Wearable Medical Device Market Size, Share & Forecast 2026–2034

Wearable Medical Device Market Size, Share, Trends, By Device Type (Diagnostic Devices, Therapeutic Devices, Drug Delivery Devices), By Application (Remote Patient Monitoring, Sports & Fitness, Home Healthcare, Chronic Disease Management), By End User (Hospitals & Clinics, Homecare Settings, Sports & Fitness Centres, Research Institutions), By Connectivity Technology (Bluetooth, Wi-Fi, NFC, Cellular), By Region, and Forecast 2026 - 2034

| Market Size in 2025 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 34,120 Million | USD 148,640 Million | 17.7% | 2025 |

Wearable Medical Device Market: Industry Perspective

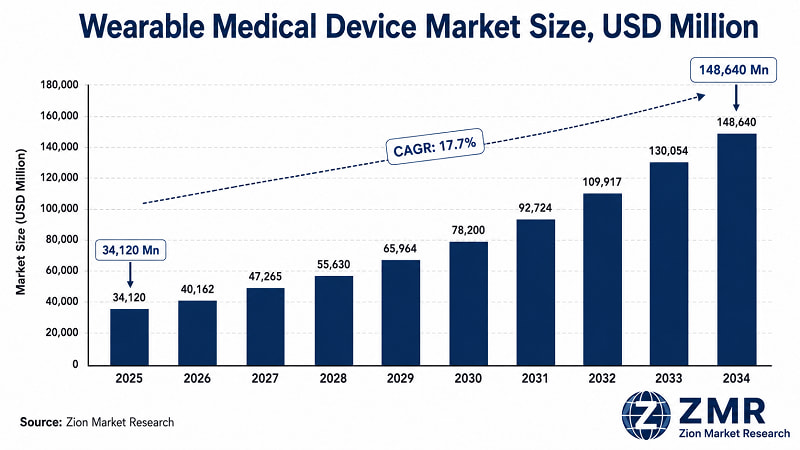

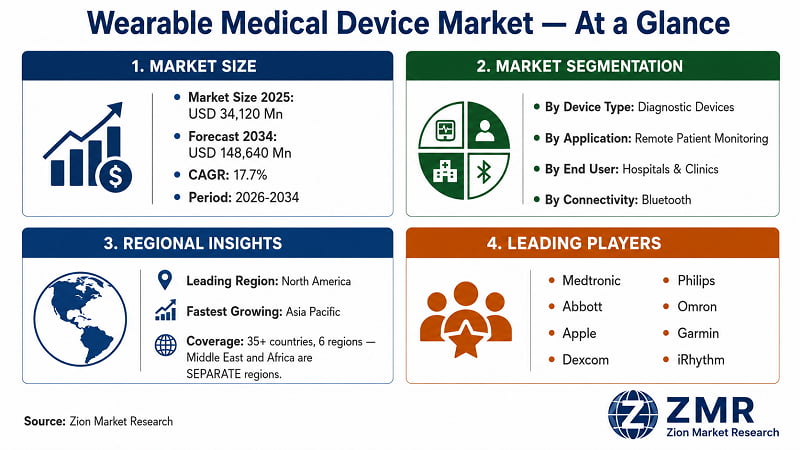

- The Global Wearable Medical Device market reached USD 34,120 Million in 2025 and is forecast to expand to USD 148,640 Million by 2034 at a 17.7% CAGR. This isn't speculative growth — it's demand-pull from three structural forces converging simultaneously: 537 million adults with diabetes, 1.28 billion with hypertension, and health systems globally under acute cost pressure to move monitoring from hospitals to the home.

- Reimbursement infrastructure in the U.S. and EU has moved from experimental to mainstream.

- The clinical evidence base has crossed the formulary adoption threshold. Zion Market Research identifies a market entering its volume phase — not its discovery phase.

Request Free SampleRequest Free Sample

Request Free SampleRequest Free Sample

Wearable Medical Device Market: Overview

- The Wearable Medical Device market encompasses body-worn electronic systems designed for clinical or clinically adjacent use — continuous glucose monitors, cardiac event monitors, smartwatch-based ECG devices, wearable blood pressure monitors, neurostimulation wearables, and connected drug delivery systems. The market's scope explicitly excludes general consumer wellness wearables without regulatory clearance, though this boundary is narrowing as consumer platforms achieve FDA and CE approvals.

