Natural And Manufactured Sand Market Size, Share, Trends, Growth 2034

Natural And Manufactured Sand Market By Product Type (Natural Sand, Manufactured Sand), By Application (Concrete, Brick Manufacturing, Road Base & Pavement), By End Use Industry (Construction, Manufacturing, Infrastructure), and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 179.36 Billion | USD 407.43 Billion | 10.80% | 2024 |

Natural And Manufactured Sand Industry Perspective:

What will be the size of the global natural and manufactured sand market during the forecast period?

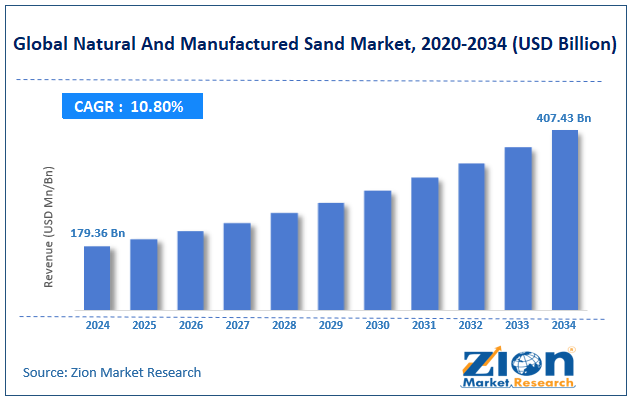

The global natural and manufactured sand market size was around USD 179.36 billion in 2024 and is projected to reach USD 407.43 billion by 2034, with a compound annual growth rate (CAGR) of roughly 10.80% between 2025 and 2034.

Request Free SampleRequest Free SampleRequest Free Sample

Request Free SampleRequest Free SampleRequest Free Sample

Key Insights:

- As per the analysis shared by our research analyst, the global natural and manufactured sand market is estimated to grow annually at a CAGR of around 10.80% over the forecast period (2025-2034)

- In terms of revenue, the global natural and manufactured sand market size was valued at around USD 179.36 billion in 2024 and is projected to reach USD 407.43 billion by 2034.

- The natural and manufactured sand market is projected to grow significantly, driven by infrastructure development projects, rising demand for cement and concrete, and environmental regulations on sand mining.

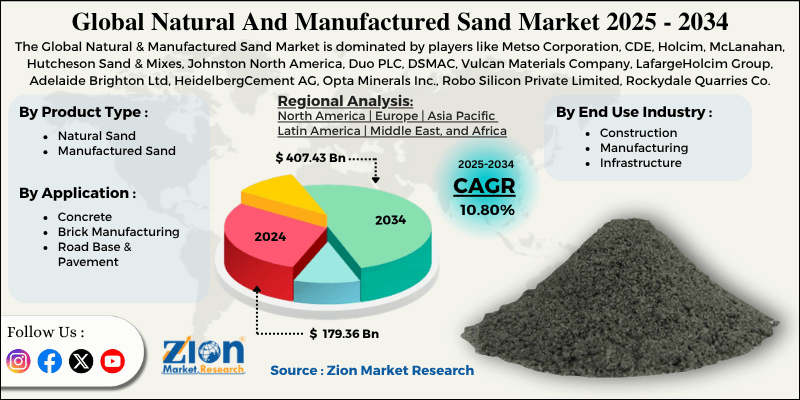

- Based on product type, the manufactured sand segment is expected to lead the market, while the natural sand segment is expected to grow considerably.

- Based on application, the concrete segment is the dominating segment, while the brick manufacturing segment is projected to witness sizeable revenue over the forecast period.

- Based on end-use industry, the construction segment is expected to lead the market, followed by the infrastructure segment.

- Based on region, the Asia Pacific is projected to dominate the global market during the estimated period, followed by North America.

Natural And Manufactured Sand Market: Overview

Natural sand is procured from natural deposits or riverbeds and typically has rounded, smooth particles formed by erosion over time. M-sand, or manufactured sand, is artificially produced by crushing stone or rock, resulting in angular particles with controlled grading. Though natural sand is limited and can harm ecosystems when used for prolonged periods, M-sand is more consistent in quality, sustainable, and widely used in modern construction. The global natural and manufactured sand market is poised to expand rapidly, driven by rapid urbanization and population growth, infrastructure development projects, and the depletion of natural sand reserves. The growing global population and urban expansion are driving large-scale commercial and residential construction. This majorly drives demand for sand as a core construction material. Developing nations are primarily driving sustained consumption growth.

Moreover, abundant investment in bridges, highways, smart cities, and railways is increasing global demand for sand. Governments are prioritizing infrastructure modernization to support economic development. This creates continuous demand for manufactured and natural sand. Furthermore, excessive mining has reduced the availability of natural sand and rivers in several regions. This scarcity raises costs and shifts demand towards alternatives. Manufactured sand emerges as a reliable substitute.

