Stem Cell Therapy Market Size, Share, Trends & Forecast 2026–2034

Global Stem Cell Therapy Market Size, Share, Trends, Analysis, Growth, Segments, Revenue, Manufacturers, and Forecast 2026–2034.-

| Market Size in 2025 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 12,840 Million | USD 64,820 Million | 19.6% | 2025 |

Stem Cell Therapy Market: Industry Perspective

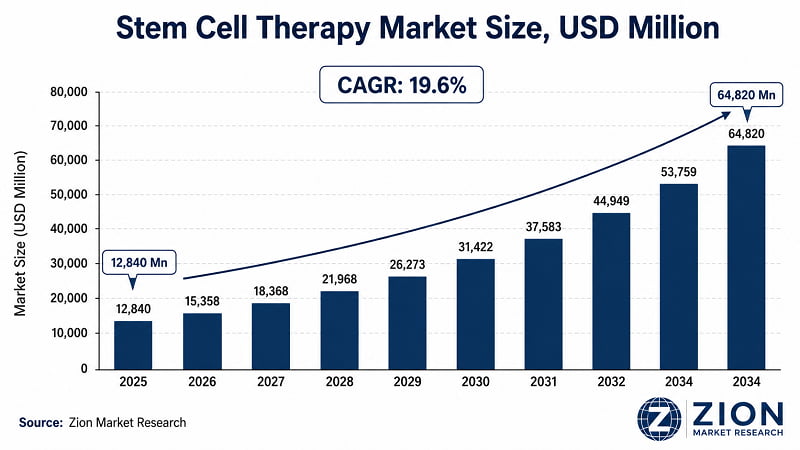

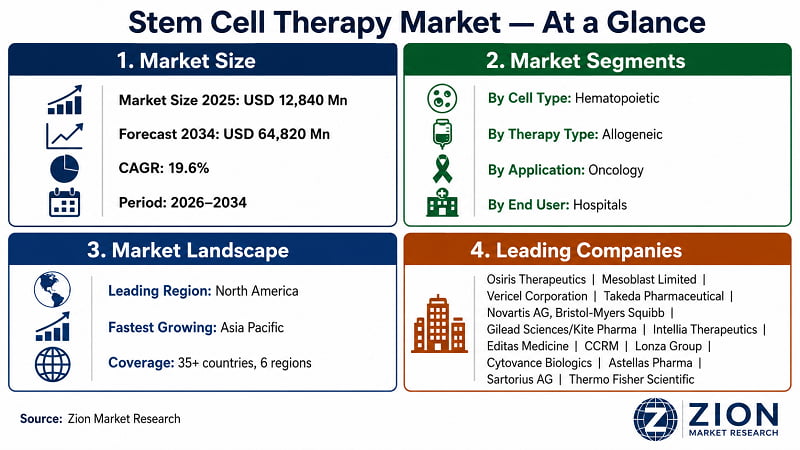

- The global stem cell therapy market was valued at USD 12,840 Million in 2025. It's projected to expand to USD 64,820 Million by 2034 at a 19.6% CAGR — representing an absolute incremental opportunity of USD 51,980 Million over nine years.

- This isn't a speculative forecast driven by pipeline potential alone; it's anchored by commercial-stage approved products, established reimbursement infrastructure in North America and Germany, and a manufacturing technology curve that is systematically reducing per-unit cost of goods.

- The structural shift from autologous to allogeneic therapy architectures is the defining commercial transition of the current forecast period.

- According to Zion Market Research, allogeneic platforms will capture a growing majority of new commercial launches through 2030 as off-the-shelf scalability resolves the volume constraints that have historically capped market penetration.

- For procurement executives and investors, the analytical priority is not aggregate market size but segment-level divergence — particularly the emerging gap between allogeneic scalability economics and autologous margin profiles.

Request Free SampleRequest Free SampleRequest Free Sample

Request Free SampleRequest Free SampleRequest Free Sample

Stem Cell Therapy Market: Overview

- Stem cell therapy encompasses the clinical and commercial application of stem cells — self-renewing, undifferentiated progenitor cells — to repair, restore, or replace damaged or dysfunctional tissues and organs. The market spans five primary cell types: hematopoietic, mesenchymal, induced pluripotent (iPSC), neural, and embryonic stem cells. Therapeutic applications cover oncology, musculoskeletal, cardiovascular, neurological, and wound care indications, delivered through autologous (patient-derived) and allogeneic (donor-derived) therapy architectures. The full value chain includes cell sourcing, GMP bioprocessing, cryopreservation, logistics, clinical administration, and post-treatment monitoring infrastructure.

- The value chain operates across three tiers. Foundational providers — infrastructure and platform layer — include Lonza Group (Switzerland), Sartorius AG (Germany), and Thermo Fisher Scientific (USA), which supply GMP bioreactors, cryopreservation systems, and quality control platforms. Specialist developers — sector-specific integrators — include Mesoblast Limited (Australia), Vericel Corporation (USA), and Osiris Therapeutics (USA), which develop and manufacture cell therapy products for defined clinical indications. Application-layer specialists — vertical product companies — include Bristol-Myers Squibb (USA) and Novartis (Switzerland), which commercialise FDA-approved CAR-T and gene-modified cell therapy products directly to hospital networks.

- For procurement and investment decision-makers, the distinction that matters is not whether the stem cell therapy market will grow — that question is settled — but which segments, geographies, and deployment models will capture disproportionate value within that growth. This report provides sub-segment level data, country-level forecasts, and competitive positioning analysis across four segmentation dimensions and 35+ geographies.

Key Insights

- The global stem cell therapy market grows at 19.6% CAGR (2026–2034) to reach USD 64,820 Million by 2034, per Zion Market Research.

- Hematopoietic stem cells (HSCs) hold the dominant cell type segment share at ~38%, driven by decades of clinical validation in bone marrow transplantation and CAR-T constructs.