- The value chain operates across three tiers. Foundational providers — Texas Instruments, STMicroelectronics, and Analog Devices — supply core sensing and processing components. Specialist developers — Medtronic, Abbott, Dexcom, and iRhythm — integrate these into clinically validated, regulatory-cleared device platforms. Application-layer specialists — Apple, Samsung, and Garmin — build the data ecosystems, AI analytics layers, and care coordination software that convert raw biometric streams into clinical decision support.

- For procurement and investment decision-makers, the question is not whether the Wearable Medical Device market will grow — that question is settled — but which segments, geographies, and deployment models will capture disproportionate value within that growth. This report provides sub-segment level data, country-level forecasts, and competitive positioning analysis across 4 segmentation dimensions and 35+ geographies.

Key Insights

- Global CAGR: 17.7%, growing from USD 34,120 Mn (2025) to USD 148,640 Mn (2034). Source: Zion Market Research.

- Diagnostic Devices: largest device-type share at ~43% in 2025, led by CGMs and cardiac monitors.

- Therapeutic Devices: fastest-growing sub-segment at ~21% CAGR through 2034 — neurostimulation and drug delivery.

- Remote Patient Monitoring: dominant application at ~35% revenue share in 2025, supported by CMS reimbursement.

- Homecare Settings: fastest-growing end-user segment as hospital-at-home models scale globally.

- North America: ~38% regional revenue share in 2025, underpinned by FDA and CMS infrastructure.

- Asia Pacific: highest regional CAGR at ~19.8% through 2034 — China, India, Japan, South Korea.

- Competitive differentiation has shifted from hardware accuracy to AI analytics depth and EHR integration capability.

- Bluetooth dominates connectivity at ~55% share; cellular wearables grow fastest in rural/emerging-market deployments.

Why Choose the Zion Market Research Wearable Medical Device Market Report?

Decision-makers comparing market intelligence reports on Wearable Medical Devices will find the Zion Market Research report differentiated on the following dimensions.

|

Dimension |

Zion Market Research Report |

Industry Average |

|

Report Pages |

300+ |

~120 pages |

|

Forecast Horizon |

9 years (2026–2034) |

7 years |

|

Segmentation Dimensions |

4 dimensions |

4–5 dimensions |

|

Historical Data |

6 years (2019–2024) |

4–5 years |

|

Country Coverage |

35+ countries |

15–18 countries |

|

Companies Profiled |

15 companies |

10 companies |

|

DROC Framework |

Full (Drivers, Restraints, Opportunities, Challenges) |

Drivers only |

For custom scope — additional segments, specific geographies, or extended forecast periods — contact sales@zionmarketresearch.com

Wearable Medical Device Market: Dynamics (Drivers, Restraints, Opportunities, Challenges)

Request Free SampleRequest Free Sample

Request Free SampleRequest Free Sample

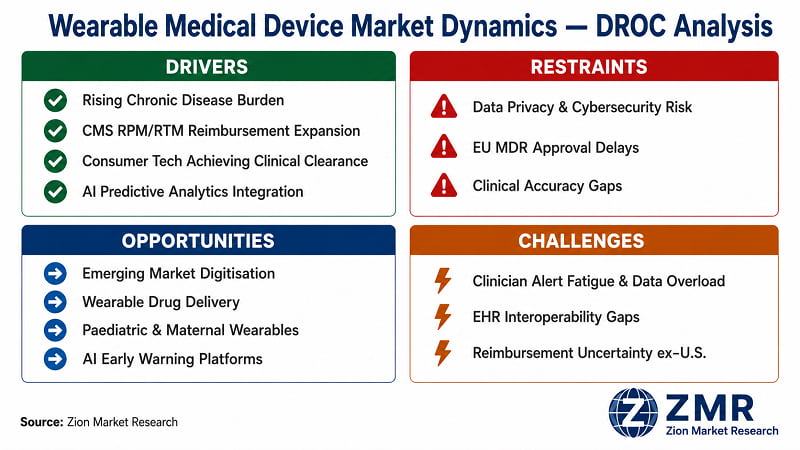

What Is Driving the Wearable Medical Device Market?