Despite growth, the global market is constrained by factors such as the environmental impact of sand production and high capital investment requirements. Natural sand mining causes erosion, ecological imbalance, and habitat destruction. Manufactured sand production also generates noise and dust and consumes energy. These concerns lead to compliance costs and regulatory restrictions. Similarly, setting up sand plants needs major investment in infrastructure and machinery. This creates barriers for medium and small enterprises. High initial costs hamper market growth and entry.

Nonetheless, the global natural and manufactured sand industry stands to benefit from several key opportunities, including growth in infrastructure investments and the development of high-performing concrete. Large-scale private and public investments create long-term demand for sand. Projects such as transport corridors and smart cities require high-quality materials, creating opportunities for sustained market growth. Advanced construction techniques require durable, high-strength concrete. Manufactured sand can be customized for specific performance needs. This creates niche product opportunities.

Natural And Manufactured Sand Market: Dynamics

Growth Drivers

How is the growth of the construction industry and RMC demand augmenting the natural and manufactured sand market?

The worldwide construction industry remains the backbone of demand for sand, mainly for concrete and mortar production. Sand is a vital input in ready-mix concrete (RMC), which is increasingly adopted worldwide. Growing residential and commercial activity continues to push sand consumption upward. Infrastructure and industrial construction further amplify bulk demand. This propeller is essential, as almost all construction activities depend largely on sand availability. Hence, these factors ultimately fuel the growth of the natural and manufactured sand market.

How are environmental regulations and mining restrictions positively impacting the natural and manufactured sand market development?

Stringent regulations on river sand mining are hampering supply and increasing dependency on alternatives. Governments are imposing seasonal restrictions and bans to protect ecosystems and prevent illegal mining. These restrictions have led to supply scarcities and price variations in most regions. Environmental concerns, such as water pollution and habitat destruction, are major policy drivers. Hence, regulatory pressure is indirectly accelerating the advancement and adoption of sustainable sand sources.

Restraints

Market resistance to manufactured sand adoption unfavorably impacts the market progress

Despite its benefits, manufactured sand witnesses resistance from builders and contractors who prefer natural sand. Concerns regarding workability, long-term performance, and strength slow its adoption. The lack of technical knowledge and awareness further contributes to hesitation among end consumers. Unstable quality standards in regions also create trust issues in the market. This resistance delays the transition towards more sustainable sand choices.

Opportunities

How are recycling and circular-economy integration presenting favorable prospects for the expansion of the natural and manufactured sand market?

The integration of recycling practices into construction is offering new opportunities for sand production. Demolition and construction waste can be processed into recycled sand, reducing reliance on natural resources. Organizations and governments are promoting circular-economy initiatives to reduce waste. This approach not only supports sustainability but also offers fresh revenue streams for vendors of the natural and manufactured sand industry. Recycled sand is gradually gaining prominence as a practical alternative in construction.

Challenges

High energy consumption in production restricts the market growth

Manufactured sand production is an energy-intensive process that involves crushing and processing rocks. Growing energy costs elevate overall production expenses and lower profit margins. Furthermore, high energy consumption contributes to carbon emissions and environmental concerns. This creates pressure on producers to adopt more energy-efficient solutions. Balancing cost efficiency with sustainability is still a key operational challenge.

Request Free SampleRequest Free SampleRequest Free Sample

Request Free SampleRequest Free SampleRequest Free Sample

Natural And Manufactured Sand Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Natural And Manufactured Sand Market |

| Market Size in 2024 | USD 179.36 Billion |

| Market Forecast in 2034 | USD 407.43 Bllion |

| Growth Rate | CAGR of 10.80% |

| Number of Pages | 228 |

| Key Companies Covered | Metso Corporation, CDE, Holcim, McLanahan, Hutcheson Sand & Mixes, Johnston North America, Duo PLC, DSMAC, Vulcan Materials Company, LafargeHolcim Group, Adelaide Brighton Ltd, HeidelbergCement AG, Opta Minerals Inc., Robo Silicon Private Limited, Rockydale Quarries Corporation, and others. |

| Segments Covered | By Product Type, By Application, By End Use Industry, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Natural And Manufactured Sand Market: Segmentation

The global natural and manufactured sand market is segmented based on product type, application, end-use industry, and region.

Why is the Manufactured Sand segment projected to dominate the natural and manufactured sand market?

Based on product type, the global natural and manufactured sand industry is divided into natural sand and manufactured sand. Manufactured sand accounts for a dominant 60% of the total market. Its dominance is supported by environmental regulations and bans on river sand mining, which limit the availability of natural sand. M-sand offers consistent particle size, suitability, and better workability for high-performance concrete. Speedy urbanization and the need for sustainable construction have further strengthened its leadership worldwide.

Nonetheless, natural sand ranks second with 45% market share. It is widely used due to its minimal processing requirements and traditional acceptance. Yet stringent mining restrictions and the depletion of riverbeds are hampering its availability in most regions. Its use is now concentrated in areas with less regulatory pressure, while manufactured sand steadily gains market share.

What factors help the Concrete segment lead the natural and manufactured sand market?