- Induced pluripotent stem cells (iPSCs) are the fastest-growing sub-segment by cell type, with pipeline growth projected at 24%+ CAGR as CRISPR-edited iPSC platforms approach clinical-stage validation.

- Oncology is the dominant application, accounting for ~45% of total market revenue in 2025, anchored by FDA-approved CAR-T therapies for haematological malignancies.

- Hospitals & Clinics are the dominant end-user segment, comprising ~60% of procedure volume, as high-acuity stem cell procedures require inpatient administration infrastructure.

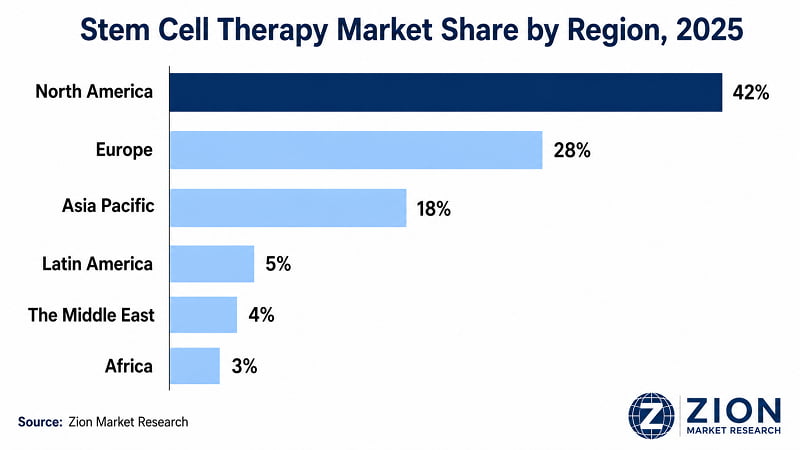

- North America holds the dominant regional share at ~42% in 2025, driven by U.S. FDA approvals, reimbursement infrastructure, and the highest concentration of stem cell trial sites globally.

- Asia Pacific is the fastest-growing region, registering 22%+ CAGR, led by Japan's regulatory innovation, China's biomanufacturing capacity expansion, and South Korea's cell therapy competencies.

- Competitive landscape is moderately fragmented: large pharma (BMS, Novartis) dominate approved CAR-T products; specialised biotechs lead mesenchymal and orthopaedic applications.

- The 2026–2030 sub-period will be disproportionately shaped by allogeneic platform approvals — companies with scalable off-the-shelf programmes are positioned to capture outsized commercial share as payer coverage expands.

Why Choose the Zion Market Research's Stem Cell Therapy Market Report?

Decision-makers comparing market intelligence reports on Stem Cell Therapy will find the Zion Market Research's report differentiated on the following dimensions.

|

Dimension |

Zion Market Research Report |

Industry Average |

|

Report Pages |

300+ |

~120 pages |

|

Forecast Horizon |

9 years (2026–2034) |

7 years |

|

Segmentation Dimensions |

4 dimensions |

2-3 dimensions |

|

Historical Data |

6 years (2019–2024) |

4–5 years |

|

Country Coverage |

35+ countries |

15–18 countries |

|

Companies Profiled |

15 companies |

10 companies |

|

DROC Framework |

Full (Drivers, Restraints, Opportunities, Challenges) |

Drivers only |

**For custom scope — additional segments, specific geographies, or extended forecast periods — contact sales@zionmarketresearch.com

Stem Cell Therapy Market: Dynamics (Drivers, Restraints, Opportunities, Challenges)

Request Free SampleRequest Free SampleRequest Free Sample

Request Free SampleRequest Free SampleRequest Free Sample

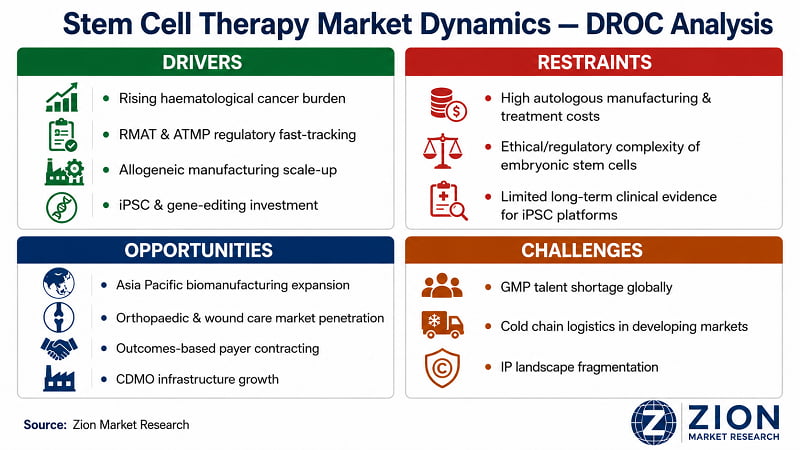

What Is Driving the Stem Cell Therapy Market?

- Rising Haematological Cancer Burden:

The global incidence of haematological malignancies — leukaemia, lymphoma, multiple myeloma — reached an estimated 1.24 million new cases annually by 2024, according to WHO Cancer Statistics. This demand-side dynamic is not cyclical; it's structural, driven by ageing demographics and improved diagnostic rates that convert previously undetected cases into treatment-eligible patients. Hematopoietic stem cell transplantation (HSCT) remains the standard of care for relapsed/refractory haematological cancers, ensuring base-load demand stability even as CAR-T alternatives expand the treatment spectrum. Bristol-Myers Squibb deployed Breyanzi (lisocabtagene maraleucel) across 150+ U.S. treatment centres by 2023, generating USD 631 Million in net product sales in FY2023 alone — concrete evidence that commercial-scale stem cell therapy revenue generation is already in progress, not speculative. In Europe, Germany's statutory health insurance (GKV) system approved reimbursement for axicabtagene ciloleucel (Yescarta) for diffuse large B-cell lymphoma in 2023, extending the TAM for commercially viable stem cell therapy to the second-largest healthcare market in the OECD.