- Chronic Disease Epidemic Requiring Continuous Monitoring:

The IDF reports 537 million adults with diabetes globally (2025), projected to reach 783 million by 2045. WHO estimates 1.28 billion adults have hypertension. These patient populations require daily or continuous biometric monitoring that episodic clinic visits cannot fulfil. Abbott Laboratories deployed FreeStyle Libre across 58 countries, reaching 5+ million users and exceeding USD 5.3 billion in annual CGM revenue by 2024 — proving the scale achievable when device reimbursement aligns with clinical need. U.S., EU, Japan, and Australian regulatory agencies are updating clinical guidelines to recommend CGMs as first-line monitoring tools, creating a regulatory tailwind pulling procurement.

- CMS Reimbursement and Value-Based Care Architecture:

CMS expansion of remote physiologic monitoring (CPT 99453–99458) and remote therapeutic monitoring (CPT 98975–98980) codes from 2022 has restructured the commercial model for hospital wearable deployment. Best Buy Health deployed hospital-at-home monitoring platforms to 30+ U.S. health systems by 2023 via its Current Health acquisition, reporting 40% reductions in unnecessary emergency visits. Germany's DiGA pathway approved 50+ digital health applications by 2024, creating a parallel European commercial runway.

- Consumer Technology Achieving Clinical Regulatory Clearance:

Apple's FDA clearances for AFib history, AFib detection, and irregular rhythm notification — and ECG app clearance in 50+ countries — represents a structural market inflection. Consumer platforms with hundreds of millions of installed devices now deliver clinical-grade cardiac monitoring below USD 500 per unit. iRhythm Technologies processed over 4 million Zio Patch cardiac analyses by 2024. This expands the TAM and creates volume-value split pressure on traditional cardiac monitor manufacturers.

- AI and Predictive Analytics Integration:

On-device and cloud AI models for predictive health scoring — early warning of heart failure decompensation, hypoglycaemia prediction, sleep apnoea scoring — convert wearables from monitoring tools to clinical decision-support systems. Medtronic's March 2025 partnership with Google Cloud targets AI-enhanced predictive algorithms across its wearable cardiac and diabetes platforms. Health systems increasingly evaluate AI analytics capability as the primary procurement criterion, not hardware specifications alone.

|

"We are moving from a world where wearables collect data to a world where wearables understand patients. The AI layer is what makes the difference between a sensor and a clinical tool." |

|

— Sharmila Bhatt, Former Director, Digital Health Center of Excellence, U.S. Food and Drug Administration |

|

(Source: MedCity INVEST Digital Health Conference, 2023) |

What Is Restraining the Wearable Medical Device Market?

- Data Privacy, Cybersecurity, and HIPAA/GDPR Compliance:

Wearable devices generate continuous streams of individually identifiable health data, creating acute HIPAA obligations in the U.S. and GDPR Article 9 requirements in Europe. The FDA issued 15+ medical device cybersecurity advisories between 2021 and 2024. Enterprise hospital IT procurement committees now mandate formal cybersecurity assessments — adding 6–12 months to procurement cycles. This restraint is felt most acutely in North America and Europe.

- EU MDR Transition and Market Access Friction:

Full EU MDR (2017/745) implementation has extended CE marking timelines by 12–18 months versus the prior MDD framework. Over 600 manufacturers reported compliance challenges in 2024 surveys. Large-cap manufacturers with dedicated regulatory teams absorb the burden; mid-market players face de facto exclusion from certain EU submarkets through 2026–2027.

- Clinical Accuracy Gaps and Clinician Adoption Hesitancy:

Independent validation studies found accuracy gaps between consumer wearable claims and clinical measurement standards, particularly for optical blood pressure and SpO2 monitoring across skin tone groups. A 2023 JAMA Cardiology study identified clinically significant accuracy differences for Apple Watch and Samsung Galaxy Watch SpO2 sensors across demographic groups. Published clinical guidance from several hospital systems recommends against relying solely on consumer wearable data for clinical decisions, slowing formulary adoption.

|

"The accuracy limitations of consumer-grade wearables in diverse patient populations remain an unresolved clinical concern. We cannot treat all wearable outputs as equivalent to calibrated clinical instruments without systematic validation across demographic groups." |

|

— Dr. Joseph Dron, Lead Researcher, Wearable Technology Review, American Heart Association |

|

(Source: AHA Scientific Sessions, November 2023) |

What Opportunities Exist in the Wearable Medical Device Market?