Based on application, the global natural and manufactured sand market is segmented into concrete, brick manufacturing, and road base & pavement. The concrete segment leads the market with 55% market share. This is backed by the large-scale commercial, residential, and infrastructure construction projects worldwide. Both manufactured and natural sand are widely used in concrete production due to their vital roles in durability and strength.

Conversely, the brick manufacturing holds a second-leading position in the market. Sand is a vital component in most masonry products and clay brick products, offering structural stability and texture. The segment continues to grow substantially, especially in regions with expanding industrial and residential construction.

What are the key reasons for the leadership of the Construction segment in the natural and manufactured sand market?

Based on end-use industry, the global market is segmented into construction, manufacturing, and infrastructure. The construction segment captures nearly 60% of the market. Sand is a crucial component in the production of mortar, concrete, and masonry materials used in commercial and residential buildings. Speedy urbanization and surging housing demand continue to fuel strong consumption in the domain.

However, the infrastructure segment holds the second-largest market share with nearly 30%. Sand is extensively used in bridges, roads, public works projects, and highways, offering durability and structural stability. Government-led investments in urban development projects and transportation projects are driving demand in the segment.

Natural And Manufactured Sand Market: Regional Analysis

Why is Asia Pacific outperforming other regions in the global Natural And Manufactured Sand market?

Asia Pacific is anticipated to retain its leading role in the global natural and manufactured sand market, with a 6-7% CAGR, driven by speedy urbanization and population growth, large-scale infrastructure development, and adoption of manufactured sand (M-sand). APAC holds some of the fastest-growing urban populations worldwide, especially in economies like India and China. This fuels ample demand for commercial and residential construction, directly driving sand consumption. Speedy urban growth continues to sustain the region’s market leadership. Massive infrastructure projects, including bridges, highways, smart cities, and metro systems, require large quantities of sand for road and concrete construction.

Public investment programs and government-led initiatives drive this demand. These projects make the region the leading end-user worldwide. Furthermore, environmental regulations and depletion of river sand have augmented the adoption of manufactured sand in APAC. M-sand offers consistent quality and meets modern construction standards, mainly for high-performing concrete. Its rapid acceptance strengthens its dominance in the global sand market.

Why does North America rank second in the global Natural And Manufactured Sand Market?

North America ranks as the second-largest region in the global natural and manufactured sand industry, with a 3-4% CAGR, driven by strong infrastructure and construction industry, high adoption of M-sand, and commercial and industrial development. North America holds a well-established infrastructure and construction sector, comprising commercial, residential, and industrial projects. Constant expansion and renovation of urban areas fuel steady demand for sand. This strong construction activity keeps the region a key market for manufactured and natural sand. Sustainability goals and environmental regulations have promoted the use of M-sand over natural sand. Manufactured sand promises consistent quality and supports high-performance concrete applications. Its adoption in construction projects strengthens North America’s rank in the worldwide market.

Additionally, the expansion of industrial parks, logistics hubs, and commercial complexes requires large quantities of sand for mortar, road, and concrete construction. Current industrial and urban projects create a stable consumption base. This fuels sustained demand for the region's sands.

Natural And Manufactured Sand Market: Competitive Analysis

The leading players in the global natural and manufactured sand market are:

- Metso Corporation

- CDE

- Holcim

- McLanahan

- Hutcheson Sand & Mixes

- Johnston North America

- Duo PLC

- DSMAC

- Vulcan Materials Company

- LafargeHolcim Group

- Adelaide Brighton Ltd

- HeidelbergCement AG

- Opta Minerals Inc.

- Robo Silicon Private Limited

- Rockydale Quarries Corporation

What are the key trends in the global Natural and Manufactured Sand Market?

Technological advancements in sand processing:

Advancements in screening, crushing, automation, and washing technologies are transforming sand production. Advanced equipment enables producers to produce high-quality manufactured sand with an enhanced particle-size distribution. These innovations reduce waste, enhance efficiency, and lower production costs. Technology adoption is becoming a key differentiator for the suppliers of competitive sand worldwide.

Digitalization and smart supply chain practices:

Data analytics and digital platforms are actively used to optimize supply chains, from quarrying to delivery. Real-time tracking, inventory management systems, and demand forecasting are enhancing logistics efficiency. This digital transformation helps reduce delays, improve customer service, and cut costs. Smart supply chains are increasingly crucial as demand becomes more just-in-time oriented and fragmented.

The global natural and manufactured sand market is segmented as follows:

By Product Type

- Natural Sand

- Manufactured Sand

By Application

- Concrete

- Brick Manufacturing

- Road Base & Pavement

By End Use Industry

- Construction

- Manufacturing

- Infrastructure

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table Of Content

Methodology

FrequentlyAsked Questions

List of Contents

Natural And Manufactured SandIndustry Perspective:Key Insights:OverviewDynamicsReport ScopeSegmentationRegional AnalysisCompetitive AnalysisWhat are the key trends in the global Natural and Manufactured Sand Market?The global natural and manufactured sand market is segmented as follows:HappyClients