Heavy Equipment Components and Parts Market Size and Forecast 2034

Heavy Equipment Components and Parts Market By Equipment Type (Excavators, Bulldozers, Loaders, Crushers, Dump Trucks, Backhoes, Graders, and Others), By Component Type (Engine Parts, Hydraulic Components, Transmission Parts, Undercarriage Parts, Electrical Components, Wear and Tear Parts, and Others), By Application (Construction, Mining, Agriculture, Forestry, Infrastructure, and Others), and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

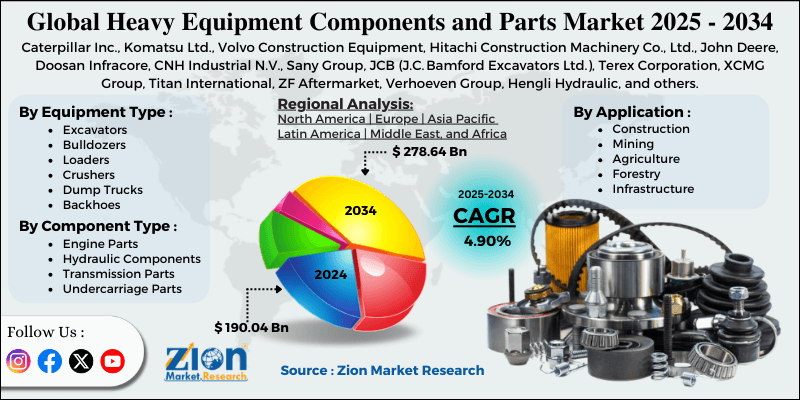

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 190.04 Billion | USD 278.64 Billion | 4.90% | 2024 |

Heavy Equipment Components and Parts Industry Perspective:

What will be the size of the global heavy equipment components and parts market during the forecast period?

The global heavy equipment components and parts market size was around USD 190.04 billion in 2024 and is projected to reach USD 278.64 billion by 2034, with a compound annual growth rate (CAGR) of roughly 4.90% between 2025 and 2034.

Request Free SampleRequest Free Sample

Request Free SampleRequest Free Sample

Key Insights:

- As per the analysis shared by our research analyst, the global heavy equipment components and parts market is estimated to grow annually at a CAGR of around 4.90% over the forecast period (2025-2034)

- In terms of revenue, the global heavy equipment components and parts market size was valued at around USD 190.04 billion in 2024 and is projected to reach USD 278.64 billion by 2034.

- The heavy equipment components and parts market is projected to grow significantly owing to the rising construction and mining activities, increasing demand for automation and IoT-enabled equipment, and replacement and aftermarket demand.

- Based on equipment type, the excavators segment is expected to lead the market, while the loaders segment is expected to grow considerably.

- Based on component type, the engine parts segment is the largest, while the hydraulic components segment is projected to record sizeable revenue over the forecast period.

- Based on application, the construction segment is expected to lead the market, followed by the mining segment.

- By region, Asia Pacific is projected to dominate the global market during the forecast period, followed by North America.

Heavy Equipment Components and Parts Market: Overview

Heavy equipment components and parts are crucial to ensuring optimal durability, performance, and safety of machinery used in mining, construction, and agriculture. Major parts include hydraulic systems, engines, undercarriages, electrical components, and transmissions, all designed to tolerate harsh conditions and heavy workloads. The global heavy equipment components and parts market is projected to grow substantially, driven by a surge in infrastructure development, the expansion of the mining industry, and technological advancements. The speedy growth of global infrastructure projects has significantly increased the demand for heavy machinery. Replacement parts and reliable components are important for minimizing downtime and keeping these machines operational. This sustained demand has strengthened both the aftermarket and OEM markets worldwide.

Moreover, expanding mining activities in the energy and minerals sectors need more heavy equipment for operations. As machines experience high wear and tear, durable replacement parts become vital to maintain efficiency. This trend has augmented the demand for specialized components and maintenance services. Furthermore, modern heavy equipment increasingly integrates sensors, automation, and IoT technology. These advancements require high-precision, advanced components to function properly. Suppliers and manufacturers are innovating speedily to meet the changing technological needs of operators.

Although drivers exist, the global market is challenged by factors such as supply chain disruptions and rising raw material prices. Shortages of raw materials and delays in logistics may impact the availability of crucial components. Manufacturers experience complexities in meeting demand, which may slow down operations. These disturbances may impact customer satisfaction and industry growth. Similarly, varying prices of aluminum, steel, and alloys raise manufacturing costs for parts. High expenses may force operators to postpone purchases. Suppliers face pressure to maintain profitability while staying competitive.