- Emerging Market Healthcare Digitisation:

India, Brazil, Indonesia, and Nigeria collectively represent 2+ billion people with rapidly expanding smartphone ownership, growing private healthcare systems, and governments investing in digital health infrastructure. India's Ayushman Bharat Digital Mission builds the patient identity framework that wearable monitoring can integrate with at population scale. These markets are largely untapped — the first-mover positioning window is open but time-limited as Chinese manufacturers aggressively target lower-cost segments.

- Wearable Drug Delivery Systems:

Wearable insulin patch pumps, transdermal drug delivery wearables, and on-body injectors represent a fast-growing convergence of pharma and device categories. Insulet's OmniPod DASH and OmniPod 5 systems exceeded USD 1.7 billion in annual revenue by 2024. The broader opportunity extends to biologics, oncology, and cardiovascular medications — the highest-margin segment in the wearable medical device value chain.

- Paediatric and Maternal Health Wearables:

Wearable monitoring for newborn vital signs, foetal heart rate, and maternal blood pressure is a clinically high-need, commercially underserved segment. The maternal mortality crisis in the U.S. and sub-Saharan Africa has created policy urgency around continuous monitoring during high-risk pregnancies. Masimo's neonatal monitoring solutions and companies like Bloomlife represent early commercial entries into a segment attracting significant venture and strategic investment through 2027.

- AI-Powered Early Warning and Predictive Health Platforms:

Layering machine learning models on continuous wearable data to predict clinical deterioration before symptoms appear is the next commercial frontier. Early sepsis warning, pre-hypoglycaemic event alerting, and AFib pattern prediction are in active clinical development. Platform companies establishing proprietary training datasets through clinical partnerships will have durable competitive moats.

What Challenges Does the Wearable Medical Device Market Face?

- Clinician Alert Fatigue and Patient Engagement Drop-off:

Continuous wearable monitoring generates data volumes that current clinical workflows are not designed to process. Clinician alert fatigue — ignoring automated notifications due to high false-positive rates — is well-documented in remote monitoring settings. Patient engagement drop-off in remote monitoring programmes frequently exceeds 40% at 6 months, creating a chronic disease management gap that undermines clinical outcomes.

- EHR Interoperability and HL7 FHIR Integration Gaps:

Most wearable devices operate in proprietary data silos that do not natively integrate with hospital EHR systems. Achieving HL7 FHIR-compliant data exchange with Epic, Cerner, and Oracle Health requires significant integration engineering. The absence of standardised wearable data ontologies means that even when data flows into EHRs, clinicians cannot easily contextualise or act on it — the primary reason many wearable pilot programmes fail to scale.

- Reimbursement Uncertainty Outside the U.S.:

While U.S. CMS reimbursement has matured, payer reimbursement for wearable monitoring outside the U.S. remains fragmented. Most European national health systems have not established standardised remote monitoring reimbursement codes equivalent to U.S. CPT codes, limiting health system adoption to self-pay or risk-sharing arrangements.

Wearable Medical Device Market: Report Scope

|

Attribute |

Detail |

|

Report Name |

Global Wearable Medical Device Market Size, Share, Trends & Forecast 2026–2034 |

|

Market Size in 2025 |

USD 34,120 Million |

|

Market Forecast in 2034 |

USD 148,640 Million |

|

Growth Rate (CAGR) |

17.7% (2026–2034) |

|

Historical Data Period |

2019–2024 |

|

Base Year |

2025 |

|

Forecast Period |

2026–2034 |

|

Number of Pages |

300+ |

|

Tables & Figures |

110–140 tables, 80–100 figures |

|

Report Code |

ZMR-0000 |

|

Report Format |

|

|

Delivery Format |

Email attachment within 24–48 hours of purchase |

|

Published Date |

May 2026 |

|

Research Methodology |

Primary Research + Secondary Research + Data Triangulation |

|

Key Companies |

Medtronic, Abbott, Philips, Apple, Dexcom, Garmin, Omron, Fitbit/Google, Samsung, Withings, iRhythm, Insulet, BioTelemetry, Polar Electro, LifeScan |