- Regulatory Fast-Tracking via RMAT & ATMP Frameworks:

The FDA's Regenerative Medicine Advanced Therapy (RMAT) designation, established under the 21st Century Cures Act (2016), has meaningfully compressed approval timelines for eligible cell therapies. RMAT-designated programmes averaged 4.6 years from IND filing to approval between 2016 and 2023, compared to 8–12 years via standard review pathways — a 20–40% reduction depending on indication complexity. The EMA's ATMP framework provides an equivalent acceleration pathway across EU member states, with centralised approval enabling simultaneous market access in 27 countries on a single dossier. This regulatory tailwind directly reduces the risk-adjusted cost of capital for stem cell therapy developers, accelerating investor deployment into the sector. Novartis received RMAT designation for its gene-modified cell therapy platform in 2021, and its Zolgensma programme completed EMA approval within 4.2 years of IND — below category average, validating the pathway's structural advantage for well-prepared sponsors.

- Allogeneic Manufacturing Technology Maturation:

The commercial shift from patient-specific autologous manufacturing to scalable allogeneic ('off-the-shelf') cell therapy platforms is the most consequential supply-side development in the stem cell therapy market. Autologous processes are inherently batch-of-one: each patient's cells must be collected, processed, quality-tested, and returned within a constrained timeframe — a logistical chain that carries USD 400,000–500,000 per-patient list prices and a 15–30% manufacturing failure rate. Allogeneic platforms, by contrast, allow a single donor batch to generate hundreds of patient doses under standardised GMP conditions, reducing per-unit cost of goods by an estimated 60–80%. Intellia Therapeutics disclosed its allogeneic CRISPR-edited CAR-T programme targeting commercial-stage IND filing by 2025. Editas Medicine has a parallel allogeneic programme, with preclinical data presented at ASH 2023 showing durable remission in haematological cancer models — technical validation that off-the-shelf cell therapy is approaching Phase I clinical entry.

- Expanding iPSC & Gene-Editing Platform Investment:

Induced pluripotent stem cells, combined with CRISPR-Cas9 gene editing, represent the fastest-growing technology sub-segment in the stem cell therapy pipeline. iPSC platforms allow generation of patient- or donor-derived cells at near-unlimited scale, bypassing the sourcing constraints of primary cell isolation. Total global venture and corporate investment in iPSC-based cell therapy exceeded USD 2.1 Billion between 2021 and 2024, per Pitchbook data, reflecting institutional conviction in the platform's long-term displacement of first-generation autologous therapies. Japan's CCRM-affiliate and Takeda Pharmaceutical announced a JPY 3.5 Billion co-investment in iPSC cell therapy manufacturing infrastructure in Osaka in 2023 — one of the largest single iPSC manufacturing commitments in Asia Pacific — demonstrating sovereign-scale capital deployment aligned with the technology trajectory.

|

"RMAT has fundamentally changed our clinical and commercial planning timelines. The ability to engage the FDA in rolling review changes the economics of cell therapy development in a way that benefits the entire ecosystem — developers, patients, and payers alike." |

|

— Dr. Helen Sabzevari, President and CEO, Puma Biotechnology (former NCI/FDA regulatory executive) |

|

(Source: Alliance for Regenerative Medicine State of the Industry Briefing, ARM, January 2024) |

What Is Restraining the Stem Cell Therapy Market?

- High Autologous Manufacturing & Treatment Costs:

The per-patient economics of autologous cell therapy remain a structural barrier to broad market penetration. FDA-approved autologous CAR-T products carry list prices of USD 400,000–500,000 per course of treatment in the U.S. market, creating access constraints even in the highest-income payer environment globally. This isn't merely a pricing problem — it's a manufacturing architecture problem. Autologous processes require patient-specific leukapheresis, complex cell processing, independent quality release testing, and a temperature-controlled logistics chain with a 10–15% vein-to-vein failure rate. For hospital systems in Latin America, The Middle East, and Africa, the cold chain and quality infrastructure alone represent prohibitive capital investment. The restraint is most pronounced in low-to-middle income markets, where the USD 10,000+ per-dose infrastructure cost floor for even simplified allogeneic products remains above reimbursement ceilings.

- Ethical & Regulatory Complexity Around Embryonic Stem Cells:

Embryonic stem cell (ESC) research faces legislative prohibition or severe restriction in Germany, Austria, Italy, Poland, and several U.S. states — markets that collectively represent over 30% of global pharmaceutical revenue. This creates a fragmented regulatory landscape that complicates global trial design, limits the TAM for ESC-based programmes, and introduces reputational risk for multinationals operating across jurisdictions. The restraint is stable in the near term; no meaningful regulatory liberalisation on ESC is anticipated in these markets before 2028.

- Limited Long-Term Safety Data for Next-Generation Platforms:

iPSC-based therapies and several mesenchymal cell programmes lack the 10–15 year safety datasets that formulary committees at major health systems increasingly require before expanding coverage. The oldest iPSC clinical trial data is barely five years old; tumorigenicity concerns — while not validated in current clinical evidence — remain an unresolved theoretical risk that payer medical directors cite in coverage denial rationale. This evidence gap is a timeline constraint, not a fundamental scientific barrier, but it delays payer acceptance by 3–5 years for novel platforms relative to autologous HSCT, which carries decades of safety records.

|

"The GMP manufacturing capacity gap is real. We have clinical demand outpacing qualified manufacturing slots at every major academic medical centre in the U.S. Until we fix the infrastructure equation — either through CDMO scale-up or hospital-integrated manufacturing — we will leave treatable patients behind." |

|

— Dr. Carl June, Richard W. Vague Professor, University of Pennsylvania Perelman School of Medicine |

|

(Source: AACR Annual Meeting, April 2023) |

What Opportunities Exist in the Stem Cell Therapy Market?