Even so, the global heavy equipment components and parts industry is well-positioned due to growth in the mining industry and technological advancements. Growing mining activity leads to increased use of heavy equipment. Frequent wear and tear fuels demand for durable replacement parts. Operators may depend on quality components to reduce downtime. Additionally, modern machinery uses sensors, automation, and IoT. These technologies require high-precision, specialized components. Suppliers innovate to meet these changing needs.

Heavy Equipment Components and Parts Market: Dynamics

Growth Drivers

How are aftermarket growth and fleet maintenance driving progress in the heavy equipment components and parts industry?

The aftermarket parts market is progressing as operators favor cost-effective maintenance over full replacement and fleets age. Demand surges for durable components such as undercarriage systems, transmissions, and engine modules. Replacement cycles and downtime reduction drive aftermarket revenue growth faster than sales of new OEM equipment. Improved distribution networks and e-commerce increase worldwide accessibility. This trend strengthens customer retention and long-term growth of the heavy equipment components and parts market.

How is the heavy equipment components and parts market fueled by technological advancement and digitalization?

Heavy equipment is speedily adopting AI diagnostics, IoT sensors, and predictive maintenance, driving efficiency and uptime. This digital shift increases demand for smart and connected components in machinery fleets. Predictive analytics is projected to impact nearly half of aftermarket parts purchases by 2030. Manufacturers now offer modernized hydraulic modules, electronic control units, and engine sensors to meet these requirements. This technological evolution is transforming component design, customer expectations, and value.

Restraints

Regulatory and compliance burdens negatively impact the market progress

Strict environmental safety standards, varying emissions across regions, and frequent redesigns of parts to comply. Manufacturers should absorb regulatory compliance costs, certification, and testing, as these delay time-to-market and affect pricing. Emission regulations, such as the EU and Tier 5 regulations, demand continuous innovation. SMEs usually struggle more with compliance costs than large OEMs. This regulatory complexity restrains wide market growth.

Opportunities

How is electric & sustainable equipment component demand offer advantageous for the growth of the heavy equipment components and parts market?

The shift towards hybrid and electric machinery is creating new component segments, such as electric drive trains, battery modules, thermal management systems, and power electronics. Adoption of environmentally-friendly machinery is growing due to government incentives and corporate ESG commitments. These new parts usually hold higher margins and need specialized engineering. This transition accelerates as infrastructure for electrification grows worldwide. Sustainability mandates, hence, translate into long-term growth for the heavy equipment components and parts industry.

Challenges

Intense competition and price pressure limit the market growth

The market features strong competition among aftermarket and OEM suppliers vying for quality, price, and distribution benefits. This competition compresses margins, especially for commoditized parts, and complicates differentiation. Independent suppliers may struggle to maintain profitability against low-cost substitutes. OEMs usually compete with 3rd-party distributors that focus on faster delivery and lower costs. Sustaining a competitive edge needs continuous branding and innovation.

Request Free SampleRequest Free Sample

Request Free SampleRequest Free Sample

Heavy Equipment Components and Parts Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Heavy Equipment Components and Parts Market |

| Market Size in 2024 | USD 190.04 Billion |

| Market Forecast in 2034 | USD 278.64 Bllion |

| Growth Rate | CAGR of 4.90% |

| Number of Pages | 224 |

| Key Companies Covered | Caterpillar Inc., Komatsu Ltd., Volvo Construction Equipment, Hitachi Construction Machinery Co., Ltd., John Deere, Doosan Infracore, CNH Industrial N.V., Sany Group, JCB (J.C. Bamford Excavators Ltd.), Terex Corporation, XCMG Group, Titan International, ZF Aftermarket, Verhoeven Group, Hengli Hydraulic, and others. |

| Segments Covered | By Equipment Type, By Component Type, By Application, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Heavy Equipment Components and Parts Market: Segmentation

The global heavy equipment components and parts market is segmented based on equipment type, component type, application, and region.

Why is the Excavators segment projected to dominate the heavy equipment components and parts market?

Based on equipment type, the global heavy equipment components and parts industry is divided into excavators, bulldozers, loaders, crushers, dump trucks, backhoes, graders, and others. The excavators segment accounts for a dominant 38% share of the market, driven by broader use in mining and construction. Frequent use fuels elevated demand for hydraulics, engines, and undercarriage parts. Their versatility promises aftermarket and OEM sales.

Conversely, the loaders segment ranks second in the market with a 22% share, due to their major role in site preparation and material handling. Constant operation creates a steady demand for hydraulics, buckets, and transmissions. Their wide range of applications sustains a strong demand for parts.

What factors help the Engine Parts segment lead the heavy equipment components and parts market?

Based on component type, the global heavy equipment components and parts market is segmented into engine parts, hydraulic components, transmission parts, undercarriage parts, electrical components, wear and tear parts, and others. The engine parts segment leads the market with a 35% share. They form the core power system of machinery and require regular replacement due to high operational wear. These parts include pistons, fuel systems, crankshafts, and filters, all of which are crucial for emissions compliance and performance. Consistent demand is backed by frequent servicing cycles and strict performance requirements in mining and construction equipment.