|

Segments Covered |

By Device Type, By Application, By End User, By Connectivity Technology |

|

Regions Covered |

North America, Europe, Asia Pacific, Latin America, The Middle East, Africa |

|

Customization Scope |

20% free customization — contact sales@zionmarketresearch.com |

Request Free SampleRequest Free Sample

Request Free SampleRequest Free Sample

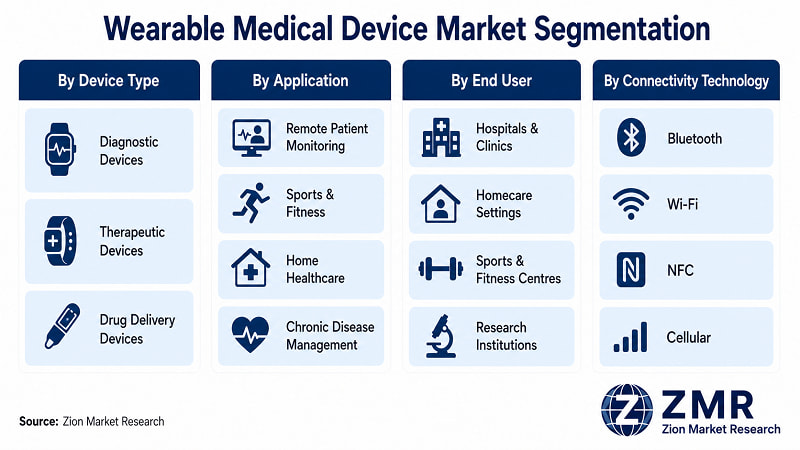

Wearable Medical Device Market: Segmentation

The Global Wearable Medical Device market is segmented by Device Type, Application, End User, and Connectivity Technology.

- By Device Type

Diagnostic Devices hold the dominant share at approximately 43% in 2025, driven by CGM adoption at scale (Abbott FreeStyle Libre, Dexcom G-series), cardiac event monitor deployment, and pulse oximetry integration. Therapeutic Devices — neurostimulation, TENS, light therapy — grow fastest at ~21% CAGR as non-pharmacological pain management gains reimbursement traction. Drug Delivery Devices, led by Insulet's OmniPod wearable patch pump (USD 1.7+ Bn revenue by 2024), represent the highest per-unit revenue segment and are expanding into biologics delivery.

- By Application

Remote Patient Monitoring leads at ~35% share in 2025 with CMS reimbursement code expansion driving hospital procurement. Chronic Disease Management is the fastest-growing application, reflecting converging monitoring needs of diabetic, cardiac, and respiratory patient populations. Sports & Fitness and Home Healthcare grow steadily but represent lower-ARPU deployments attracting consumer-grade device manufacturers.

- By End User

Hospitals & Clinics dominate procurement through group purchasing organisations and formulary adoption. Homecare Settings grow fastest — the hospital-at-home model, incentivised by CMS Advanced Care at Home waivers, is pulling wearable monitoring from in-patient settings into home environments at scale. Sports & Fitness Centres and Research Institutions are high-engagement niche categories driving device iteration and generating clinical evidence.

- By Connectivity Technology

Bluetooth dominates at ~55% share for its low power consumption, universal smartphone compatibility, and established Bluetooth medical device profiles. Wi-Fi is preferred for hospital in-patient continuous high-frequency data transmission. NFC is used for implantable device programming. Cellular-enabled wearables grow fastest for patients without reliable Wi-Fi access, particularly in rural and emerging-market deployments where 4G/5G rollout enables direct-to-cloud connectivity.

Request Free SampleRequest Free Sample

Request Free SampleRequest Free Sample

Wearable Medical Device Market: Regional Analysis

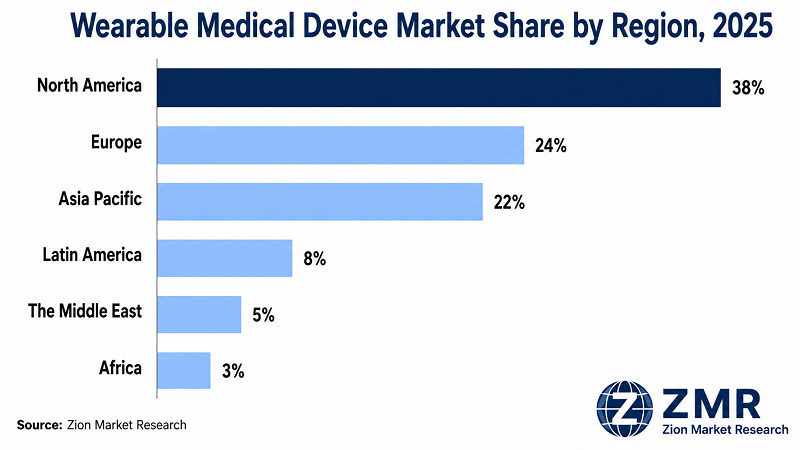

North America holds the leading revenue position at ~38% share in 2025, underpinned by the world's most mature RPM reimbursement infrastructure and the highest concentration of clinical wearable manufacturer headquarters. Asia Pacific registers the highest CAGR, driven by policy mandates, demographic volume, and electronics manufacturing capability.

