium-99m

- Lutetium-177

- Actinium-225

- Others

By Therapeutic Area

- Oncology

- Neurology

- Cardiology

- Others

By Application

- Diagnostic Radiopharmaceuticals

- Therapeutic Radiopharmaceuticals

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table Of Content

Methodology

FrequentlyAsked Questions

The radiopharmaceutical CDMO market is an industry comprising third parties that provide services, including research and development, manufacturing, packaging, testing, and distribution of radiopharmaceutical drugs used in nuclear medicine.

The key growth drivers for the Radiopharmaceutical CDMO market include rising demand for precision oncology and theranostics, increasing adoption of PET and SPECT imaging, expanding radioligand therapy pipelines, growing outsourcing by pharmaceutical companies, advancements in isotope production technologies, and increasing investments in nuclear medicine infrastructure.

The major challenges restraining the growth of the Radiopharmaceutical CDMO market include high capital investment requirements, limited availability of critical radioisotopes, complex regulatory compliance, short isotope half-lives, radiation safety concerns, shortage of skilled professionals, high operational costs, and logistical challenges associated with time-sensitive transportation and cold-chain distribution.

Based on the application, the diagnostic radiopharmaceuticals segment is expected to dominate the Radiopharmaceutical CDMO market growth during the projected period.

Emerging trends and innovations impacting the Radiopharmaceutical CDMO market include the expansion of theranostics and radioligand therapies, advancements in cyclotron and isotope production technologies, increasing use of AI-driven radiopharmaceutical development, growth of Actinium-225 and Lutetium-177 therapies, automation in radiochemistry manufacturing, and rising investments in decentralized nuclear medicine production facilities.

According to the report, the global Radiopharmaceutical CDMO market size was worth around USD 2.9 billion in 2024 and is predicted to grow to around USD 7.2 billion by 2034.

The global Radiopharmaceutical CDMO market is expected to grow at a CAGR of 9.5% during the forecast period.

The global Radiopharmaceutical CDMO industry growth is expected to be led by North America over the forecast period.

The global Radiopharmaceutical CDMO market is dominated by players like ABX advanced biochemical compounds, Cardinal Health Nuclear & Precision Health Solutions, AtomVie Global Radiopharma, Cyclotek, Curium, Eckert & Ziegler Radiopharma, Evergreen Theragnostics, Isotopia Molecular Imaging, ITM Isotope Technologies Munich, Jubilant Radiopharma, Nihon Medi-Physics, Minerva Imaging, NorthStar Medical Radioisotopes, Nucleus RadioPharma, Monrol, SpectronRx, PharmaLogic, SOFIE and Siemens Healthineers PETNET Solutions among others.

The market report covers the geographical market along with a comprehensive competitive landscape analysis. It also includes cash flow analysis, profit ratio analysis, market basket analysis, market attractiveness analysis, sentiment analysis, PESTLE analysis, trend analysis, SWOT analysis, trade area analysis, demand & supply analysis, Porter’s five forces analysis, and value chain analysis.

HappyClients