- Asia Pacific Biomanufacturing Infrastructure Expansion:

Japan, China, and South Korea are collectively investing in GMP cell therapy manufacturing infrastructure at a pace that will structurally alter global production geography by 2028. Japan's PMDA conditional approval pathway enables early commercialisation while long-term clinical data accumulates — a model that reduces developer cash-burn risk substantially. China's 14th Five-Year Plan (2021–2025) allocated CNY 15 Billion for biopharmaceutical manufacturing modernisation, a portion of which is specifically directed at cell and gene therapy CDMOs. South Korea's Celltrion and Samsung Biologics are diversifying into cell therapy CDMO services, leveraging existing GMP infrastructure built for biosimilar production. For global developers, the opportunity is not just a faster-growth market — it's access to lower-cost GMP manufacturing that can serve Asian regulatory filings while reducing global cost of goods sold.

- Orthopaedic & Wound Care Market Penetration:

Musculoskeletal disorders and chronic wound management represent a substantially underpenetrated opportunity within the stem cell therapy market. Vericel Corporation's MACI (autologous chondrocytes) product generated USD 202 Million in 2023 revenue from a single orthopaedic indication — cartilage repair — illustrating the category's commercial viability independent of the oncology segment. The global chronic wound management market exceeds USD 20 Billion annually; stem cell-derived treatments for diabetic foot ulcers, pressure ulcers, and burn wounds represent an early-stage but high-growth insertion point. Japan's 2023 MHLW approval of allogeneic adipose-derived MSCs for diabetic foot ulcers validates the regulatory pathway and sets a direct precedent for similar approvals in South Korea, Australia, and the EU through 2026–2027.

- Outcomes-Based Payer Contracting Frameworks:

The emergence of outcomes-based contracts for high-cost cell therapies — where manufacturers share financial risk with payers tied to real-world patient outcomes — represents a structural mechanism to unlock reimbursement in markets currently deterred by upfront cost exposure. Novartis pioneered this model for Kymriah in the U.S. in 2017; by 2024, outcomes-based contracting had been adopted by over 60% of large U.S. commercial payers for at least one cell therapy product. As this contracting architecture scales to Germany, the U.K., and Japan, it directly addresses the cost access barrier and expands the commercially addressable patient population for all approved stem cell therapies. The model also creates a data collection mechanism — real-world outcomes evidence — that accelerates payer acceptance for subsequent approved products.

- CDMO Sector Growth as Infrastructure Enabler:

The cell therapy contract development and manufacturing organisation (CDMO) market is growing at an estimated 25%+ CAGR, outpacing even the therapy market itself. Companies including Lonza Group, Samsung Biologics, and Charles River Laboratories are expanding GMP cell therapy manufacturing capacity through both greenfield builds and strategic acquisitions. For smaller biotech developers that cannot justify USD 50–100 Million GMP facility capital expenditure, CDMO access provides a clear route to clinical and commercial-stage manufacturing without balance sheet constraint. Lonza's Houston cell therapy CDMO facility — opened in 2023 with 12 GMP manufacturing suites — directly addresses the North American supply bottleneck that has constrained commercial launch timelines for multiple developers simultaneously.

What Challenges Does the Stem Cell Therapy Market Face?

- GMP-Qualified Talent Shortage:

The global shortage of GMP-trained bioprocess scientists, quality assurance professionals, and cell therapy manufacturing operators is constraining production capacity expansion at a critical phase of market growth. A 2023 industry survey by the Alliance for Regenerative Medicine (ARM) identified GMP talent availability as the top operational constraint cited by 68% of cell therapy manufacturers globally. This isn't a temporary bottleneck — it reflects a training pipeline that runs 3–5 years behind commercial demand, given the highly specialised nature of cell therapy bioprocessing relative to conventional biopharmaceutical manufacturing. Universities and vocational programmes have not yet scaled GMP cell therapy curricula to match the pace of commercial facility construction; the gap will persist through at least 2027 without targeted workforce investment.

- Cold Chain Logistics in Developing Markets:

Cryopreserved cell therapies require continuous -80°C or liquid nitrogen cold chain management from the manufacturing facility to the clinical administration site without interruption. In markets across Africa, Latin America, and parts of Asia Pacific, the healthcare logistics infrastructure cannot reliably maintain these temperature requirements without significant capital investment in specialised transport containers, dedicated storage units, and trained cold chain personnel. This cold chain constraint is a practical market access barrier that limits the geographic penetration of even affordably priced allogeneic products in developing markets through at least 2030, effectively capping the addressable patient population well below the epidemiological opportunity these geographies represent.

- IP Landscape Fragmentation & Freedom-to-Operate Risk:

The stem cell therapy patent landscape is densely contested, with overlapping claims on cell processing methods, culture conditions, specific cell surface marker combinations, and gene-editing delivery vectors. Freedom-to-operate analyses for new cell therapy programmes routinely identify 200–400 potentially relevant patents requiring legal assessment before clinical entry. IP fragmentation increases legal spend by USD 2–5 Million per programme, delays IND filings by 6–18 months, and creates royalty stacking economics that erode developer margins even for commercially successful programmes. The problem is compounding: as CRISPR, iPSC, and allogeneic platform patents multiply, the freedom-to-operate landscape for next-generation programmes entering clinical development from 2025 onwards will be materially more complex than it was for first-generation CAR-T programmes.