- North America Wearable Medical Device Market

The U.S. anchors global demand, accounting for 85%+ of North American revenue. CMS reimbursement codes for RPM and RTM, expanded between 2019 and 2023, have created the world's highest hospital wearable monitoring programme deployment rate. The FDA's Digital Health Centre of Excellence has accelerated clearance pathways, with De Novo and 510(k) clearances for AI-enhanced wearables increasing year-on-year through 2024. Canada contributes through provincial home-care investments and Indigenous community remote monitoring programmes. Mexico's growing private hospital sector is beginning to procure clinical-grade wearables, though reimbursement infrastructure is nascent. Cybersecurity compliance burden is the primary factor extending enterprise procurement cycles.

- Europe Wearable Medical Device Market

Europe is the second-largest region, with Germany, U.K., and France as primary demand centres. Germany's DiGA pathway — approving 50+ applications by 2024 — is Europe's most advanced public payer reimbursement system for digital health. NHS England's virtual ward programme deployed wearable monitoring to 10,000+ patients by end of 2023. EU MDR compliance burden remains the primary restraint, delaying market entry for mid-market manufacturers by 12–18 months. BENELUX, Sweden, and Denmark drive above-average per-capita adoption.

- Asia Pacific Wearable Medical Device Market

Asia Pacific registers an estimated 19.8% CAGR through 2034, driven by China's Healthy China 2030 digital health mandates, India's Ayushman Bharat Digital Mission patient identity infrastructure, and Japan and South Korea's combined manufacturing and healthcare innovation capabilities. Domestic Chinese companies including Huawei Health and Xiaomi Health compete in consumer-clinical wearables at lower price points. South Korea leads the region in CGM and cardiac monitor per-capita adoption. Australia is the region's most mature reimbursement environment for remote monitoring outside Japan.

- Latin America Wearable Medical Device Market

Brazil dominates at ~48% of regional revenue in 2025, driven by SUS public health system scale and expanding private health insurance. Brazil's SUS chronic disease management programme is evaluating wearable monitoring as a cost-containment tool. Import duties and local content requirements constrain device pricing competitiveness, creating opportunities for regional manufacturing partnerships. Argentina, Colombia, Peru, and Chile represent smaller but growing markets driven by private healthcare investment.

- The Middle East Wearable Medical Device Market

The Middle East is led by GCC countries — Saudi Arabia, UAE, and Qatar — where sovereign wealth-funded healthcare investment creates demand for clinical connected care solutions. Saudi Arabia's Vision 2030 healthcare transformation has prioritised digital health and remote monitoring as core components of a hospital-to-home care transition. The UAE's Dubai Health Authority has approved wearable remote monitoring programmes for diabetes and cardiac patients. Israel represents a distinctive innovation cluster with companies like Biobeat developing multi-parameter wearable monitors. Turkey is an emerging market; Iran is constrained by sanctions.

- Africa Wearable Medical Device Market

Africa is the smallest regional market by current revenue but a high-potential long-term opportunity, given high disease burden, expanding mobile connectivity, and health system capacity constraints favouring home-based monitoring. South Africa and Egypt are the primary current demand centres. Nigeria presents significant opportunity at 220 million population with growing private healthcare infrastructure. Cellular-connected wearables are the primary growth enabler given limited Wi-Fi infrastructure. The primary restraints are purchasing power and the absence of public payer reimbursement frameworks across most African markets.