Nonetheless, the hydraulic segment holds the second-largest share in the market at 24%. They are important for digging, lifting, steering, and other power-transmission functions in heavy machines. Parts such as pumps, cylinders, hoses, and valves experience continuous wear and use in excavators, backhoes, and loaders. The growth of IoT-integrated hydraulic systems helps maintain segmental leadership.

What are the key reasons for the leadership of the Construction segment in the heavy equipment components and parts market?

Based on application, the global market is segmented into construction, mining, agriculture, forestry, infrastructure, and others. The construction segment accounts for 42% of the total market due to the extensive use of excavators, graders, and loaders. Frequent operation fuels high demand for maintenance and replacement parts. Ongoing urbanization and infrastructure projects help maintain the segmental dominance.

However, the mining segment ranks second in the market, with a 26% share, driven by the use of heavy equipment in resource and mineral extraction. Harsh conditions accelerate wear, increasing demand for durable components. Continuous mining activities promise steady aftermarket and OEM part consumption.

Heavy Equipment Components and Parts Market: Regional Analysis

What enables Asia Pacific to have a strong foothold in the global Heavy Equipment Components and Parts Market?

Asia Pacific is likely to sustain its leadership in the heavy equipment components and parts market, with a 5-6% CAGR, driven by speedy urbanization and infrastructure growth, booming mining and construction activity, and industrialization and manufacturing growth. APAC’s urban development and infrastructure growth are driving strong demand for heavy machinery. Frequent equipment use increases the need for replacement parts. This consistent activity helps maintain the regional dominance.

Moreover, extensive mining and construction operations need constant equipment use. Harsh conditions accelerate wear, driving demand for aftermarket and OEM components. Continuous utilization reinforces industry dominance. Furthermore, rising industrial hubs increase the deployment of machinery for logistics and production. Continuous use fuels parts replacement and maintenance. Local production and distribution networks support industry growth.

Why does North America rank second in the global Heavy Equipment Components and Parts Market?

North America continues to hold the second-highest share, with a 4-5% CAGR in the heavy equipment components and parts industry, driven by advanced mining, technological improvements in machinery, and well-developed aftermarket services. The region boasts well-developed mining operations for metals, coal, and minerals, which require extensive deployment of machinery. Heavy equipment in these industries experiences significant wear and tear, driving strong demand for durable aftermarket and OEM components. The technical sophistication and scale of mining projects promise ongoing market activity. North American operators swiftly adopt telematics, automation, and IoT-enables equipment. These advanced systems require high-precision, specialized components to maintain reliability and efficiency. Manufacturers continuously innovate to meet the demand for technologically advanced parts.

Additionally, service centers and extensive dealer networks provide operators with speedy access to replacement parts. Aftermarket offerings like extended warranties and maintenance contracts enhance equipment uptime and operational reliability. This support infrastructure strengthens suppliers' recurring revenue.

Heavy Equipment Components and Parts Market: Competitive Analysis

The leading players in the global heavy equipment components and parts market are:

- Caterpillar Inc.

- Komatsu Ltd.

- Volvo Construction Equipment

- Hitachi Construction Machinery Co. Ltd.

- John Deere

- Doosan Infracore

- CNH Industrial N.V.

- Sany Group

- JCB (J.C. Bamford Excavators Ltd.)

- Terex Corporation

- XCMG Group

- Titan International

- ZF Aftermarket

- Verhoeven Group

- Hengli Hydraulic

What are the key trends in the global Heavy Equipment Components and Parts Market?

Growth of aftermarket services and extended warranties:

Operators are increasingly investing in aftermarket services, comprising extended warranties and maintenance contracts. This promises equipment longevity, enhances operational efficiency, and reduces downtime. Suppliers are expanding service offerings alongside components to capture recurring value. The aftermarket segment is becoming a main propeller of the overall industry.

Increasing use of durable and wear-resistant components:

Harsh operating conditions in mining, construction, and industrial applications demand high-strength, wear-resistant parts. Manufacturers are developing advanced coatings and materials to enhance component life. This trend reduces replacement frequency while supporting higher performance. Demand for quality wear parts continues to rise in equipment types and regions.

The global heavy equipment components and parts market is segmented as follows:

By Equipment Type

- Excavators

- Bulldozers

- Loaders

- Crushers

- Dump Trucks

- Backhoes

- Graders

- Others

By Component Type

- Engine Parts

- Hydraulic Components

- Transmission Parts

- Undercarriage Parts

- Electrical Components

- Wear and Tear Parts

- Others

By Application

- Construction

- Mining

- Agriculture

- Forestry

- Infrastructure

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table Of Content

Methodology

FrequentlyAsked Questions

HappyClients