Stem Cell Therapy Market: Report Scope

|

Attribute |

Details |

|

Report Name |

Stem Cell Therapy Market Size, Share, Trends & Forecast 2026–2034 |

|

Market Size in 2025 |

USD 12,840 Million |

|

Market Forecast in 2034 |

USD 64,820 Million |

|

Growth Rate (CAGR) |

19.6% (2026–2034) |

|

Historical Data Period |

2019–2024 |

|

Base Year |

2025 |

|

Forecast Period |

2026–2034 |

|

Number of Pages |

300+ |

|

Tables & Figures |

110–140 tables, 80–100 figures (complex market: 4 segmentation dimensions) |

|

Report Code |

ZMR-10574 |

|

Report Format |

|

|

Delivery Format |

Instant digital download |

|

Published Date |

May 2026 |

|

Research Methodology |

Primary Research (interviews, surveys) + Secondary Research (databases, filings, publications) |

|

Key Companies Covered |

Osiris Therapeutics, Mesoblast Limited, Vericel Corporation, Takeda Pharmaceutical, Novartis AG, Bristol-Myers Squibb, Gilead Sciences/Kite Pharma, Intellia Therapeutics, Editas Medicine, CCRM, Lonza Group, Cytovance Biologics, Astellas Pharma, Sartorius AG, Thermo Fisher Scientific |

|

Segments Covered |

By Cell Type, By Therapy Type, By Application, By End User |

|

Regions Covered |

North America, Europe, Asia Pacific, Latin America, The Middle East, Africa |

|

Customization Scope |

20% free customization included. Contact sales@zionmarketresearch.com |

Request Free SampleRequest Free SampleRequest Free Sample

Request Free SampleRequest Free SampleRequest Free Sample

Stem Cell Therapy Market: Segmentation

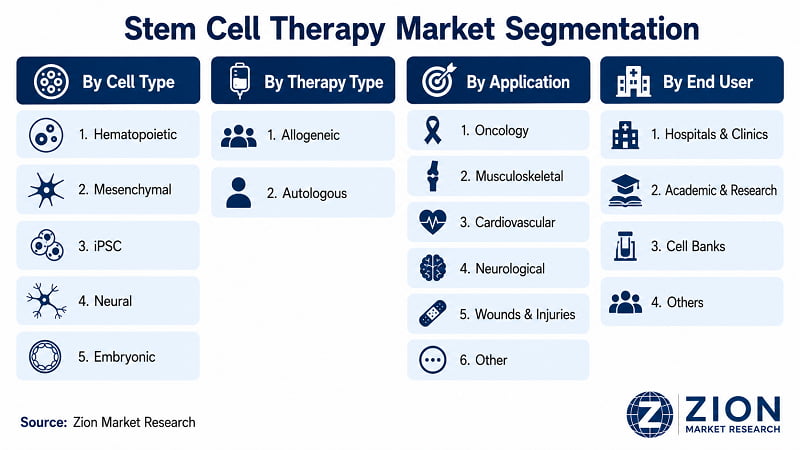

The Global Stem Cell Therapy market is segmented by cell type, therapy type, application, and end user.

- By Cell Type

The stem cell therapy market by cell type covers hematopoietic stem cells (HSCs), mesenchymal stem cells (MSCs), induced pluripotent stem cells (iPSCs), neural stem cells, and embryonic stem cells. Hematopoietic stem cells hold the dominant sub-segment share at approximately 38% in 2025, driven by decades of clinical validation across bone marrow transplantation and the commercial CAR-T product category. The mechanism is straightforward: HSCs are the only autologous cell type with established FDA-approved manufacturing protocols and payer reimbursement — advantages that take years to replicate for competing cell types. Bristol-Myers Squibb's Breyanzi (HSC-derived) and Novartis's Kymriah both leverage HSC biology, anchoring commercial revenue in the segment. Induced pluripotent stem cells (iPSCs) are the fastest-growing sub-segment, forecast at 24%+ CAGR, as CRISPR-edited iPSC programmes approach Phase I clinical entry in haematological and neurodegenerative indications.

- By Therapy Type

The market by therapy type divides between allogeneic stem cell therapy and autologous stem cell therapy. Allogeneic therapy holds and is extending its dominant share — estimated at 58% of the market in 2025 and forecast to reach 65%+ by 2030. The dominance mechanism is economic: allogeneic platforms generate multiple patient doses from a single manufacturing run, collapsing per-unit COGS by 60–80% versus autologous batch-of-one processes. Takeda Pharmaceutical's allogeneic bone marrow transplant support programmes and Mesoblast's remestemcel-L allogeneic MSC platform illustrate the breadth of clinical applications already in commercial or late-stage allogeneic development. Autologous therapy maintains strong positions in high-acuity haematological indications where personalised T-cell specificity is clinically required, but the strategic direction of the market is clearly allogeneic.

- By Application

Application segments include oncology, musculoskeletal disorders, cardiovascular diseases, neurological disorders, wounds & injuries, and other applications. Oncology is the dominant application, capturing approximately 45% of total revenue in 2025. The FDA's commercial approval of five distinct CAR-T products by 2024 — for DLBCL, ALL, multiple myeloma, mantle cell lymphoma, and follicular lymphoma — has created a multi-indication commercial base that anchors oncology's segment leadership through the forecast period. Musculoskeletal disorders are the fastest-growing non-oncology application, driven by orthopaedic stem cell therapies for cartilage repair (Vericel's MACI) and emerging MSC programmes for degenerative joint disease. The wound care application (particularly diabetic foot ulcers) received a notable regulatory catalyst with Japan's 2023 MHLW approval, accelerating the commercial timeline for this sub-segment across Asia Pacific.

- By End User

End users in the stem cell therapy market are hospitals & clinics, academic & research institutes, cell banks, and others. Hospitals & Clinics hold the dominant end-user position, accounting for approximately 60% of procedure volume in 2025. High-acuity stem cell procedures — particularly HSCT and CAR-T administration — require inpatient monitoring infrastructure, specialised haematology/oncology nursing staff, and ICU backup capabilities that are only available in hospital settings. Academic & Research Institutes hold a disproportionately large share relative to their clinical volume, as they serve as trial sites for the pipeline of next-generation therapies that will convert to commercial revenue from 2027 onwards. Cell banks — private and public umbilical cord blood banks — are a growing end-user category as allogeneic therapy platforms increase demand for diverse, quality-tested cell inventory.

Request Free SampleRequest Free SampleRequest Free Sample

Request Free SampleRequest Free SampleRequest Free Sample

Stem Cell Therapy Market: Regional Analysis

North America leads the global stem cell therapy market with approximately 42% revenue share in 2025. Asia Pacific is the fastest-growing region. The structural reason for this divergence is regulatory: North America's RMAT pathway and payer reimbursement for approved CAR-T products give it a commercial maturity advantage that Asia Pacific is systematically closing through regulatory innovation and biomanufacturing investment.