Request Free SampleRequest Free Sample

Request Free SampleRequest Free Sample

Full Country Coverage

|

Region |

Countries Covered |

|

North America |

The U.S., Canada, Mexico |

|

Europe |

Germany, France, U.K., Italy, Spain, Russia, BENELUX, Sweden, Denmark, Poland, Austria, Rest of Europe |

|

Asia Pacific |

China, Japan, India, South Korea, Australia, Thailand, Indonesia, Vietnam, Malaysia, Philippines, Taiwan, Rest of Asia Pacific |

|

Latin America |

Brazil, Argentina, Colombia, Chile, Peru, Rest of Latin America |

|

The Middle East |

GCC (Saudi Arabia, UAE, Qatar, Kuwait, Bahrain, Oman), Israel, Turkey, Iran, Rest of Middle East |

|

Africa |

South Africa, Egypt, Nigeria, Algeria, Morocco, Rest of Africa |

Country-level market sizing, historical data, and forecasts available for all geographies listed. Custom regional add-ons available — contact sales@zionmarketresearch.com

Request Free SampleRequest Free Sample

Request Free SampleRequest Free Sample

Wearable Medical Device Market: Competitive Landscape

- The market is moderately concentrated — five companies (Medtronic, Abbott, Apple, Dexcom, Philips) account for an estimated 45–50% of 2025 total revenue — but fragmented across therapeutic and connectivity niches.

- The primary strategic differentiator has shifted from hardware accuracy to software ecosystem depth: companies with proprietary AI analytics, EHR integration partnerships, and payer-reimbursed clinical programmes command pricing premiums over hardware-only competitors. Strategic acquisitions of AI analytics and digital therapeutics platforms dominate competitive activity.

|

Company |

HQ Country |

Primary Focus |

Key Strategy |

Notable Recent Action |

|

Medtronic plc |

Ireland |

Cardiac & Diabetes Wearables |

AI-enhanced predictive analytics |

Google Cloud AI partnership (Mar 2025) |

|

Abbott Laboratories |

U.S. |

CGM — FreeStyle Libre |

Global OTC CGM scale-up |

Libre 3 deployed 58+ countries (2024) |

|

Apple Inc. |

U.S. |

Consumer-Clinical Smartwatch |

FDA clearance expansion |

Series 10 Sleep Apnoea clearance (2024) |

|

Dexcom Inc. |

U.S. |

Continuous Glucose Monitoring |

OTC CGM for non-insulin T2D |

Stelo OTC CGM FDA cleared (Jan 2025) |

|

Philips Healthcare |

Netherlands |

Hospital Patient Monitoring |

Connected care platform |

HealthSuite platform expansion (2024) |

|

Omron Healthcare |

Japan |

Blood Pressure Wearables |

Clinical-grade consumer devices |

HeartGuide global rollout |

|

Garmin Ltd. |

Switzerland |

Fitness & Health Wearables |

B2B health solutions |

Garmin Health B2B programme growth |

|

iRhythm Technologies |

U.S. |

Wearable Cardiac Monitor |

AI arrhythmia detection at scale |

4M+ Zio Patch analyses by 2024 |

|

Insulet Corporation |

U.S. |

Tubeless Insulin Pump |

Closed-loop AID system |

OmniPod 5 EU expansion (2024) |

|

Samsung Electronics |

South Korea |

Consumer Health Wearables |

Clinical FDA clearances |

Galaxy Watch 7 AFib clearance (2024) |

|

Withings |

France |

Medical-Grade Consumer Devices |

Prescription digital health |

ScanWatch 2 BP + ECG (2024) |

|

BioTelemetry (Philips) |

U.S. |

Remote Cardiac Monitoring |

MCT + Holter service scale |

Integrated into Philips RPM platform |

|

LifeScan Inc. |

U.S. |

Blood Glucose Monitoring |

BGM to CGM market transition |

OneTouch Verio Reflect smart meter |

|

Polar Electro |

Finland |

Sports & Clinical HR Monitor |

Clinical research partnerships |

Polar Vantage V3 clinical-grade HR |

|

Masimo Corporation |

U.S. |

SpO2 & Multiparameter |

Consumer wearable expansion |

W1 health smartwatch launch (2023) |

Request Free SampleRequest Free Sample

Request Free SampleRequest Free Sample

Recent Developments in the Wearable Medical Device Market

Strategic activity has intensified through 2024–2025, with regulatory clearances, platform partnerships, and OTC market expansion defining the competitive pace.