- North America Stem Cell Therapy Market

North America's market leadership reflects the convergence of three structural advantages: the FDA's RMAT designation fast-tracking commercial approvals, the highest global density of academic medical centres with approved stem cell therapy dispensing capability, and a payer environment that has — despite cost controversy — established reimbursement pathways for FDA-approved CAR-T products. The U.S. dominates the region, home to the majority of commercially approved stem cell therapy products globally. Canada contributes through CCRM, which supports Canadian and international cell therapy companies through GMP manufacturing, clinical development, and regulatory infrastructure. Mexico's market remains nascent, primarily limited to haematopoietic transplantation in academic centres in Mexico City and Guadalajara. The primary challenge in North America is access inequality: high autologous therapy costs concentrate treatment in wealthy urban health systems, leaving rural and lower-income populations underserved despite commercially available therapies.

- Europe Stem Cell Therapy Market

Europe holds the second-largest regional share, underpinned by the EMA's ATMP framework, which enables centralised approval covering all 27 EU member states on a single dossier. Germany leads European adoption, driven by statutory health insurance coverage of axicabtagene ciloleucel (Yescarta) approved in 2023 and a strong academic stem cell transplantation infrastructure concentrated in Berlin, Munich, and Frankfurt. The U.K., operating under the MHRA post-Brexit, maintains one of the most active stem cell trial environments in Europe through the Cell and Gene Therapy Catapult in London. France and Italy contribute through national haematology networks. Sweden and the Netherlands are emerging precision hubs for MSC research. Reimbursement variability across EU member states — Germany's robust coverage versus Italy's fragmented regional reimbursement — remains the most significant commercial constraint in the region.

- Asia Pacific Stem Cell Therapy Market

Asia Pacific is the market's fastest-growing region at 22%+ CAGR, driven by a combination of regulatory innovation, manufacturing investment, and epidemiological demand. Japan's PMDA conditional approval pathway has enabled earlier commercialisation of cell therapy products than any other major market; Japan's 2023 MHLW approval of allogeneic MSCs for diabetic foot ulcers is directly replicable in South Korea, Australia, and Indonesia under bilateral mutual recognition frameworks. China's biomanufacturing capacity is scaling rapidly: the 14th Five-Year Plan allocated CNY 15 Billion for bioprocessing modernisation, a portion directed at cell and gene therapy CDMOs. South Korea's Celltrion and Samsung Biologics are diversifying into cell therapy manufacturing. India's stem cell therapy market, while early-stage, is growing at 20%+ driven by haematological cancer incidence and expanding private hospital networks. Australia's TGA is actively reviewing allogeneic MSC applications for orthopaedic and wound care indications.

- Latin America Stem Cell Therapy Market

Latin America's stem cell therapy market is led by Brazil, which accounts for approximately 60% of regional revenue through its national bone marrow transplant network (REDOME) and emerging private cell therapy centres in Sao Paulo and Rio de Janeiro. Argentina has an active academic stem cell transplantation programme and has approved several MSC clinical trials. Colombia and Chile are early-stage markets with growing medical tourism infrastructure for stem cell procedures. The primary constraint across the region is cold chain logistics: maintaining -80°C temperature requirements for cryopreserved cell products across Brazil's vast logistics geography adds cost and failure risk that limits commercial scalability beyond major urban centres.

- The Middle East Stem Cell Therapy Market

The Middle East stem cell therapy market is developing at an accelerating pace, led by the GCC countries — particularly Saudi Arabia and the UAE. Saudi Arabia's Vision 2030 healthcare transformation has directed significant investment toward advanced therapy capabilities at King Faisal Specialist Hospital (KFSH) in Riyadh, which operates one of the largest HSCT programmes in the region. The UAE's Dubai Healthcare City and Cleveland Clinic Abu Dhabi are building cell therapy administration capabilities targeting medical tourism from South Asia and Africa. Israel is the region's most advanced stem cell technology market, with multiple clinical-stage companies including Gamida Cell and PolyPid operating in haematological and bone marrow applications. Turkey is an emerging market for MSC therapies, with a regulatory framework under revision. The primary challenge across GCC markets is localisation of GMP manufacturing — most therapeutic products are currently imported, creating supply chain fragility.

- Africa Stem Cell Therapy Market

Africa's stem cell therapy market is at an early commercial stage, but structural growth drivers are accumulating. South Africa holds the dominant regional position through Groote Schuur Hospital in Cape Town and Charlotte Maxeke Hospital in Johannesburg — the two primary HSCT centres on the continent. Egypt is developing stem cell capabilities through Cairo University's bone marrow transplantation unit, with government investment in regenerative medicine under the Egyptian Healthcare Authority's 2030 plan. Nigeria, Algeria, and Morocco have nascent programmes, primarily limited to haematopoietic transplantation at national referral hospitals. The continent's primary constraint is infrastructure: consistent electricity supply for cryopreservation, trained cell therapy nursing staff, and regulatory harmonisation across SADC and ECOWAS frameworks are all prerequisites for sustainable market growth that are not yet uniformly present.

Request Free SampleRequest Free SampleRequest Free Sample

Request Free SampleRequest Free SampleRequest Free Sample

Full Country Coverage

|

Region |

Countries Covered |

|

North America |

The U.S., Canada, Mexico |

|

Europe |

Germany, France, U.K., Italy, Spain, Russia, BENELUX, Sweden, Denmark, Poland, Austria, Rest of Europe |

|

Asia Pacific |

China, Japan, India, South Korea, Australia, Thailand, Indonesia, Vietnam, Malaysia, Philippines, Taiwan, Rest of Asia Pacific |

|

Latin America |

Brazil, Argentina, Colombia, Chile, Peru, Rest of Latin America |

|

The Middle East |

GCC (Saudi Arabia, UAE, Qatar, Kuwait, Bahrain, Oman), Israel, Turkey, Iran, Rest of Middle East |

|

Africa |

South Africa, Egypt, Nigeria, Algeria, Morocco, Rest of Africa |

**Country-level market sizing, historical data, and forecasts available for all geographies listed. Custom regional add-ons available — contact sales@zionmarketresearch.com

Request Free SampleRequest Free SampleRequest Free Sample

Request Free SampleRequest Free SampleRequest Free Sample

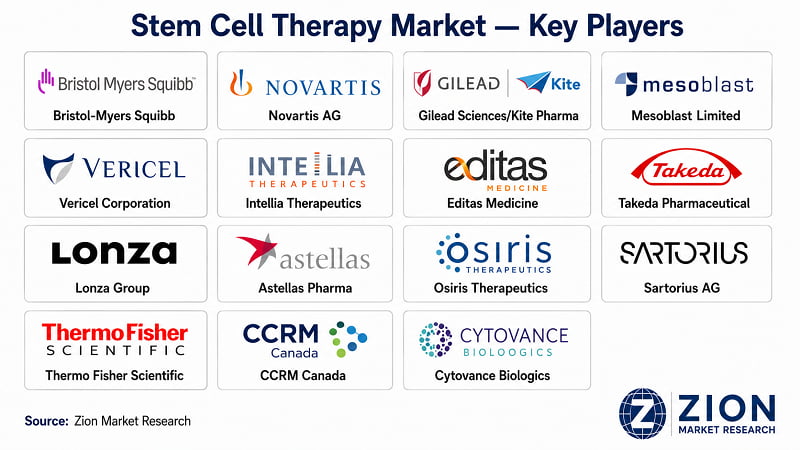

Stem Cell Therapy Market: Competitive Landscape

- The global stem cell therapy competitive landscape is moderately fragmented, with a clear two-tier structure. Large-cap pharmaceutical companies — primarily Bristol-Myers Squibb, Novartis, and Gilead Sciences/Kite Pharma — dominate the commercially approved CAR-T segment through FDA- and EMA-cleared products with established payer reimbursement. The second tier comprises specialised biotechs and platform companies (Mesoblast, Vericel, Intellia, Editas) that operate in distinct therapeutic niches or next-generation technology platforms. The dominant strategic pattern across the competitive set is pipeline diversification: leading players are simultaneously defending approved-product revenue while investing in next-generation allogeneic and gene-edited platforms to prevent revenue cliff as first-generation patents expire from 2028 onwards.

- Key players: Osiris Therapeutics (USA), Mesoblast Limited (Australia), Vericel Corporation (USA), Takeda Pharmaceutical (Japan), Novartis AG (Switzerland), Bristol-Myers Squibb (USA), Gilead Sciences/Kite Pharma (USA), Intellia Therapeutics (USA), Editas Medicine (USA), CCRM — Centre for Commercialization of Regenerative Medicine (Canada), Lonza Group (Switzerland), Cytovance Biologics (USA), Astellas Pharma (Japan), Sartorius AG (Germany), Thermo Fisher Scientific (USA).

|

Company |

HQ Country |

Primary Focus |

Key Strategy |

Notable Recent Action |

|

Bristol-Myers Squibb |

USA |

CAR-T (Oncology) |

Commercial scale-up & geographic expansion |

Expanded Breyanzi manufacturing, Leiden facility, 2024 |

|

Novartis AG |

Switzerland |

CAR-T, Gene Therapy |

RMAT pipeline & outcomes-based contracting |

Kymriah reimbursement expanded to EU, 2023 |

|

Gilead/Kite Pharma |

USA |

CAR-T (Haematology) |

Multi-indication approvals & payer coverage |

Yescarta approved for follicular lymphoma, FDA, 2022 |

|

Mesoblast Limited |

Australia |

Allogeneic MSC |

Regulatory resubmission & Asian partnerships |

Remestemcel-L CRL resubmission planned, 2024 |

|

Vericel Corporation |

USA |

Orthopaedic Cell Therapy |

Niche dominance & direct hospital sales |

MACI revenue USD 202 Mn FY2023 |

|

Intellia Therapeutics |

USA |

CRISPR/iPSC Allogeneic |

Gene-editing IP moats & allogeneic pipeline |

Allogeneic CAR-T IND filing targeted 2025 |

|

Editas Medicine |

USA |

CRISPR Cell Therapy |

Allogeneic platform development |

ASH 2023 preclinical allogeneic data presented |

|

Takeda Pharmaceutical |

Japan |

Allogeneic HSCT |

Asia Pacific manufacturing investment |

JPY 3.5 Bn iPSC co-investment, Osaka, 2023 |

|

Lonza Group |

Switzerland |

CDMO Infrastructure |

Cell therapy CDMO capacity expansion |

Houston cell therapy CDMO facility opened, 2023 |

|

Astellas Pharma |

Japan |

Regenerative Medicine |

iPSC platform partnerships |

Collaboration with Heartseed for iPSC cardio, 2023 |

|

Osiris Therapeutics |

USA |

MSC Wound & Orthopaedic |

Wound care commercialisation |

Grafix portfolio expansion, 2022–2023 |

|

Sartorius AG |

Germany |

Bioprocess Equipment |

Cell therapy bioreactor & analytics supply |

Stedim Biotech cell therapy tools expansion, 2023 |

|

Thermo Fisher Scientific |

USA |

Cell Processing Platform |

End-to-end cell therapy tools & logistics |

Continuum of Care cell therapy platform, 2023 |

|

CCRM Canada |

Canada |

Commercialisation Hub |

iPSC manufacturing infrastructure |

National iPSC facility expansion, Toronto, 2024 |

|

Cytovance Biologics |

USA |

CDMO Cell Therapy |

Contract manufacturing scale-up |

GMP capacity expansion for CAR-T clients, 2023 |

- Three strategic themes define the competitive set. First, every major CAR-T commercialist is simultaneously developing or partnering on allogeneic next-generation platforms — no large-cap player is defending autologous-only. Second, CDMOs have moved from peripheral suppliers to structural market participants: Lonza's cell therapy CDMO business grew 35% in 2023, positioning it as a de facto competitive enabler for smaller biotechs. Third, geographic diversification to Asia Pacific — through manufacturing investment, regulatory partnerships, or joint ventures — is a nearly universal strategy among players ranked in the top ten.