|

Date |

Company |

Type |

Description |

Market Impact |

|

Mar 2025 |

Medtronic / Google Cloud |

Strategic Partnership |

AI predictive analytics across wearable cardiac and diabetes platforms |

Elevates clinical decision-support; raises AI benchmark for competitors |

|

Jan 2025 |

Dexcom Inc. |

Regulatory Clearance |

Stelo OTC CGM FDA cleared for T2D non-insulin users |

Opens ~25M U.S. adult TAM; accelerates CGM commoditisation |

|

Sep 2024 |

Apple Inc. |

Product Launch |

Watch Series 10 — enhanced AFib + Sleep Apnoea FDA clearance |

Expands consumer-clinical installed base globally |

|

Jul 2024 |

Insulet Corporation |

Product Expansion |

OmniPod 5 AID system expanded to 20+ additional EU countries |

Strengthens insulin pump leadership in Europe |

|

Apr 2024 |

Samsung Electronics |

Regulatory Clearance |

Galaxy Watch 7 FDA clearance for AFib detection |

Second consumer-clinical smartwatch with clinical cardiac credentials |

About Zion Market Research

Zion Market Research is an obligated company. We create futuristic, cutting-edge, informative reports ranging from industry reports, company reports to country reports. We provide our clients not only with market statistics unveiled by avowed private publishers and public organizations but also with vogue and newest industry reports along with pre-eminent and niche company profiles. Our database of market research reports comprises a wide variety of reports from cardinal industries. Our database is updated constantly in order to fulfil our clients' requirements for prompt and direct online access. Keeping in mind the client's needs, we have included expert insights on global industries, products, and market trends in this database.

Author:

Mr. Nilesh Patil

Zion Market Research

LinkedIn- www.linkedin.com/in/nilesh-patil-m-s-m-b-a-bba33067

Table Of Content

Methodology

FrequentlyAsked Questions

The report includes 300+ pages covering market sizing with historical data from 2019, base-year analysis for 2025, and granular forecasts through 2034. It covers 4 segmentation dimensions (Device Type, Application, End User, Connectivity Technology), country-level forecasts for 35+ geographies across 6 regions, profiles of 15 competitive companies, full DROC analysis, recent industry developments (2022–2025), research methodology, and 110–140 tables with 80–100 figures.

The Global Wearable Medical Device market was valued at USD 34,120 Million in 2025. Zion Market Research forecasts the market will reach USD 148,640 Million by 2034 at a 17.7% CAGR. These figures are based on primary stakeholder research, CMS billing data, device clearance databases, and triangulation against publicly reported manufacturer revenues.

The report segments across four dimensions: (1) By Device Type — Diagnostic, Therapeutic, Drug Delivery; (2) By Application — Remote Patient Monitoring, Sports & Fitness, Home Healthcare, Chronic Disease Management; (3) By End User — Hospitals & Clinics, Homecare Settings, Sports & Fitness Centres, Research Institutions; (4) By Connectivity Technology — Bluetooth, Wi-Fi, NFC, Cellular. Each segment includes historical data, base-year sizing, forecast, and CAGR.

35+ countries across 6 regions analysed separately: North America (The U.S., Canada, Mexico); Europe (Germany, France, U.K., Italy, Spain, Russia, BENELUX, Sweden, Denmark, Poland, Austria, Rest of Europe); Asia Pacific (China, Japan, India, South Korea, Australia, Thailand, Indonesia, Vietnam, Malaysia, Philippines, Taiwan, Rest of Asia Pacific); Latin America (Brazil, Argentina, Colombia, Chile, Peru, Rest of Latin America); The Middle East (GCC: Saudi Arabia, UAE, Qatar, Kuwait, Bahrain, Oman — plus Israel, Turkey, Iran); Africa (South Africa, Egypt, Nigeria, Algeria, Morocco, Rest of Africa). The Middle East and Africa are always covered as separate regions.

Zion Market Research offers up to 20% free customization: additional country coverage, extra segmentation dimensions (e.g., by price tier, device brand), competitive profiling of specific companies, extended forecast horizon beyond 2034, custom regional deep-dive modules, and integration with client proprietary data for benchmarking. Contact sales@zionmarketresearch.com to discuss.

(1) Free Sample 2) Full Report Purchase (3) Custom Inquiry — contact sales@zionmarketresearch.com | +1 (302) 444-0166 | Toll Free: +1 (855) 465-4651.

List of Contents

Industry PerspectiveOverviewKey InsightsWhy Choose the Zion Market ResearchMarket Report?Wearable Medical DeviceDynamics (Drivers, Restraints, Opportunities, Challenges)Report ScopeSegmentationRegional AnalysisFull Country CoverageCompetitive LandscapeRecent Developments in the MarketHappyClients