Request Free SampleRequest Free SampleRequest Free Sample

Request Free SampleRequest Free SampleRequest Free Sample

Recent Developments in the Stem Cell Therapy Market

Strategic activity in the global stem cell therapy sector accelerated through 2023–2024, with manufacturing capacity expansion, regulatory milestones, and platform investment dominating the news flow.

|

Date |

Company |

Type |

Description |

Market Impact |

|

Mar 2024 |

Bristol-Myers Squibb |

Capacity Expansion |

Expanded Breyanzi CAR-T manufacturing at Leiden, Netherlands facility targeting 40% throughput increase |

Strengthens EU commercial supply reliability for approved CAR-T |

|

Jan 2024 |

Mesoblast Limited |

Regulatory |

Received FDA Complete Response Letter for remestemcel-L in paediatric SR-aGvHD; resubmission planned H2 2024 |

Delays near-term U.S. revenue; resubmission maintains long-term market optionality |

|

Oct 2023 |

Japan MHLW |

Regulatory Approval |

Approved allogeneic adipose-derived MSCs for diabetic foot ulcers — first Asian Pacific approval for this indication |

Opens regulatory precedent for South Korea, Australia, and EU filings |

|

Sep 2023 |

Lonza Group |

Infrastructure |

Opened dedicated cell therapy CDMO facility in Houston, Texas with 12 GMP manufacturing suites |

Expands North America CDMO capacity; reduces developer manufacturing bottleneck |

|

Jun 2023 |

Takeda Pharmaceutical |

Investment |

Announced JPY 3.5 Billion co-investment with CCRM in iPSC manufacturing infrastructure, Osaka, Japan |

Largest single iPSC manufacturing commitment in Asia Pacific; validates platform commercially |

|

Apr 2023 |

Novartis AG |

Regulatory |

Kymriah reimbursement approved by German GKV for follicular lymphoma, expanding addressable European patient population |

Direct revenue impact in largest EU pharmaceutical market |

About Zion Market Research

Zion Market Research is an obligated company. We create futuristic, cutting-edge, informative reports ranging from industry reports, company reports to country reports. We provide our clients not only with market statistics unveiled by avowed private publishers and public organizations but also with vogue and newest industry reports along with pre-eminent and niche company profiles. Our database of market research reports comprises a wide variety of reports from cardinal industries. Our database is updated constantly in order to fulfil our clients' requirements for prompt and direct online access. Keeping in mind the client's needs, we have included expert insights on global industries, products, and market trends in this database.

Author:

Mr. Nilesh Patil

Zion Market Research

LinkedIn- www.linkedin.com/in/nilesh-patil-m-s-m-b-a-bba33067

Table Of Content

Methodology

FrequentlyAsked Questions

The Zion Market Research Stem Cell Therapy market report delivers 300+ pages of intelligence covering: global market sizing and nine-year forecasts (2026–2034); segmentation analysis across four dimensions (cell type, therapy type, application, end user); regional analysis for North America, Europe, Asia Pacific, Latin America, The Middle East, and Africa — each as a separate chapter with country-level data; competitive profiles of 15 leading companies; full DROC analysis; and a research methodology section. The report includes 110–140 data tables and 80–100 figures.

The global stem cell therapy market was valued at USD 12,840 Million in 2025, per Zion Market Research. It's forecast to reach USD 64,820 Million by 2034 at a 19.6% CAGR over the forecast period 2026–2034. This represents an absolute incremental value of USD 51,980 Million over nine years — one of the highest absolute growth opportunities in the biotechnology sector.

The Zion Market Research report segments the stem cell therapy market across four dimensions: By Cell Type (hematopoietic, mesenchymal, iPSC, neural, embryonic stem cells); By Therapy Type (allogeneic, autologous); By Application (oncology, musculoskeletal, cardiovascular, neurological, wounds & injuries); and By End User (hospitals & clinics, academic & research institutes, cell banks). Each segment includes historical data, base year sizing, and forecast to 2034.

The report provides country-level data across all 6 ZMR regions — analysed as separate regional chapters. North America: The U.S., Canada, Mexico. Europe: Germany, France, U.K., Italy, Spain, Russia, BENELUX, Sweden, Denmark, Poland, Austria, Rest of Europe. Asia Pacific: China, Japan, India, South Korea, Australia, Thailand, Indonesia, Vietnam, Malaysia, Philippines, Taiwan. Latin America: Brazil, Argentina, Colombia, Chile, Peru. The Middle East: GCC (Saudi Arabia, UAE, Qatar, Kuwait, Bahrain, Oman), Israel, Turkey, Iran. Africa: South Africa, Egypt, Nigeria, Algeria, Morocco. Middle East and Africa are always covered as separate regional analyses — never combined.

All Zion Market Research reports include 20% free customization at no additional cost. Customization options include: addition of specific countries or sub-regions not in the standard scope; custom segmentation breakdowns tailored to your business unit; competitive benchmarking of specific companies against your portfolio; extended forecast periods beyond 2034; and executive briefing sessions with a Zion Market Research analyst. Contact sales@zionmarketresearch.com or call +1 (302) 444-0166 to discuss requirements before purchase.

List of Contents

Stem Cell Therapy Industry PerspectiveStem Cell Therapy OverviewKey InsightsWhy Choose the Zion Market ResearchsStem Cell Therapy Market Report?Stem Cell Therapy Dynamics (Drivers, Restraints, Opportunities, Challenges)Stem Cell Therapy Report ScopeStem Cell Therapy SegmentationStem Cell Therapy Regional AnalysisFull Country CoverageStem Cell Therapy Competitive LandscapeRecent Developments in theMarketHappyClients